‘Japanisation’ of Europe: Takeaways from Japan’s banks, 15 years later

The persistence of zero interest rates and stubbornly low inflation in the eurozone mirrors the two-decade long situation in Japan. For this reason, it is possible to glean some lessons from the experience of Japanese banks and anticipate what might lie in store for eurozone banks’ net interest margins, business volumes and profitability levels.

Abstract: With the eurozone’s Main Refinancing Operations rate having stagnated at zero percent, inflation has remained frustratingly below the ECB’s target of ‘below but close to 2%’. The situation has notable parallels with Japan, where interest rates have lingered at 0% and inflation below 2% for two decades. For this reason, it is pertinent to consider lessons that could be drawn from Japan and to gain insight into what might lie in store for Europe’s banks. The persistence of ultra-low interest rates in Japan has exerted systemic downward pressure on banks’ unit margins. Interestingly, European banks’ net interest margins are currently the same as those achieved by Japanese banks in the early years of the century. Since then, however, Japanese banks’ net interest margins have fallen to around 0.6-0.7%. Japanese banks do benefit from two advantages not shared by their European counterparts, namely lower NPL ratios and a far lighter cost structure. Turning to profitability levels, Japanese banks have achieved a reasonably low, but stable, ROE of between 5% and 7%. Meanwhile, capitalisation levels are below those of European banks, where ratios of capital to assets have increased by over 50%. This divergence could be due to the difficulty for Japanese banks to raise capital in light of offering such a low ROE, and/or less stringent regulatory capital requirements in the context of a low volatility/low risk climate.

Zero rates in Japan and the EZ: 15 years of hindsight

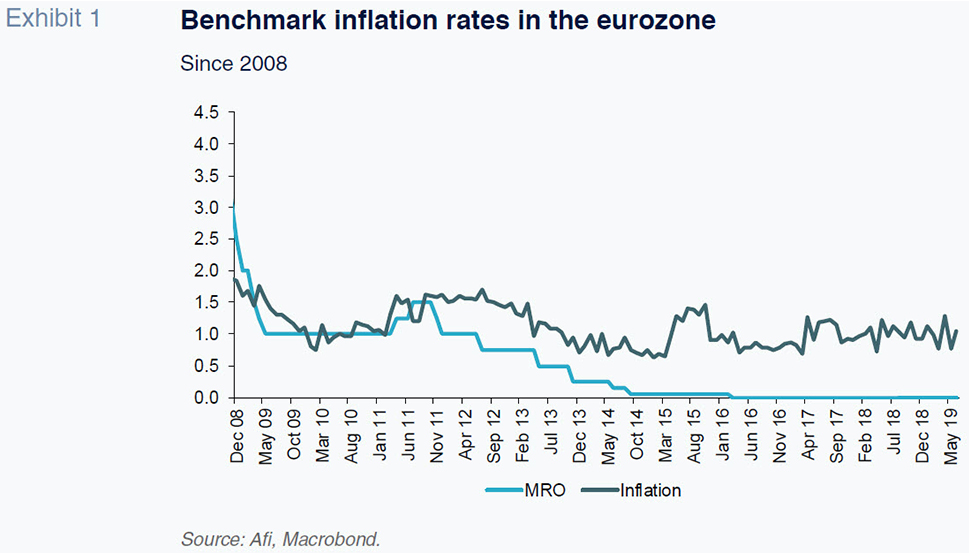

The ECB reduced the rate on its main monetary policy instrument, known as the Main Refinancing Operations (MRO) rate, to zero percent a little over five years ago. Before that, it had cut rates aggressively in response to the crisis (from 4% to 1%). In 2011, it made the decision to raise the rate by half a percentage point (to 1.5%), reversing it just a few months later. Further cuts then followed, with the rate ultimately falling to 0%, where the MRO has stood for nearly four years now.

That zero-rate policy, complemented by other non-conventional measures - successive rounds of LTRO/TLTRO; negative rates on the deposit facility; the massive asset buyback programmes,

etc. - have not been enough to increase inflation in the eurozone (EZ) to the targeted goal of “below but close to 2%”. This is by no means a criticism of the ECB’s actions; to the contrary, had it not intervened in the manner it did, the narrative would probably be considerably worse. Nevertheless, it must be acknowledged that the marginal effects of additional measures are clearly diminishing. For this reason, it is useful to examine a longer track record pursuing a similar inflation target.

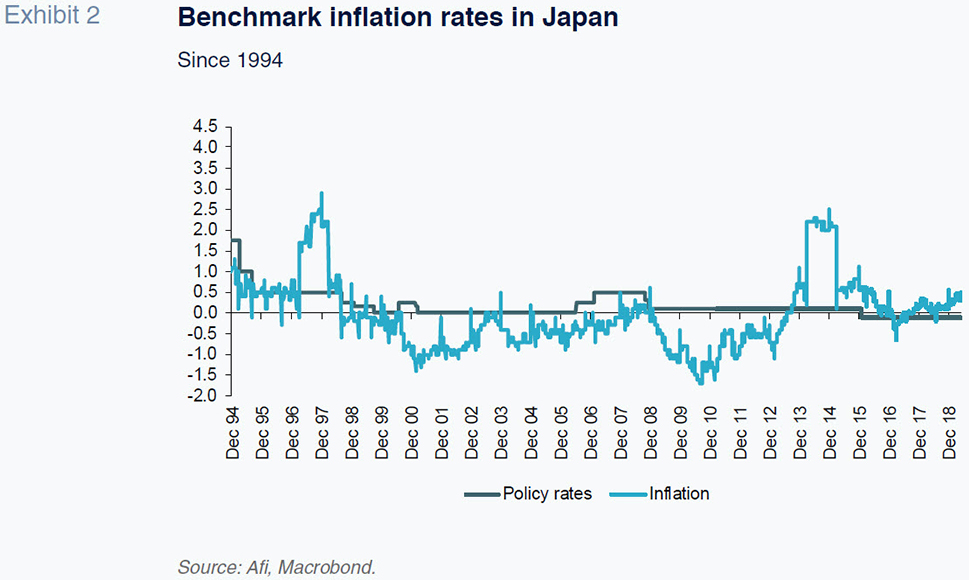

Specifically, the Bank of Japan (BoJ) embarked on an aggressive series of benchmark rate cuts in 1993. Its policy rate would reach zero percent in 1999, where it has remained ever since. The BoJ attempted to raise rates twice, in 2000 and 2006. Those attempts had to be abandoned in the context of wholly unanchored inflation expectations. During the last 25 years, inflation has only topped 2% for two short periods of time, heavily influenced by the fiscal policies implemented by the Japanese government. Indeed, episodes of negative or scantly positive inflation, such as that observed during the last four years, have been far more common.

Putting structural considerations and other differences aside (demographics, expansionary fiscal policies, etc.), a prolonged period of zero percent rates lies in store for the EZ. Given that prospect, we believe it is pertinent to analyse how Japanese banks have fared in a similar environment and to compare the situation with European banks.

Banks and zero rates: The eurozone following in Japan’s footsteps

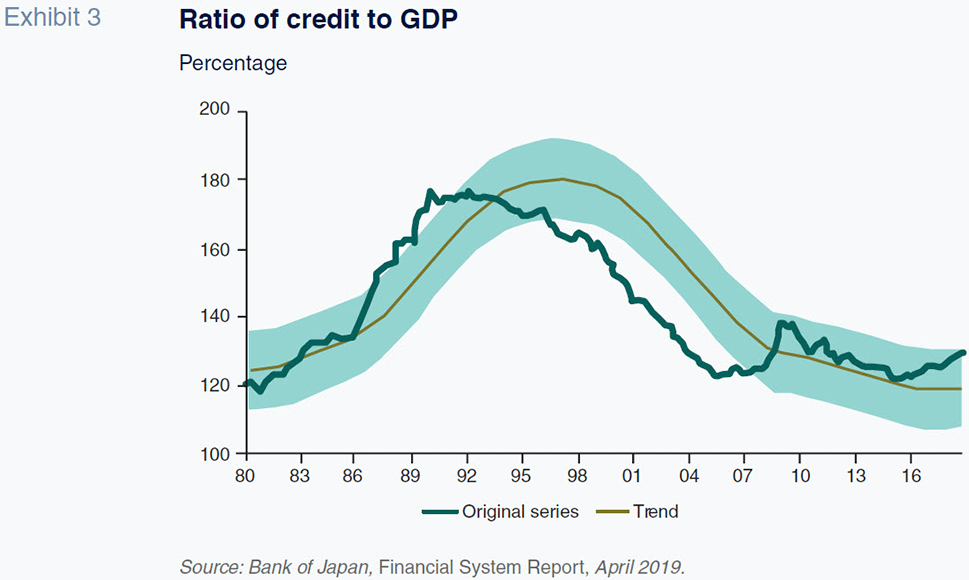

If interest rates in the EZ emulate those of Japan with a 15-year lag, we should be able to draw conclusions about the banks’ future by analysing their balance sheets, specifically in terms of the weight of loans in the overall economy, as depicted in Exhibit 3. The ratio of credit to GDP peaked in Japan (at close to 170%) in the mid-1990s and was followed by a long period of intense deleveraging over the course of more than a decade. Credit to GDP eventually settled at around 130% of GDP, a level at which it has been stable for the last decade, with credit growing in line with GDP,

i.e., at between 1% and 2% per annum.

In the aftermath of previous excesses (the bubbles of the 80s and early 90s), Japanese banks have seen business volumes grow, albeit reduced and balanced (in terms of GDP). As a result, the banks have avoided unpleasant surprises in terms of risk, having absorbed the adverse legacy left behind by the historical crisis of the 80s.

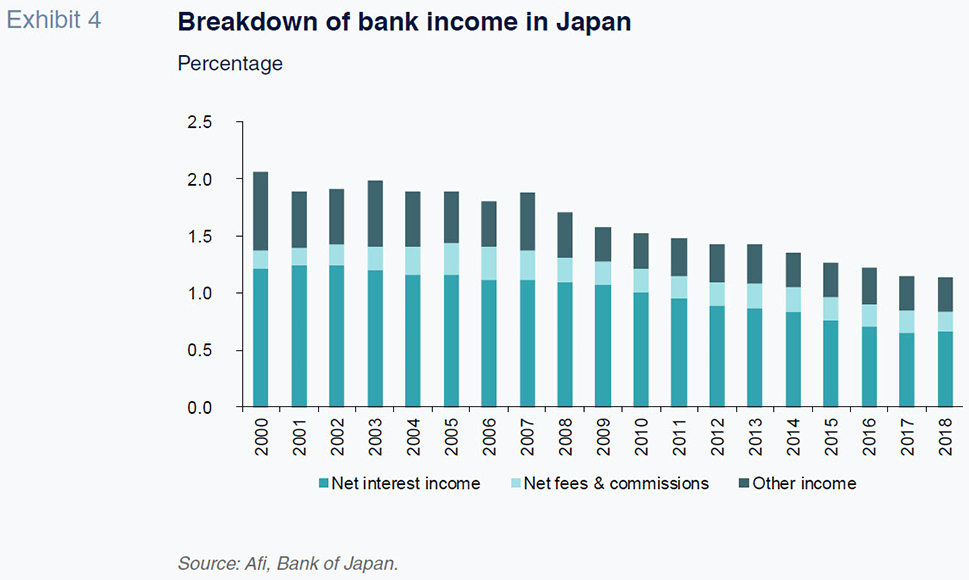

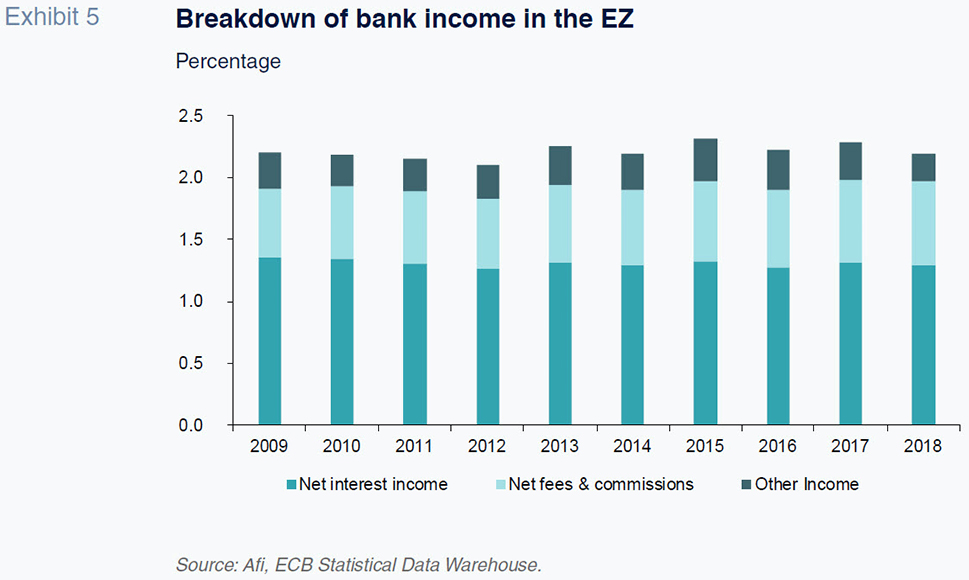

In that business climate, the fact that interest rates have remained at zero for nearly two decades has exerted systematic downward pressure on Japanese banks’ unit margins. These dynamics are evidenced in the following exhibits, which compare the performance of Japanese banks (since 2000) against that of their European counterparts (since 2009). Note that European banks’ net interest margins are currently the same (approximately 1.2%) as those achieved by the Japanese banks in the early years of the century. However, since then, Japanese banks’ net interest margins have fallen to around 0.6-0.7%.

The gross value of net interest margins includes fee and commission income, which is low in Japan (around 0.3% of assets, less than half the percentage presented by European banks), and other income, mainly from holding and trading securities, a source of revenue that is somewhat more significant in Japan compared to Europe.

The sum of these components yields the gross margin, which since the turn of the century and the introduction of zero rates, has fallen in Japan to 1.2% from 2%, the level currently reported by European banks.

Faced with such depressed margins, Japanese banks have exhibited two advantageous factors in comparison with their European peers. Firstly, the virtual absence of non-performing loans, and thus a scant provisioning burden. Granted, this occurred after having dealt with the toxic assets left behind by the crisis of the 80s and 90s, when their NPL ratios had topped the 10% mark.

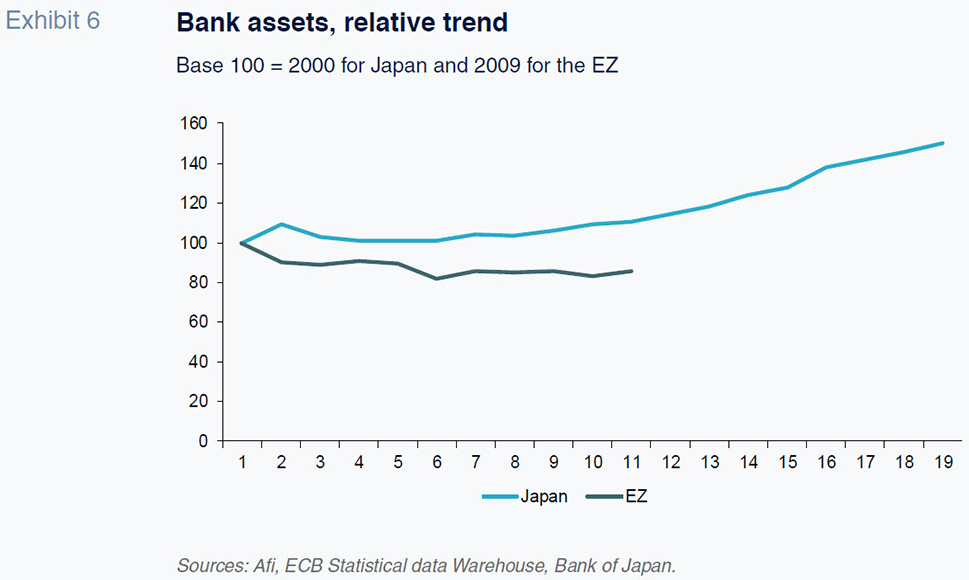

Secondly, a far lighter cost structure, in terms of personnel and general expenses, compared to European banks. Specifically, the expense-to-assets ratio of 1.4% currently presented by European banks is closer to that reported by the Japanese banks in 2000. Since then, Japanese banks have brought this metric down to 0.6%. However, this trend has been helped by growth in assets held by Japanese banks over the last decade, growth which has yet to be mirrored by European banks.

The growth in assets held by Japanese banks in recent years indicates that these entities have orientated their business strategies towards volume growth (positive volume effect for net interest income) to offset lower rates on new loans (negative rate effect).

Conclusion: Profitability and solvency

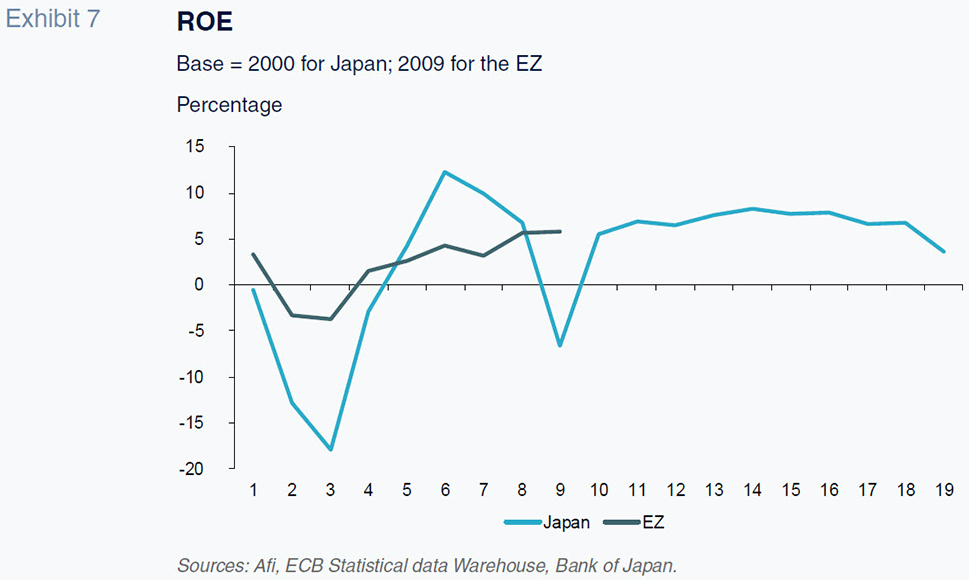

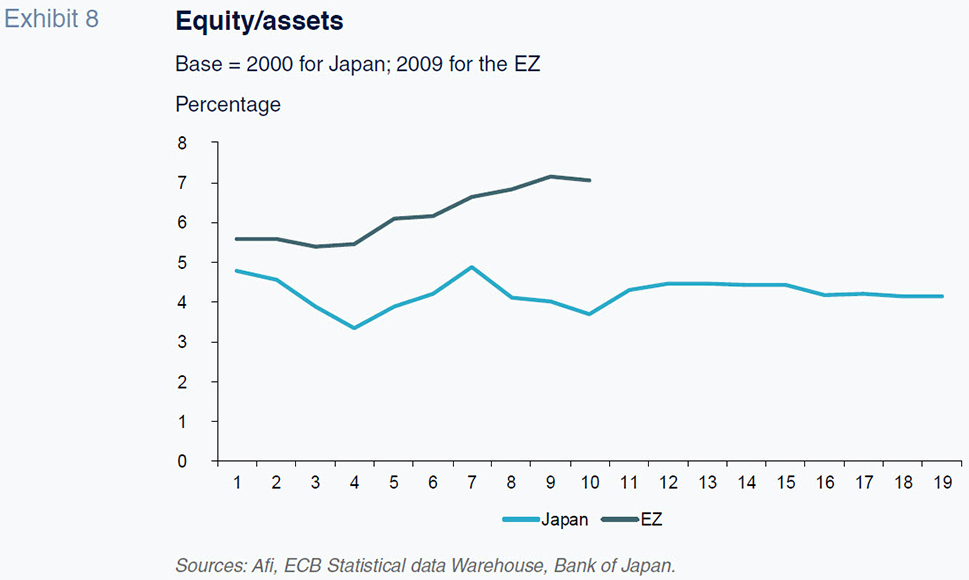

Aggregating the above metrics (asset volumes, margins as a percentage of assets, expense structure and risk cost) yields the key parameter in determining the viability of a bank or a banking system as a whole, namely its ability to generate a return on the capital it is required to hold. Exhibit 7 compares the return on equity (ROE) in Japan and the EZ over different time horizons in each instance: from 2000 for Japan and from 2009 for the EZ. Exhibit 8 illustrates the same trend in terms of the weight of equity over total assets, which is a proxy for solvency without risk weighting.

Two conclusions jump out from these comparisons. In terms of profitability, the decade lead commanded by Japan over Europe has translated into a reasonably stable yet reduced ROE, of between 5% and 7%. It has tended towards the lower end of that range in the last two years and at no time veered towards the 10% mark, which is often cited as the cost of capital required by the market in order to invest in bank stocks.

This observation leads us directly to the second conclusion, drawn from the comparison between the two systems’ ratios of capital to assets. While in Europe that ratio has increased by over 50%, largely in response to tighter regulations in the wake of the crisis, in Japan the capital ratio has remained stable at a level that is well below the European ratio.

One possible reason for the Japanese banks’ low capitalisation could be the difficulty in raising capital when offering such a low ROE, in light of the prevailing growth in business volumes. Alternatively, in an industry exhibiting such low volatility and credit risk as the Japanese banking system for more than a decade, it is feasible that the supervisor no longer needs to insist on higher levels of capital.

References

Ángel Berges, Federica Troiano and Fernando Rojas. A.F.I. - Analistas Financieros Internacionales, S.A.