The dollar′s uncertain hegemony: Headed towards a new equilibrium?

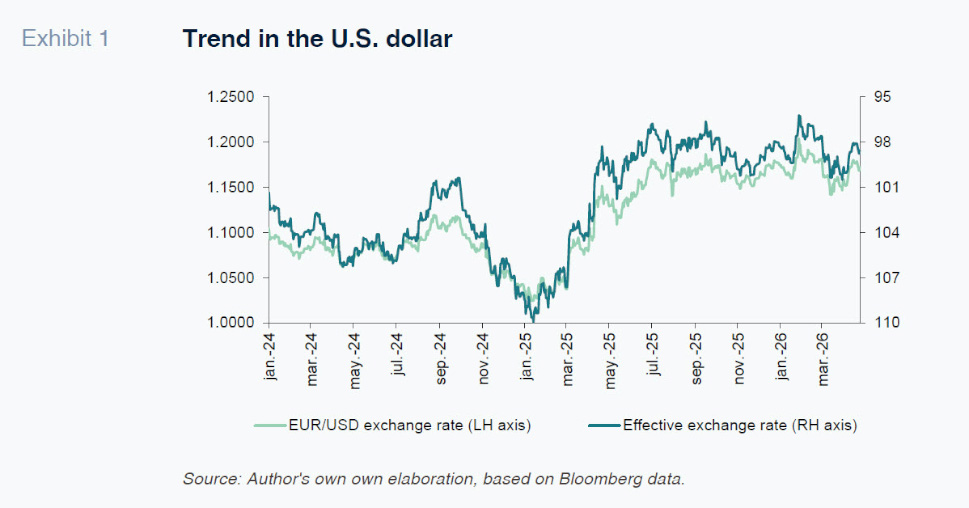

The dollar has lost more than 11% of its effective exchange rate value since early 2025, defying the appreciation that would normally accompany higher tariffs. The evolution reflects not just policy uncertainty but a deeper recalibration of the dollar′s role as the anchor of the international financial system.

Abstract: For decades, the dollar′s dominance rested on a set of durable foundations: deep capital markets, credible monetary institutions, and the implicit guarantee that the U.S. would not weaponize its currency against allies. That compact is fraying, as the Trump administration has recast the dollar as an instrument of geopolitical leverage. The cost of doing so is already visible in currency markets: the greenback weakened through 2025 even as tariff hikes should, by conventional logic, have pushed it higher. In response, central banks and sovereign wealth funds have begun accelerating reserve diversification and driving gold to historic highs as an alternative reserve asset. The dollar′s structural position, anchoring 56% of global reserves and the bulk of international trade finance, remains intact, and the “there is no alternative” (TINA) argument still holds in the short run. However, the incentive to reduce dollar dependence grows with each new sanction deployed and each threat of financial exclusion. Whether the current weakness reflects a transient risk premium or the early phase of a more durable erosion is a crucial uncertainty.

The dollar: A new economic policy tool?

The accession to power of the new U.S. administration has implied a radical shift in foreign policy of the world′s leading power and, along with it, in diplomatic relations with the U.S.′s traditional allies. In parallel, it is also affecting economic policy, which is striving to adapt the role played by the U.S. as anchor and equilibrium of the global economy in recent decades for new geopolitical paradigms (Lighthizer, 2026).

The U.S. administration’s new security strategy starts from the following premise: competition between the major powers has become structural and the economy in general, and the international financial system in particular, is a core instrument of national power. Seen through this lens, the dollar ceases to be merely a financial asset or international currency, emerging as another national security tool, playing a role similar to that of tariffs. This could have profound implications for its role as reserve currency, payment mechanism and store of value.

In recent decades, the strength of the dollar has relied on deep financial markets, low-risk, abundant and liquid assets, the independence and credibility of the Federal Reserve since the days of Volcker and dominance of the international payment systems (cards, SWIFT, etc.). All of which under the umbrella created by the existence of mutual trust among traditional allies, namely the certainty that the U.S. would provide liquidity in dollars if needed and would not use sanctions as a coercive tool.

However, one eye-opening trait of the new American strategy is the potential use of the dollar as a tool of geoeconomic power. Applying economic sanctions, blocking access to the dollar payment systems and freezing assets have emerged as staple tools of American foreign policy rather than mechanisms to be used only in extreme circumstances. In the short term, this new strategy may reinforce the role of the greenback, as there is no alternative capable of replacing the financial infrastructure dominated by the U.S. However, it could lead countries from the global south (as well as middle powers) to perceive greater risk associated with holding reserves in dollars, which would trigger a search for ways to diversity in terms of both currency reserves and dependence on the payment systems operated by U.S. companies. At the end of the day, it would not look like a smart idea to provide the users of your star product with incentives to look for alternatives.

In sum, the pre-eminence of the dollar is not in imminent danger, but its use as an economic policy instrument will imply decreasing returns: each new sanction is effective in the short term but increases the incentive to taper reliance on the dollar in the long term. Therefore, geopolitical factors stand to have a bigger medium-term impact on a shift in the role played by the dollar in recent decades. Against this backdrop, the question is whether such changes are already tangible in the dollar′s trading performance.

A year of changes in the currency markets

Since October 2024, when the polls began to discount victory for Donald Trump in the presidential elections, the trend in the dollar has reflecting the ups and downs in investor sentiment in response to the dysfunctional U.S. economic policy roadmap. More specifically, in just over 12 months, we have witnessed the dollar navigate four phases.

Phase 1: Intense initial appreciation of the U.S. currency between October 2024 and February 2025 (gains of 8% against the euro and in the effective exchange rate), shaped by initial expectations that liberalisation and fiscal expansion policies (tax cuts) would shore up economic growth and business profits, offsetting the adverse effects of the new administration’s tariff and immigration policies. That initial “Trump trade” reflected investors’ bet on a strong dollar.

Phase 2: Sharp depreciation from the end of the first quarter of 2025 until the summer (11.2% in the case of the effective exchange rate and nearly 13% against the euro) as the U.S. administration tightened its foreign policy, announced higher trade barriers than investors had initially priced in and, above all, increased uncertainty around the use of tariffs as a geopolitical bargaining chip. In parallel, fears grew that the exchange rate could be used as yet another coercive tool in negotiations with other countries, creating the risk of a shift in the traditional defence of a “strong dollar” by all preceding U.S. administrations, regardless of political affiliation. Those fears were fuelled by the positions taken by some of the prominent members of the new economic team (such as Stephen Miran

[1]) in favour of using the dollar to achieve domestic strategic targets (manufacturing, employment, tax receipts), including the potential use of unilateral and politically sensitive pressure measures (Miran, 2024).

Phase 3: Stabilisation of the dollar between the summer of 2025 and February 2026, following the negotiation of tariff agreements with America’s most important trade partners, although uncertainty around U.S. economic policy increased somewhat, particularly after the appointment of Kevin Warsh as a candidate for Fed Chairman.

Phase 4: Following the onset of the war in the Persian Gulf on 28 February 2026, the dollar appreciated during the first few weeks of the conflict, gaining almost 4% against the euro; however, the dollar gave back those gains after the U.S. administration declared a ceasefire mid-March, trading back at the levels observed prior to the start of the war. Therefore, in a context of significantly heightened uncertainty, the traditional role of the dollar as a safe haven asset has been less pronounced than in previous episodes of increased risk and volatility.

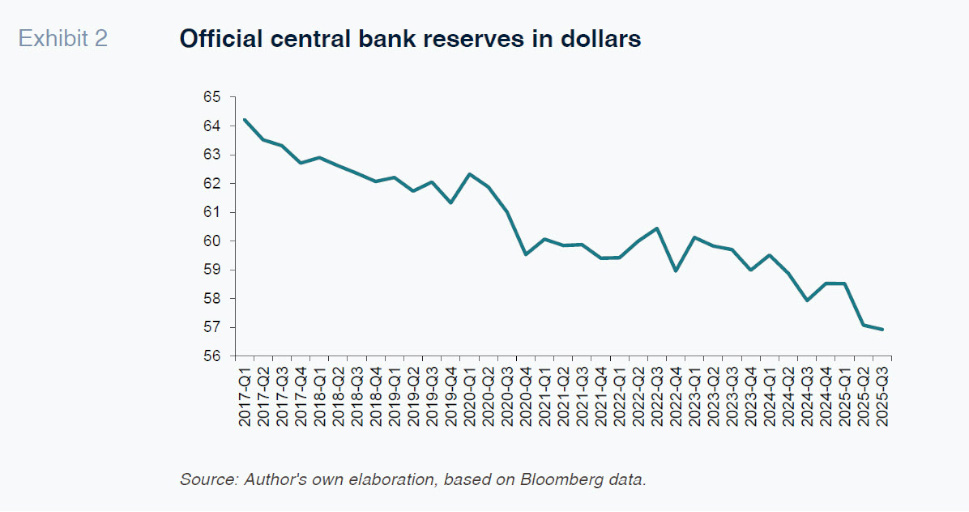

This is borne out by an upward trend in dollar position hedging by the major international fund managers

[2] and continuation of the reserve currency diversification process by central banks around the world (Exhibit 2), coupled with a reduction in dollar holdings across the major sovereign funds of countries affected by American foreign policy noise (

e.g., Greenland). In short, the sudden change in direction in the greenback’s evolution since the first quarter of 2025 (with the exception of the first fortnight of the war) is attributable to structural drivers related to both changes in the geopolitical order, with the global south looking to reduce dependence on the U.S., and circumstantial factors associated with heightened uncertainty about the tone of U.S. economic policy.

The loss of dollar value in 2025 is more significant considering that according to conventional theory, the greenback should have appreciated on the back of the tariff hikes. Traditionally, the currency of the country that raises trade barriers tends to increase in value in real terms. As imports become more expensive, domestic demand for foreign products decreases, reducing the need to purchase foreign currency to import them. This currency appreciation acts as an adjustment mechanism that neutralises much of the expected effect of the higher tariffs on foreign trade. However, this has not been the case with the dollar since the first quarter of 2025: not only has it not appreciated in real terms, it has lost value against the majority of other currencies.

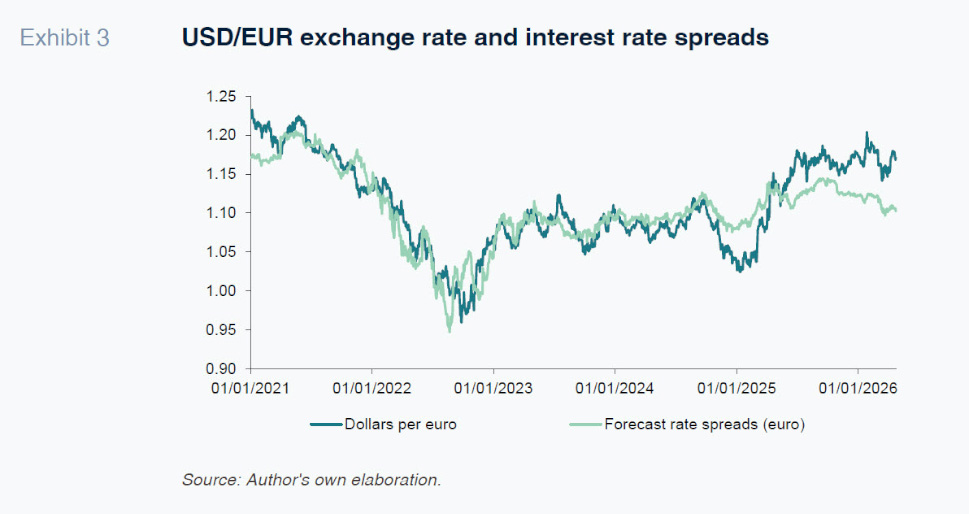

Another indication of the downturn in sentiment towards the greenback is the gap opened since last April between the trend in the dollar against the euro (depreciation) and the trajectory predicted by the interest rate spreads between the two monetary regions (Exhibit 3).

[3] The decoupling since that turning point amounts to nearly 10%, evidencing investor concern about the tone of U.S. economic policy, in addition to improved sentiment towards Europe (relative institutional quality, outlook for more dynamic growth on the back of fiscal expansion in Germany and higher spending on defence,

etc.).

Lastly, it is worth noting that the correlation between the dollar and commodities markets has also changed since Donald Trump came to power, albeit in this instance revisiting the traditional negative correlation which had inverted from 2020-2021, when the U.S. switched from being a net importer of oil to a net exporter. The return to pre-pandemic patterns largely reflects a strengthening of the negative correlation between the dollar and precious metals, particularly gold. Gold has become increasingly attractive both as a safe-haven asset for investors and as a reserve asset for central banks, reinforcing its role as a natural hedge against concerns over the performance of the dollar.

The traditional negative correlation between commodity prices and the value of the dollar is explained by the fact that most commodities are priced in dollars,

[4] so that dollar weakness lowers the cost of those products for non-U.S. buyers, increasing demand and pushing up prices. However, on this occasion, the movement has been more intense, because some portfolios are beginning to reflect the “debasement trade” and, by extension, a loss of confidence in fiat currencies as a result of trade tensions and imbalanced macroeconomic policies.

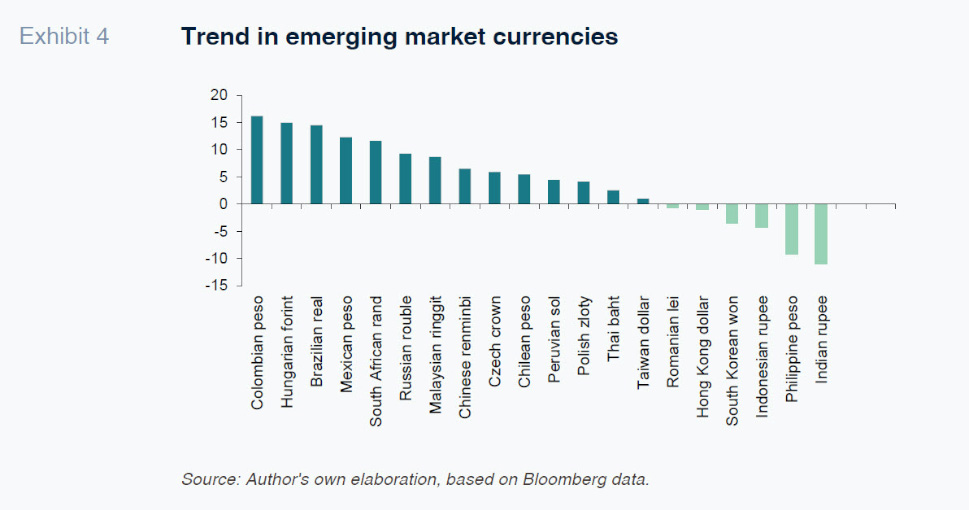

The winners in this scenario of concerns about the dollar’s performance and newfound negative correlation with commodity prices have been the emerging market currencies, particularly the commodities-producing economies. This is also sketching out a new and more fragmented global order in which the 10 largest emerging economies already account for over 50% of global GDP.

[5]

In short, during the last 12 months, the dollar has weakened by more than would be expected in light of macroeconomic fundamentals or interest rate expectations, evidencing a degree of international investor concern about the role it could play in the future. Dollar weakness is a true reflection of a disruptive economic policy without a clear objective, particularly with respect to trade policy, with average effective U.S. tariffs currently at their highest levels since World War II.

If the question is whether we are likely to see an accelerating decline in the dollar’s pre-eminence in the near term, the answer is no: the greenback continues to account for 56% of international currency reserves (followed by the euro at 21% and the yen at 6%); 45% of daily trading volumes in the currency markets (14% in euros and 9% in yen);

[6] and is the currency of denomination of 53% of international loans (23%, the euro). There is no currency capable of challenging its role as the benchmark currency of global trade and finance in the short term. Recall that previous benchmark currencies (pound sterling or Spanish

real) only lost their dominance after wars or debt crises (Rogoff, 2025). However, what we may end up seeing is a rebalancing, evidencing the global south’s efforts to reduce dependence on the dollar and the ambitions of the middle powers to gain financial autonomy.

Conclusions

The trend in the dollar in recent months reflects a change of attitude among global investors towards the greenback. Underpinning that performance, unusual for a country that has raised tariffs substantially in recent months, lie investor concerns about the tone of American economic policy and, underneath that, uncertainty around the new administration′s strategic vision for its currency. The upshot is that some of the long-standing correlations in the financial markets are decoupling, reflecting doubts about the future role of the greenback that are translating into increased diversification of global investment portfolios. In parallel, central banks around the world are fine-tuning their balance sheets in response to this emerging multi-polar world.

As a result, the future of the dollar in the face of geopolitical tensions has emerged as a key topic of today′s economic agenda. In the near term, the TINA argument is the most robust line of reasoning. However, the attacks on the credibility of U.S. institutions, widening fiscal imbalances and the suspicion that the dollar could be used as a bargaining tool within U.S. economic policy could prove a cocktail that ends up harming the dollar.

The question is whether we are looking at a transient trend — an increase in the dollar risk premium tied to the instability and noise being created by the Trump administration′s economic policy — or, to the contrary, we are at the beginning of a more meaningful shift attributable to structural vulnerabilities in the U.S. caused by a combination of institutional fragility, discretionary fiscal policy and political interference at the central bank. Ultimately, monetary and exchange rate credibility tends to take a long time to build but can be lost very swiftly. And even the benchmark currency could get caught up in that asymmetry. As Kenneth Rogoff said, the dollar will probably continue to dominate for some time (he describes its situation as a “late middle age”) with the adjustment taking place gradually at the beginning and then more abruptly. The problem is that in that transition we could see a sharp increase in global instability, reflecting the relevance of the old adage: “The dollar is our currency, but it is your problem”.

[7]

Notes

Chair of the Council of Economic Advisers (CEA) between March 2025 and February 2026 and member of the Federal Reserve Board of Governors since September 2025.

Before the distortion of portfolio asset allocations caused by the war in Iran, global fund manager surveys indicated that nearly 30% were overweight European assets in their portfolios relative to neutral levels (9% in the autumn of 2025).

We use the real 2Y OIS swap rate (i.e., subtracting the 2Y inflation swap).

The Bretton Woods (1944) Agreements laid the foundations for the generalised use of the dollar in commodity trading. Despite the fact that the collapse of Bretton Woods (1971-1973) ended dollar-gold convertibility, the denomination of all other commodities (oil, metals and agricultural commodities) has continued, underpinned by the depth of the financial markets in dollars, liquidity and dominant role of the U.S. in international trade.

Financial Times. (11 February 2026). Emerging economies shine despite US volatility.

According to the BIS, of the 7.5 trillion daily trades, the U.S. dollar is involved on one or other side of the trade 88% of the time.

A phrase attributed to John Connally, U.S. Treasury Secretary under President Richard Nixon.

References

FURCERI, D., HANNAN, S. A., JONATHAN, H., OSTRY, J. D., ROSE, A. K. (2018). Macroeconomic consequences of tariffs.

NBER Working Paper, 25402.

https://www.nber.org/papers/w25402LIGHTHIZER, R. E. (2026). The new trade order. Restoring balance to a broken global economy.

Foreign Affairs , 105(3).

https://www.foreignaffairs.com/united-states/new-trade-order-robert-lighthizerMIRAN, S. (2024).

A User’s Guide to Restructuring the Global Trading System. Hudson Bay Capital.

https://www.hudsonbaycapital.com/documents/FG/hudsonbay/research/638199_

A_Users_Guide_to_Restructuring_the_Global_Trading_System.pdfROGOFF, F. (2025).

Our Dollar, Your Problem: An Insider’s View of Seven Turbulent Decades of Global Finance, and the Road Ahead. Yale University Press.

José Ramón Díez Guijarro. CUNEF