Private credit and the relocation of risk in modern finance

Private credit has expanded rapidly into segments vacated by banks, emerging as a central pillar of corporate financing within the non-bank ecosystem. Its continued growth, alongside persistent linkages to the banking system, is reshaping the distribution of risk and raising questions about how losses would be absorbed under stress.

Abstract: The rapid expansion of non-bank financial intermediation since 2008 has reshaped the global credit landscape, with private credit growing from roughly $400 billion in 2020 to nearly $1.8 trillion today. This segment now concentrates many of the tensions shaping the current cycle: opaque valuations, liquidity mismatches, continued reliance on bank funding, and rising exposure to sectors facing refinancing pressure and technological disruption. Recent stress points in U.S. evergreen business development companies (BDCs)—publicly listed vehicles that provide financing to mid-sized firms—and the acceleration of synthetic risk transfers (SRTs)—transactions through which banks transfer credit risk to investors without selling the underlying loans—in Europe illustrate how these vulnerabilities are manifesting. In the United States, liquidity promises attached to illiquid loans have been tested by valuation gaps and rising redemption pressure. In Europe, banks have used SRTs to release regulatory capital while often retaining the underlying exposures, raising questions about how much risk is actually being transferred and how incentives to monitor borrowers evolve after the transfer. The picture is not one of imminent systemic crisis, but of mounting friction within an increasingly complex financial architecture. Credit risk has shifted into structures with different transparency, governance, and loss-absorption dynamics, while remaining closely interconnected with the banking system. Understanding where that risk ultimately resides, and how it would behave under stress, has become central to assessing financial stability in this cycle.

From the banking system to the NBFI ecosystem

The NBFI (Non-bank financial intermediation) ecosystem is a mixed bag of entities: insurance companies, pension funds, money market funds, hedge funds, structured vehicles, etc. These different moving parts do not all imply the same levels of risk and many simply offer an alternative channel for funnelling savings into the real economy. However, the scale and opacity of the universe as a whole have forced the supervisor to classify it. Acharya, Cetorelli and Tuckman, in a paper taken up by the G30, distinguish between three types of entities depending on how they engage with the banks: the parallel view, where entities offer services the banks do not provide; the substitution view, where entities compete directly with the traditional banks; and the transformation view, where entities are reorganising the banking business without migrating away from it altogether. Private credit belongs to the third category: private lenders lend to companies that used to finance themselves using bank loans but continue to rely on those same banks for credit facilities and/or repos (back leverage).

This is why private credit has become a focal point of concern within the non-bank financial intermediation (NBFI) system. Not because it poses an immediate systemic risk, but because it concentrates many of the features that preoccupy supervisors: rapid growth (from $400 billion in 2020 to nearly $1.8 trillion today), opaque valuations, a mismatch between illiquid assets and investor liquidity expectations, continued reliance on bank funding, and concentrated exposure to sectors undergoing disruption from artificial intelligence. A recent development is exacerbating those concerns: private credit has made its way into the retail investor segment through evergreen vehicles and their distribution through private banking networks, reshaping the profile of the investors who would end up absorbing the losses should they materialise.

This paper focuses on two specific episodes — the deterioration of BDCs in the U.S. and the growth in SRTs in Europe — in order to argue that the right question today is not whether private credit will trigger the next crisis but what does it tell us about the system in which it has embedded itself. Since 2008, credit risk has not decreased on aggregate; rather it has shifted location, form and counterparty. Mapping those routes and understanding who stands to absorb any losses at their endpoints is where the supervisor needs to focus in this cycle.

The space occupied by private credit

Episodes of financial instability rarely take the same form as those that precede them. After the subprime mortgage, shadow banking and commercial real estate crises, the market is currently shining the spotlight on private credit and semi-liquid (evergreen) investment funds. The draw is clear: the market has grown very swiftly in recent years, is opaque by definition, uses valuations that are less tested by the market than other segments and has emerged as a key channel for financing businesses that used to depend far more on the banks or syndicated loan markets. It would be a mistake to conclude we are looking at the functional equivalent of 2008. But it would also be wrong to conclude that the growth in private credit does not pose a “systemic” risk just because the banks are better capitalised than they were 20 years ago.

The important question is to understand the shift in the financial architecture since the Great Financial Crisis. Within that new architecture, credit risk has not decreased in aggregate terms; it has shape-shifted, relocating to other types of balance sheets and vehicles. In the U.S., that shift has taken the form of vehicles that promise access to illiquid assets, or assets which cannot be monetised quickly. In Europe, it has often taken a less visible form: that of the synthetic transfer of credit risk to allow the release of capital without removing the loans from the balance sheet. The two paths look different on paper but both lead to the same question: who really assumes the risk when credit migrates outside the banking perimeter?

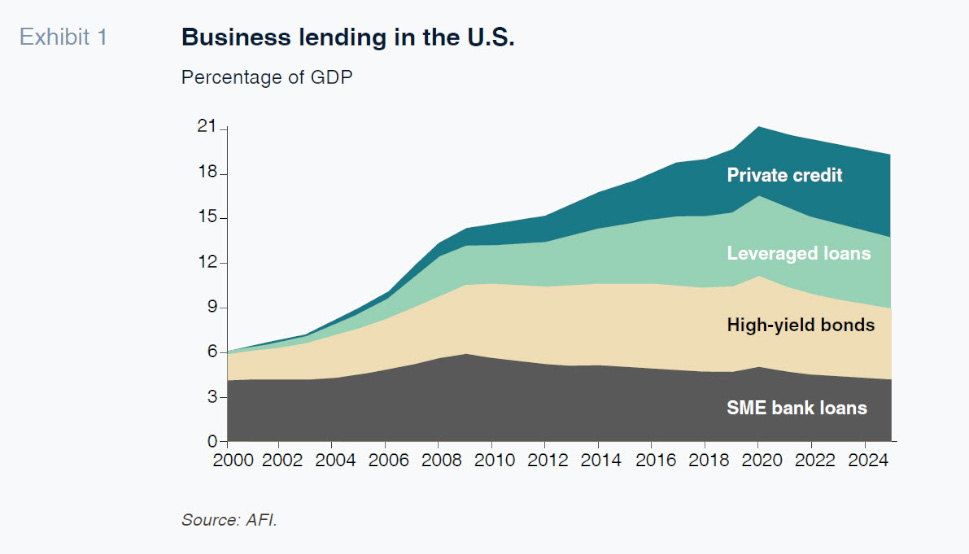

Private credit has filled a structural vacuum. The regulatory climate prevailing since 2008 has pushed the banks to abandon the originate-and-hold model (where they extend a loan and then hold it on their balance sheet) in favour of an originate-and-distribute model, transferring risk to institutional investors. That shift accelerated the banks’ withdrawal from multiple leveraged finance segments as well as from the middle market. In parallel, many medium- and large-sized enterprises continued to need flexible, swift and tailored financing. That is where private credit found its niche. Moreover, the market no longer only serves small or bank-restricted borrowers: the growth in large transactions and increasingly blurred line between bilateral direct lending and the syndicated loan market evidence the existence of a financing continuum rather than a clear boundary between the two worlds. The private credit market has grown to close to 1.8 trillion dollars (from around 400 billion dollars in 2020), making it a structural component of the leveraged financing world.

U.S.: When the liquidity promised is mismatched with the asset

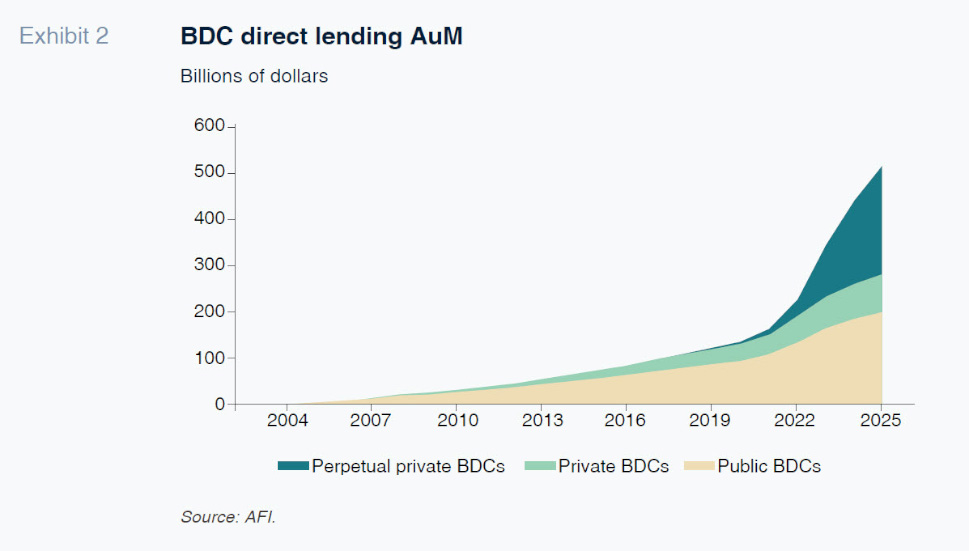

In the U.S., the highest-profile episode involves BDCs and within that segment, the boom in evergreen structures. BDCs were created to finance middle market companies that had been abandoned by bank credit. For years they took one of two forms: listed BDCs, which offer daily market liquidity; and the classic private and closed-end BDCs. The evergreen BDC is a more recent development, promising periodic liquidity windows, usually quarterly and capped at around 5% of net asset value. This new format has been one of the key drivers of the recent growth by offering access to private credit yields without, at least on paper, the illiquidity associated with this asset class. Assets under management (AuM) in BDCs currently stand at around 500 billion dollars, half of which is in evergreen funds.

Here is where the first source of friction emerges. The underlying asset remains an illiquid, bilateral loan with a scant secondary market and valuations that often rely on internal models. The liability, in contrast, features a promised periodic exit. This mismatch becomes an issue when a listed BDC begins to send a price signal that differs from unlisted BDC valuations. That is what happened in the U.S., where the listed BDCs were at some point trading at discounts to NAV (Net Asset Value) of close to 20%. For investors in an evergreen vehicle, that discount suggests that their fund’s internal valuation may not match its market value. At that juncture, the liquidity window becomes a valuable option. Redemption requests surge, triggering gate activation by some of the biggest managers.

It is important to underline that those gates are not evidence of a market failure. They are defence mechanisms designed to prevent the forced sale of illiquid assets at distressed prices. The underlying problem is not the liquidity gates, which fulfil their function, but rather the message that may have been marketed to retail investors, creating an expectation of more liquidity than the underlying asset can bear.

The second source of friction has less to do with the vehicle structure and more to do with the quality of the underlying credit. The software sector has accounted for a very considerable share of the growth in private credit in the last decade, representing more than 20% of today’s portfolios. The investment rationale made perfect sense when rates were low: high-growth businesses, high margins, recurring income and asset light models. Today, however, the sector faces existential threats. Firstly, many of these companies will have to refinance their debt in the next two years in a much tougher rate and spread environment. Secondly, artificial intelligence is altering the outlook for the sustainability of the business model. In addition, being an asset-light model, originally a plus, has become a liability, implying lower recoverability rates in the event of default.

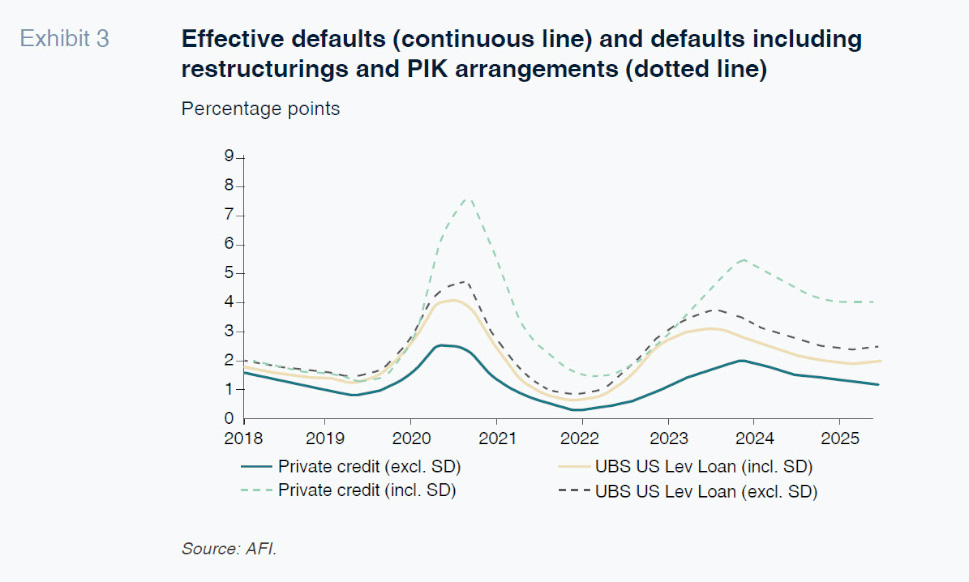

For that reason, it is important not to make too light of the trend in default rates. The headline default metrics remain relatively contained. However, the downturn is more tangible when the scope of the analysis is broadened to include more hidden signs of distress such as restructurings, maturity extensions, and payment-in-kind options. Looking at defaults in the strictest sense, the figure is barely over 2%, but adding in those other practices, the rate could be more than 6%. Another concern is the growth in the share of interest accrued and not collected at some BDCs, where those accruals are running at 6% of their income.

That being said, it would be just as mistaken to turn this snapshot into a prediction of looming collapse as it would be to minimise it. Recent evidence does not point to an imminent systemic threat. Other than the Great Financial Crisis, private credit does not have a history of major losses and other indicators do not yet indicate abrupt deterioration. In addition, the software exposure issue is not exclusive to private lending; it is also a factor in the syndicated markets and pockets of the high yield universe, albeit to a lesser degree. That curbs the temptation to present the problem as something idiosyncratic to private credit. The current situation is more compatible with a cyclical and sector correction, exacerbated by liquidity friction, rather than an episode of a systemic nature.

Europe: Risk transfer without derecognition

The picture looks different in Europe, where the issue has not been about the liquidity promised to end investors as much as capital engineering by the banks in the form of synthetic risk transfers (SRTs). Here the loans remain on the banks′ balance sheets, but the banks transfer the first-loss or junior tranche to investors, so reducing risk-weighted assets and freeing up regulatory capital. In contrast to BDCs, the investor does not buy direct exposure to the loan. The difference with a traditional securitisation is that the asset is not removed from the bank′s balance sheet. This alters the location of the risk substantially. In Europe, the problem is not one of a vehicle promising liquidity from an illiquid asset; it is one of the banks boosting their capitalisation without offloading the credit or reducing the system′s vulnerability proportionately.

The market growth speaks for itself. The outstanding balance of synthetically transferred corporate loans in the eurozone jumped from around 60 billion euros in 2018 to over 300 billion euros at the end of 2024. The median size of the junior tranche is roughly 15%. That stock of credit is estimated to have enabled the release of between 20 and 25 billion euros of Tier 1 capital. Sizeable numbers but a nuanced interpretation is required. From the aggregate perspective, the BIS underlines that the protection provided by SRTs was equivalent at the end of 2024 to around 2% or less of total loans and that the average relief in terms of CET1 (common equity tier 1) was around 40 basis points. Seen that way, the market continues to be small relative to the size of the banking system. However, even though the market remains contained at the system level, at the individual entity level, it can be relevant.

What concerns the supervisor the most is not, therefore, the standalone size of the market but rather the incentives it generates. A recent ECB paper provides valuable evidence. It appears that the banks do randomly select loans for SRTs. They tend to transfer assets that are especially “efficient” from the regulatory perspective, i.e., loans that consume substantial capital relative to their economic risk. That means that the capital released can be reused without generating a proportionate improvement in loss-absorbing capacity. The banks can end up with a more comfortable capital ratio without delivering a more robust balance sheet in economic terms. Moreover, after the risk is transferred, the incentive to monitor the borrower fades. The ECB finds significant reduction in the frequency with which the banks update their default probabilities for transferred exposures.

Elsewhere, some of the investors who purchase risk in SRTs also have credit relationships with the banks. In the sample analysed by the ECB, the banks are more inclined to sell risk to investors to which they also extend credit, and a significant share of those investments would appear to be financed, directly or indirectly, using bank debt. This nexus does not mean there is a “doom” loop but does suggest that the risk transferred may re-enter the system through another door. The BIS dubs this spillover phenomenon “circles of risk”: the credit formally exits the banking perimeter but returns as exposure to funds, insurers or vehicles financed by banks. If you then add in the risk of rollover (the SRTs mature and, in order to maintain the capital relief, need to be renewed), this circular chain becomes more worrying during periods of stress.

In other words, the European version of the problem is not one of open-end vehicles facing a surge in redemptions but rather one of a system that may be creating the appearance of more risk transfer than is actually taking place. As long as financing is abundant, investors accept the subordinated tranche and the regulator agrees to the capital relief, the mechanism works well. However, if appetite for risk, the cost of credit protection or supervisory tolerance shift, some of that risk could re-emerge, and do so at a time when the banks have already used the capital released to extend new credit or remunerate their shareholders. Here the procyclicality dynamic comes into sharp focus.

Systemic reading and supervisory agenda

The systemic risk does not, therefore, reside solely with a hypothetical wave of defaults in private credit, but also the possibility that a sector shock or loss of confidence could force asset sales, restrict financing or shut down refinancing channels in several segments at the same time.

In the U.S., the combination of discounts to NAV, limited exit gates and gradual impairment of the credit more exposed to software and refinancing risk constitutes a stress test for the marketing promise of regular liquidity. In Europe, the growth in SRTs raises questions about the extent to which the banks’ capital optimisation efforts may be making their balance sheets appear more robust while fuelling dependence on non-bank investors and exposure to the potential closure of the SRT market. In both cases, the overriding question is whether the financial system as a whole is today more transparent and better able to absorb losses without the need for explicit public support.

For that to be the case, there needs to be improved access to information about valuations, PIK (payment in-kind) usage, maturity extensions, sector exposures and interconnectedness between the banks and non-bank vehicles. There is also a need for truly systemic and not just entity-specific stress tests. The supervisor needs to understand not only what would happen to each bank or fund as a standalone entity but also what would happen if a shock were to force all of them to demand liquidity at the same time. Lastly, it is advisable to resist the deregulation thrust. It is no longer sufficient to look at headline default rates or funds’ targeted returns. It is important to follow the less visible signs such as the distance between price and NAV at listed comparables; the growing share of capitalised interest; the share of uncollected income; concentrated exposure to sectors with low recovery rates; maturity schedules; dependence on sponsor recapitalisations; and, in Europe, the scale of the capital relief being generated by certain entities thanks to SRTs and their resulting future dependence on that market.

Conclusions

The moral of this story is, ultimately, simple. Private credit has provided financing where the banks pulled back. And precisely because it has already become a structural component of the system, it requires more balance sheet rigour as a whole and less marketing messaging. The right question is not whether the risk has left the banking perimeter but rather where it reappears when tension rises. In the U.S., it reappears in BDCs as a conflict between promised liquidity and an illiquid underlying asset. In Europe, it emerges in SRTs as a possible circular chain between capital relief, laxer monitoring and dependence on non-bank investors. In either case, the conclusion is the same: the risk has not disappeared; it has changed location and form.

Crises rarely return in the same form.Since 2008, the system has been reinforced along some of its more visible seams, but that process has also displaced risk to less transparent and harder to discipline areas. This does not condone private credit, but it does spell abandoning the simple notions held by those who believe that all non-bank growth is synonymous with healthy innovation and by those who believe that anything opaque necessarily implies an immediate crash. Between the two simplifications, there is less comfortable but more useful terrain: that of understanding how to connect the dots today between liquidity, capital, valuations and supervision in a system in which what counts is who ultimately absorbs the losses when confidence fails more than who provides the credit.

Javier Pino and José Manuel Amor. Afi