Bank valuations: Good news and bad news

Positive earnings performance and lower cost of equity have led the European banks to outperform the general stock indices for the last two years; nevertheless, they have yet to close the gap between their market value and book value, despite the fact that their return on equity (ROE) is back above 10%, the threshold traditionally deemed necessary to close the valuation gap. While the inability to close this gap appears to lie with the fact that the cost of equity (CoE) required of the banks has increased above the conventionally assumed threshold of 10%, the discount at which the European and Spanish banks are currently trading seems excessive.

Abstract: After two years of tailwinds, the Spanish and European banks’ earnings have capitalised on the favourable interest rate climate, which has catapulted their margins while asset quality has kept the cost of risk at very low levels. By comparison with their outstanding earnings performance, the banks’ stock market performance has been more nuanced. On the one hand, the banks have outperformed the general stock indices for the last two years. Nevertheless, they have yet to close the gap between their market value and book value (the ratio known as price-to-book value, or P/B, remains at around 0.7x, implying a discount of 30%), despite the fact that their return on equity (ROE) is back above 10%, the threshold traditionally deemed necessary to close the valuation gap. Given the aforementioned correlation between the ROE and CoE implied by the P/B ratio, it can be deduced that the inability to close the gap can be attributed to one or both of the following factors: a) doubts about the banks’ ability to sustain the current ROE levels; and/or, b) the cost of equity (CoE) required of the banks has increased above the conventionally assumed threshold of 10%. On the basis of the takeaway from the responses provided to the Risk Assessment Questionnaire carried out by the European Bank Authority (EBA) across a wide sample of European banks, the explanation appears to most likely lie primarily with the second factor. In any event, without questioning the banks’ perception that their cost of equity has increased in the past year (attributable, to a degree, to an element of ‘stagnation’ in long-term interest rates at high levels), the discount at which the European and Spanish banks are currently trading seems excessive considering that a good percentage of the banks surveyed see their ROEs as sustainable over the coming year.

European banks: Profitability and resilience a decade on from the banking union

Thanks to strong tailwinds in the form of high interest rates without adverse effects on the economy or employment, in 2023, the European banks, and the Spanish banks in particular, posted their best performance since the introduction of the Single Supervisory Mechanism, the first pillar of the banking union, nearly a decade ago.

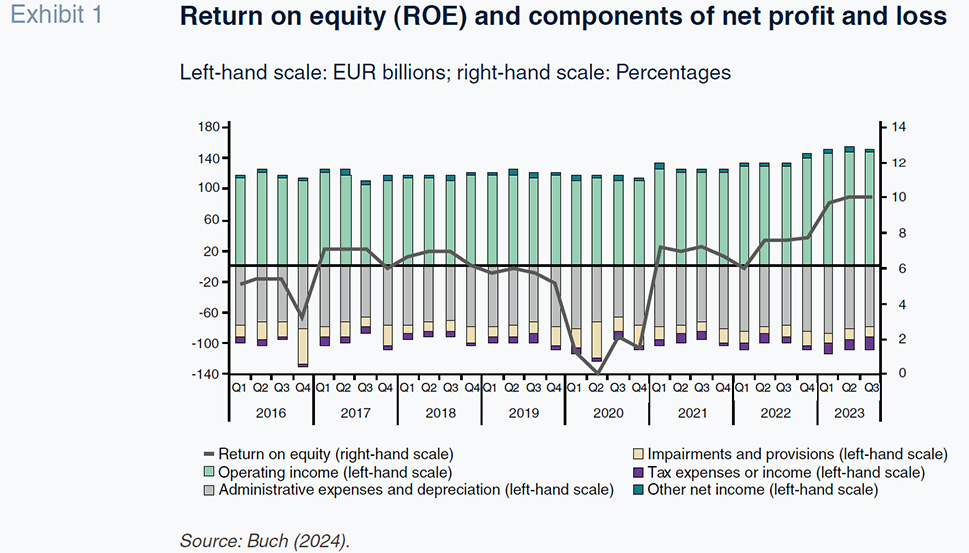

Although the fourth-quarter figures for the overall European banking system are not yet available, an extrapolation of the third-quarter figures and the results already released by the listed banks (Exhibit 1) suggest that the sector is on track to report record aggregate profits of close to 180 billion euros. That would imply growth of nearly 50% from 2022 and a return on equity (ROE) of roughly 10%, the first time such a result was attained since the introduction of the banking union (indeed, since before the financial crisis of 2008) and the threshold traditionally considered the minimum demanded by market participants for holding banks’ equity.

Nearly all of the improvement in the European banks’ ROE (4 percentage points) was generated by growth in their net interest margin, thanks to more intense pass-through (or “beta”) of the increase in Euribor to loans than to retail deposits, as analysed in an earlier article for this publication (Alberni et al., 2023).

Compared to that positive contribution via margins, the increase in operating expenses induced by inflation eroded the ROE by a little under one percentage point, while non-performing asset provisions did not impact the banks’ ROE, remaining flat year-on-year. Without question, the absence of adverse consequences for credit quality (NPL ratios in check) in the current context of high inflation and high interest rates is the other piece of good news for the resilience of the European and Spanish banks.

This scenario of contained non-performance injects value into the sizeable profits obtained and their use by the banks: their profits have been used almost equally to remunerate shareholders (via dividends or share buybacks) and to reinforce their solvency via retained earnings.

More specifically, the approximately 90 billion euro increase in reserves via retained earning implies an increase of nearly 1% in the banks’ CET1 ratio, which stood at close to 15.8% for the aggregate European banking system according to the most recent information published by the EBA in its last Risk Dashboard for 3Q, the highest since the banking union entered into force. Note, however, that the improvement in solvency has come not only from the numerator (growth in own funds thanks to the retained earnings effect) but also the denominator, as the volume of risk-weighted assets has stabilised or even decreased in a context of zero growth, or even contraction, in credit, particularly in the segments with higher risk weightings.

Profitability and dividends have driven stock market gains

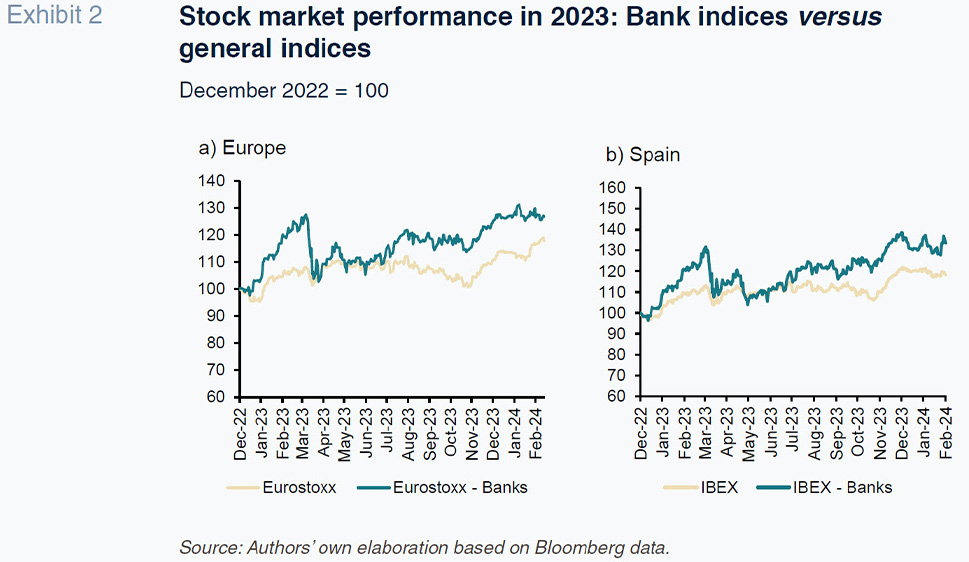

This ample solvency buffer, in a context in which credit is not expected to grow by much and NPL coverage levels remain high, justifies the fact that the banks have maintained, or even slightly increased, the percentage of profits they have earmarked to shareholder remuneration in the form of dividends or share buybacks. This increase in the payout ratio in a year of high profits has translated into generous shareholder remuneration, which is up by over 50% from the year before. For the European banking system as a whole, our estimates point to the distribution of around 85 billion euros, which is a little more than 5% of the system’s total book value. This simultaneous improvement in shareholder remuneration and in own funds has been the main factor driving the clearcut recovery in the banks’ market values in 2023, a year in which the sector clearly outperformed other sectors.

This is evident in a comparison between the bank stock indices and the general indices, as illustrated in Exhibit 2 for both Spain and Europe. In both geographies, the banking indices have clearly outperformed, gaining close to 30% in Spain and Europe, which is nearly twice the general market gains.

Valuation gap: Explanatory variables

This positive stock market performance over the past year should not, however, mask the reality that the banks’ market value continues to lag book value by a considerable amount.

To document this claim, we analysed the relationship between the market capitalisation and book value at year-end 2023 of a broad sample of Spanish and European banks that have already presented their financial statements for the full year. The sample is made up of 22 European banks, including five Spanish banks, all of which are traded in the Euro STOXX Banks Index (and in the case of the Spanish banks, the Ibex Banks Index).

The sample is considered sufficiently representative for the purpose of analysing the sector’s valuation as, between them, the 22 European banks analysed account for 50% of total assets in the banking union, and 70% of total bank assets in Spain in the case of the five Spanish banks analysed.

For the sample of banks analysed, the weighted average P/B ratio is still only 0.65x, despite the stock market gains of 2023, implying a valuation discount of 35% to book value.

That valuation gap is being watched with interest, and some concern, by the regulators and supervisors, as it means that the market is applying a significant discount to the value of the banks’ own funds for accounting purposes, which are the basis of their capital adequacy ratios. In other words, the solvency perceived or priced in by the market is substantially lower than the solvency for regulatory purposes, which means that in the event of having to raise equity urgently, the cost would be very high in terms of dilution for existing shareholders. That is why the authorities are monitoring the key valuation metrics closely and trying to identify the factors that are hindering closure of the gap relative to book value.

The conventionally accepted business valuation models rely on the ratio between the return a business can obtain on its equity on a recurring basis (ROE) and the cost of equity required by the market to provide those funds (CoE), so that a business that generates an ROE above its CoE would fetch a P/B ratio of over 1, while a P/B ratio of under 1 indicates an ROE below its cost of capital.

For many years it was assumed that, in the case of the European banks, the cost of capital required by the market was around 10% such that, once the banking business was able to generate an ROE above that threshold on a sustained basis, the valuation gap relative to book value would be eliminated, that gap having gone as a high as 50% in the years in which the banks were generating ROEs of 5%, or even lower.

That said, delivery of an ROE of just over 10% in 2023 has not been sufficient to close the valuation gap, which remains at over 30%. Given the aforementioned correlation between the ROE and CoE implied by the P/B ratio, it can be deduced that the inability to close the gap can be attributed to one or both of the following factors: a) doubts about the banks’ ability to sustain the current ROE levels; and/or b) the cost of equity (CoE) required of the banks has increased above the conventionally assumed threshold of 10%.

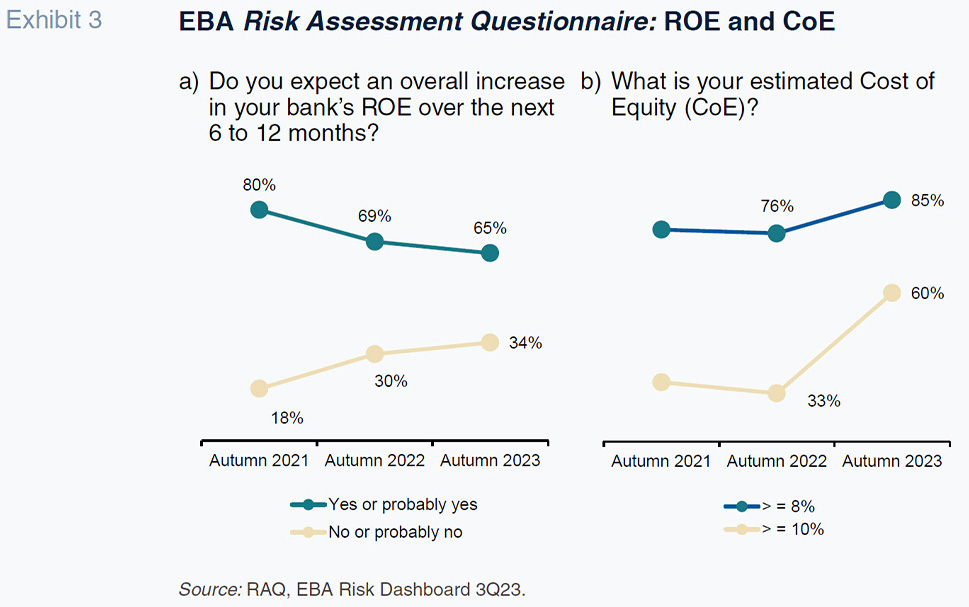

The explanation probably lies more with the second factor, or at least that is the takeaway from the responses provided to the Risk Assessment Questionnaire carried out by the European Bank Authority (EBA) across a wide sample of European banks, whose latest survey, from autumn 2023, throws up interesting food for thought with respect to ROE and CoE. Specifically, the Questionnaire asks the banks about their outlook for growth in their ROE over the next 6 to 12 months and also asks them for their estimated CoE. Recall that the cost of equity is a variable that is not explicitly observable and can only be derived using valuation models or on the basis of surveys of market participants or bank managers, as in the case of the EBA Questionnaire. Exhibit 3, parts a) and b), synthesises the responses provided in the last Questionnaire and compares them with those provided during the previous two surveys, for 2021 and 2022.

In the case of ROE, albeit less pronounced than in the previous two surveys, the majority of respondents continues to expect an increase, supporting the hypothesis that ROEs are sustainable at current levels.

However, the change in the respondent banks’ perceived cost of equity (CoE) is more explicit. Compared to just one-third of the banks who estimated their CoE at 10% or higher a year ago, in the last survey a clear majority (60%) of the banks identified 10% as the lower limit of their estimated CoE.

Without questioning the banks’ perception that their cost of equity has increased in the past year (attributable, to a degree, to an element of “stagnation” in long-term interest rates at high levels), the discount at which the European and Spanish banks are currently trading seems excessive considering that a good percentage of the banks surveyed see their ROEs as sustainable over the coming year.

References

ALBERNI, M., BERGES, A. and RODRÍGUEZ, M. (2023). Cost of deposits and Euribor: Why this time is different.

Spanish Economic and Financial Outlook, Vol. 12 | No. 3, May 2023.

https://www.funcas.es/wp-content/uploads/2023/06/05-Alberni-12-3.pdfBUCH, C. (2024). European banking supervision a decade on: safeguarding banking resilience amid global challenges. Speech at House of the Euro, Brussels, February 2024.

ENRIA, A. (2023). Press conference on the 2023 SREP results and the supervisory priorities for 2024-26. Frankfurt, December 2023.

EUROPEAN BANKING AUTHORITY, EBA. (2023a).

Risk Assessment Questionaire (RAQ), Summary of Results. Autumn 2023.

EUROPEAN BANKING AUTHORITY, EBA. (2023b).

Risk Dashboard 3Q23. Autumn 2023.

Marta Alberni, Ángel Berges and Alejandro Montesinos. Afi