Banking-versus market-oriented financial systems: Questioning the European-US paradigm

Based on the value of assets and certain stock metrics in each jurisdiction, conventional opinion holds that the EU banking system is ‘overcrowded’ compared to the more market-oriented system in the US. However, further analysis of each systems’ metrics, particularly from a flows perspective, suggests the situation is far more nuanced.

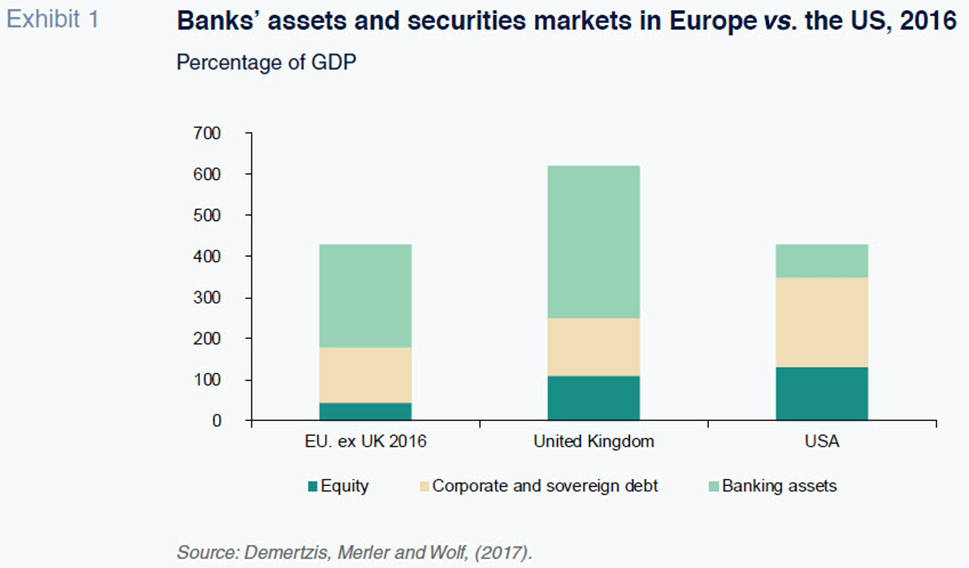

Abstract: Comparative economic literature differentiates between market-oriented and bank-oriented financial systems, with the former generally associated with the US. Moreover, ECB President Mario Draghi has described the European banking system as ‘overcrowded’. This tendency towards black-and-white categorisation relies on the comparison of ‘stock’ metrics, such as the weight of bank assets and the market value of listed securities (stocks and bonds) in GDP. Specifically, the ratio of bank assets to GDP in the US and Europe is 80% and 250%, respectively. However, such analysis can be flawed. For instance, due to the nature of the US mortgage market, these assets are frequently excluded from US banks’ balance sheets. It is also worth noting that the US banking sector includes twice as many institutions as those regulated by Europe’s Single Supervisory Mechanism. Furthermore, so-called ‘flow’ metrics challenge the prevailing assumption that Europe is less market-oriented than the US. Over the last decade, European bond and stock markets have channelled around 80 billion euros, net, to the corporate sector a year, whereas the net flows via the US bond and stock markets have been negative by nearly 100 billion euros.

Banking-versus market-oriented financial systems: The traditional paradigm

Economic literature makes a distinction between so-called ‘bank-oriented’ systems in which financial institutions are the predominant source of financing and a ‘market-oriented’ model whereby funds are raised primarily via the securities markets. In the former, banks are responsible for channelling funds from savers to borrowers, particularly non-financial corporates. By performing this intermediation role, banks constantly ‘monitor’ the borrowers on behalf of the deposit holders, a function which could not be conducted individually by each of those deposit holders or lenders.

In a market-oriented system, the companies are more inclined to issue securities (shares, bonds, etc.). Savers purchase these securities directly through distribution networks or banks. However, the key difference is the absence of any financial intermediary that alters the nature of the security issued.

Although both forms of financing coexist in all jurisdictions, countries differ in terms of the relative weight of each model. The synthetic proxies often used to determine the system bias include the stock of bank credit outstanding with the private sector and the market value of the securities –equity (shares) and fixed income (bonds and notes)– issued by private enterprises. In order to facilitate a comparison between countries, these indicators are usually measured against the value of a country’s gross domestic product (GDP).

A comparison using those benchmarks (Exhibit 1) confirms that the US is the most market-oriented system, while the banks dominate the financial systems in Europe. Specifically, the European banking system, measured by its volume of assets or their weight in GDP, is nearly three times the size of the US system. Conversely, the percentage of listed securities’ market values over GDP in the US is much higher. This can be partially attributed to the fact that the US system is more specialised in direct financing via the markets.

Since launching the Capital Markets Union (CMU) four years ago, the European Commission has shined the spotlight on the divergent nature of the two financial systems and considered the advisability of moving closer to the US model. When the Commissioner responsible for the CMU announced its establishment, he stressed that one of the objectives was to ‘unbank’ Europe. This expression is strikingly similar to how the president of the European Central Bank, Mario Draghi, described the Euro Area (EA) banking system as ‘overcrowded’.

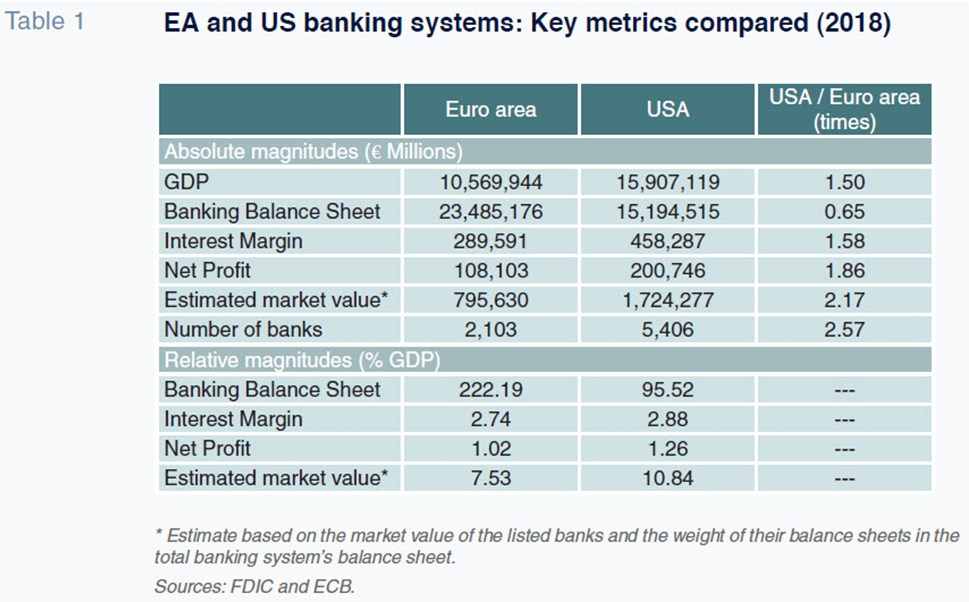

Questioning the paradigm (I): Defining a ‘banked’ systemOne of the objectives of this paper is to question the conclusion that the European system is overbanked in comparison with the US system. The standard proxy for measuring banking orientation is the weight of bank assets over GDP. According to this measure, it is clear that bank penetration in the US is less than half that of Europe (Table 1, which shows the main aggregate parameters for both banking systems for 2018). In the US, the Federal Deposit Insurance Corporation (FDIC) aggregates the parameters while in the EA, the parameters are the total aggregate for the ECB/SSM (Single Supervisory Mechanism), including the significant entities subject to direct supervision (118) and the less significant entities (~ 2,000), which are supervised indirectly by the national competent authorities.

With a GDP that is 1.5 times that of the EA, the US clearly has fewer bank assets. This correspond with the substantial difference in the ratio of bank assets to GDP of 80% in the US versus 250% in the EA. It is on this basis that observers have concluded the US is less ‘banked’ than the EA.

However, that conclusion is derived from a single parameter, namely bank assets. This parameter is less meaningful in the US context given that the mortgage market is articulated around a securitisation system underpinned by public guarantees (the public agencies popularly known as Fannie Mae and Freddie Mac). This has the effect of removing a large percentage of mortgages from American banks’ balance sheets. Those transferred loans not only reduce the size of the banks’ balance sheets, they also reduce their exposure to credit risk (absorbed entirely by Fannie Mae). As a result, the weighting of those assets for capital adequacy purposes falls, thereby significantly boosting American banks’ solvency.

Given this important distinction, it is clear that the penetration of the banks in the US should not be measured exclusively in terms of balance sheet metrics such as assets or own funds. Instead, business, cost and profit indicators are more appropriate metrics.

In terms of the more traditional banking business, the purest indicator is the net interest margin. This refers to the difference between the revenue earned on loans and paid on deposits. Importantly, it assumes balanced liquidity, as is currently the case in both the US and the EA.

Indeed, the net interest margin generated by the US banking system in 2018 was 1.58 times that generated in the EA. Expressing that margin as a percentage of GDP, the indicator is still slightly higher in the US (2.9%) than in the EA (2.7%), which suggests bank intermediation in the US is accompanied by higher transaction costs than in the EA.

With a much smaller asset base, the margin advantage commanded by US banks widens towards the bottom of the income statement. Specifically, US banks generate 1.8 times more net profit than their European counterparts.

Lastly, judging by the market values of the banks in the US and EA, the market is clearly signalling its belief that the profit margin differential will persist. Against that backdrop, we have attempted to approximate the value of the overall banking systems in both regions by extrapolating the listed banks’ metrics for the systems as a whole. It should be noted that in the EA, the listed banks account for 60% of the financial system’s assets, compared to 82% in the US.

The higher relative percentage of listed banks in the US compared to the EU could bias the comparison. However, we believe it does not substantially change the conclusions. Measured relative to GDP, the market has assigned a value to the US banking system that is almost double that of the EA system.

These valuations undermine the conventional belief that the US economy is far less banked than the European economy, a conviction upheld only by the relative size of the two systems’ bank assets and not their net interest margins, net profit or stock market valuations.

Another measurement that questions the ‘underbanked’ nature of the US system stems from a comparison between the number of banks in each jurisdiction. As already noted, the ECB has described the EA’s banking system as ‘overcrowded’ (see ECB, 2019). However, the number of banks covered by the US deposit guarantee scheme (FDIC) is more than twice the number of banks under the purview of the Single Supervisory Mechanism (ECB/SSM) in its dual capacity as direct supervisor of significant entities and indirect supervisor of less significant entities.

Questioning the paradigm (II): How do corporates raise money in the markets?

Having highlighted the contrasts between the EA and US banking systems, we next analyse certain aspects of their respective capital markets, which further question the traditional characterisation of US corporate financing as more strongly oriented towards the securities market than in Europe.

It is necessary to begin by providing an overview of ‘stock’ indicators for capital markets (market caps of stocks and bonds) alongside the net flows those markets have channelled towards corporate financing in the last decade.

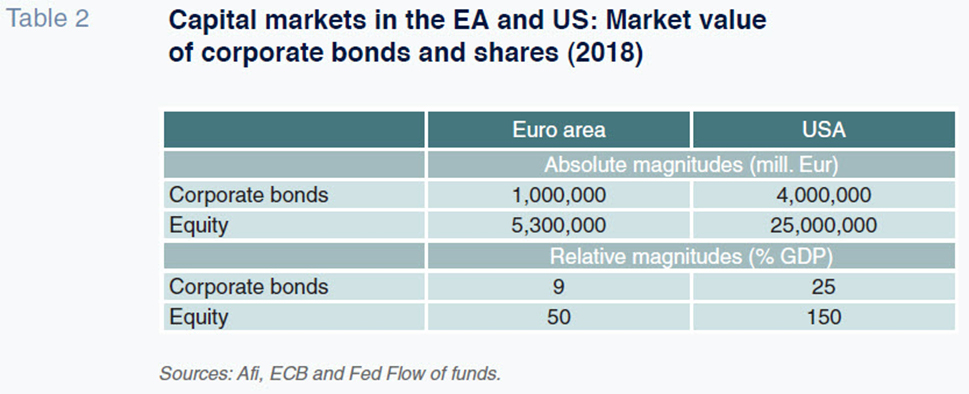

If the analysis is performed using stock metrics such as the market value of the fixed-income and equity securities listed on the capital markets, the comparison is overwhelmingly in favour of the US (Table 2), which uses year-end 2018 figures.

In the case of both corporate bonds

[1] and shares, the US dominates the EA by a factor between 4 and 5 in absolute terms and by a factor of 3 when the figures are stated as a percentage of GDP.

This striking contrast underpins the belief that the US financial system is far more market-oriented than bank-oriented. The combined market value of US bonds and shares is more than three times the volume of outstanding bank loans, whereas in the EA that ratio between securities and outstanding bank loans is exactly the opposite.

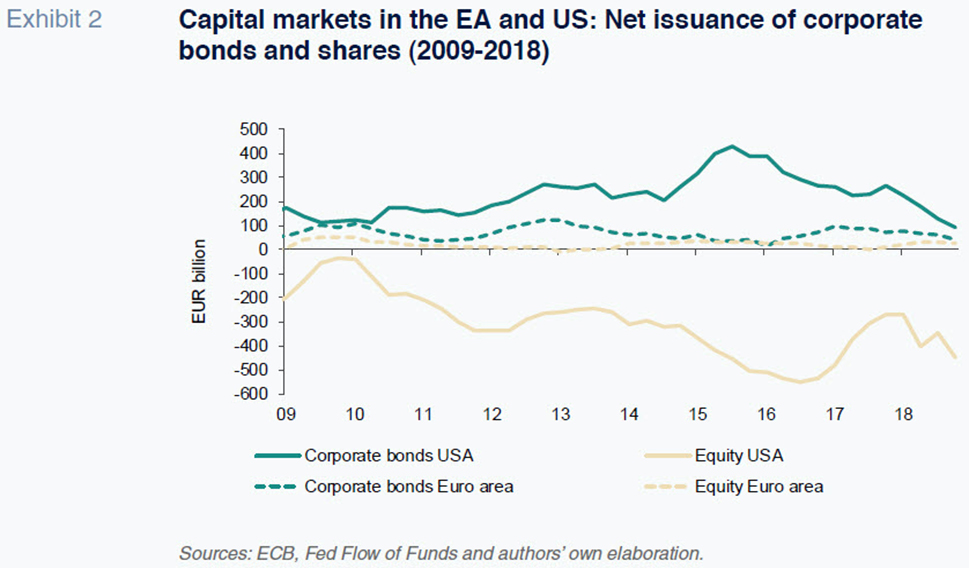

However, the comparison would be incomplete if we were only to look at stock figures (market value) and not the flow of financing towards productive activities. We therefore estimate the value of net issuance (net of bond redemptions and/or share buybacks) in the two economies during the last decade.

Exhibit 2 summarizes the net issuance flows for both economies, distinguishing between bonds and shares, as this yields a radically different reading in each instance. The figures show that the EA has experienced positive net issuance flows over the entire decade, which has been more pronounced in the bond markets (~60 billion euros per annum on average) than in the equity markets (~20 billion euros per annum on average).

In the US, the bond market has helped the country’s corporates raise funding to the tune of around 200 billion euros a year on average, which is three times the EA figure, thereby maintaining the ratio implied by the stock of outstanding bonds.

The situation is radically different with net equity issues. Net issuance of shares in the US market has been systematically negative every year during the last decade, which mirrors the patterns observed during the prior decade. Specifically, the economy has experienced an average annual negative net issuance of 300 billion euros, meaning that share buybacks exceeded new share issues by that figure.

Aggregating net bond and share issuance in the US and EA, the resulting snapshot clearly questions the conventional notion that corporate financing in the former is far more market-oriented. Specifically, during the last decade, the EA bond and stock markets have channelled around 80 billion euros, net, to the corporate sector a year, whereas the net flows via the US bond and stock markets have been negative by nearly 100 billion euros.

The key: ‘Internalisation’ of corporate finance

These data highlight the contradictory nature of one of the most widely accepted conventions in the literature on comparative financial systems. Indeed, the US, often touted as the preeminent example of a market-oriented, and specifically stock-oriented, system, is actually more nuanced than frequently portrayed.

The stock markets provide a valuation function (secondary market) for existing shares, while the listed companies, particularly those with higher levels of profits and liquidity, internalise their financing functions. This allows them to generate liquidity well in excess of their investment requirements, leaving substantial room for share buybacks, which leads to the re-assessment of stock market values.

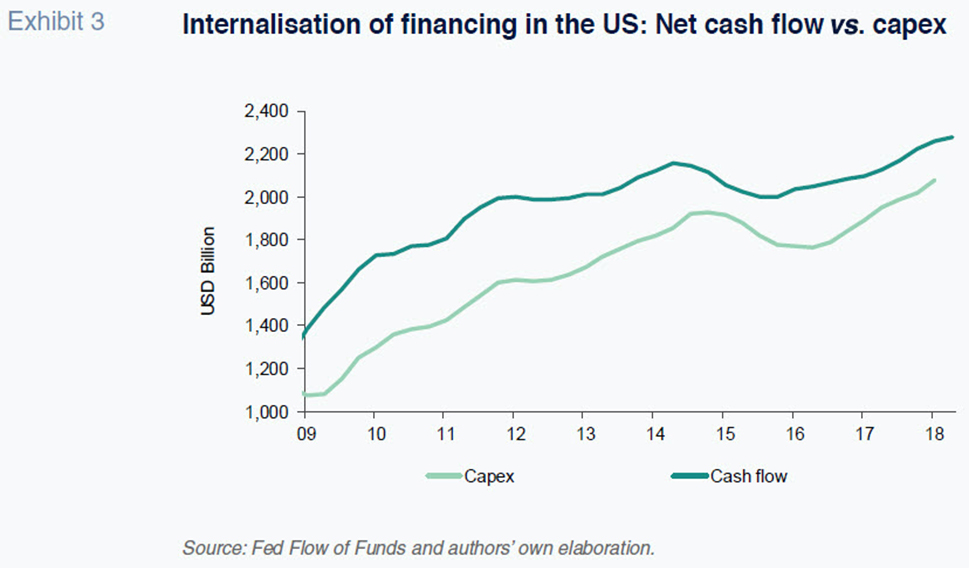

Throughout the last decade, the net cash flow generated by US companies has exceeded their capital expenditure (Exhibit 3). As such, they have fully self-funded their investments, generating enough surplus cash to buy back their shares and reduce their total outstanding shares. However, this situation is not mirrored in their stock market values, which have increased by far more in percentage terms than shares taken out of circulation.

However, additional analysis of the sector as well as a company breakdown of the practice of full internal self-financing accompanied by massive share buybacks is also necessary. Both practices are concentrated in certain sectors (especially tech) and particular companies (the so-called FAANGs-Facebook, Amazon, Apple, Netflix and Google), which have shown an impressive ability to generate cash flow, aided by low investment requirements measured by traditional standards. In many instances, these companies’ investments have entailed the acquisition of existing firms as a means of outsourcing of R&D. However, this practice impacts the negative net flow of funding from the stock market to the corporate sector as each acquisition implies the disappearance of existing stocks.

Notes

We examine the case of corporate bonds to emphasise the fact that the analysis does not include sovereign bonds or the bonds issued by financial institutions, which in the EA account for a much higher volume than those issued by non-financial corporates.

References

BERGES, A. and ONTIVEROS, E. (2018). De la Unión Bancaria a la Unión de Mercado de Capitales [From Banking Union to Capital Markets Union].

Información Comercial Española, No. 902, May, pp. 95-107.

DEMERTZIS, M., MERLER, S. and WOLF, G. (2017). Capital Markets Union and the Fintech Opportunity.

Bruegel Policy Contribution, No. 22, September.

ECB. (2019).

European Central Bank, Press conference: Introductory statements and Q&A, April 4

th. Retrieved from:

www.ecb.europa.eu/press/pressconf/2019/html/ecb.is190410~c27197866f.en.html

Ángel Berges, Álvaro López and Fernando Rojas. A.F.I. - Analistas Financieros Internacionales, S. A.