Spanish economic forecasts panel: May 2026*

Funcas Economic Trends and Statistics Department

Growth in 2026

Consensus 2026 GDP growth cut 0.1pp to 2.2%

Spanish GDP increased by 0.6% in 1Q26, which is 0.1pp better than the most recent consensus forecast. Domestic demand contributed 0.4pp, driven above all by private consumption, whereas investment slowed. Foreign demand contributed 0.2pp, with the drop in imports exceeding the correction in exports.

For the rest of the year, the analysts expected quarterly growth to slow to 0.4% (Table 2). That yields a GDP growth projection for 2026 as a whole of 2.2%, with domestic demand contributing 2.6pp and foreign trade detracting 0.4pp (Table 1).

Compared to the last survey, the analysts now see significant downside risks. Most of them think there is a higher probability that growth will fall short of their forecasts, with just one seeing upside risks.

The uncertainty derived from the conflict in the Middle East has increased variability in the assumptions used by the analysts to draw up their forecasts, particularly with respect to where they think oil prices may be headed. On average, they are assuming that a barrel of Brent will cost around 103 dollars in June, 82 dollars in December and around 74 dollars in 2027.

Growth in 2027

2027 GDP growth forecast unchanged at 2%

The consensus forecast for GDP growth in 2027 is unchanged at 2%. That is higher than the growth forecast by the Bank of Spain and other international organisations such as the OECD or IMF (Table 1).

The slowdown with respect to 2026 would come from domestic demand, whose contribution would slow to 2.1pp (down 0.1pp from the last consensus forecast), with foreign demand detracting 0.1pp. As for the quarterly profile, the analysts are looking for quarterly growth of around 0.5% (Table 2).

Inflation

Significant upward revision to inflation forecasts due to the Gulf conflict

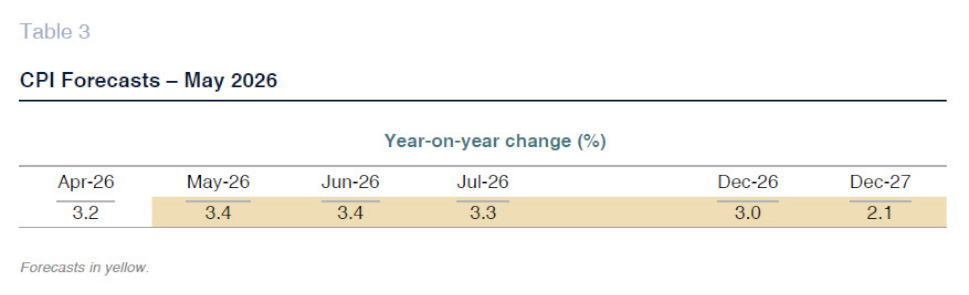

Following the onset of the Gulf conflict, headline inflation increased to 3.4% in March, falling back slightly to 3.2% in April. Core inflation has moved between 2.6% and 2.8% during the first four months of the year.

The consensus forecast for the average rate this year is 3.1% for headline inflation and 2.7% for core inflation, up 0.5pp and 0.2pp from the last set of forecasts, respectively. For 2027, the consensus forecasts for the headline and core rates are 2.3% and 2.4%, respectively, both of which 0.2pp higher than in the previous consensus. The year-on-year rates of change in December of this year and next are currently forecast at 3% and 2.1%, respectively (Tables 1 and 3).

Labor market

Unemployment estimated at around 10% in 2026

According to the labour force survey, employment increased by 0.4% in the first quarter, adjusting for seasonal effects, marking slight easing from the quarterly growth observed in 2025 (with the exception of the third quarter). The unemployment rate was 10.8%, down 0.6pp year-on-year. Social Security contributors also registered weaker growth in the first quarter due to poor performances in January and February, shaped by weather conditions. However, job creation accelerated in March and April, returning to the average month-on-month rates observed throughout 2025.

The consensus forecasts for growth in employment in 2026 and 2027 are unchanged at 1.9% and 1.5%, respectively. As a result, the unemployment rate is expected to come in at 10% in 2026 (up 0.1pp from the last set of forecasts) and drop another 0.4pp in 2027 to 9.6% (unchanged). (Table 1).

Productivity and unit labour costs (ULCs), calculated on the basis of the forecasts for growth in GDP, employee compensation and employment (as per LFS), are expected to register growth of 0.3% and 3%, respectively. For 2027, additional growth of 0.5% and 2.5% is expected.

Balance of payments

Current account surplus expected to decline

According to the revised figures, the current account surplus amounted to 49.3 billion euros in 2025, which is the second best figure on record in nominal terms and one of the best relative to GDP, at 2.9%, with higher surpluses only ever recorded in 2016 and 2024. In the first two months of 2026, the trade deficit improved year-on-year, while the deficit in the primary and secondary income accounts widened, so that the current account surplus was almost unchanged compared to last year.

The consensus forecast is for a current account surplus equivalent to 2.2% of GDP in 2026 and 2% in 2027, down 0.2pp from the last set of forecasts in both instances (Table 1).

Public deficit

The public deficit could increase this year

Spain recorded a general government deficit of 2.4% of GDP in 2025 (excluding expenditure related with the deadly flash floods, the deficit was 2.2%), compared to 3.2% in 2024. In the first two months of 2026, the balances recorded by the Social Security and regional governments improved, while the state government reported a similar deficit. However, the early months of the year are scantly representative.

The analysts expect the public deficit to increase this year to 2.5% (up 0.1pp from the last set of forecasts), going on to fall back to 2.3% (down 0.1pp) in 2027 (Table 1).

International context

Deteriorating international climate

The uncertainty around the conflict in the Middle East continues to cloud the global economic outlook. At the time of writing, the Strait of Hormuz remained blockaded, choking the global supply of oil, gas and other commodities, whose prices have shot up from the levels observed prior to the flare-up. The futures markets point to a more lasting disruption than anticipated at the time of our last report, with prices remaining high until at least the end of the year. In addition, the International Energy Agency has warned that there is a risk that oil reserves could be depleted if the shipping restrictions through the Persian Gulf continue beyond the summer.

In this context, the IMF, in its April round, cut its forecast for global growth to 3.1%, down 0.2pp from its January projections. Importantly, the IMF considers that, if it were not for the war in Iran, the growth forecast would have been upgraded due to the catalytic impact of AI on investment, among other factors.

The European Union, which was already starting from a situation of relative weakness, is one of the regions most exposed to the oil shock. This is already visible in the behaviour of the purchasing managers’ index (PMI) of the eurozone, which dropped below the 50-mark in both April and May.

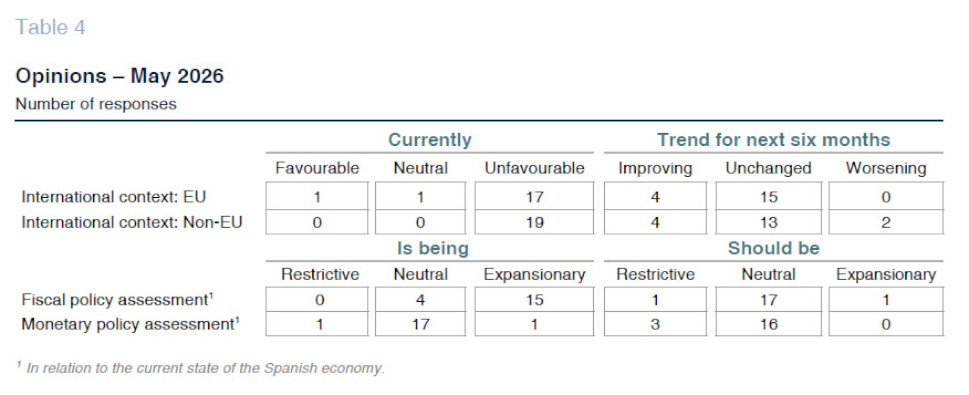

In line with these trends, the analysts have become more pessimistic about the international outlook (Table 4). They all believe that the global context is unfavourable and the majority thinks that the current situation will continue or even worsen in the short run. Their assessments with respect to the situation in the EU and the outlook for the region in the near term are similarly pessimistic.

Interest rates

The ECB is expected to raise rates by a quarter of a point in June

The spike in consumer price inflation triggered by the run-up in energy and other commodity prices is complicating the task of monetary policy, in light of the difficulty in assessing the risk of inflation expectations decoupling in such an uncertain environment. For now, the main central banks have opted to leave their interest rates unchanged, while expressing their readiness to react if they detect signs that the inflationary episode could prove persistent.

Markets believe that rate adjustments are inevitable. Euribor is trading at around 2.8%, up from 2.2% before the Gulf war (and close to 30 basis points above the levels observed at the time of the last Panel in March). Likewise, the yield on the 10-year Spanish bond has increased from 3% in February to close to 3.6% at present (up 0.1pp versus March). The analysts expect the yield to continue to trade at current levels throughout most of the year (Table 2), i.e., above the last consensus forecast.

Similarly, the consensus forecast is for an increase in the ECB’s deposit facility rate from 2% currently to 2.25% next month. After that, the European monetary authority is expected not to tighten rates again throughout the end of 2027 (Table 2).

Currency market

Euro appreciation against the dollar over the projection horizon

Currency markets have moved in tandem with the news flow around the conflict in the Middle East. Reflecting its safe haven status, the dollar has tended to appreciate since the start of the attacks on Iran, albeit oscillating significantly. Today, the dollar is trading at around 1.16 per euro, compared to 1.18 in February. However, the consensus forecast is that between now and the end of 2027, the euro will regain the ground lost during the past two months (Table 2).

Fiscal and monetary policy considerations

Fiscal policy should be less expansionary

The analysts believe that the Spanish economic cycle is sufficiently robust as to not need additional stimulus via fiscal policy. According to a majority of analysts, the budget remains expansionary when it should be neutral, meaning it should not provide additional stimulus. As for monetary policy, the perception is one of a better fit with the cycle: the consensus is that monetary policy is neutral, which is what the Spanish economy currently requires (Table 4).

*

The Spanish Economic Forecast Panel is a survey conducted by Funcas among the 19 research services listed in Table 1. The survey, which dates back to 1999, is published every two months, in January, March, May, July, September and November. The responses to this survey generate “consensus” forecasts, which are calculated as the arithmetic mean of the 19 individual forecasts. For comparative purposes, albeit not part of the consensus, the forecasts of the Spanish government, AIReF, Bank of Spain and leading international organisations are also presented.