Forbearance patterns at Spanish banks: Impact of COVID-19

Government support measures such as the furlough scheme and payment moratoria have artificially held down a rise in Spanish banks’ NPL ratios. However, recent trends in forborne exposures relative to Spain’s previous performance and that of the eurozone average suggest NPLs could rise once these measures expire.

Abstract: Curiously, the COVID-19 crisis has yet to translate into an increase in Spanish banks’ non-performing loan (NPL) ratio. This is due to government measures implemented to mitigate the impact of the crisis, such as the furlough scheme and payment moratoria. However, there are signs of a deterioration in asset quality. For example, the downward trend in forborne exposures (FBE) of recent years has ground to a halt. [1] The fourth- quarter 2020 data reveal an increase in the FBE ratio quarter-over-quarter, a trend worth monitoring in the coming months. A comparison of Spanish banks’ forbearance rates to the rest of the eurozone also yields some notable insights. Prior to the crisis, Spanish banks’ exposure to forbearance had been falling more intensely than in Europe in recent years, with the gap narrowing 2.9 percentage points since 2015. That said, this ratio was still 0.5 percentage points higher in Spain by year-end 2020. With a share of 20%, this puts Spain at the top of the list of eurozone banking systems in terms of FBEs. Finally, it is worth highlighting that in Spain the percentage of forborne exposures classifi as non-performing is 11.5 percentage points above the eurozone average (50.2% vs. 38.7%) implying greater reliance on the refinancing route when borrowers run into trouble.

Introduction [2]

Despite the intensity of the economic fallout from the COVID-19 pandemic, Spanish banks’ asset quality has not deteriorated. Indeed, the NPL ratio across banks’ domestic business stands at 4.53% (as of April 2021), down from 4.8% before the onset of the pandemic one year earlier. In respect of total exposures (i.e., including their overseas businesses), the non-performing exposures ratio also fell in 2020 (from 2.32% to 2.17%), although the trendline was interrupted in the fourth quarter when the ratio rose. Regarding loans and advances, the non-performing ratio declined from 3.13% at year-end 2019 to 2.83% at year-end 2020 and trended lower for the entire period.

The fact that the NPL ratio did not rise in 2020 despite the 10.8% drop in GDP is attributable to the measures taken to mitigate the impact of the crisis on business and household income (such as the furlough scheme). The temporary freezing of certain accounting rules and capital regulations also played a role, excluding assets benefitting from payment moratoria from banks’ valuation of non-performing loans. Specifically, the accounting rules have been relaxed so that forborne credit transactions are not classified as ‘standard exposures under special monitoring’ (using the Bank of Spain’s nomenclature) so long as the banks believe there has not been a significant increase in credit risk. Previously, the general rule was that the granting of forbearance measures automatically implied a significant increase in credit risk. The change introduced in June 2020 implies a modification of an earlier Bank of Spain Circular on credit institutions’ public and confidential reporting requirements and financial statement templates. This was in response to the recommendations issued by the European Banking Authority (EBA) in the context of the COVID-19 crisis, which aimed to prevent banks from being penalised and ensure they would continue lending.

Although non-performance has not yet increased, the substantial economic impact of COVID-19 means it is expected to do so as soon as the support measures and regulatory hiatus are rolled back. As the Bank of Spain (2021) cautioned in its last Financial Stability Report, there are concerning signs, including the 35% increase in business loans classified as ‘under special monitoring’ (stage 2) in 2020 and the slowdown in the downtrend in forborne exposures (based on data pertaining to banks’ Spanish businesses). It will be important to watch how these trends evolve over the coming months as the volume of forbearance could be a leading indicator for non-performance.

The purpose of this paper is to analyse the most recently available information –which dates to year-end 2020– on Spanish banks’ forborne exposures (FBEs), comparing their situation with that of the other European banking systems. The analysis includes the domestic and overseas businesses and uses data published by the Bank of Spain (Supervisory Statistics on Credit Institutions) and the ECB (in some instances for significant entities and in others using consolidated banking data).

Trend in forbearance as an indicator of asset quality

For Spanish banks’ business as a whole (domestic and international), the most recent fourth-quarter 2020 data indicate a pause in the downward trend in the FBE ratio (forborne exposures as a percentage of total exposures) observed in recent years. Specifically, the FBE ratio increased from 1.86% in the third quarter to 1.87% in the fourth, implying a slight increase of 0.53% in the volume of forborne exposures (€420 million). In the second quarter of 2020, FBEs had increased by 2.2%, in contrast with uninterrupted contractions in recent years. However, that quarter the FBE ratio did not increase thanks to the 5.7% growth in total exposures, shaped in part by the increase in credit driven by the provision of state guarantees. At year-end 2020, forborne exposures totalled 79.03 billion euros, down 36% from the first quarter of 2018 (123.23 billion euros).

The analysis of the breakdown of forborne exposures suggests that COVID-19 has not yet had an adverse impact on non-performance. Indeed, the percentage of FBEs classified as non-performing decreased from 55.2% in the first quarter of 2020 to 54% by the fourth. Between the fi and second quarters of 2020, the volume of non-performing and performing FBEs both increased (the latter with greater intensity), but between the third and fourth quarters, the volume of non-performing FBEs decreased (by 1.3%), while the volume of performing FBEs increased (by 2.8%), so that the total balance increased by 0.5%. Between 2018 and 2020, non-performing forborne exposures declined by 34%, while performing FBEs fell by 38%.

The data published by the ECB enables a comparative analysis at the European level up to the end of 2020 with the caveat that the figures relate to significant entities (those supervised directly by the ECB) and not the entire universe of credit institutions. However, this subset of FBEs represents 93.4% of total system exposures.

The significant entities’ FBE ratio similarly increased in the fourth quarter of 2020, from 1.95% to 1.97%, to stand 0.49 percentage points above the EU average. The good news is that the long-standing gap with respect to this average has narrowed significantly in recent years. Between the second quarter of 2015 (earliest reading available) and the end of 2020, that gap has narrowed from 3.39 percentage points to 0.49 percentage points.

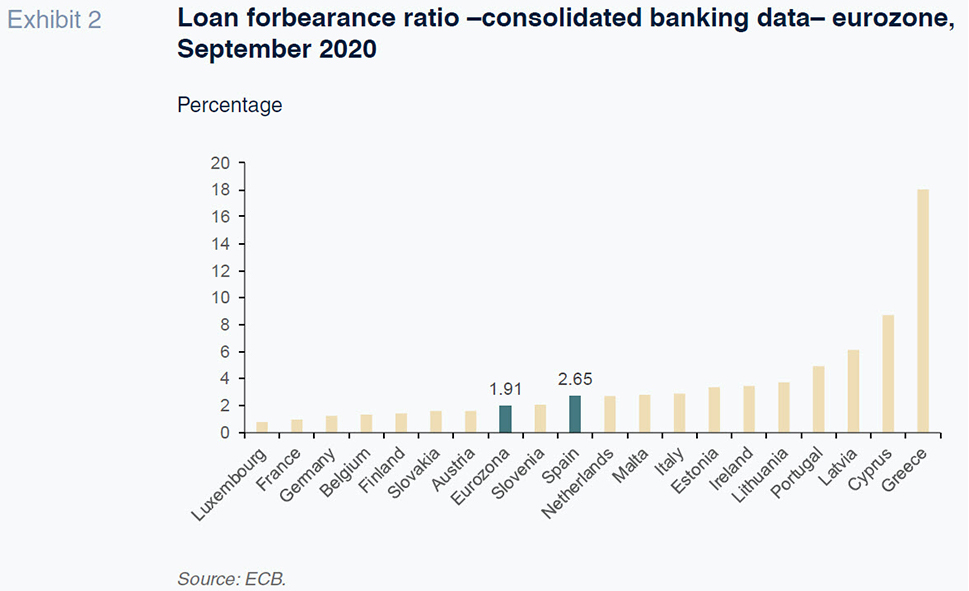

To draw a comparison with the rest of the eurozone, we focus on the consolidated banking data, which run until the third quarter of 2020. Using those figures, Spain’s most recent NPL ratio of 2.28% is the seventh highest in the list of 19 eurozone countries, behind Estonia (2.99%), Ireland (2.99%), Portugal (3.79%), Lithuania (4.73%), Cyprus (7.10%) and Greece (15.21%). However, relative to the main eurozone economies, Spain’s FBE ratio is higher: Italy (2.27%), Germany (1.05%) and France (0.86%).

In the case of loans, the Spanish banks’ FBE ratio is 0.74 percentage points above the eurozone average (2.65% vs. 1.91%), with that gap having narrowed considerably in recent years, dropping from 5.8 percentage in 2014 to 0.74 percentage points as of the third quarter of 2020. Note that in 2014, Spain’s loan forbearance ratio was extremely high (9.76%) at a time when non-performance was much higher than it is today (8.1% vs. 2.92% in September 2020).

Weight of forbearance measures in total loans: Performing vs. non- performing

It is worth analysing the weight of forbearance exposures relative to total loans, distinguishing between their classification for risk purposes, i.e., between performing (standard exposures and exposures under special monitoring, using the Bank of Spain’s nomenclature) and non-performing (doubtful for arrears or reasons other than arrears). Obviously, the weight of forbearance will be much higher in the latter category than in the former.

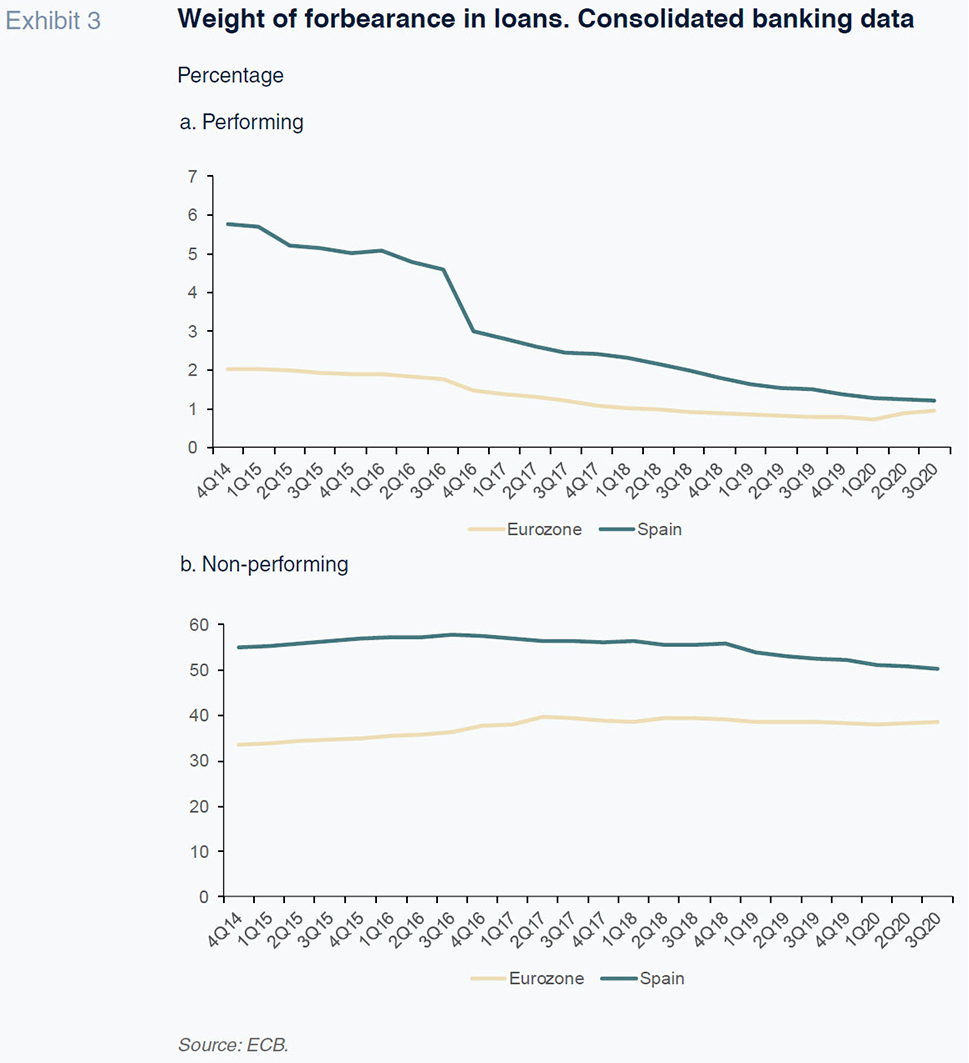

Based on data as of the third quarter of 2020, 1.21% of total performing loans in Spain were classified as forborne, which is above the eurozone average of 0.94%. Prior to the pandemic, this ratio had been falling. Although the pace of that downward trend slowed in 2020, the ratio continued to decline. As a result, the gap relative to the eurozone has narrowed by 3.5 percentage point to mark a low in September 2020.

In the case of the non-performing loans, as of September 2020, forborne assets accounted for 50.3% of the total in Spain, which is some 11.5 percentage points above the eurozone average. The gap with respect to the eurozone has tightened by 10 percentage points since 2014, shaped by a 4.8 percentage point drop in the percentage of non-performing forborne loans in Spain and a 5.2 percentage point increase in the rest of the eurozone. COVID-19 does not appear to have driven an increase in that percentage in Spain.

Breakdown of total forborne exposures by country

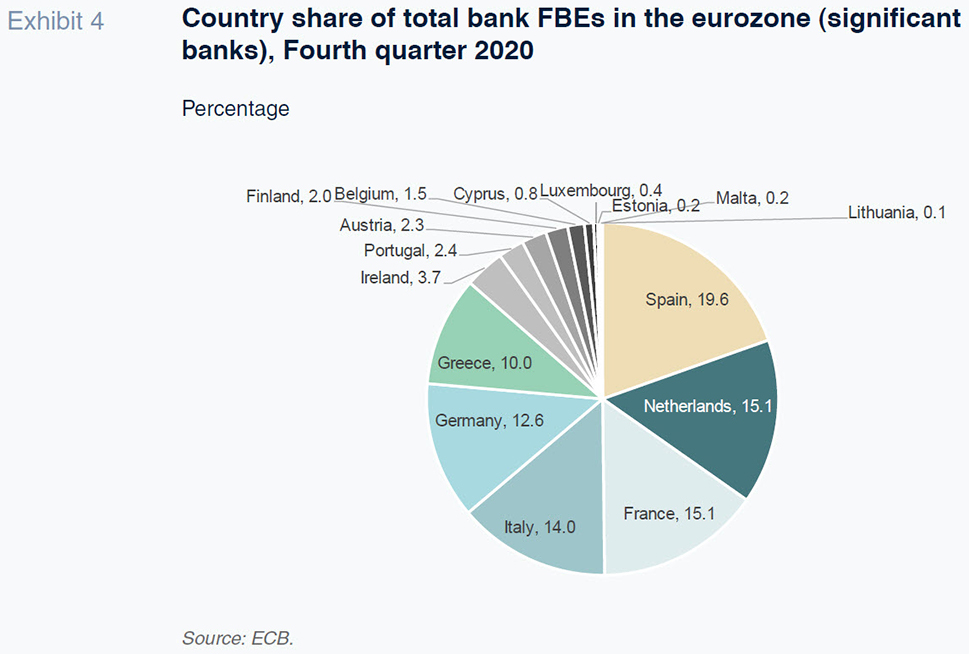

Looking at significant banks (those supervised directly by the ECB), Spain’s FBE ratio topped the list of eurozone countries by volume of FBEs at year-end 2020, accounting for nearly 20% of the European total (Exhibit 4). This is despite the sharp fall in Spain’s FBE ratio in recent year. Spain is followed by Netherlands (15.1%), France (15.1%), Italy (14%) and Germany (12.6%). Greece, despite being the European country with the highest FBE ratio (12.9%), accounts for just 10% of the European total in absolute terms. Total forborne exposures in the eurozone amount to €378 billion, which is 1.5% of total exposures.

The ranking is very similar in the case of non- performing FBEs, with Spain accounting for the highest share in the eurozone (21.1%), followed by France (16.7%), Italy (16.6%) and Greece (13.3%). In the eurozone as a whole, 50.6%, or €191.4 billion, of forborne exposures are non-performing.

Conclusions

As mentioned by the Bank of Spain in its last Financial Stability Report, there are already indications of impairment of bank asset quality. Although it is not yet apparent in an increase in the NPL ratio, the volume of loans ‘under special monitoring’ (stage 2) and the reduced pace of reduction in forborne exposures in the Spanish banking business are tell-tale signs. Adding in the business carried on by banks’ international subsidiaries, forborne exposures actually increased in Spain in the fourth quarter of 2020, albeit only slightly, halting the downward trend of previous years. Regarding significant entities, Spanish banks’ FBE ratio is 0.5 percentage points above the European average. Spain accounts for 20% of all eurozone bank FBEs, ranking first in the region in terms of absolute exposures. It would be a favourable development to see that percentage come down.

It is also worth monitoring the trend in FBEs in the coming months as it could herald an uptick in non-performance. Indeed, the weight of the consolidated banking groups’ FBEs in total non-performing assets is 11.5 percentage points above the eurozone average (50.2% vs. 38.7%), suggesting that the Spanish banks are more inclined to refinance when borrowers run into diffi According to a recent IMF study (2020), which draws on post-COVID-19 evidence, those banks that face higher non- performance levels (in relation to their own funds and provisions) are more inclined to grant forbearance measures to riskier borrowers. This means it is important to track the trend in FBEs given that the percentage of financially vulnerable businesses has increased.

Notes

Forbearance is defined as a concession granted to a counterparty for reasons of financial difficulty (present or foreseeable) that would not be otherwise considered by the lender. Therefore, an increase in forborne exposures (or a slowdown in the rate of reduction) could herald an uptick in non-performance.

This article falls under the scope of research project ECO2017-84828-R of the Spanish Ministry of the Economy, Industry and Competitiveness and AICO2020/217 of the Valencian Government.

References

BANK OF SPAIN. (2021). Financial Stability Review, April.

BERGANT, K. AND KOCKERO, T. H. (2021). Forbearance Patterns in the Post-Crisis Period. IMF Working Paper, WP/20/140.

Joaquín Maudos. Professor of Economic Analysis at the University of Valencia, Deputy Director of Research at Ivie and collaborator with CUNEF