2025 budget: At an impasse over financing for Catalonia

The probability of a second consecutive budget carryover in 2025 is high, with the main obstacle to approval constituted by the new financing framework under negotiation for the Catalan region. As a result of the tense climate created by these negotiations, the government is having a hard time getting approval for the ceiling on non-financial spending, the first prerequisite for passing a budget for 2025.

Abstract: The probability of a second consecutive budget carryover in 2025 is high, with the main obstacle to approval constituted by the new financing framework under negotiation for the Catalan region. The new framework would give this region similar status to the accords in place in the Basque region and Navarre, which are outside of the so-called common regime that currently encompasses Spain’s 15 other ‘autonomous regions’. Catalonia’s exit from the common regime would leave the state with as much as 22 billion euros less for regional redistribution. As a result of the tense climate created by these negotiations, the government is having a hard time getting approval for the ceiling on non-financial spending, the first prerequisite for passing a budget for 2025.

The new financial accord for Catalonia: An obstacle for the next budget

On 16 July, the Spanish Cabinet approved the non-financial spending ceiling for 2025, along with new deficit and debt targets for 2025 to 2027. The spending ceiling is a compulsory step in the process of presenting and debating the budget in Parliament. However, against expectations, the spending threshold was not ratified in the Lower House one week later. As a result, the 2025 budget is, at the time of writing, at an impasse. The failure to secure the majority Parliamentary vote needed to pass the spending threshold was the result of votes against it by Junts per Catalunya, one of the partners of the ruling socialist party’s minority government, which demanded greater leeway around the regional government deficit. Specifically, 0.1pp more than the 0.1% deficit approved by the Cabinet.

However, the obstacles facing the government in pushing the budget through go beyond a simple falling-out over the allocation of deficit targets among the various levels of government, particularly because the bulk of the consolidation effort looming in 2025 and beyond will fall on the central government. Political complexities in Catalonia have been tensing different aspects of national politics, including the state budget dynamics, for months now. The decision to call early elections in that region last March already led the President, Pedro Sánchez, to renounce the 2024 budget in anticipation of the failure to gain the support of his government’s Catalan partners. As a result, the 2023 budget has been carried over to this year. Moreover, as part of the government deal reached in the wake of those regional Catalan elections, PSOE and Catalan party Esquerra Republicana agreed a new financing framework for the region of Catalonia which was coined a ‘singular financing system’. In this new system, Catalonia would have its own taxation system and taxation authority which would have no ties whatsoever with their national counterparts. The precise impact on tax revenue of the region’s exit from the common regime will depend on the specific terms and conditions agreed upon, the details of which have not yet been made public. Specifically, there is no information about how the region will pay for the services the state provides in Catalonia. Or about how Catalonia will contribute to the so-called inter-regional solidarity mechanism. Nevertheless, De la Fuente (2024) has estimated that the region’s exit from the common regime will cost the system around 2.1 billion euros. On top of that, the state would cease to collect up to 22 billion euros in Catalonia. The creation of a Catalan tax agency is no small matter as it will have direct effects on fraud control efforts nationwide, depending on the impact on the level of collaboration with the state tax agency (AEAT).

There is broad consensus in the academic world that the new tax regime for Catalonia would be, in essence, similar to the economic accords in place in the Basque region and in Navarre. However, the Spanish Constitution only explicitly contemplates that possibility for those two autonomous regions. Legal matters aside, approval of an accord for a region other than the Basque region and Navarre would have adverse effects on inter-regional solidarity among the remaining autonomous regions, by leaving the central government with fewer resources to distribute among the common regime regions with higher financing requirements. The new accord will create losers, especially among the regions, such as Andalusia, Valencia or Murcia, that have been struggling with underfinancing problems for years due to the failure to reform the common regime, unresolved since 2014.

To tackle this situation, the government has announced that it will double the funds it contributes to the so-called Interregional Compensation Fund (FCI for its acronym in Spanish) which is funded exclusively from state money. However, the FCI is, from a financial perspective, a small fund sized at less than 450 million euros per annum in recent years. To raise those extra funds, the government plans to take measures such as increasing the last state tranche of personal income tax, which is levied on tax bases of over 300,000 euros at a marginal rate of 24.5% (state share). To illustrate the impact, the 2-point increase in the marginal rate in that income bracket increased tax receipts by around 300 million euros in 2022 (AEAT, 2022). In short, this proposal is far from covering the financing needed to make up for the funds lost as a result of the economic accord in Catalonia. Indeed, endowing the FCI with sufficient funds would require far more ambitious tax measures. Looking at the general personal income tax rate, for example, the government would need to intervene in the middle class income brackets – between 20,000 and 60,000 euros according to the OECD (2019) – which is where most tax receipts come from. There are other reform options, such as fresh increases in capital gains tax or even increases in other taxes like VAT. What is clear is that it will take high-impact tax reforms that are hard to apply in the short-term. By way of example, full elimination of the two reduced VAT rates would raise around 15 billion euros (Government of Spain, 2023). In the absence of sufficient funding, the common regime regional governments will be forced to borrow if they want to maintain current funding levels for their public services. If not, they will have to reduce spending on those services.

There is no set date for voting on the new financing model in Parliament, which may not happen until the end of November, in light of the 100-day deadline agreed between the accord’s signatories. However, the government only has until 30 September to put the spending ceiling to another vote in the Lower House (the government approved the same spending ceiling in a Cabinet meeting on 10 September). The government will be hard pressed the break the current deadlock within that tight timeframe, although it is looking to accelerate the process with bilateral agreements with the various regional governments. The deals on offer are likely to include additional spending mandates (such as commuter trains) and haircuts on the debt owed by the regional governments to the state via the Regional Liquidity Fund (FLA for its acronym in Spanish). This fund was set up in 2012 to help the regional governments raise financing. Indeed, as part of the national government investiture deal hammered out last November, the socialist party conceded its Catalan partners a 20% haircut on the regional government’s FLA debt, equivalent to 15 billion euros. In short, the tremendous impact of these agreements on the regions’ long-term funding tips the balance in favour of a second consecutive carryover of the 2023 budget. Such a rollover would be particularly inopportune in the year that the EU’s new fiscal rules are reinstated.

Spending ceiling and deficit target for 2025

The Cabinet-approved spending ceiling for 2025 amounts to 195.35 billion euros, excluding expenditure financed by European funds, which marks growth of 3.2% from 2024. This increase reflects an expansionary bias, although it does not include the budgets of the regional governments or the Social Security (it does, however, include transfers to the Social Security). With this ceiling, in 2025, the government would have an additional roughly 6.1 billion euros for its budget action plan. The spending ceiling was calculated estimating growth of 6.5% in tax receipts in 2025. That figure is in line with growth in total non-financial receipts of 5.1%, according to the forecasts compiled by AIReF (2024), which projects revenue equivalent to 42.5% of GDP in 2024 and 42.6% in 2025. The estimated growth in non-financial revenue, while high, marks a slowdown from the growth of 8.4% and 8.9% observed in 2022 and 2023, heavily influenced by inflation-related tailwinds (IGAE, 2024). At any rate, to deliver that level of growth in tax receipts, the government will have to take decisions about the measures in place for mitigating the effects of inflation, like the VAT cut on certain food products, and consider making the temporary levies introduced on energy companies and banks, and the solidarity tax levied on large fortunes, permanent taxes. These are very important considerations as the reduced VAT rates reduce revenue by around 1 billion euros per annum, while the three temporary taxes mentioned above bring in around 3.5 billion euros (AIReF, 2024).

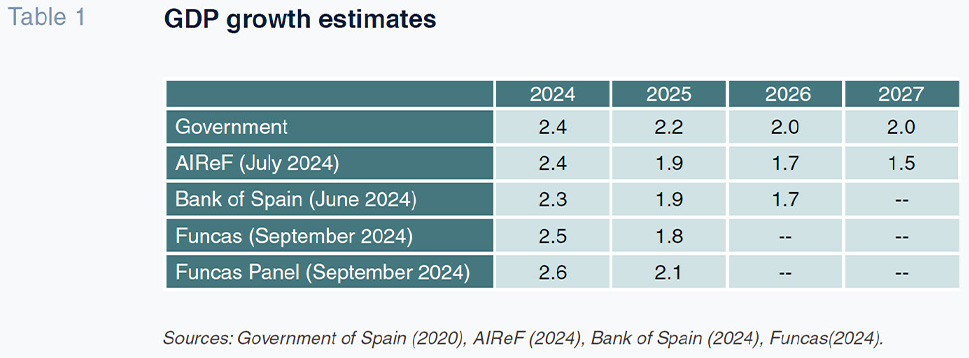

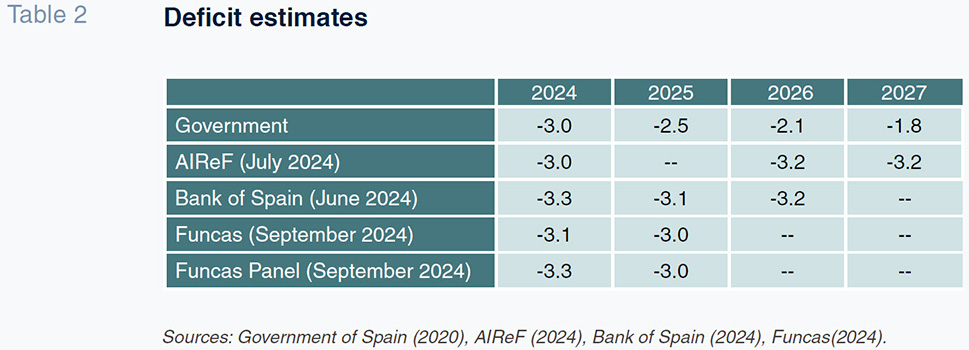

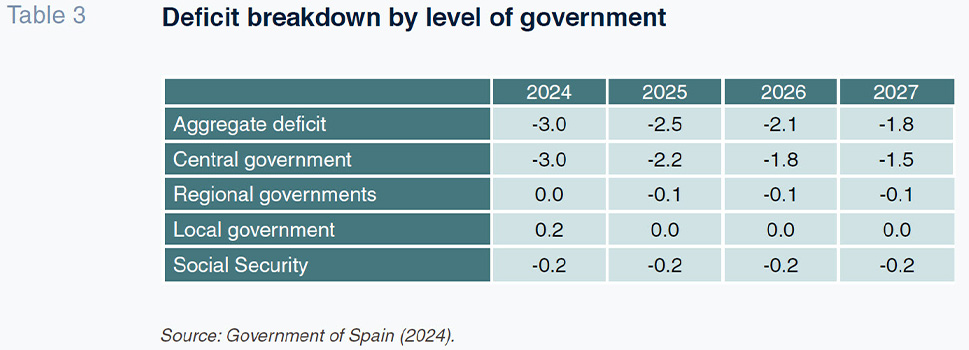

As shown in Table 1, the budget is underpinned by GDP growth of 2.4% in 2024, an estimate that is backed up by both AIReF and the Funcas Panel (AIReF, 2024; Funcas, 2024). However, growth is expected to lose steam in 2025, moving closer to 2% (AIReF, 2024; Funcas, 2024; Bank of Spain, 2024). The projected trajectory in the deficit and its breakdown by level of government are shown in Tables 2 and 3. The government expects the deficit to come down to 3% in 2024, a target that looks feasible on the basis of the current estimates of the Bank of Spain and leading Spanish think tanks. Looking further out, the government is projecting a clear downtrend in the deficit, to 2% by 2026. However, this estimate is far more optimistic than other projections. Specifically, the government’s deficit target for 2025, of 2.5%, is between 0.5pp and 0.6pp better than the rest of the projections. As the Bank of Spain and AIReF have repeatedly warned, the deficit is expected to start to increase from 2026 in the absence of a fiscal consolidation plan. In other words, the medium-term deficit projections are subject to uncertainty that will only be dissipated when: (i) we know the contents of the fiscal plan to be sent by the government to Brussels in September; and, (ii) we have information about the Draft State Budget for 2025 or, in its absence, the Budgetary Plan.

The burden of the effort to rein in the deficit will fall on the central government. In 2025, it plans to reduce its deficit by 0.8pp, from 3% in 2024 to 2.2%. In contrast, the regional governments have been given more leeway around their deficits. The regional governments will be allowed to present a deficit of 0.1% (compared to the requirement to present balanced budgets this year), while the local governments will be asked to present a balanced budget in 2025, compared to a surplus of 0.2% in 2024. In sum, the sub-national governments will have more room for fiscal manoeuvre and spending. If these deficit targets are not approved, the deficit roadmap currently in place for 2024-2026 would remain in effect, which would be more exacting for the regional and local governments, both of which would then be required to present a budget surplus of 0.1% in 2025. That would require adjustments estimated by the government at 3.3 billion euros in the case of the regional governments and 1.6 billion euros in the case of the local bodies.

The governments’ forecasts also point to higher funding via advance payments for both the regional and local governments in 2025. Those payments are forecast to increase by 9.5% in the case of the regional governments (to 147.41 billion euros) and by 13.1% for the local governments (to 26.89 billion euros). As for the Social Security, its deficit targets are unchanged at 0.2% in 2025 and subsequent years. The budget includes the transfer of 22.88 billion euros to the Social Security in 2025 to cover that deficit, growth of 7% from the transfer for 2024.

Expenditure rule in 2024 and 2025

The EU’s new fiscal rules come into effect in 2025. They will limit growth in primary spending, which excludes interest expenditure, expenditure financed by European funds, cyclical unemployment benefits and discretionary revenue measures. Year-end 2024 will be the benchmark for application of Spain’s medium-term fiscal strategy. For this transition year, the European Commission recommended limiting the growth in nationally financed primary expenditure net of discretionary revenue measures to 2.4%. However, AIReF (2024) estimates that this measure will increase by about 4.3% nationally, clearly above the Commission’s recommendation. Meeting this recommendation would have required budget belt tightening in 2024 of 10.7 billion euros, which would have put the public deficit at 2.3% rather than 3%.

Indeed, AIReF estimates the growth in primary expenditure at the regional and local government levels at 6.7% and 7.3%, respectively, in 2024, well above even the 4.8% forecast at the state level. These figures, particularly those of the regional and local governments, may mask strategic moves ahead of the tighter restrictions on spending growth looming at all levels of government from 2025. In fact, the budget outturn figures so far for 2024 indicate deterioration in the regional governments’ deficit, which could deviate from the initially targeted 0.1% and come in at 0.3%. Nevertheless, this deviation is being offset over the course of the year by a better than forecast trend in the state deficit, which is headed for 2.5%. To meet the deficit targets contemplated in Table 3, the government has approved growth in primary expenditure of 3.2% in 2025, 3.3% in 2026 and 3.4% in 2027, limits it will include in the fiscal plan to be sent to the European Commission in October. As for the debt consolidation targets, the government estimates a leverage ratio of 103.6% in 2025, falling to under 100% in 2027. We will have to wait for the Commission’s reports to see whether the primary expenditure growth targets contemplated by the government are deemed sufficient to deliver the deficit and debt consolidation targets through 2027.

References

Desiderio Romero-Jordán. Rey Juan Carlos University and Funcas