Artificial intelligence and the labor market in Spain: Occupational exposure and estimated effects on employment

AI adoption among Spanish firms rose from 12.4% to 21.1% between 2023 and 2025, concentrated in sectors where exposure to automation is already highest. While the distributional consequences fall disproportionately on mid-level white-collar workers, reversing earlier displacement patterns, Spain’s position at a historic employment peak offers an opportunity to manage this transition from a position of relative strength.

Abstract:

[1] The relationship between artificial intelligence and employment has shifted substantially since Frey and Osborne′s (2017) estimate that 47% of U.S. jobs faced high automation risk, a figure now subject to methodological revision. Second-generation indices, built on task-level analysis rather than occupational categories, find that exposure to generative AI is concentrated among educated, higher-wage workers, not the routine manual jobs of the previous paradigm. Experimental evidence reinforces this picture: productivity gains are significant, but benefit less experienced workers the most, while aggregate TFP gains over a ten-year horizon are estimated at under 1%. Applying an adapted version of the AI Occupation Exposure index to Spain′s CNO-11 occupational classification, the model projects gross job displacement of between 1.7 and 2.3 million positions over 2025–2035, with a central estimate of 2.0 million concentrated in administrative, technical support, and scientific professional roles. Against this, complementarity effects benefit an estimated 3.1 million workers in services and manufacturing, and new occupation creation is projected at 1.61 million, placing the net loss at around 400,000 jobs in the baseline scenario. The distribution of that loss across geography, sector, and educational level is highly uneven, and the transition window depends critically on the pace at which displaced workers can access reskilling. Spain′s position at a historic employment peak as AI adoption accelerates represents an opportunity to manage that transition from a position of relative strength.

The transition from the Frey and Osborne paradigm to second-generation indices

Modern analysis of the relationship between technology and employment is grounded in the task framework proposed by Autor et al. (2003), whose key contribution was to distinguish between the content of the tasks performed by workers and occupations as aggregate categories. This perspective was formalized by Acemoglu and Restrepo (2018, 2019, 2020) in a model that identifies two opposing mechanisms: the productivity effect, which increases labor demand by reducing costs, and the displacement effect, which reduces demand by replacing human labor in specific tasks. The sign of the net effect depends on the relative magnitude of both.

The estimate by Frey and Osborne (2017) that 47% of U.S. jobs were at high risk of automation marked the first generation of exposure studies. Today, it is the subject of systematic methodological criticism: it treated entire occupations as units of analysis, without recognizing that automation operates on a task-by-task basis and that workers can be reassigned to non-automated tasks within the job. The widespread adoption of generative AI starting in 2022 spurred a second generation of more nuanced indices.

Felten et al. (2023) construct the AIOE (AI Occupational Exposure) index based on ten capabilities of AI systems and link them to the skills of each occupation according to the O*NET database. Their most significant finding is that exposure to generative AI correlates positively with median wages and educational attainment: it is white-collar and highly skilled occupations—not the routine manual jobs of the previous paradigm—that are most exposed. Eloundou et al. (2024), in a paper published in Science, reach a similar conclusion: approximately 80% of the U.S. workforce could see at least 10% of their tasks affected by language models, and around 19% could see more than half affected.

The OECD (2024), applying methodologies similar to its PIAAC database, places Spain at a potential exposure of 27.4%, slightly above the average (26%). However, the same report distinguishes between potential exposure and actual risk of automation: in Spain, the actual risk is estimated at 5.9%, considerably below the OECD average of 12%. This difference is attributed to the higher proportion of tasks with interpersonal, physical, or creative components in the Spanish occupational structure, which are difficult to automate even in occupations with high potential exposure.

Experimental evidence on productivity

Alongside exposure studies, controlled experiments measuring the actual impact of generative AI on productivity have proliferated. Brynjolfsson et al. (2023, published in QJE in 2025) study the implementation of a conversational assistant among 5,179 customer service agents: access to the assistant increases productivity by 14% on average, with a 34% effect on new employees and virtually none on veterans. The authors —interpret this pattern as evidence that AI encodes best practices and narrows the productivity distribution within the company.

Noy and Zhang (2023), in an experiment published in Science, randomly assign access to ChatGPT to 453 professionals performing writing tasks: the time required is reduced by 40%, and quality, as evaluated by blind judges, increases by 18%. Once again, workers with lower relative skill benefit the most. These results, however, should be interpreted with caution when extrapolated to the economy as a whole. Acemoglu (2024, published in Economic Policy in 2025) provides the framework for this extrapolation using Hulten’s theorem: by combining the exposure parameters from Eloundou et al. with the experimental savings estimates, he concludes that the cumulative increase in TFP over ten years will not exceed 0.66%. This result is modest because, although savings on individual tasks are significant, the share of total value added corresponding to tasks that are currently automatable is relatively small.

Spanish business adoption confirms this tension between microeconomics and macroeconomics. The INE’s ETICCE for the first quarter of 2025 puts adoption at 21.1% of firms with ten or more employees, compared to 12.4% in 2023: an increase of 8.7 percentage points in just two years. Sectoral heterogeneity is very pronounced: the ICT sector leads with 58.7%, compared to 25.7% in services, 17.5% in industry, and 11.4% in construction. The COTEC-ISEAK report (2025) estimates that adopting companies have an average productivity 27% higher than non-adopting companies, although the authors themselves caution against reverse causality: the most productive companies are also the ones most likely to adopt AI.

Estimate for Spain: The AIOE-CNO model

Applying the above framework to the Spanish labor market requires resolving the issue of correspondence between occupational classifications: the AIOE index uses the U.S. SOC, while the Spanish EPA uses the CNO-11. The strategy adopted consists of a double mapping: first between SOC and ISCO-08 using tables from the Bureau of Labor Statistics and Eurostat, and then between ISCO-08 and CNO-11 using tables from the INE. To account for the loss of precision associated with this double translation and the structural differences between the two labor markets, an adjustment factor φ = 0.82 is applied, which reduces the AIOE score by 18%. This value is an assumption of the analysis and will need to be refined once an exposure index constructed directly on the CNO-11 is available.

The model estimates the effects through three channels. The substitution channel applies to groups with an AIOE-CNO above the threshold α = 0.35 and combines the fraction of tasks susceptible to automation (δ_sust = 0.22, calibrated with Eloundou et al., 2024), the fraction that is actually automated over the ten-year horizon (γ = 0.65, based on Acemoglu, 2024), and the firm-level diffusion rate (ρ = 0.211, equal to the ETICCE adoption rate in 1Q2025). The complementarity channel affects groups with AIOE-CNO between 0.15 and 0.35 with a parameter of productivity gain δ_comp = 0.09. The creation of new occupations is exogenous to the model and is calibrated using Randstad/COIT (2024).

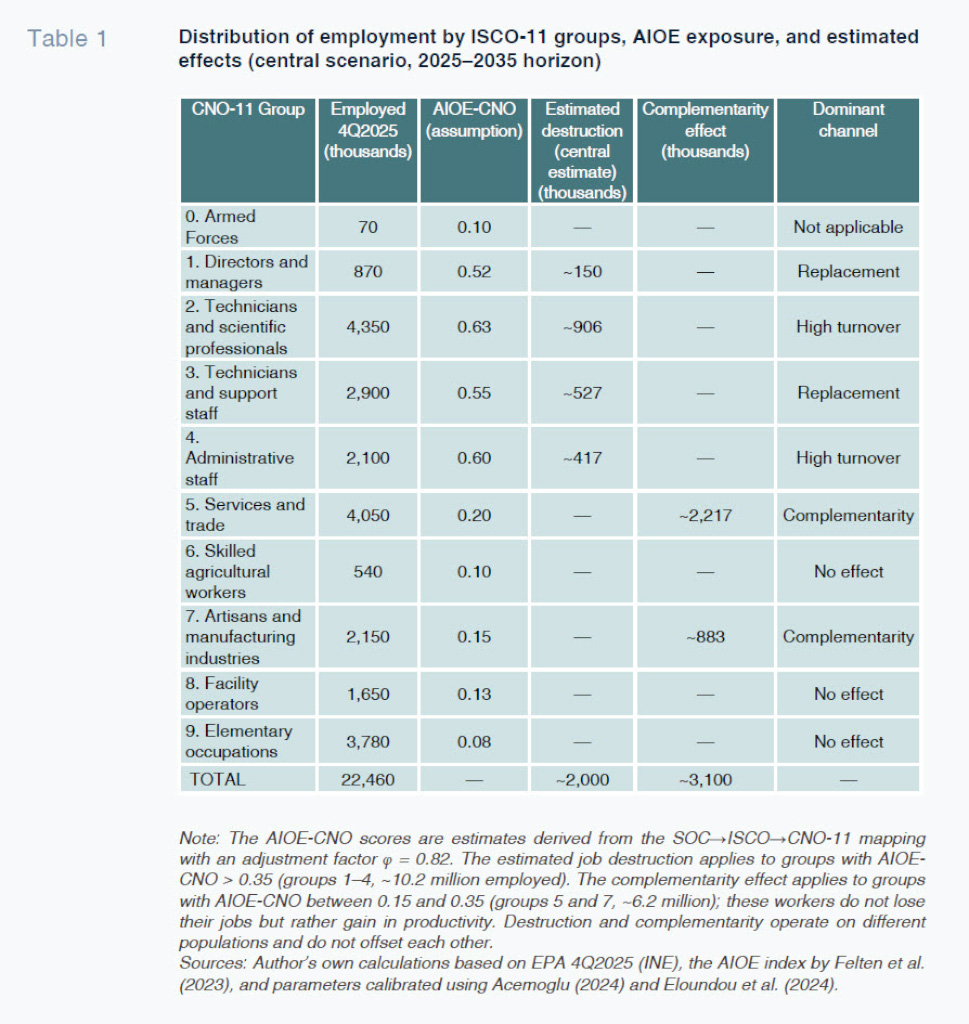

Table 1 summarizes the distribution of employment by CNO-11 groups, the AIOE-CNO scores, and the estimated effects in the baseline scenario. The four groups with AIOE-CNO scores above the threshold account for virtually all of the estimated job losses: scientific technicians and professionals (group 2) represent 45% of total job losses, support technicians (group 3) 26%, and administrative employees (group 4) 21%. Directors and managers (group 1) have high AIOE but a more modest total volume. In contrast, groups 5 (services and commerce) and 7 (crafts and manufacturing) experience a complementarity effect affecting 3.1 million workers who do not lose their jobs but gain relative productivity.

Results, net balance, and uncertainty

Applying the model to the baseline scenario data yields a gross job destruction of between 1.7 and 2.3 million jobs over the 2025–2035 horizon, with a central value of approximately 2.0 million. This estimate is consistent with the independent projections by Randstad Research/COIT (2024) for Spain. It is important to clarify what this job loss means: it does not imply that all these jobs will disappear en masse, but rather that this volume of tasks—currently performed by workers—could be carried out by AI systems over the considered time horizon. The reality will be a combination of workforce reductions through non-renewal of contracts, reduced hiring of replacements, and reorganization of duties within remaining positions.

Alongside the displacement channel, the model identifies two positive forces. Complementarity affects 2.8–3.5 million workers in groups 5 and 7, whose productivity increases without their jobs disappearing. The creation of new occupations—exogenous to the model and calibrated with Randstad/COIT (2024)—is estimated at 1.61 million over the 2023–2033 horizon, primarily technical and AI systems management roles. The net balance between gross job destruction (2.0 million) and creation (1.61 million) places the net loss at around 400,000 jobs in the baseline scenario, although its distribution by geography, sector, and educational level is highly uneven.

Whether this net loss will materialize depends, above all, on the speed at which displaced workers can acquire the skills demanded by the new occupations. The PwC AI Jobs Barometer (2025) documents a 56% wage premium for jobs requiring AI skills and 14% growth in occupations with the highest exposure to AI in Spain during 2019–2024, compared to 7% for those with the lowest exposure. This suggests that recent trends have been predominantly characterized by complementarity and job creation, not net displacement; however, this outcome may be temporary if technological acceleration continues.

The model’s uncertainty is very high. In the optimistic scenario (minimum parameters), job losses are reduced to about 700,000; in the pessimistic scenario (maximum parameters), they exceed 3.5 million. This wide range reflects genuine uncertainty regarding the pace of adoption and the speed of process redesign in companies. Additionally, the ten-year horizon is not an empirical estimate of diffusion in Spain, but rather a convention in the field inherited from Acemoglu (2024) and Svanberg et al. (2024). A five-year horizon would be equally plausible if diffusion continues at the pace observed between 2023 and 2025.

Implications for economic policy

The reviewed evidence and the model results point to a scenario of significant labor transition, although the mechanisms and magnitude depend on parameters with considerable uncertainty. The most relevant distinction is between the short-term horizon—where complementarity and job creation effects predominate—and the medium-term horizon, where deepening automation may generate more intense displacement pressures. The fact that Spain is at an all-time high in employment just as AI adoption accelerates offers a window of opportunity to anticipate the transition from a position of strength.

The priority should be the design of active labor market policies specifically targeted at groups most at risk of displacement—mid-level administrative and technical employees—combining intensive reskilling programs with hiring incentives for new AI-related occupations. The 56% wage premium suggests that acquiring these skills is a significant driver of upward mobility. However, access to AI training tends to be concentrated among workers with higher prior educational attainment, which may widen existing gaps. Policies that combine training support with mechanisms for recognizing skills acquired through non-formal channels will be particularly important for expanding access for lower-skilled workers.

From a business perspective, the risk that SMEs—which account for 99.8% of the business sector and approximately 70% of private employment—will lag behind in adoption is real and has direct implications for employment. If large firms automate at a faster pace, the competitiveness gap widens and sectoral concentration accelerates. Policies supporting the digitalization of SMEs, including access to low-cost AI tools and assistance with managing organizational change, are a necessary complement to labor market policies. The full version of this paper elaborates on the model’s parameters, the optimistic and pessimistic scenarios, and a detailed analysis of methodological limitations.

Notes

References

ACEMOGLU, D. (2024). The simple macroeconomics of AI. NBER Working Paper 32487. Published in Economic Policy, 40(121), 13–58.

ACEMOGLU, D., and RESTREPO, P. (2018). The race between man and machine: Implications of technology for growth, factor shares, and employment. American Economic Review, 108(6), 1488–1542.

AUTOR, D. H., LEVY, F., and MURNANE, R. J. (2003). The skill content of recent technological change: An empirical exploration. Quarterly Journal of Economics, 118(4), 1279–1333.

BRYNJOLFSSON, E., LI, D., and RAYMOND, L. R. (2023). Generative AI at work. NBER Working Paper 31161. Published in Quarterly Journal of Economics (2025).

COTEC / ISEAK (2025). Artificial intelligence and its effects on labor productivity. COTEC Foundation for Innovation / ISEAK, October.

ELOUNDOU, T., MANNING, S., MISHKIN, P., & ROCK, D. (2024). GPTs are GPTs: Labor market impact potential of LLMs. Science, 384(6702), 1306–1308.

FELTEN, E. W., RAJ, M., & SEAMANS, R. (2023). Occupational heterogeneity in exposure to generative AI. SSRN Working Paper, 4414065.

FREY, C. B., and OSBORNE, M. A. (2017). The future of employment: How susceptible are jobs to computerization? Technological Forecasting and Social Change, 114, 254–280.

INE. (2025). Survey on the Use of ICT and E-commerce in Enterprises (ETICCE), Q1 2025. Published on October 22, 2025.

INE. (2026). Labor Force Survey, Q4 2025. Published on January 27, 2026.

NOY, S., and ZHANG, W. (2023). Experimental evidence on the productivity effects of generative artificial intelligence. Science, 381(6654), 187-192.

OECD. (2024). Job Creation and Local Economic Development. November.

PwC. (2025). The Fearless Future: 2025 Global AI Jobs Barometer. PricewaterhouseCoopers, June.

RANDSTAD RESEARCH / COIT (2024). AI and the Labor Market in Spain. February.

SVANBERG, M., LI, W., FLEMING, M., GOEHRING, B., & THOMPSON, N. (2024). Beyond AI exposure: Which tasks are cost-effective to automate with computer vision? SSRN Working Paper, 4700751.

Francisco Rodríguez Fernández. University of Granada and Funcas