The impact of the Middle East conflict on the Spanish economy

The conflict in the Middle East has renewed inflationary pressures in Spain through higher energy and commodity prices, further weakening a growth outlook already strained by rising trade tensions. Domestic demand remains strong for now, but a prolonged closure of the Strait of Hormuz would push Europe closer to recession and inevitably also weigh on the Spanish economy.

Abstract: The conflict in the Persian Gulf has delivered a renewed supply-side shock to the Spanish economy at a time when growth remained relatively strong, unemployment was falling, and the effects of the tariff war were beginning to ease. Energy markets are the main transmission channel: following the sharp rise in oil and gas prices, the pass-through to fuel and food prices is already visible, while futures markets suggest elevated costs could persist well into 2027. Unlike the 2022 shock following Russia’s invasion of Ukraine, however, this episode is not being driven by excess demand. Household savings are more limited, and domestic consumption, while resilient, is not overheating, reducing the risk of a sustained inflationary spiral. Under the baseline scenario—in which the Strait of Hormuz gradually reopens before the summer—Funcas projects GDP growth of 2.2% in 2026, with inflation averaging 3.3% this year. Tourism flows redirected toward Spain as a perceived safe destination may partially offset weaker goods exports and softer private consumption. The more serious risk lies in a prolonged closure of the Strait of Hormuz. Under that scenario, inflation would rise to 4% and GDP growth would slow to 1.8% in 2026, while Europe would move close to recession in the second half of the year. More broadly, the succession of shocks since 2020 has significantly reduced Spain’s fiscal room for manoeuvre: although public debt has stabilised relative to GDP thanks to strong nominal growth, its trajectory would become more difficult to manage in the event of a deeper economic downturn.

Foreword

The Spanish economy, having weathered the trade turbulence sparked by the tariff war, is now facing a new stress test as a result of the conflict in the Middle East. The starting point is relatively favourable, with Spain having already recorded growth of 0.6% in the first quarter, a result that, within a robust growth cycle, does not yet reflect the impact of the geopolitical crisis.

The shock in oil and commodity prices unleashed by the onset of the conflict is trickling through to more recent indicators. Indeed, although the ceasefire reached between the U.S. and Iran on 7 April marked a change of scenario, bringing immediate relief for oil prices, tensions have resumed and continued to simmer in recent weeks. At the time of writing, passage through the Strait of Hormuz was heavily restricted, creating a bottleneck for the movement of oil, gas and other key commodities.

The purpose of this paper is to show how the conflict is affecting the Spanish economy and present our forecasts for the next two years on the basis of different assumptions, modelling a baseline scenario and a prolonged-conflict scenario.

Conflict transmission channels

The standstill in exports of oil, gas, fertiliser, chemicals and a wide range of minerals and parts produced in the Gulf states has thrown supply chains into disarray. Kerosene, for example, is running short in some regions, disrupting civil aviation.

Even if shipping through the Strait were to resume in the coming weeks, energy product prices would take time to come back down to pre-conflict levels as the war has caused damage to the production infrastructure throughout the region, curbing supply in the short term. The world’s largest gas field, shared by Qatar and Iran, has been one of the hardest hit by missile crossfire. The hostilities have also caused grave harm to major petrochemical complexes in the region and to one of the main oil pipelines. Port facilities have emerged as war targets and Kharg Island, the lifeline of Iranian crude exports, has been bombed.

In addition to destroying production capacity, the conflict has interrupted oil and gas pumping in the regions where exports must necessarily pass through the Persian Gulf, in the absence of alternative shipping routes. Resuming production will not only require new investments, it will also take time. Another factor expected to continue to exert pressure on international prices is the surplus demand that will foreseeably flood the market in order to replenish the strategic reserves depleted in recent weeks and perhaps even increase them in light of the prevailing uncertainty.

Elsewhere, we are looking at a lasting increase in shipping insurance costs, as the perceived risks for maritime safety will take time to dissipate, even if the ceasefire holds. If Iran were to levy a toll on freight passage through the Strait, that would imply an additional cost.

These repercussions, or hysteresis effects, are tangible in the forward energy markets, which are discounting Brent oil prices above pre-conflict levels for the months to come, albeit trending lower. The forecast gap narrows to 20% by the end of the year. Gas prices are expected to remain high for even longer: futures point to barely any movement in prices until next winter, i.e., 35% more expensive than at the end of February (according to the Mibgas futures market).

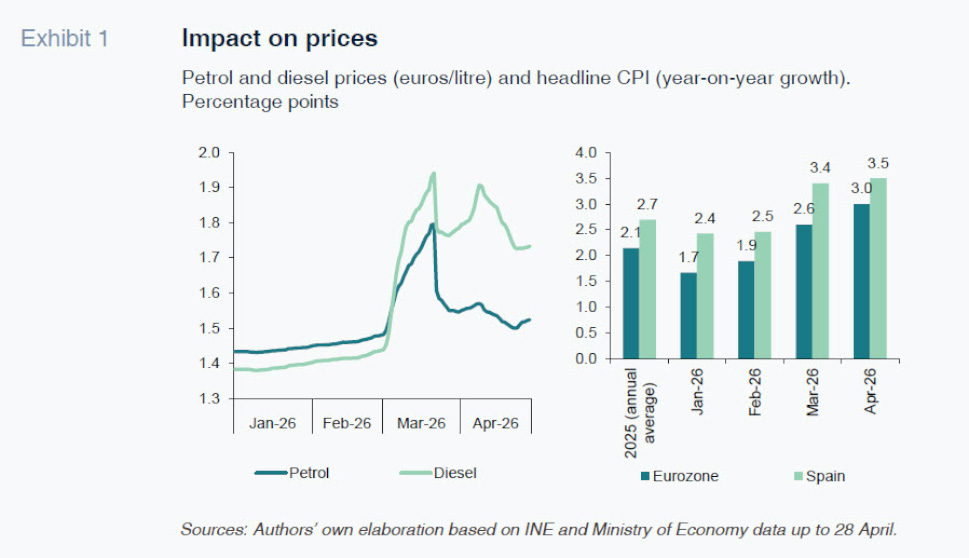

The increase in oil and gas prices has been passed through to end prices. Refilling the tank cost 4% more in Spain as of the end of April, even after the VAT and duty cuts, and diesel remains 20% above the average February reading, fully absorbing those cuts. Unlike what happened following the onset of the war in Ukraine, however, electricity bills have not moved significantly, even though the electricity pool price in April was 150% above average February levels.

Inflation has begun to reflect the energy shock, highlighting the so-called first-round effects. Harmonised Spanish CPI increased by nearly one percentage point in March to 3.4%, with the eurozone average increasing to 2.6% (Exhibit 1), with both rising again to 3.5% and 3%, respectively, in April. In the months to come, food could well take the baton from energy, due to the higher cost of transportation, fertilisers and other raw materials needed for agriculture.

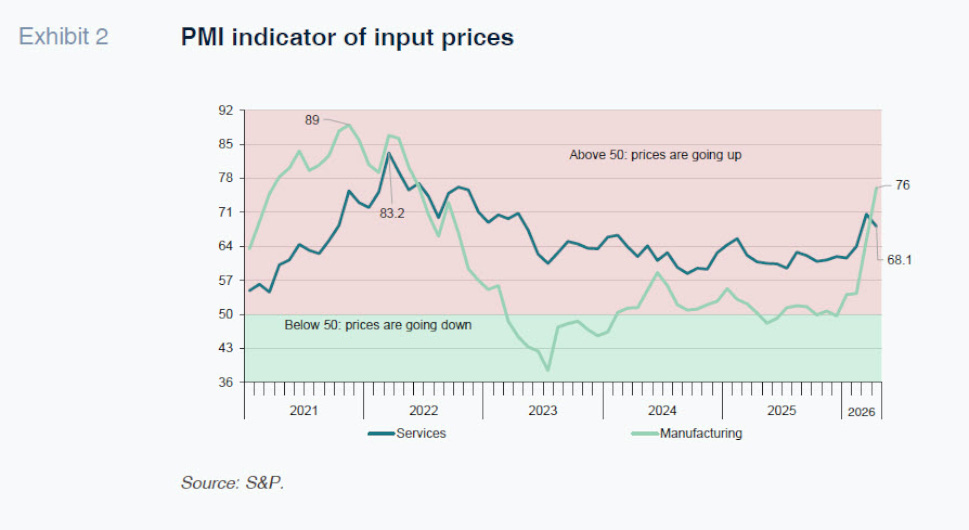

According to purchasing managers’ index (PMI), businesses are already reporting a sharp increase in input costs, as well as greater difficulty in obtaining them as a result of the freight transportation disruption caused by the conflict (Exhibit 2). The cost increase is being felt in both manufacturing and services. In the case of manufacturing, the PMI indicator of prices paid by enterprises climbed to levels not far off the peaks reached during the 2022 crisis triggered by the war in Ukraine. In services, the increase has been more moderate but is similarly worrying given service businesses’ greater propensity to pass cost increases through to end prices. That said, while we are therefore seeing inflationary pressures on the supply side, the extent to which they materialise will depend on how long the conflict lasts.

The trajectory in interest rates is consistent with this prognosis of a considerable —so far, manageable—, uptick in inflation. 12-month Euribor has been hovering at around 2.8% since mid-March, which is 0.6 points above pre-conflict levels, discounting three ECB rate increases. The yield on the 10-year Spanish bond, meanwhile, has registered a smaller increase, from around 3.2% in February to 3.5%.

As for the trend in economic activity since the war began, the few indicators available point to a downturn in the European economy but not a recession, at least for now. In Spain, the manufacturing PMI performed well in April, reaching one of its highest levels of the past six months. However, this result appears to have been driven in part by customer order front-loading amid concerns over potential supply chain disruptions. Meanwhile, the services PMI continued its sharp decline, falling to its lowest level in the last two years and dropping below the 50 threshold that signals lower output. The confidence and economic sentiment readings also registered dips, albeit moderate, with the exception of consumer confidence, which suffered a more notable decline. However, the number of social security contributors has continued to increase vigorously, without sending any signs, at least for now, of a weakening job market. All of which suggests that, so far, the impact of the Middle East crisis has been contained.

Baseline scenario for 2026-2027

Our forecasts are based on the assumption that energy prices will move in line with futures markets. This means that a barrel of Brent oil would still cost around 80 dollars at the end of the year, with gas prices at roughly 45 euros per MWh. Prices are projected to return to pre-conflict levels, i.e., around 70 dollars and 30 euros, respectively, towards the end of 2027. Other commodities such as fertilisers and polymers are expected to follow a similar path. Importantly, the assumption that the energy and commodity price shock will prove contained presupposes that the Strait of Hormuz will gradually reopen before the summer.

On the macroeconomic policy front, we assume two ECB interest rate hikes, increasing the deposit facility rate from 2% today to 2.5% in September, after which we are forecasting no additional movements. Fiscal policy reflects the measures taken in response to the war in Iran, some of which, including the energy tax relief, are assumed to be reversed in the autumn. Meanwhile, public support for investment will continue throughout the projection horizon, as the addendum simplifying the management of Next Generation funds spreads the execution of the programme over time, i.e. beyond the initial deadline of August 2026 (González Simón et al., 2026). The other budget metrics (non-energy taxes and current spending) are expected to trend in line with the budget carryover scenario that has been playing out for the last three years.

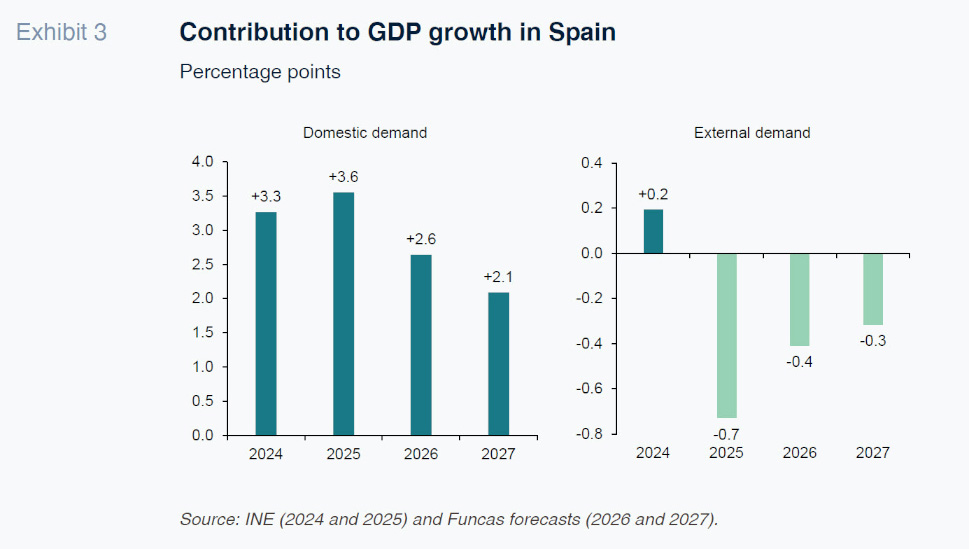

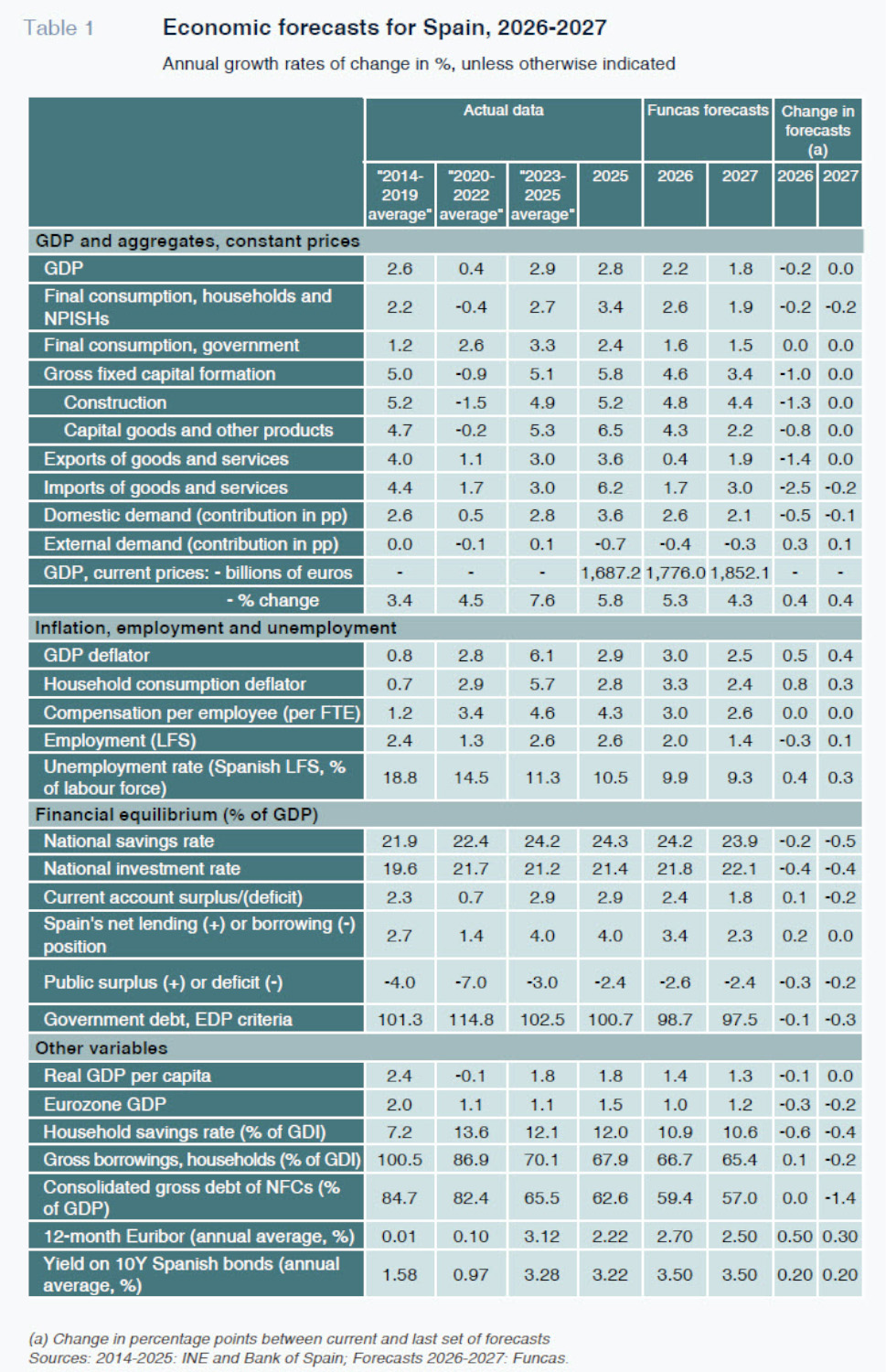

Framed by these assumptions, the Spanish economy is expected to continue to grow, albeit somewhat less vigorously. GDP growth is forecast at 2.2% this year, down 0.2 points from the last set of Funcas forecasts. The reduction is attributable to a loss of momentum in domestic demand, whose contribution to growth is now forecast at 2.6 points, down half a point from the last round of forecasts (Exhibit 3) (Torres et al., 2026). Private consumption is now expected to be less dynamic due to a loss of purchasing power on the heels of a fresh bout of inflation. Growth in investment is also expected to be slower due to the uncertainty implied by the conflict and supply chain disruption caused by the closure of the Strait of Hormuz.

Foreign trade is expected to detract from growth by 0.4 percentage points, which marks an improvement of 0.3 points compared to the February forecasts. Here, the improvement is explained by the redirection of tourism to safer destinations like Spain in response to the risks associated with travelling to the Middle East. Nevertheless, the sharp increase in the cost of air travel and flight cancellations already beginning to materialise could limit longer-distance travel, while foreseeably translating into lower average spending per visitor. The growth in the number of tourists should offset greater weakness in goods exports in the context of economic stagnation in Europe. Imports, meanwhile, are still expected to register strong growth, particularly imports from China.

In this baseline scenario, the Spanish economy is predicted to continue to grow above the European average in 2027, at 1.8%, unchanged with respect to the last set of Funcas forecasts. The growth cycle would be nurtured by domestic demand, in turn underpinned by population growth, construction and the remnant of European funds. External demand would continue to undermine GDP growth, as the complex international context drags on activity in the EU, the Spanish economy’s most important export market.

This growth pattern, coupled with higher import prices, is expected to erode the current account surplus, from 2.9% of GDP in 2025 to 1.8% in 2027. That surplus would nevertheless remain solid by historical standards and also in comparison with the other large European economies, where growth is expected to be more sluggish.

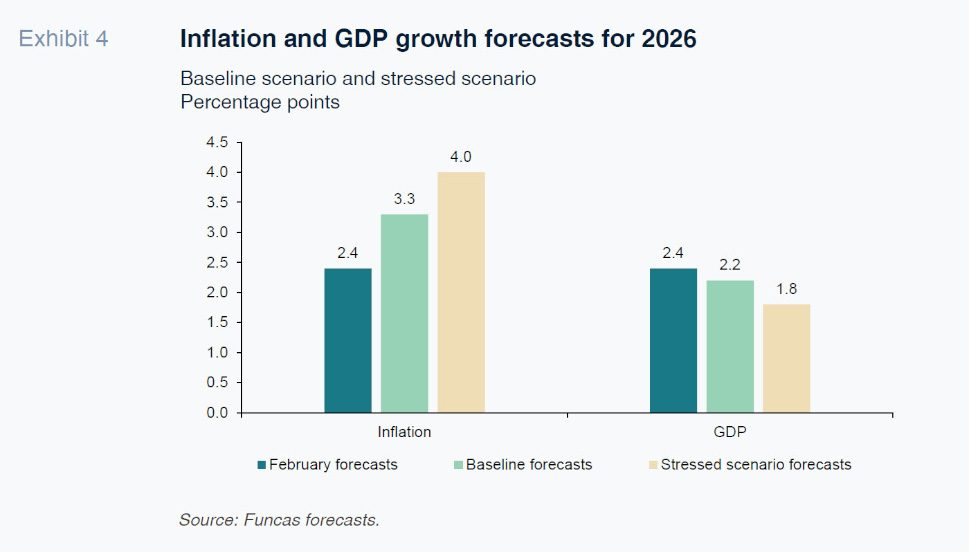

The inflation path will be altered by the Middle East conflict, even assuming a prompt peaceful resolution and a gradual reopening of the Strait of Hormuz before the summer, in line with the assumptions outlined above. This assessment is consistent with an inflation rate (CPI) of around 3.5% until the end of the year, which would translate into a rate of 3.3% for the year as a whole.

The slowdown in growth will in turn slow the downtrend in unemployment a little. Spain is expected to create nearly 650,000 jobs over the two years, which would imply an average annual unemployment rate of 9.3% in 2027, up 0.3 points from our February forecasts. Elsewhere, the legalisation on immigration will increase the labour force participation rate by injecting undocumented workers who are not currently looking for work (such a labour force expansion effect took place during a previous amnesty episode back in 2005).

The package of measures for mitigating the impact of the conflict in the Middle East will also halt progress in the correction of budget imbalances. The public deficit is now forecast to increase by 0.2 points to 2.6% and fall back slightly to 2.4% in 2027, as those measures are rolled back. At the end of that year, government debt is forecast at 97.5% of GDP, which is still a relatively high figure.

Prolonged-conflict scenario

Uncertainty continues to dominate the international climate, marked by geopolitical conflicts and the transition from a rules-based multilateral system to an asymmetric power-based order. The biggest risk at present relates to the situation in the Persian Gulf, whose impact on the supply of certain basic products is already beginning to be felt. If passage through the Strait of Hormuz remains closed for several months longer, the fuel shortage would lead to more pronounced increases in oil and gas prices and would hit manufacturing, firstly, in Asia, and, later, in the rest of the world, given the Asian nations’ position in the global value chains, with a much bigger impact on the global — and Spanish — economy than is contemplated in the baseline set of forecasts.

To simulate this risk, we modelled an alternative scenario in which oil prices remain at around 115 dollars per barrel all year long. In this stressed scenario, inflation would average 4% (+0.7pp compared to the baseline scenario) and GDP growth would slip to 1.8% (-0.4pp) (Exhibit 4). In this scenario, the Spanish economy would barely grow in the second half of the year and the European economy would verge on recession.

In addition to the risk of persistently stressed energy prices, it is possible that the perception of insecurity and uncertainty generated by the geopolitical turbulence could have a more lasting impact on precautionary savings and investment decisions at the global scale, translating into lower growth rates.

[1]

On the other hand, in this alternative scenario, and in line with the positive recent trend in hotel bookings, we would expect to see a bump in tourist flows to Spain as it is viewed as a safer, closer destination. However, this effect could be smaller than expected if offset by a general slump in global tourist flows on the back of higher flight prices or a desire among households to rein in spending out of precaution in light of the uncertainty or general inflation.

The role of fiscal policy in response to the succession of shocks

In sum, a relatively short conflict would have limited consequences for the Spanish economy. It looks unlikely that the first-round price effects, which are inevitable, will lead to a bout of inflation similar in magnitude to that unleashed four years ago, when the supply shock coincided with abundant demand, fuelled by the excess savings set aside by households during the pandemic. This time around, pressure via demand is weaker, even in a growing economy like Spain. By the same token, the growth momentum is expected to continue, albeit at a slower pace than was forecast before the onset of the war.

However, if the conflict were to drag into the summer, the consequences would be significant for both growth and inflation, particularly in Europe, which would very likely tip into recession.

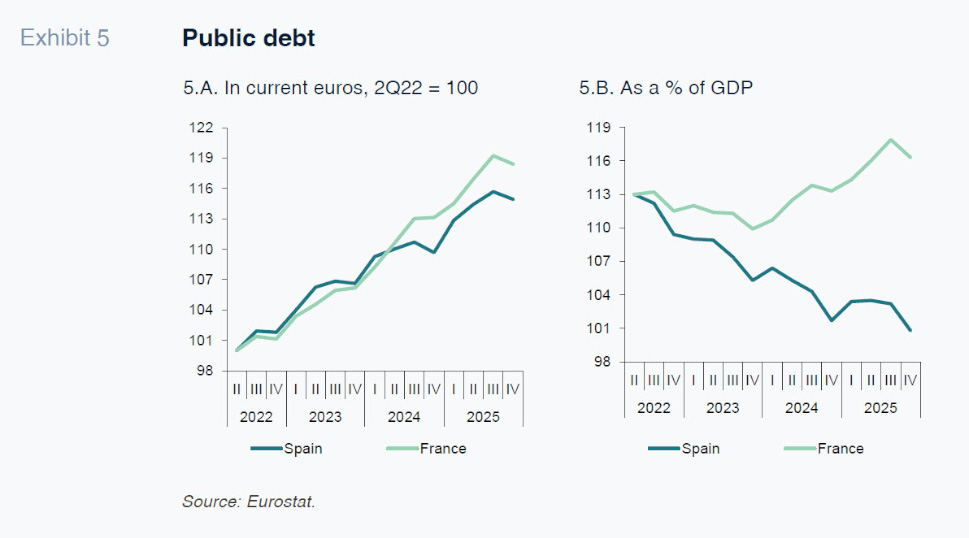

In general, the succession of shocks sustained in recent years has evidenced the importance of having room for budget manoeuvre so as to mitigate their effects. Here it is important to recall that Spanish public debt has been rising continuously in nominal terms, at a pace very similar to that of other countries like France. Meanwhile, the ratio of debt-to-GDP has come down, that is thanks to the considerable nominal growth enjoyed by the Spanish economy, which sets it apart from its northern neighbour (Exhibit 5).

That has kept Spain’s risk premium in check, below that of even France. In the event that a serious disruption were to trigger a significant downturn, however, the public deficit would shoot up, and the “denominator” effect would cease to work in Spain’s favour. The public debt ratio would head sharply north, leaving Spain exposed to new risks, which would not only impede the ability to implement fiscal relief measures but would oblige it to make deep cuts at exactly the most inopportune time.

Notes

Private investment is, already, the Spanish economy’s weak link (see Torres, 2026).

References

GONZÁLEZ SIMÓN, M. Á., LÓPEZ, G., y RODRÍGUEZ, B. (2026).

El impacto de los fondos Next Generation en la economía española (versión preliminar). Funcas.

https://www.funcas.es/libro/el-impacto-de-los-fondos-nextgeneration-en-la-economia-espanola-version-preliminar/TORRES. R. (2026). Private investment: The weak link in Spain’s expansionary phase.

SEFO, 15(1).

https://www.sefofuncas.com/Investment-and-productivity-in-an-era-of-change-and-uncertainty/Private-investment-The-weak-link-in-Spains-expansionary-phaseTORRES, R., and FERNÁNDEZ, M. J. (2026). Geopolitical risks and the outlook for Spain’s growth cycle.

SEFO, 15(2).

https://www.funcas.es/articulos/geopolitical-risks-and-the-outlook-for-spainsgrowth-cycle/

Raymond Torres, María Jesús Fernández and Fernando Gómez Díaz. Funcas.