Geopolitics and the internationalization of Spanish Banking: Risk and diversification

Rising geopolitical tensions are increasingly shaping bank valuations, financial conditions, and risk perceptions in global markets. Spanish banks’ high degree of internationalization offers a partial buffer, with geographic diversification helping to stabilize earnings and mitigate exposure to localized shocks.

Abstract: Geopolitical risk is playing an increasingly visible role in the valuation of banks and their operating conditions. Evidence from the IBEX-35 Banks index shows that immediate and persistent equity declines follow major geopolitical events, such as Russia’s invasion of Ukraine, escalating tensions in the Middle East, and protectionist policy announcements. These episodes reflect a combination of weaker macroeconomic expectations, tighter financing conditions, and rising risk premiums. At the same time, the Spanish banking sector stands out for its high level of internationalization, with nearly 56% of total activity linked to foreign markets as of the end of 2025. This geographic diversification allows banks to offset adverse shocks in some regions with stronger performance in others, acting as a stabilizing mechanism for earnings and valuations. However, the effectiveness of this buffer depends not only on

the extent of internationalization but also on the composition of exposure across economies with different risk profiles and cycles. The findings suggest that geopolitical risk is now a structural feature of the global banking environment, requiring more systematic integration into banks’ strategic planning and risk management frameworks.

Introduction

Geopolitical risk is associated with the probability that international events may negatively impact economic activity and financial markets, altering both the expectations of market participants and the functioning of trade channels and capital flows. Recently, these types of risks—typically associated with trade tensions, international conflicts, economic sanctions, or the strategic use of industrial and financial policies by countries—have gained increasing relevance, becoming a focal point of economic and financial analysis.

The financial system—and, specifically, the banking sector—is no exception. The role of banks as intermediaries that facilitate the flow of funds and manage risk in an increasingly global environment means that such uncertainties stemming from the geopolitical landscape directly affect their performance. The growing global interconnectedness and the expansion of banks’ international business in recent years have amplified the impact of geopolitical factors, so that localized disruptions can spread rapidly to other regions not only through commercial channels but also through financial markets. Recent examples of geopolitical tensions illustrate this reality. The war between Russia and Ukraine has caused disruptions in energy markets that have led to significant episodes of volatility in financial markets. During the first quarter of 2026, the conflict in the Middle East has led to increased global uncertainty, pushing up commodity prices and, consequently, increasing market volatility, resulting in a perception of widespread economic uncertainty.

In this context, the international banking business faces significant challenges, such as the potential increase in credit risk in certain environments, the need to adapt to new regulations resulting from changes in the institutional and/or political setting, or the management of operational risks stemming from its exposure to jurisdictions particularly affected by such geopolitical risks. At the same time, however, the greater internationalization of the banking business can act as a mitigating factor for risks arising from geopolitical tensions. Indeed, adequate geographic diversification can help institutions offset the negative impact borne in regions more exposed to geopolitical uncertainty with better performance in others, thereby reducing their aggregate exposure to specific shocks and contributing to greater resilience against geopolitical risks.

The objective of this article is, therefore, to examine the extent to which the geopolitical landscape affects the market valuation of banks and how banks’ international exposure can play a moderating role in reducing risks and leveraging the benefits of business diversification, with a specific focus on the Spanish case.

Geopolitical risk and the financial environment

The financial system is not immune to the risks stemming from geopolitical and geoeconomic conditions. Indeed, investment and financing decisions—and, consequently, expectations of economic growth—depend on the stability of financial markets (Levine, 1997). On the one hand, episodes of armed conflicts, diplomatic tensions, or shifts in strategic alliances generate uncertainties that often translate into greater volatility in financial markets, fluctuations in commodity prices, and movements in exchange rates. All of this affects the real economy through changes in the prices of goods and services. On the other hand, geoeconomic risk—related to trade policies, the imposition of tariffs, regulatory changes, or crisis episodes—impacts supply chains, international trade, and capital flows. Both risks are closely interconnected and can amplify each other.

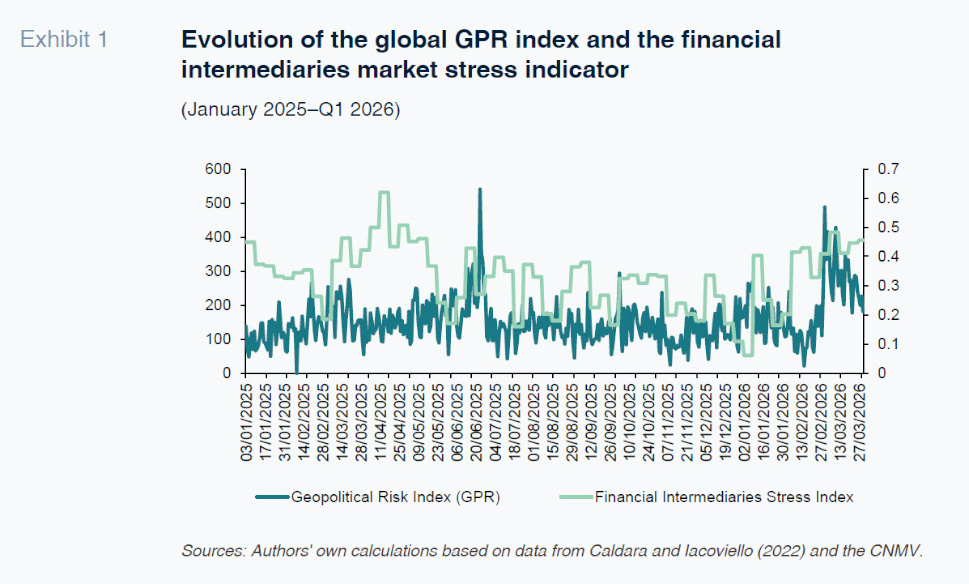

To provide evidence on the most recent trend in the geopolitical scenario, Exhibit 1 presents the daily evolution of the Geopolitical Risk Index (GPR) provided by Caldara and Iacoviello (2022) for the period from January 2025 to the first quarter of 2026. During the first months of 2025, the indicator reflects an already tense environment, marked primarily by the persistence of the war between Russia and Ukraine. Throughout 2025, other flashpoints of instability emerge—such as the escalation between India and Pakistan in May 2025 or the persistent conflicts in the Middle East—which keep the index at relatively high levels. During the second half of 2025, however, a certain easing is observed, consistent with a scenario in which conflicts persist but no new tensions arise. The index’s behavior changes significantly again in early 2026, alongside the escalation of the conflict in the Middle East following U.S. and Israeli attacks on Iran in late February 2026.

The economic consequences of these events—especially in energy markets—have been immediate, with the price of the oil barrel rising from $62 in early January 2026 to $126 on March 31. Furthermore, disruptions along strategic routes such as the Strait of Hormuz have heightened global uncertainty, as reflected in the GPR index’s performance during the first quarter of 2026.

The effects of changing geopolitical conditions also spill over into financial markets. In this regard, episodes of heightened geopolitical uncertainty, such as those mentioned above, tend to be reflected in increased volatility in financial asset prices, valuation adjustments, and changes in required risk premiums. In the specific case of banks, additional transmission channels come into play. On the one hand, a worsening macroeconomic outlook tends to degrade the quality of the loan portfolio extended to households and firms, raising the risk of default (see Correa et al., 2023). On the other hand, tensions in financial markets can make it more difficult and expensive for financial intermediaries to access financing (Phan et al., 2022).

Exhibit 1 also shows the evolution of the financial intermediaries market stress indicator in Spain, provided by the National Securities Market Commission (CNMV).

[1]

The recent evolution of this indicator reveals a dynamic that, while related to the described geopolitical context and the trend observed for the GPR index, also depicts distinct episodes potentially linked to financial and macroeconomic factors that may specifically affect the banking sector. Throughout 2025, isolated spikes are observed coinciding with the episodes of heightened geopolitical instability previously noted. However, these increases are temporary and do not consolidate at persistently high levels. In the second half of 2025, and in line with the greater stabilization of the GPR index, the market stress indicator also tends to show more stable levels. During the first quarter of 2026, rising geopolitical tensions, coupled with higher energy commodity prices and a deterioration in the economic outlook, lead to a spike in the stress indicator. This increase reflects greater risk aversion among investors, as well as a tightening of financial conditions, affecting asset valuations and, consequently, the financing conditions that financial intermediaries encounter in the markets.

Events and the banking environment

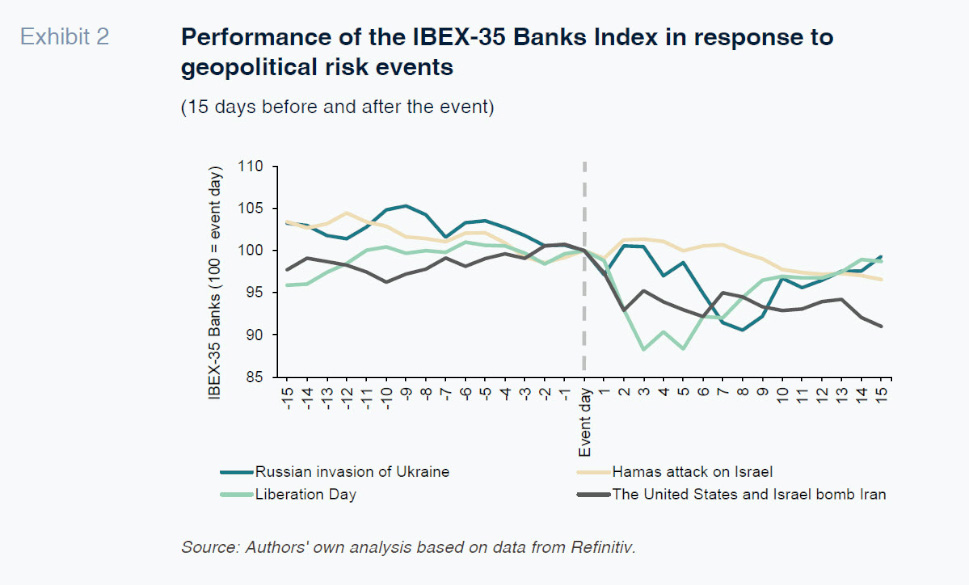

The banking sector, both in Spain and in other countries, is not immune to geopolitical events. The market valuation of banks is impacted by these events, reflecting uncertainty in financial markets. Exhibit 2 shows how the IBEX-35 Banks index reacts negatively to some of the major geopolitical events that have occurred in recent years. As can be seen, in all cases, a stock market decline is recorded in the days following the materialization of the geopolitical risk. “Liberation Day” (Trump’s tariffs announcement) stands out in particular, showing the largest correction, reaching a maximum drop of 11.72% and reflecting a strong impact of increased protectionism on the banking sector. By comparison, Russia’s invasion of Ukraine caused a maximum drop of 9.43%, while the U.S. and Israeli attack of Iran resulted in a slightly smaller decline of 8.97%. This confirms that, although all events have a negative impact, the intensity varies depending on their nature and economic consequences.

Furthermore, in the four cases, a certain degree of persistence is observed, as stock valuations do not fully recover within the fifteen days following the event. This behavior highlights the banking sector’s high sensitivity to increased uncertainty, particularly through channels such as deteriorating growth expectations, rising financing costs, and increased risk premiums. Likewise, the market reaction suggests that investors anticipate a potential negative impact on banks’ future profitability, whether due to reduced lending activity or a deterioration in asset quality. Taken together, these episodes reinforce the idea that geopolitical shocks have effects that extend beyond the immediate term.

International business: Exposure and risk diversification

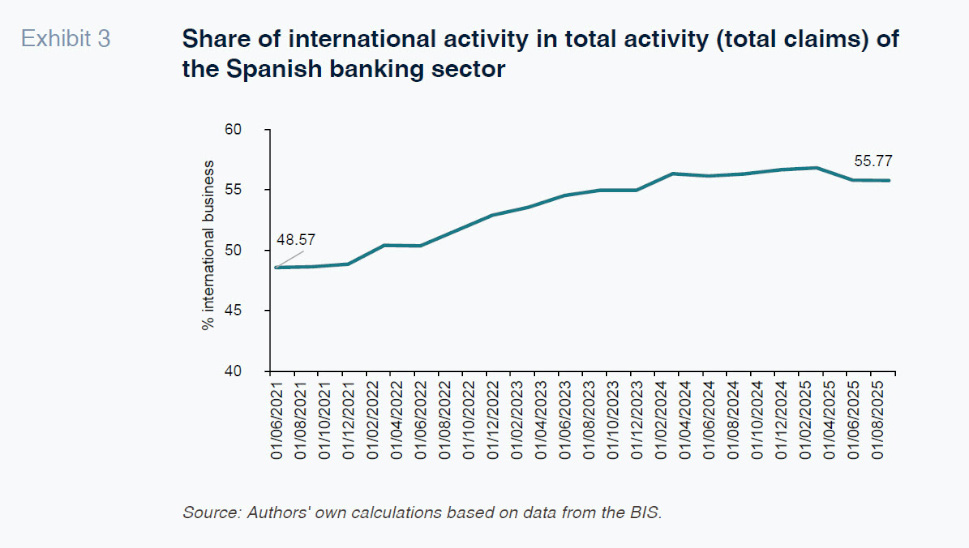

In the face of this exposure to geopolitical risks, the Spanish banking sector has a distinctive feature: its high degree of internationalization. Unlike other banking systems more focused on the domestic market, the major Spanish banks have established a significant presence in multiple regions, particularly in Latin America, the U.S., and Europe. This is especially relevant in a scenario characterized by regional uncertainty, where geographic and business diversification strengthens resilience against domestic crises. Data published by the Bank for International Settlements (BIS) confirm this geographic diversification. In the case of Spain, the data consistently show that a very significant portion of the banking sector’s aggregate balance sheet stems from business outside Spain, reflecting the sector’s strong international orientation.

Exhibit 3 clearly shows the growing trend in the share of international activity within the total activity of the Spanish banking sector in recent years. From levels close to 49% in 2021 to nearly 56% in the fourth quarter of 2025. This means that, currently, more than half of Spanish banks’ consolidated assets are linked to their international business, confirming a very high degree of internationalization compared to other European banking systems. This international expansion strategy has traditionally been interpreted as a mechanism to reduce dependence on the domestic economic cycle and take advantage of growth opportunities in other markets.

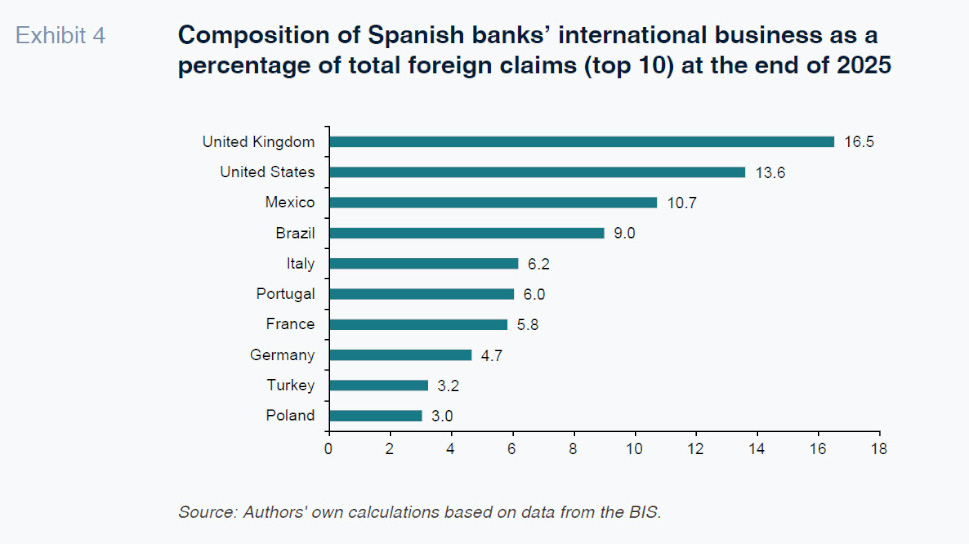

Exhibit 4 shows that the composition of Spanish banks’ international business at the end of 2025 is not concentrated solely in a few key markets. The United Kingdom (16.5%) and the U.S. (13.6%) stand out as the main destinations, followed by Mexico (10.7%) and Brazil (9.0%), reinforcing the strong presence in Latin America. In Europe, exposure is distributed among Italy (6.2%), Portugal (6.0%), France (5.8%), and Germany (4.7%), while Turkey (3.2%) and Poland (3.0%) provide diversification into emerging markets and Eastern Europe. This structure reflects the pursuit of a strategic balance between mature and emerging economies, allowing Spanish banks to combine stability and growth and strengthen their resilience in the face of episodes of geopolitical uncertainty. In this regard, internationalization and geographic diversification are key elements in managing geopolitical risk, as they reduce dependence on a single region and allow for offsetting potential adverse shocks in certain markets with better performance in others. Exposure to different economies, with distinct cycles and risks, acts as a buffer that helps stabilize results and valuations in environments of global uncertainty.

Conclusions

Geopolitical risk has become a key determinant of valuations and financing conditions in the banking sector. Recent episodes show that markets react quickly and persistently to such shocks, incorporating a heightened perception of risk regarding banks’ future profitability. At the same time, the case of Spanish banks highlights that the degree of internationalization and geographic diversification serve as a useful tool to cushion these impacts. A balanced presence across different regions and economies helps offset localized disruptions and strengthens the sector’s ability to adapt.

In the current environment, geopolitical risk can no longer be considered a residual exogenous factor, but rather a structural element of the global banking business. Consequently, banks must more systematically incorporate the geopolitical dimension into their frameworks for analysis, strategic planning, and risk management.

Furthermore, the results suggest that the quality of diversification is just as important as its extent. It is not merely a matter of expanding international presence, but of achieving an appropriate mix of markets with different risk profiles, regulatory frameworks, and economic cycles. In this regard, diversification that is overly concentrated in regions with similar vulnerabilities could limit its mitigating effect. Therefore, active management of geographic exposure, together with continuous monitoring of the geopolitical environment, is a key element in preserving financial stability and long-term value creation in the banking sector.

Notes

Note that the market stress indicator for financial intermediaries is provided on a weekly basis for the period January 2025–March 2026.

References

CALDARA, D., IACOVIELLO, M. (2022): Measuring geopolitical risk. American Economic Review 112(4), 1194-1225.

CORREA, R., DI GIOVANNI, J., GOLDBERG, L. S., MINOIU, C. (2023): Trade uncertainty and U.S. bank lending. NBER Working Paper, No. 31860.

LEVINE, R. (1997). Financial development and economic growth: views and agenda. Journal of Economic Literature, 35(2), 688-726.

PHAN, D. H. B., TRAN, V. T., IYKE, B. N. (2022): Geopolitical risk and bank stability. Finance Research Letters, 46-Part B: 102453.

Pedro Cuadros-Solas. CUNEF University and Funcas

Nuria Suárez. Autonomous University of Madrid and Funcas