The Spanish and European banking sectors today and prospects for 2017

Although market conditions and profitability/asset management challenges remain real risks for the Spanish banking system, the intense effort in these areas by Spanish institutions places them in a relatively strong position compared to their European peers. Assuming the solvency and transparency issues currently affecting other European countries are resolved, 2017 should bring a more benign market environment for Spanish banks, which could translate into improved profitability and value creation for shareholders.

Abstract: Spanish listed banks’ latest earnings result demonstrates their ability to record profits even in the face of hostile market conditions since early 2016. Spanish banks’ profits, as well as share prices, have fared relatively better than those of the their European counterparts. Non-performing assets in the Spanish banking system have contracted by 38% since December 2013. Meanwhile, their common equity tier 1 (CET1) capital ratio remains above 12%. This combined improvement in asset quality and solvency has placed Spanish banks in a better position to tackle the profitability challenge. Indeed, the intensity of restructuring already undertaken and the depth and transparency of the asset provisioning effort have emerged as competitive advantages. As European markets foreseeably stabilise and financial stability issues surrounding some countries, such as Italy, are resolved, it is likely that we will see even greater concentration within the sector. It is also possible that European bank profitability will improve somewhat in 2017, although it remains to be seen how banks will adapt to a changing monetary environment, albeit still expansionary.

The monetary and financial climate and international scrutiny

2016 is drawing to a close, having proven a tough year for Europe’s financial institutions. It was thought that 2016 would be a year of transition towards a more solid financial environment and a more robust recovery in lending and the banking business as a whole. However, expectations at the start of the year were ultimately confounded by the market reality. Securities markets exhibited signs of stress as early as January and bank stocks were among the hardest hit. This convulsive market environment lasted until well into the summer and it was not until the autumn that signs of gradual recovery, albeit not exempt from episodes of volatility, began to emerge.

This difficult transition can be attributed to a host of factors. Firstly, in the year in which the banking union’s Single Resolution Mechanism (SRM) entered into force, the challenges that are already putting it to the test were quick to emerge. When articulating the single supervision mechanism for the eurozone, it was thought that the recapitalisation and provisioning efforts made would give way to an era of enhanced transparency. However, it would appear that the stress tests conducted by the European Banking Authority this year, in coordination with the European Central Bank, have not had the desired effect. In fact, as indicated in the last edition of the Spanish Economic and Financial Outlook, questions have emerged about the quality of bank assets in Germany; meanwhile, and more worryingly, the existence of a major banking crisis in Italy has become clear, a crisis for which a definitive solution certainly remains pending. The result of all of this has been, yet again, to cast a shadow over the credibility of the sector as a whole due to the doubts circling a few. It is worth noting, at any rate, that although management of the legacy of impaired and non-performing assets left behind by the banking sector crisis still has some way to go, much has been achieved on this front.

Interest rate conditions and the role of the main central banks is also proving key. Beyond the impact of weak political stability in many countries and elections having recently taken place or planned in others, the monetary climate remains unprecedented. The possibility that the Federal Reserve will hike its benchmark rates before year-end is a development particularly worth watching. Some analysts maintain that monetary policy needs to take a definite step in the direction of tightening for private liquidity to gradually take the place of public support. The uptick in inflation is sending a positive signal in this respect. Although recent ECB talks would appear to suggest the existence of a time limit on quantitative easing in Europe, it is far less clear how private agents and markets will react to this prospect in light of the weak nature of the economic recovery in the eurozone as a whole and onerous public and private borrowing levels in many nations. Nor is this situation helping matters for the banks because the interest rate equilibrium does not correspond to the crossover between demand and supply adjusted for risk but rather reflects the actions of the European Central Bank, which is injecting liquidity and driving rates to ultra-low levels. Generating a reasonable net interest margin in this context is undoubtedly a difficult task.

The forces of supply and demand are however hovering in the background, with two important drivers of change in the near-term horizon. The first is the persistence of excess supply. The restructuring process continues in the countries in which it started earlier (e.g., Spain), while it is still now even greater in the countries where it had been limited to date (e.g., Germany, Italy, Netherlands). The second is technological change, namely the scope for accessing customers and providing services using unconventional channels associated with the digital transformation. Although customers still have to embrace some of these changes, the transformation is unquestionably gathering pace and the financial institutions are tangibly upping their stakes in this arena.

The Spanish banks are relatively well placed compared to their European peers. They have proven able to steer a course to recovery, reporting profit growth in the third quarter of 2016, despite the market difficulties. They have also stayed ahead of a good number of the changes now being tackled by the sector in Europe, standing out on two fronts: restructuring and asset quality transparency. On October 24

th, 2016, the staff of the ECB and the European Commission published a joint statement following the sixth post-programme surveillance visit to Spain.

[1] In it, the staff highlights the fact that the financial sector “has continued to show a high degree of stability, supported by low funding costs, the ongoing restructuring of the sector and the strength of the economic recovery (...) The quality of banks’ assets has further strengthened and by mid-2016, the non-performing loan ratio had fallen below 10% at the aggregate level.

The staff also notes that the main challenge for the sector, “as in other euro area countries, remains sustaining profitability over the medium term, against the background of low interest rates and still negative growth of business volumes. Although the outstanding volume of credit is still decreasing, also reflecting the continuation of the deleveraging process by households and enterprises, new bank lending to households and SMEs continues to grow and supports economic activity.”

Lastly, the staff allude to the bank restructuring process in Spain, remarking that “implementation of the restructuring plans of the Spanish banks that have received state aid is almost completed. However, there has been no progress in the re-privatisation of the two remaining state-owned banks since 2014.”

Outlook for profitability in the Spanish bank sector

The comments made by the ECB and EC staff allude to a key factor for the Spanish banks: prevailing low interest rates may be having a greater impact on the reduction in private borrowing levels than on the generation of new credit and, although this phenomenon is beginning to revert, it has delayed the generation of new funding for the reactivation of productive investment. However, this opportunity cost, sparked by accelerating private sector deleveraging, will become a plus in the long term as it will enable doing business at more manageable borrowing levels, as will be seen further on.

The outlook for bank profits is somewhat more promising than it has been in recent months insofar as Spanish banks are combining a lighter and more cost-efficient service structure with a strategic shift in distribution channels and determined management of outstanding impaired and non-performing legacy assets. In its most recent

Financial Stability Report, dated November 2016,

[2] the Bank of Spain highlights certain factors that support this prognosis:

- Non-performing bank assets had come down by 38% between December 2013 and June 2016.

- The common equity tier 1 (CET1) capital ratio remains above 12%.

- At the consolidated level, the entities’ total assets were 0.4% higher year-on-year as of June 2016. This growth is the result of increased activity internationally (growth of 15.5% in international financial assets), offsetting continued contraction in Spain (-2.2%).

- Using European Banking Authority data, the Financial Stability Report shows that the Spanish banks’ exposure to sovereign bonds is in line with the European average (13% of all exposures vs. 11.5% across the EU), with a level of exposure to home-country sovereign risk (57%) that is higher than the European average (48%) but not dissimilar to the percentages presented by the German, French and Italian banks.

- As for asset quality, the Report notes that foreclosed assets originating from the banks’ Spanish businesses (81 billion euros) had declined by 1.4% year-on-year as of June 2016, extending the downtrend, albeit modest, of recent years. In total, ‘unproductive’ assets (the sum of non-performing and foreclosed assets) have declined by 12%, although still at around 199 billion euros as of June 2016). Refinanced/restructured loans were down 12.1% year-on-year as of June 2016, and down 26% since March 2014.

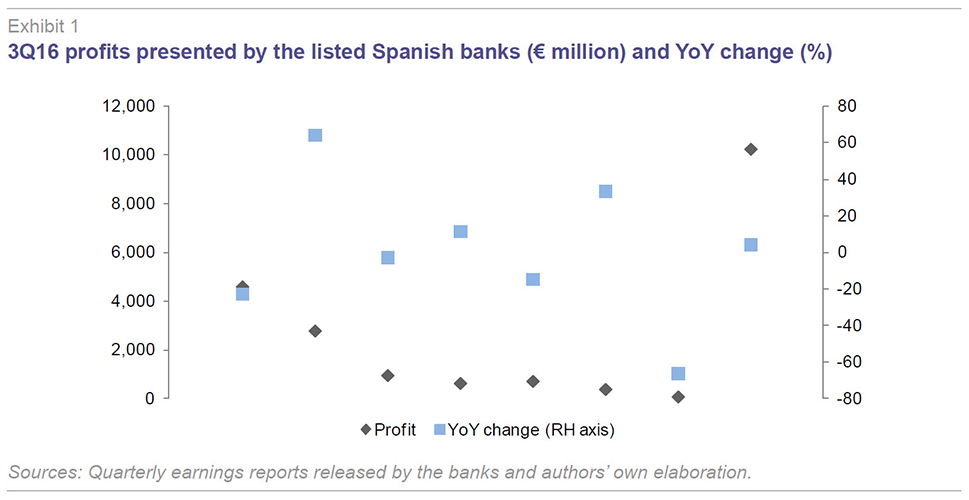

The Spanish banks presented their third-quarter 2016 earnings throughout the month of October. As shown in Exhibit 1, the universe of listed banks as a whole presented third-quarter profits of 10.25 billion euros, marking year-on-year growth of 4.4%. Although profit generation was uneven, affected moreover the impact of the numerous non-recurring, earnings-impacting transactions undertaken between 2015 and 2016, all of the banks presented a profit in a delicate market environment, in contrast to the losses reported in other European markets.

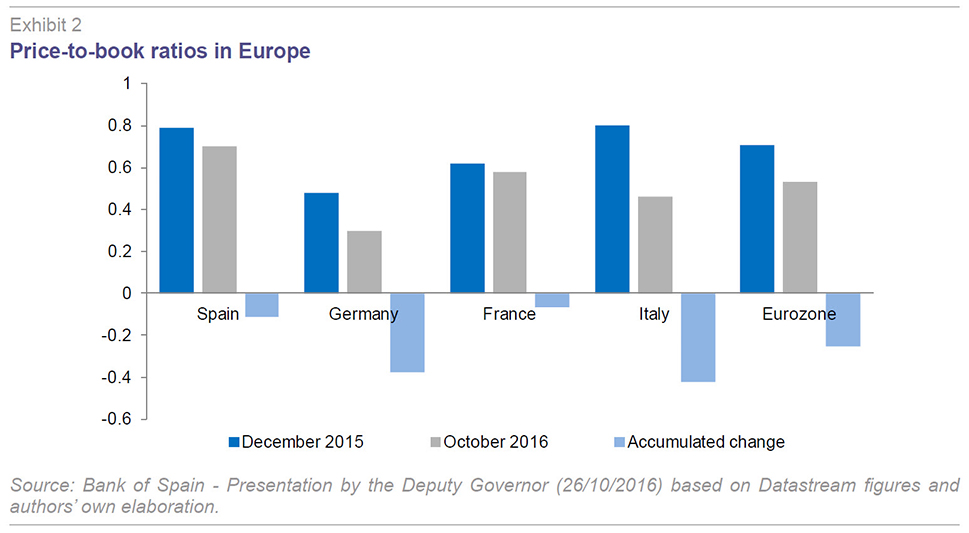

And although stock market falls have been widespread across Europe in 2016, as Exhibit 2 illustrates, the price-to-book ratio presented by the Spanish banking industry is among the highest within the major European sectors: at 0.7x, it is higher than that of Germany (0.3x) or France or Italy (between 0.5x and 0.6x).

Although there is no consensus in the investment community in this respect, a growing number of analysts are ranking Spanish banks among the institutions trading at a discount and therefore presenting significant upside in 2017, particularly if the questions regarding asset quality in other European sectors can be resolved.

Structural indicators and sector concentration

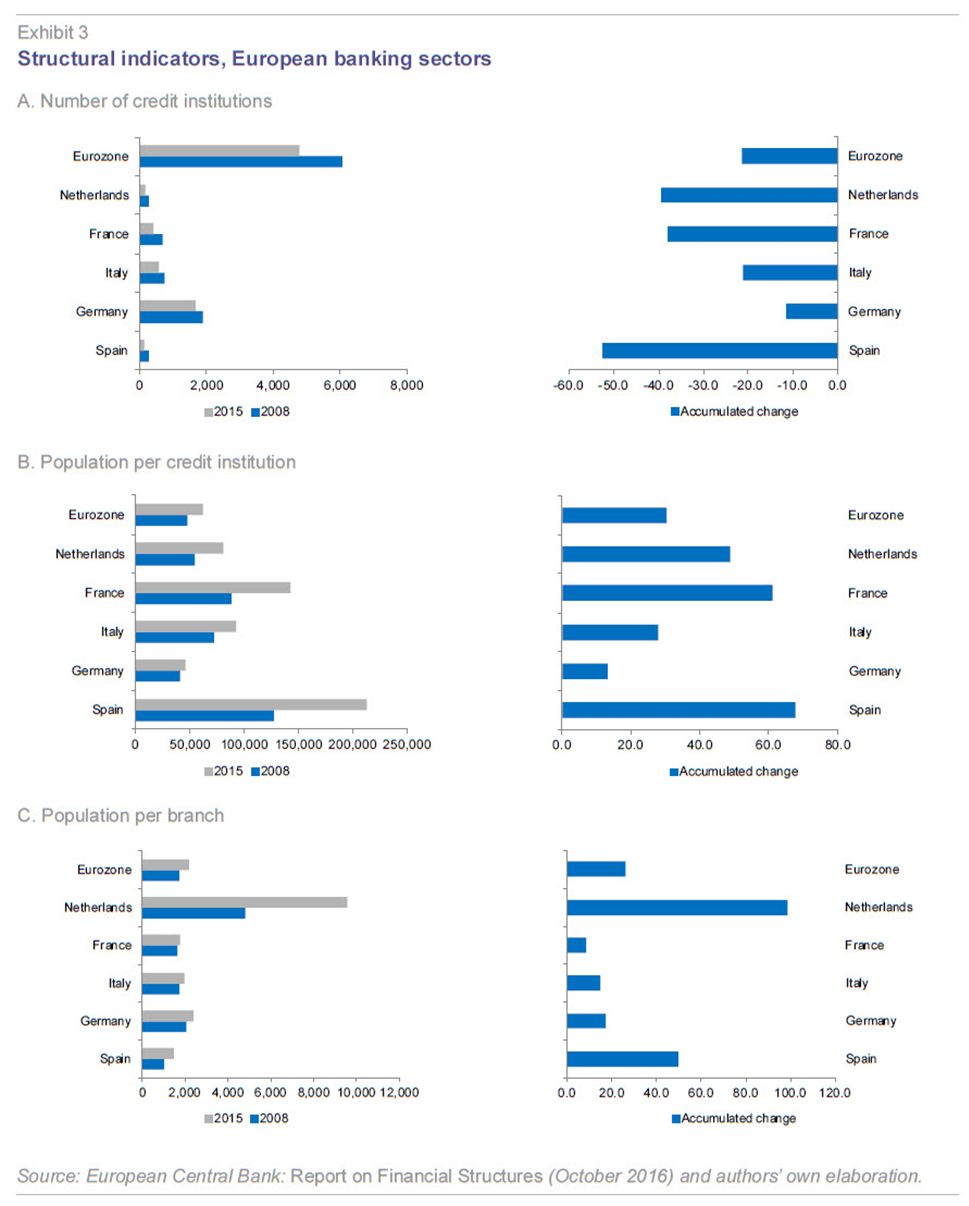

In order to evaluate the state of the European banking industry from a structural perspective, it is worth analysing the sector’s transformation since the onset of the crisis, particularly since 2008. Exhibit 3 uses figures from the ECB’s Report on Financial Structures (published in October 2016), which provides a full spectrum of structural indicators for the purpose of evaluating the transformation undertaken and its intensity in different countries:

- The number of credit institutions in Spain declined from 282 in 2008 to 134 in 2015, or 52.5% on aggregate. This contraction is more pronounced than that witnessed in the other countries analysed, the eurozone average being 21.3%.

- The reduction in the number of players has had a direct impact on the population per credit institution statistic, which increased in Spain from 127,025 people in 2008 to 212,963 in 2015, a cumulative increase of 67.6%, again above the eurozone average of 30.4%.

- Similarly, the population served per branch increased, specifically from 998 people in 2008 to 1,493 in 2015, albeit still implying a more exclusive level of customer service compared to the eurozone average (2,170).

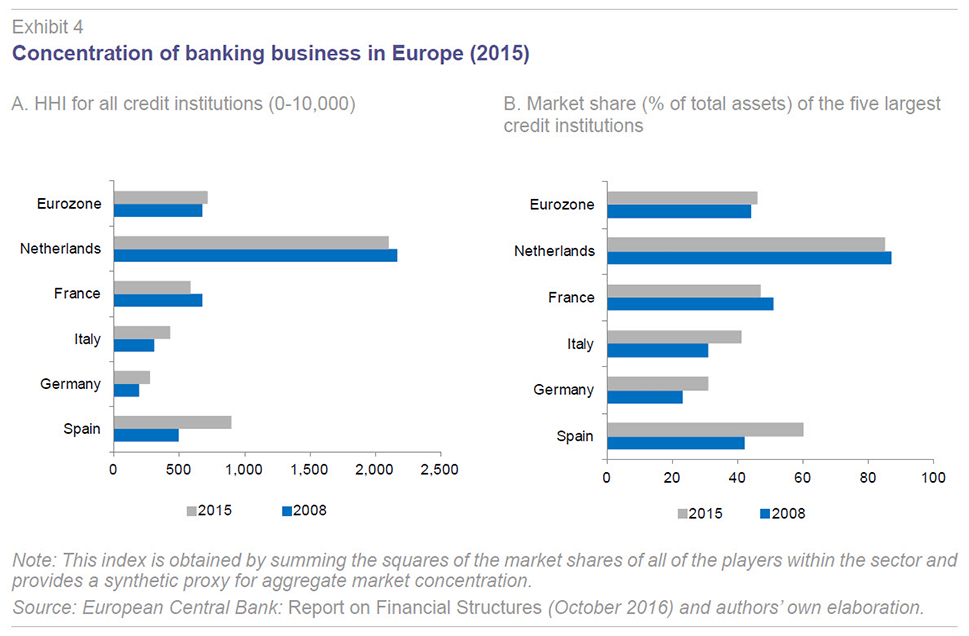

The reduction in the universe of competitors is attributable to increased concentration in the sector. Such a phenomenon is foreseeable and customary during periods of surplus supply and does not significantly impact competition in the sector, which is intense in the traditional segments. The first sub exhibit within Exhibit 4 illustrates the Herfindahl-Hirschman Index (HHI) of bank concentration for several European countries. This index is obtained by summing the squares of the market shares of all of the players within the sector and provides a synthetic proxy for aggregate market concentration. The resulting measure ranges between 0 and 10,000. Despite the increase in the concentration level and in the share commanded by the top five banks in most of the markets (the second sub exhibit), concentration remains relatively reduced in Spain, with a HHI measure of 896, in line with the eurozone average of 722.

Credit, debt and financing alternatives

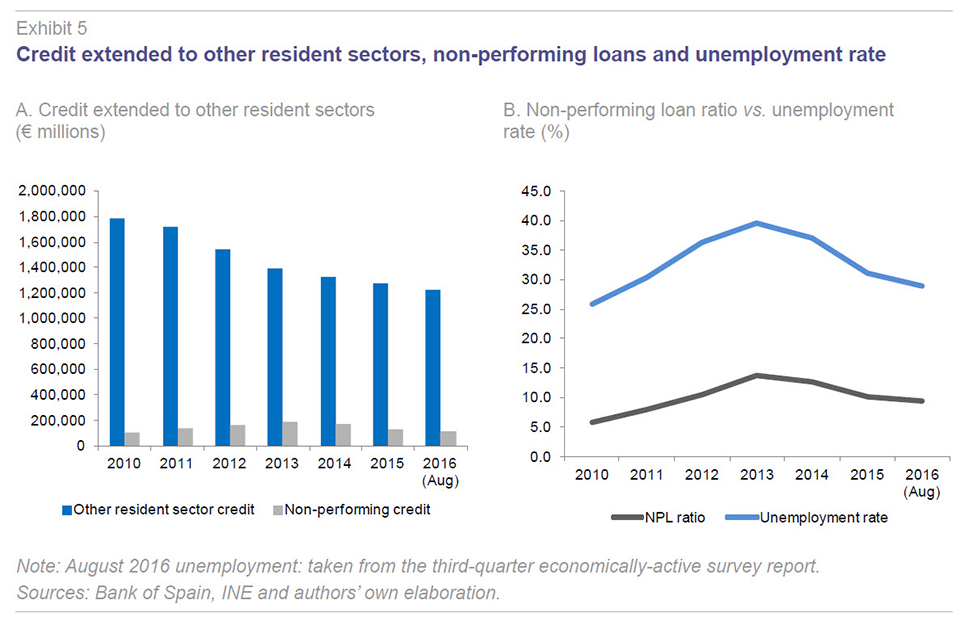

As for new business generation, the overall balance of credit extended to ‘other resident sectors’ continues to fall. As already noted, this trend is due mainly to intensifying debt repayment, offsetting growth in new loans to corporates and households.

Exhibit 5 depicts the trend in total outstanding and non-performing private sector credit (5A) and compares the trend in the non-performing loan ratio and the unemployment rate (5B). By June 2016, the NPL ratio had dipped below 10% and by August it had reached 9.44%. It is likely that the reduction in the NPL ratio will gather pace in 2017 and beyond for two reasons: i) the unemployment rate is expected to continue to decline significantly; and, ii) the balance of outstanding bank credit is set to increase which, as the denominator in this ratio, will drive an even greater reduction.

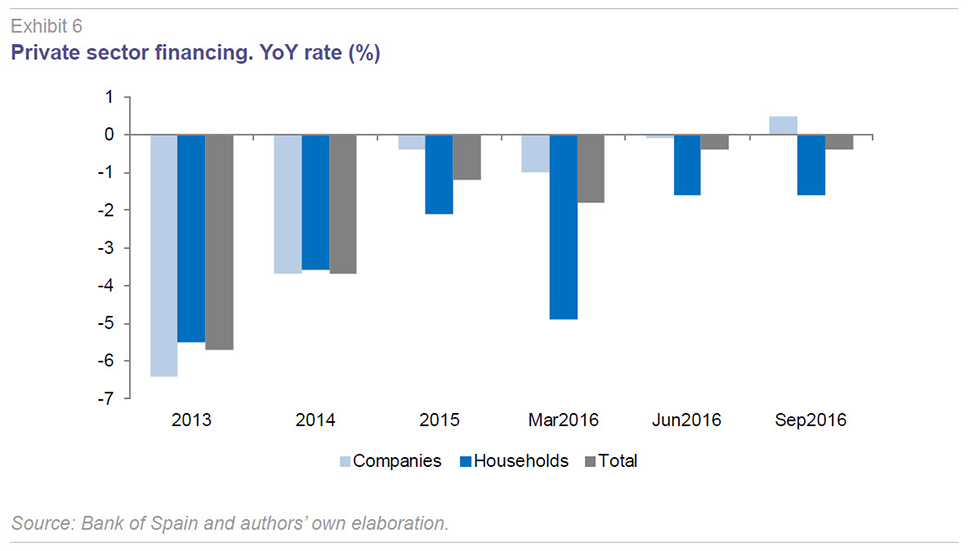

The latest private sector financing figures reveal that outstanding credit is already rising in the corporate lending segment (+0.5% YoY in September); in the household segment, while improving, the overall balance continues to decline (-1.6% YoY in September).

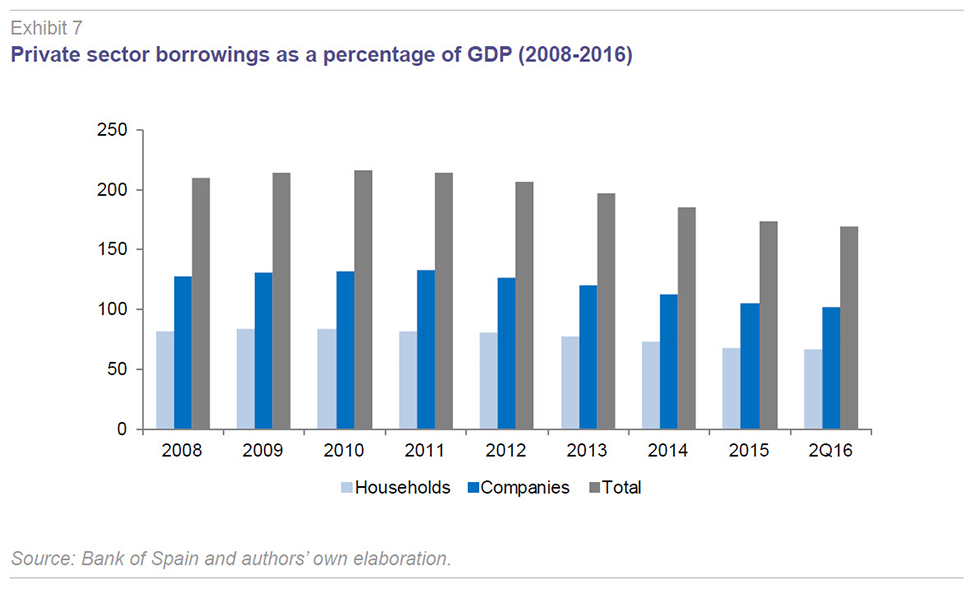

As already noted, part of the still-persistent decline in the overall balance on loans to the private sector is attributable to the accelerating pace of deleveraging. The leverage ratio presented by households and corporates on aggregate (Exhibit 7) had declined from 215.7% of GDP in 2010 to 169% by June 2016. This means that Spain’s households and companies have repaid 480 billion euros of debt in just six years.

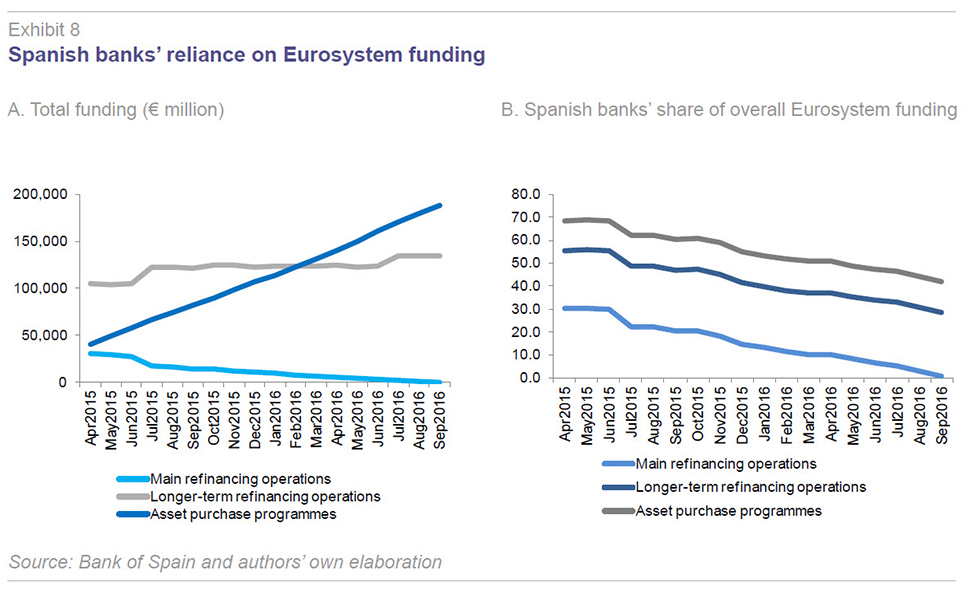

Turning to 2017 and the possible shift in monetary policy in the medium and longer term (albeit set to remain expansionary for a considerable period of time), it is important to assess to what extent the Spanish banks have reduced their reliance on the Eurosystem for funding. Exhibit 8 shows how, in line with other European countries, the asset purchase programmes (including the public sector purchase programme) have gradually garnered the bulk of the banks’ demand for funding. Spain had availed of 188.4 billion euros of funding under these programmes as of September 2016. Use of longer-term refinancing operations (LTROs) had diminished to 134.5 billion euros and use of main refinancing operations (MROs) was negligible. Notwithstanding this trend, as illustrated by 8B within Exhibit 8, Spanish banks have reduced their reliance on the Eurosystem’s liquidity mechanisms relative to the eurozone as a whole, particularly in the last year.

In conclusion, although market conditions, profitability and asset management related challenges remain real risks for Spanish banks, the extra effort made in these areas by Spanish institutions places them in a position of relative strength compared to their Eurozone peers. Foreseeably, assuming the solvency and transparency issues affecting other European countries are resolved, 2017 should bring a more benign market environment for Spanish banks which could translate into value creation for shareholders. It is also possible that the sector will achieve private sector credit growth and, as a whole, a relative improvement in profitability, although this remains the biggest challenge facing the sector in the medium term.

Notes

Santiago Carbó Valverde. Bangor Business School, Funcas and CUNEF

Francisco Rodríguez Fernández. University of Granada and Funcas