Strengthening manufacturing: A new industrial policy for Spain

Increasing the weight of manufacturing in the overall economy could make an important contribution to Spanish GDP growth and job creation. But to help achieve this goal, Spain needs a reform-minded public sector capable of launching a new industrial policy.

Abstract: Export promotion and productivity enhancement- two linked, mutually-reinforcing objectives, are the keys for rebuilding the Spanish industrial fabric and increasing its weight in the overall economy. A new, more robust, proactive and better-funded industrial policy that addresses specifically these issues, among others, may be the solution. Increasing manufacturing exports will create room for more imports and faster and sustained growth without external imbalances, providing new opportunities for employment. Productivity gains through greater innovation, skilled labour and other intangible assets will create the basis for wage recovery, greater aggregate demand and bigger and better equipped companies.

Spain’s economy has undergone a deep crisis in the past nine years from which it is only now beginning to recover. The manufacturing industry has been hit particularly hard by the contraction in internal demand, which has eroded one of its core growth drivers. Fortunately, Spain’s companies proved very astute at leveraging the growth in international demand until 2013, staving off even greater underutilisation of their productive capacity and an even more pronounced spike in unemployment.

Towards the end of 2013, the Spanish economy began to register growth, spearheaded by the manufacturing sector, so that 2015 and 2016 were years of clear-cut growth and job creation in the industry. 2017 is likely to extend this trend, which may well continue for longer, if the fragile international scenario, which is making investors very nervous, does not lead to a fresh recession.

To shore up the Spanish economy’s growth, articulating it around firm and balanced foundations (external versus domestic), requires changes in the way we produce, in the quality of what is produced and diversification of business endeavours into new activities and products. Industry, on account of its importance for innovation and exports, must play a leading role in this transformation of the productive model, winning back some of its lost share of output.

The goal of this brief article is to outline an industrial policy capable of increasing the weight of manufacturing in Spanish GDP and its ability to generate jobs, reverting some of the trends of recent years, in line with the objectives set in the European Commission’s agenda for 2020. Underpinning the formulation and presentation of the above programme is an analysis, on the one hand, of the status and performance of Spanish industry in the run-up to the crisis and during the eight years to have elapsed in the interim and, on the other, of the gap and scope for public intervention in the industrial arena in the developed economies, i.e., the role of industrial policy.

Status and performance of Spanish industry

In contrast to what is commonly believed, Spanish industry performed reasonably well until the start of the crisis, particularly considering the suboptimal environment as a result of: (i) the mass arrival of immigrants who, while fortifying internal demand, impeded productivity gains by encouraging labour intensive and low-wage production; and (ii) tremendous growth in property construction, which proved an overwhelming draw for a substantial chunk of the financial resources tapped by the banks. More than significantly curbing the flow of financing into manufacturing, this real estate boom perhaps fuelled a culture of speculative and short-term investing which does a great disservice to innovation and longer-term challenges.

Nevertheless, Spanish industry stood out among its international competitors, withstanding well ‒ better than most of its European counterparts ‒ the rapid rise of the emerging economies, with China at the fore. Productivity gains lagged those of Germany by very little, exports continued to grow strongly, outpacing those of France, Italy or the UK, and companies’ returns on equity hit the double digits in 2007, similarly setting themselves apart from their European peers by this measure.

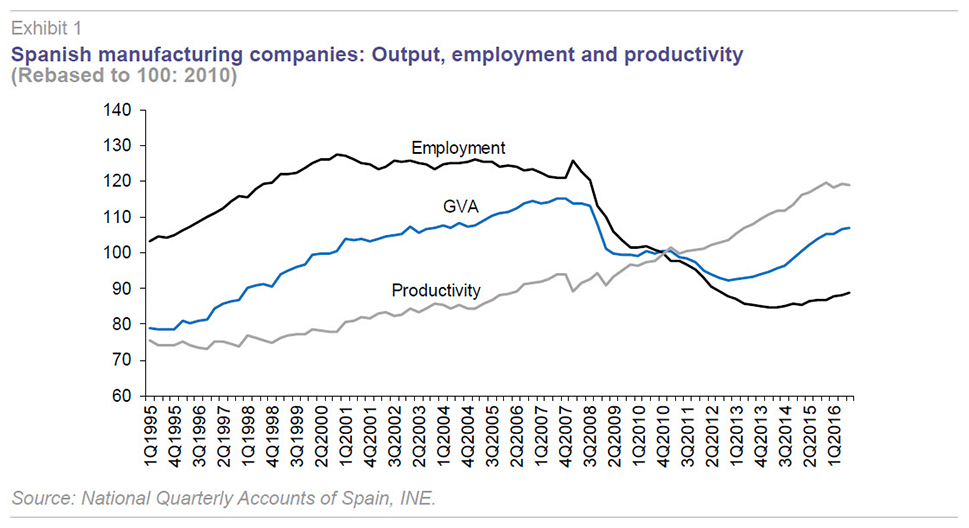

The problems arrived with the crisis and the sharp contraction in internal demand, which hit the manufacturing companies disproportionately on the back of the drop in property construction and civil works and in expenditure on gross fixed capital formation and durable consumer goods. Industrial output contracted sharply between 2008 and 2013, while employment fell even harder, impacted by the disappearance of less productive small businesses that saw their markets and financing dry up (Exhibit 1). In contrast, manufacturing sector productivity rose, mainly thanks to the closure of these less productive firms.

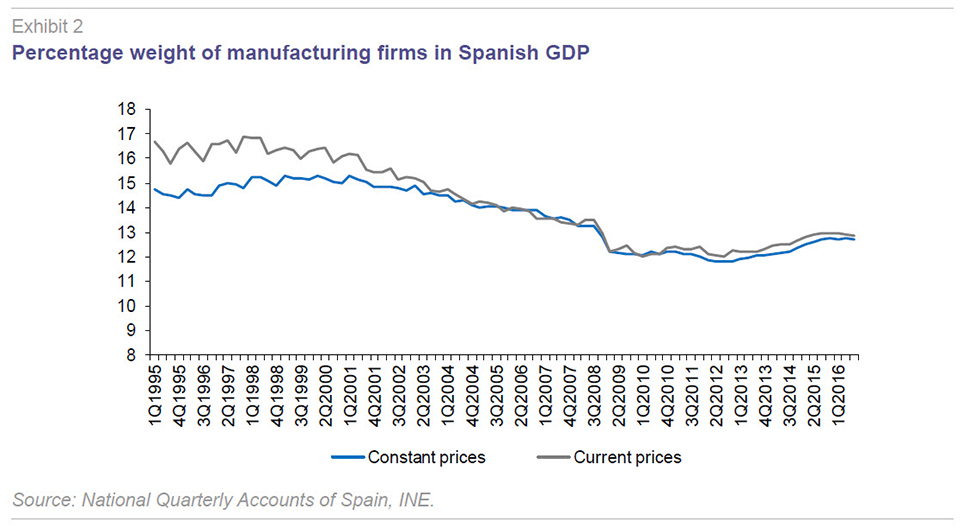

Nevertheless, the growth in exports during the central years of the crisis made a significant contribution to maintaining sector output, preventing even greater upheaval and curbing the downward trend in the sector’s contribution to GDP (Exhibit 2). The Spanish companies drew on the experience already built up overseas to offset home-market weakness with exports targeted at the countries that were still growing strongly, the emerging markets. And they succeeded, outperforming their German peers on export growth, even though the latter were better entrenched in some of these economies, namely in Asia. These noteworthy competitive advantages have been on display once again since 2013, as the Spanish economic recovery is being spearheaded by the manufacturing industry.

The surprising strength of Spanish exports, a phenomenon not new to this crisis, albeit evident throughout, is the best proof of the sector’s competitiveness, often critiqued without reason and without substantiating data. In fact this competitiveness is attributable to a varied offering of exports (medium to high-tech), well adapted to global demand; improvements in product quality and differentiation; a good combination of old markets (EC) and young and growing markets (Latam/Asia/Africa); and a roster of large companies that are highly productive on a comparative basis. It is also attributable to the effort made to become inserted in global value chains, thanks to the help of foreign multinational companies located in Spain.

That being said, not everything is working well in Spanish industry: a host of competitive disadvantages are curbing its growth and these should be addressed in the form of a more robust, proactive and better-funded industrial policy. Starting with exports ‒ already flagged as one of Spain’s greatest assets ‒ overly concentrated among a limited number of products, markets and companies. Next, the productive structure: sorely lacking in presence in the ITC sectors, which is where the seeds of new production are often found, making it imperative to nurture them. Meanwhile, productivity is making slow progress and the gains are being driven by greater mechanisation of operations rather than higher utilisation of intangible assets, which should be the key force in an economy as advanced as Spain’s. The sector is restricted, in short, by the wide sea of micro-companies that are not even able to reach the efficiency levels presented by their similarly-sized peers in other countries. Deficiencies in management and the delegation of tasks rank as important causes of Spanish companies’ relatively reduced size, perhaps ultimately a tribute to the level of mistrust among individuals, which translates in the labour arena into employee distrust vis-a-vis business owners and vice versa (Huerta and Salas, 2014). This distrust prevents a participative leadership style capable of defining objectives well and involving all members of the company in delivering them.

Spanish industry therefore needs the help of an industrial policy. It is not alone in this respect. All the European industries have lost share in the productive landscape, which is why the European Commission has placed the spotlight on re-industrialisation, setting ambitious targets for 2020 (European Commission Communication, 2014).

The role of industrial policy

Industrial policy can and should play an important role in this process. Several models substantiate this notion. There is of course, the Asian model, often criticised, and certainly hard to evaluate, but which nevertheless has had its successes, from that of Japan in the post-war years to that of China, passing through Korea, perhaps its finest and most complete manifestation. The problems facing Japan today and the Asian crisis of the end of the 1990s appear to be more the result of abandoning the model than sticking with it (Weis, 2011). Turning to the developed world, this theory is also borne out by the German and US models, both characterised by the vigour and scale of their innovation policies, unquestionably the focal point of industrial policy in the world’s most advanced economies. It is also underpinned by various applied studies evaluating the effectiveness of support for industry. Lastly, the globalisation phenomenon and the significant technological challenges facing today’s economies (nanotechnology and biology or industry 4.0, marked by 3D printing, product and transaction digitalisation and artificial intelligence), so threatening to jobs, require concerted action not only to ensure the right level of progress but also to facilitate the required transition to new productive structures.

Europe’s industries are paying the price today for notable abandonment since the early 1990s by the authorities, which, rejecting the interventionism that had been sometimes excessive and above all poorly conceived of in the prior decades, took a more bureaucratic approach and became less willing to provide financial support. The logical rejection of an administration that aspired to defining which industries should lead their economies gave way, accordingly, to the opposite extreme: a vacuum of public guidance and objectives in the industrial development arena. Europe embraced the key tenets of the liberal discourse regarding the non-need for an industrial policy per se and the advisability of limited intervention in terms of shaping the apparition and growth of businesses, without grasping the reality palpable behind the American model, a policy of fostering research and innovation, highly nurturing of its innovative small companies and very invested in large-scale and costly scientific programmes. Only Germany grasped this reality, far more obvious today. As noted by Mazzucato (2014), in the US, the state not only defines the technological development mission, it acts as guide and executive arm.

In short, an industrial policy that defines cross-cutting objectives in response to several market failures is called for (Rodrik, 2004; Chang et al, 2014). There are multiple forms of public intervention that generate positive externalities: boosting auxiliary products, needed for the development and exploitation of economies of scale in other high-potential areas of primary production, avoiding coordination failures; patronage of innovation and the discovery of new products by entrepreneurs (self-discovery); or the provision of resources and skills to SMEs that they cannot afford themselves on account of their lack of scale (expenses associated with training, investment in new management models or international expansion). These forms of intervention can be particularly effective in regional strategies, which have given rise to the rollout of smart specialisation clusters (McCann and Ortega Argilés, 2016).

Industrial policy needs to forge a closer relationship with the private sector, overcoming its fear of succumbing to private interests. To do so, all that is required is a well-trained administration and clear operating criteria. Such a policy needs the support of specialised agencies and public-private partnerships that can provide government with deep knowledge of the productive activity, while showing companies the range of public-support options that are truly necessary and effective, underscoring the importance of developing their interventions in pro-competitive environments.

Needless to say, the various levels of government, on the one hand, and all industrial organisations, particularly employer associations and unions with their various sector and regional chapters, need to participate in these agencies and partnership platforms. These organisations bring vital information for the authorities which need to learn about the industrial reality in order to better coordinate their actions and define new technology- and production-related initiatives.

Industrial policy objectives

In our opinion, industrial policy should pursue two interrelated objectives:

- Labour productivity gains; and

- Internationalisation of firms and the economy as a whole, via exports, integration in global value chains and the creation or acquisition of productive subsidiaries in other countries. Without neglecting the need to draw foreign multinationals, another integral part of the broader goal of internationalising the Spanish economy.

Progress on productivity, as well as crucial to industry’s competitiveness abroad and, by extension, its growth, is a solid and necessary step in a company’s international expansion, which in turn provides invaluable knowledge about the product manufactured, other related products and the productive processes which translates into fresh labour productivity gains and a positive spillover in the form of knowledge of new markets which the authorities can and should use in their trade development policies.

Specifically, it is vital to boost exports: this paves the way for job-creating growth and imports, without creating trade imbalances, unlike in the past, while making progress on foreign debt reduction.

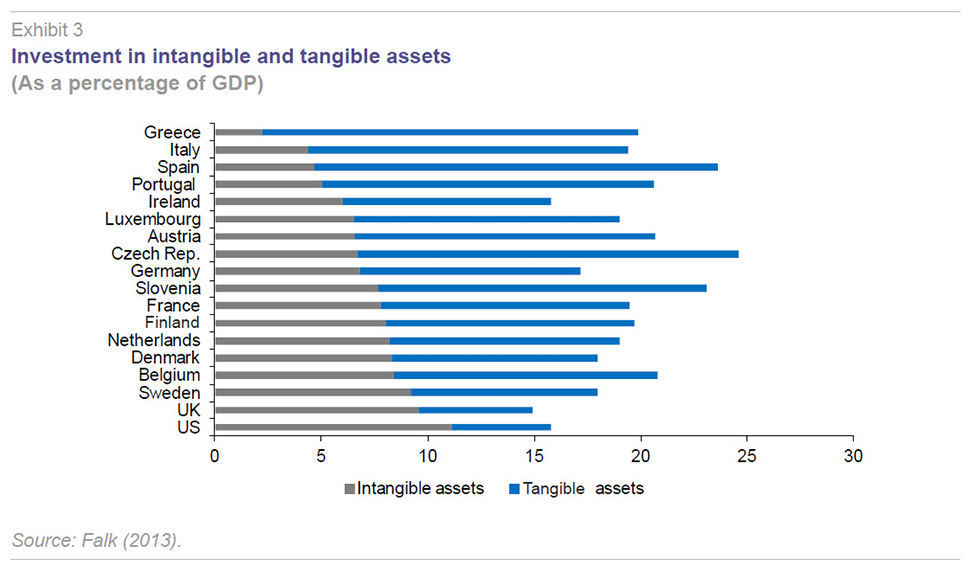

Productivity gains should be underpinned by the incorporation of skilled human capital and technology ‒ in other words intangible assets ‒into the productive process; these assets are still scantly present across Spain’s firms, as shown in Exhibit 3. This is the change in productive model that Spanish industry requires.

Innovation and how it is financed

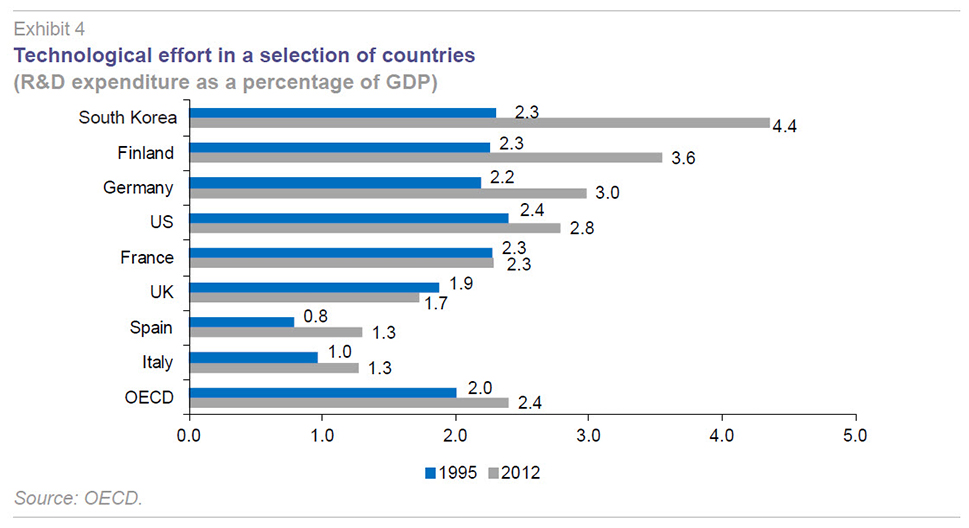

The lead role in industrial policy in advanced economies has to go to innovation. Spain consistently lost innovative companies during the crisis. Their number has halved since 2007, from 31,000 to 15,300. Behind that surprising trend lies not only a sparse innovation effort during the crisis (Exhibit 4), leaving Spain lagging further behind the leading innovating nations, but also the fragility of its innovation system. Spain belongs to the group of countries known as “moderate innovators”, alongside Italy, Hungary, Portugal, Greece, Croatia, Cyprus, the Czech Republic, Estonia, Lithuania, Malta, Poland and Slovakia. Clearly not the peer set it should aspire to in light of its level of development.

This fragility is even more evident in Spain’s position on the ranking of the 122 countries included in the Global Innovation Index (GII), at #28, far below the tenth spot commanded by Germany and South Korea’s eleventh place and in line with Italy (#29), a country that has registered annual per-capita GDP growth of just 0.8% in the last 30 years. It is vital to avoid a similar fate.

Spain’s laggard position is explained by its low scores on some of the sections used to calculate the GII, such as innovation efficiency, on which Spain ranks #48, and the level of business sophistication, which refers to the existence and operation of innovation networks: research partnerships between universities and companies, the development and role of clusters in the economy, external funding for R&D and patent families, among others. Even the IMF recently warned Spain that it stands apart for being one of the countries to provide the least financial support to innovation by private firms.

The big paradox in the innovation field lies with the fact that although Spain has the institutions befitting of a science and technology or “innovation system”, it is far from having a genuine “innovation ecosystem”, using the term coined to define smart territories in which all the agents interact in such a way as to contribute value-generating collaborative innovations. What’s more, this weakness appears to be the main reason why the European Commission agreed with the Spanish government a notable concentration of the resources contemplated in the Cohesion Fund for 2014-2020 in the programme dedicated to strengthening and supporting research, technological development and innovation. The comparison, leaving aside countries of the calibre of Germany, with less developed economies with similar performances to that of Spain, such as South Korea, is also worrisome.

An “innovation ecosystem” does not come about without the state playing a leading role and without close interaction between the latter and the private sector. And it requires the awareness that technology is a top-priority matter to which major resources must be devoted. The idea that the state is a mere provider of financing for innovation, at a remove from and ignorant of the risks and difficulties faced by its companies, is the surest way for a country to head toward technological insignificance.

The recent creation of the so-called State Innovation Agency (AEI for its acronym in Spanish) has created a new tool with which to restructure the country’s science and technology system. However, its first steps have not been very promising as the model being pursued looks more like the French model than its German counterpart as it appears to be emulating the bureaucratic-administrative culture characteristic of France. Governance of R&D and innovation policies in Spain falls, in terms of promotion and financing, since creation of this agency, to two main agents: the agency itself and the CDTI (acronym in Spanish for the Centre for the Development of Industrial Technology), both of which fall under the Ministry of the Economy and Competitiveness (specifically the Secretary of State for Research, Development and Innovation or SEIDI). The former plays the role of instrument for the management and public financing of R&D; the latter focuses on funding business innovation and development projects.

Regrettably, this initial design does not guarantee progress on articulation of an innovation ecosystem given the fact that other key organisms, such as Ministry of Industry’s ENISA, the national innovation company, have been left out.

A key aspect of the innovation thrust is its financing, which must be based on multiplying the spectrum of financing instruments so as to ensure the right kind of financing for each stage of development of an innovative business. This requires the development of alternatives to bank credit, of limited use in this field. It can be observed how, indeed, in recent years, using formulae similar to those embraced by the main European countries, new forms of alternative financing have proliferated, from the innovation incubators and accelerators devised by large companies (corporate venture capital) such as Telefónica (Open Future) and several of the banks (La Caixa: Caixa Capital Risc; BBVA: BBVA Ventures; Banco Santander: Innoventures; and Banco Sabadell: Bstartup) to expansion of business angels, crowdfunding, alternative stock markets for SMEs and above all venture capital and private equity funds which are growing very rapidly, with an increasing presence of foreign capital. The aforementioned public entities have contributed to their development, as has Spain’s Official Credit Institute, the ICO.

Although this rapid growth in funding has gone some way to reducing the impediments to the creation of start-ups in Spain, these instruments are still substantially less developed than in other European countries. Less developed too is the direct role played by the public institutions in this arena, which continue to play a very small part. Also, the financing issues intensify when companies have moved on from the start-up stage and are looking to grow and expand internationally. The reduction in funds devoted to R&D during the crisis is indicative of this financing difficulty, among other things. Not even the shrinking budgets devoted to research funding were put to full use during the crisis. A common interpretation of this paradoxical situation is that it is a problem of limited demand (from firms). A similar interpretation of the facts results from a passive approach to innovation policy, as already questioned, which assumes that companies demand funds and the authorities are there merely to help get them or offer them directly. However, an analysis of the countries with the best innovation practices ‒ the US, Germany and Korea ‒ reveals that innovation policy is also a supply-side policy, which should stimulate the emergence of new projects and their associated financing needs.

Human capital and management skills

Labour skills have depended largely until now on the education system, which could be significantly improved upon organisationally and quality-wise, as suggested at multiple times. One improvement, crucial in our opinion, is to inject it with a greater business/entrepreneurial bias, firstly by encouraging professional training and its dual character, i.e., learning fuelled simultaneously by the corporate segment and the education system, and, secondly, by encouraging companies to spend externally on training.

This latter idea is very important as the most internationalised companies present employee training costs that are well above the average, which in Spain is very low, as just 25% of industrial companies spend money on training, devoting an average of 0.2% of their labour costs (average expenditure by companies with less than 50 employees is less than 1,000 euros a year, rising to 12,500 euros at companies with between 50 and 200 employees). The figures speak to a certain rejection by business owners of the idea of involving their employees in the company’s tasks and objectives. They also reflect the prevalence of temporary work arrangements, which needs to be reduced if we are to upgrade skills.

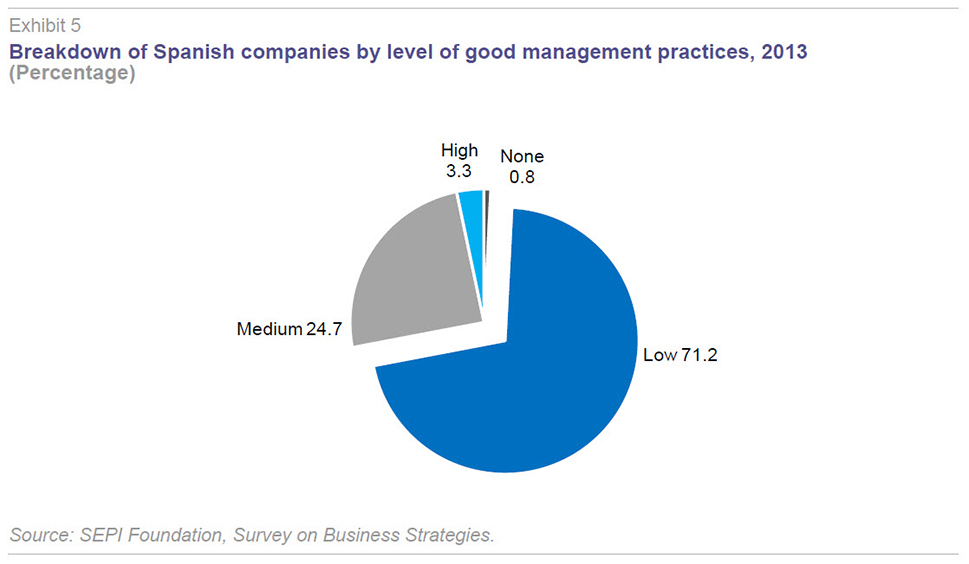

Corporate productivity also depends on the quality of its management skills, which determine how well a company is managed. An examination of multiple indicators of best management practices suggests that in Spain, companies with poor management quality predominate. In our analysis, applied to industrial companies, these companies account for 71% of the total (Exhibit 5). These are companies at which objectives are not well defined, their delivery is not controlled, efforts to learn about new technologies are lean, as are the resources devoted to market analysis/intelligence, to engaging with other peers or experts, to digitalising productive processes or to marketing. So the authorities need to find a way to provide companies with the knowledge and assistance needed to fine-tune their management practices. In reality, all support extended by the public authorities to companies, just as it should be tied to delivery of certain performance undertakings, to some results-driven, measurable conditionality, should be linked to improved management guidelines. The authorities should work with the universe of companies that are willing to do things better, stretch themselves and share the results of their efforts transparently.

The low scores achieved by Spanish companies on the most important aspect of good management practices ‒ leadership ‒ stand out. Definition of objectives and their control, know-how in the area of innovation and environmental demands, outreach by executives, experience and initiative sharing with workers and diversification of markets. Over 60% of manufacturing companies fall short on good leadership practices, presenting low or non-existent levels.

Improving the quality of management is of vital importance because, as already stressed, there is a clear link between this and productivity. Unfortunately, however, this does not depend only on taking direct action in this field (something which is, moreover, not easily done). Good management practices are also fostered by means of innovation and internationalisation policies, as well as measures designed to build company scale (eliminating regulations that encourage staying small) or increase market competition. This is because size, innovation, internationalisation, labour productivity and management quality are interrelated factors. Acting on each has a spillover effect on the rest.

As a result, in trying to eliminate impediments to company growth and regulations that favour staying small, policy should also address innovation, intangible assets, international expansion and good management practices: the upshot will be bigger and more productive companies.

Brand equityAs with human capital and innovation, brand equity is another intangible asset on which Spanish companies fall notably short. Only 20% of manufacturing companies conduct market studies or marketing, which according to our analysis are key to their market positioning.

[1] Industrial policy should champion the creation of private brands with the aim of embedding Spanish products with a good reputation and associating them with quality. Above all, however, it should take advantage of the huge potential implicit in the collective brands (protected designations of origin (PDO), protected geographic indications (PGI), traditional specialities guaranteed and quality seals). And, certainly, Brand Spain. In some sectors, such as the food sector, these collective brands have a major and largely untapped role to play but so far only 12% of agri-food sector companies sell their products under the PDO or PGI quality schemes, representing 1.1% of total sales.

Digitalisation

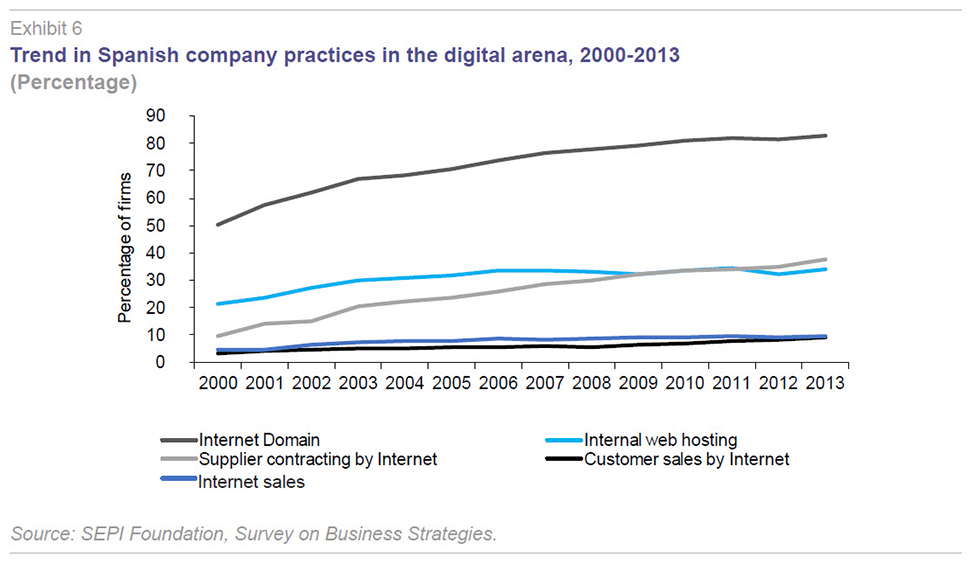

The digitalisation phenomenon is a technological revolution which in reality encompasses multiple technological changes, some of which are advancing swiftly, such as the use of big data, ultra-rapid communication, cloud computing, 3D printing, mass automation and artificial vision, while others are progressing more slowly, such as cognitive computing and artificial intelligence (natural language processing, machine learning and voice recognition). These innovative technologies will become available increasingly rapidly and at a declining cost and will change many products’ existing business models and value chains, from how they are designed to how they are sold and marketed. However, this multiple technology change is not likely to catch Spain’s industrial companies too well prepared judging by the limited progress being made on the most basic developments. Although 80% of companies now use the Internet proficiently, only 30% carry out internal web hosting and the percentage selling online is even smaller (Exhibit 6). Industrial players face a major challenge to their competitiveness, one that is, however, also a great opportunity to reinforce their competitiveness by building it on solid foundations. Here industrial policy has a key and urgent role to play, by helping to activate an intense and complex digitalisation agenda.

Internationalisation

Internationalisation is the other end goal ‒ coupled with productivity ‒ of the programme outlined in the book summarised in this paper. This is aided by boosting productivity but requires vigorous measures for promoting and developing ‘market intelligence’, knowledge of new markets, their characteristics and their players. The experience built up by companies that have already expanded internationally is crucial, which is why it is important for the authorities to reach out to them and involve them in their actions (encouraging business networks, scant in Spain).

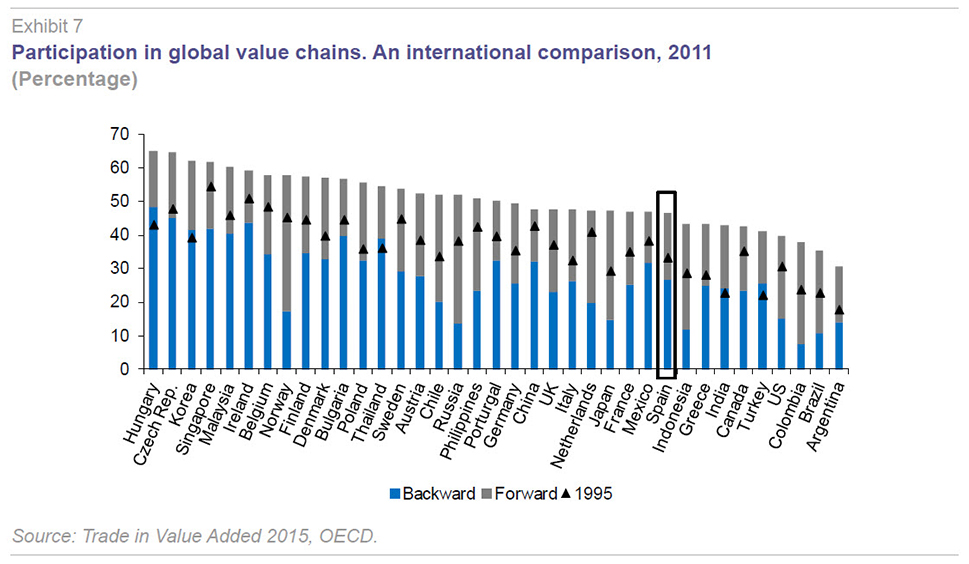

Our research assessed, firstly, the role of becoming integrated in international production networks: the global value chains. Spain’s companies, and not just the industrial ones but also its service providers, have made significant progress on inserting themselves in these chains (Exhibit 7), which has had positive effects on their productivity and the regularity and persistence of their exports. The factors driving business insertion into these global chains were studied, with the following results: a minimum company size threshold is a key enabler; in its absence, however, labour productivity is crucial, once again a decisive factor for SMEs. Product innovation also facilitates involvement in global value chains, as does the presence of international firms in their shareholder ranks or the fact of having manufacturing subsidiaries abroad.

There is room for Spain to improve its presence and position in these global chains, particularly in the links of the chain that add the most value at either end: innovation at one extreme and a sophisticated marketing network at the other.

In the broader sphere of exporting, it is even possible for policy to provide specific sector guidance, as is reflected in our work. Using the analysis performed by Hausmann and Klinger (2007), we looked for products well connected with Spain’s productive system that additionally present high levels of sophistication with a view to identifying new and highly-promising lines of development and tapping the know-how accumulated in Spain’s human capital. Against this backdrop, there are good prospects for diversifying the products Spain exports in some of the sectors that are already highly developed and competitive internationally: the textile and garment industry, food, drink and tobacco, mechanical machinery and equipment, chemical products, scientific and optical instruments and metallic products industries.

There is also scope for the provision of guidance with respect to markets. Generally speaking, the markets to be targeted are relatively obvious considering the fact that the areas set to register the fastest growth in the coming years are already well identified: Latin America, Asia, Africa and the Pacific. A significant effort should be devoted to the Pacific, necessarily overcoming the obstacles posed by a potential shift towards protectionism by the US administration. However, there are also less obvious markets worth exploring for Spanish exports, even if not among the fastest growing.

These export promotion policies should also be targeted at investing abroad, which is just another way of accessing foreign markets that is often more profitable and beneficial in terms of competitiveness, i.e. with important positive ramifications for companies’ productivity and product differentiation. Spanish investment overseas, which registered sharp growth at the turn of the century, has continued to grow, more slowly yet surely, throughout the crisis and there is substantial room for further growth (Álvarez et al, 2016).

Policy attempts to promote investment overseas should prioritise the manufacturing firms, which are lagging in this respect, given that a high percentage of Spanish investment abroad stems from foreign multinationals based in Spain. There is a broad universe of medium-sized enterprises, those with between 200 and 500 employees, which have made no progress on this front in the last 15 years but should.

It is also vital to pay attention at the policy level to attracting foreign capital. Foreign multinationals have played a very significant role in Spain’s industrialisation; and they continue to do so today, increasingly so, as their share continues to rise. Although their presence intensifies Spain’s dependence on imports from other countries, these firms are also active exporters and they help embed Spanish companies in the global value chains. They also stimulate competition in the home market, boosting technological rearmament and generating positive externalities in terms of knowledge which in turn fuels technical progress. It is therefore crucial to draw more foreign capital to Spain and although there is plenty of scope for doing so, it is necessary to modernise the promotion effort, currently spearheaded by the ICEX (Spain’s foreign trade institute).

Final considerations

In short, these brief pages summarise a more extensive study which analyses Spanish industry and the role of industrial policy as the basis for defining a specific programme of initiatives designed to fortify the industrial fabric and increase its contribution to the economy. The basic idea underpinning this programme is to boost corporate productivity and international expansion. Its success depends on a necessarily-reformed public administration, updated for modern times, up-to-speed with the opportunities and threats posed by globalisation, endowed with a breadth of vision, one that is capable of interacting closely with the private sector without bowing to its interests, championing and coordinating initiatives and catching all implicated agents in new cooperative networks. A public administration must possess the skill-sets needed as well as a keen sense of public service.

Notes

This percentage rises to 27% in the food sector which is more directly oriented towards the end consumer.

References

ALVAREZ, E; MYRO, R., and J. VEGA (2016), “La inversión de las empresas españolas en el exterior ¿se reinicia la gran ola expansiva?,” Papeles de Economía Española, nº 150: 2-19.

CHANG, H.-J.; ANDREONI, A., and M. M. KUAN (2013), International Industrial Policy experiences and the lessons for the UK, Centre for Business Research, Working Paper No. 450.

EUROPEAN COMMISSION (2014), “For a European Industrial Renaissance,” Communication from the Commission to the European Parliament (COM/2014/014 final)

FALK, M. (2013), “New empirical findings for international investment in intangible assets”, Working Paper, nº 30, WWWforEurope.

HAUSMANN, R., and B. KLINGER (2007), “The Structure of the Product Space and the Evolution of Comparative Advantage,” CID Working Paper, No. 146.

HUERTA, E., and V. SALAS (2014), “Tamaño de las empresas y productividad de la economía española. Un análisis exploratorio” [Company size and productivity in the Spanish economy. An exploration], Mediterráneo Económico, No. 25, pp. 167-191.

MAZZUCATO, M. (2014), The entrepreneurial state, RBA, Madrid.

MC CANN, PH., and R. ORTEGA-ARGILÉS (2016), “Smart specialization: Insights from the EU experience and implications for other economies,” Journal of Regional Research, No. 36, special edition, pp. 279-293.

RODRIK, D. (2004), “Industrial policy for the twenty-first century,” in One economics, many recipes, Princeton University Press, pp. 99-151.

WEIS, J. (2011), The Economics of Industrial Development, Routledge, New York.

Rafael Myro. Universidad Complutense, Madrid. This paper is a short summary of the book published under the same name by the Economic and Social Council in November 2016. It is the result of a broad group investigation directed by the author