The Spanish economy in 2015 and outlook for 2016

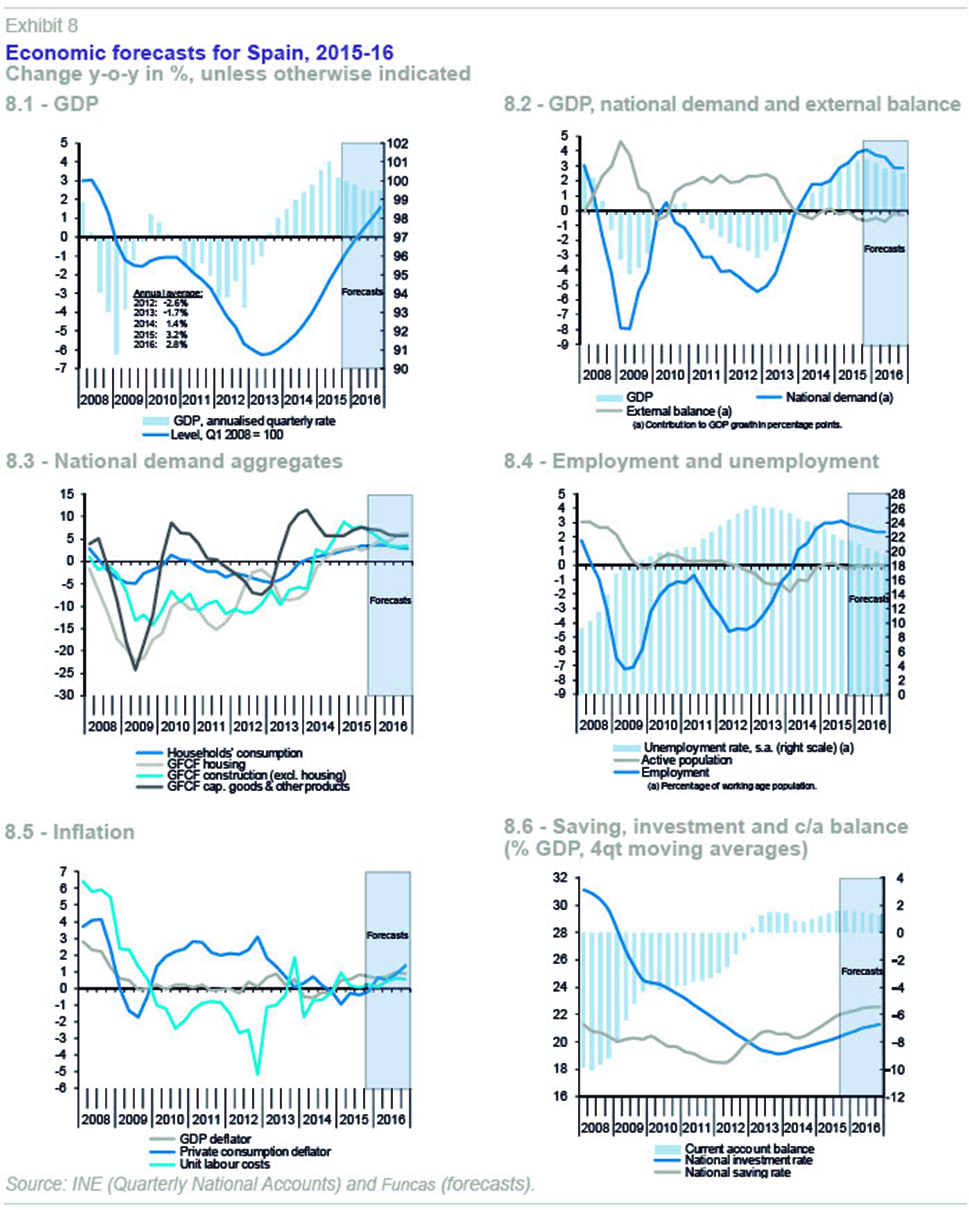

The effects of permanent factors, combined with a number of short-term positive shocks, gave a substantial boost to domestic demand, pushing GDP growth above expectations in 2015. Future estimates of potential growth are moderate; however, limiting factors will probably not prevent the Spanish economy from growing between 2.5% and 3% over the medium-term.

Abstract: The main features of the global economy in 2015 were the economic slowdown in China and other emerging economies, the sharp fall in the price of oil and other commodities, the appreciation of the dollar, the start of the cycle of interest rate hikes by the Federal Reserve and the extension of the European Central Bank’s quantitative easing policy. Spain grew dynamically, thanks to a series of transitory exogenous factors coinciding with endogenous factors, which arose mostly from the functioning of the cyclical adjustment mechanisms. As the effect of these exogenous shocks wears off, growth will slow somewhat in 2016. Going forward, the slower potential GDP growth rate, due to the damage caused by the length of the crisis, will substantially limit GDP growth unless economic policy reforms are enacted to raise its potential.

The global economy in 2015 and risks for 2016

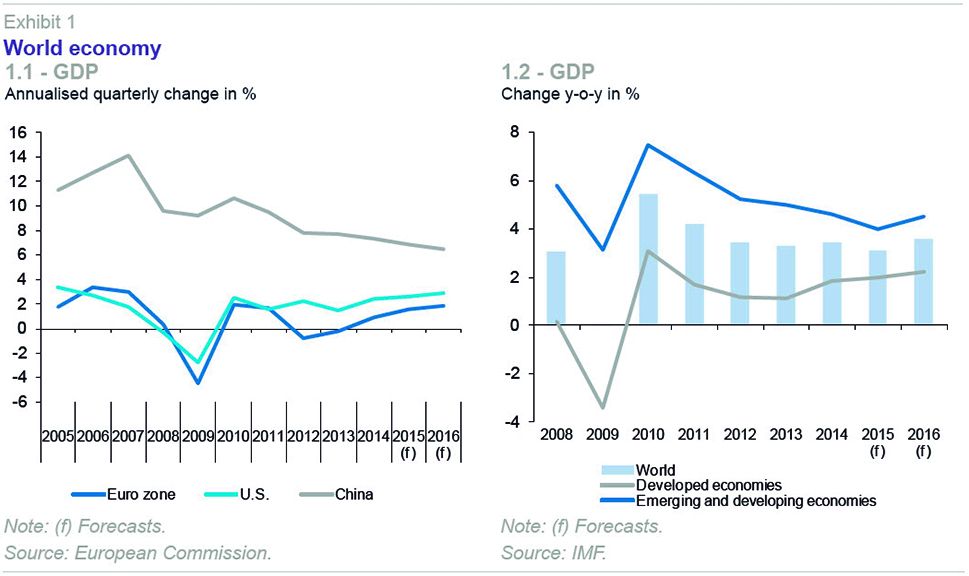

The key feature of the global economy in 2015 was the intensification of the Chinese economic slowdown. This led to a collapse in commodity prices, dragging down many emerging markets commodities exporters. As has been the case for several years, the main feature in the case of the developed economies was the contrast between the dynamism of the United States and the weakness of the euro area (Exhibits 1.1 and 1.2).

The slowing of China’s growth rate, which dropped to below 7% in 2015, according to official figures, well below the double-digit rates that have been habitual over the last thirty years, is assumed to be permanent, as the country is undergoing a process of structural transformation. This means a hugely important change in scenario, with far-reaching consequences for the world economy as a whole. One of these consequences is the drop in commodity prices –although in the case of oil, other factors on the supply side have also played a role– which is also considered to be lasting, with a negative impact on oil-exporting emerging economies. However, this impact will be positive for most developed economies, and at least partially compensate for the negative impact of the drop in international trade caused by the weakening of China and other emerging economies.

Another factor with a negative impact on emerging economies in 2015 was the expected tightening of U.S. monetary policy. The Federal Reserve ended its bond-buying programme in late 2014 and it was widely expected to begin raising rates in 2015 which pushed up both the dollar and yields on short-term dollar-denominated debt throughout the year. This triggered capital outflows from the emerging economies, leading to the collapse of many of their currencies. This in turn has heightened the risk of currency crises and a risk of default on dollar-denominated debt taken on by private companies during the boom years. The latter, in turn, increases the risk of a banking crisis.

The Federal Reserve’s interest-rate increase was initially expected in June, and then in September, and finally took place in December. This contrasts with the European Central Bank’s announcement of a rate cut in the interest charged on credit institutions’ deposits to -0.3% and an extension of its bond-purchase programme until March 2017.

The divergence in monetary policy stance is explained by the differing economic conditions on either side of the Atlantic. The U.S. economy grew by around 2.5% in 2015, the fifth consecutive year of growth since the 2008-2009 crisis (growth has averaged over 2% since that period), the unemployment rate has dropped to 5% and, at the end of the year, the core inflation rate was close to 2% (the headline rate was lower due to the fall in prices of energy products). Growth last year in the euro area barely reached 1.5%, 2015 being the second consecutive year of growth. The unemployment rate, which at the end of the year stood at around 10.5%, has been coming down only slowly. And core inflation has hovered around 0.9% for most of the year, while headline inflation has been close to zero, also as a result of energy prices.

How financial markets will adapt to this scenario of opposing monetary policies in the two major economic areas is another reason for uncertainty in 2016. This potential focus of instability and financial markets stress comes in addition to the risks already mentioned arising from the situation in China and the emerging economies.

The Spanish economy in 2015

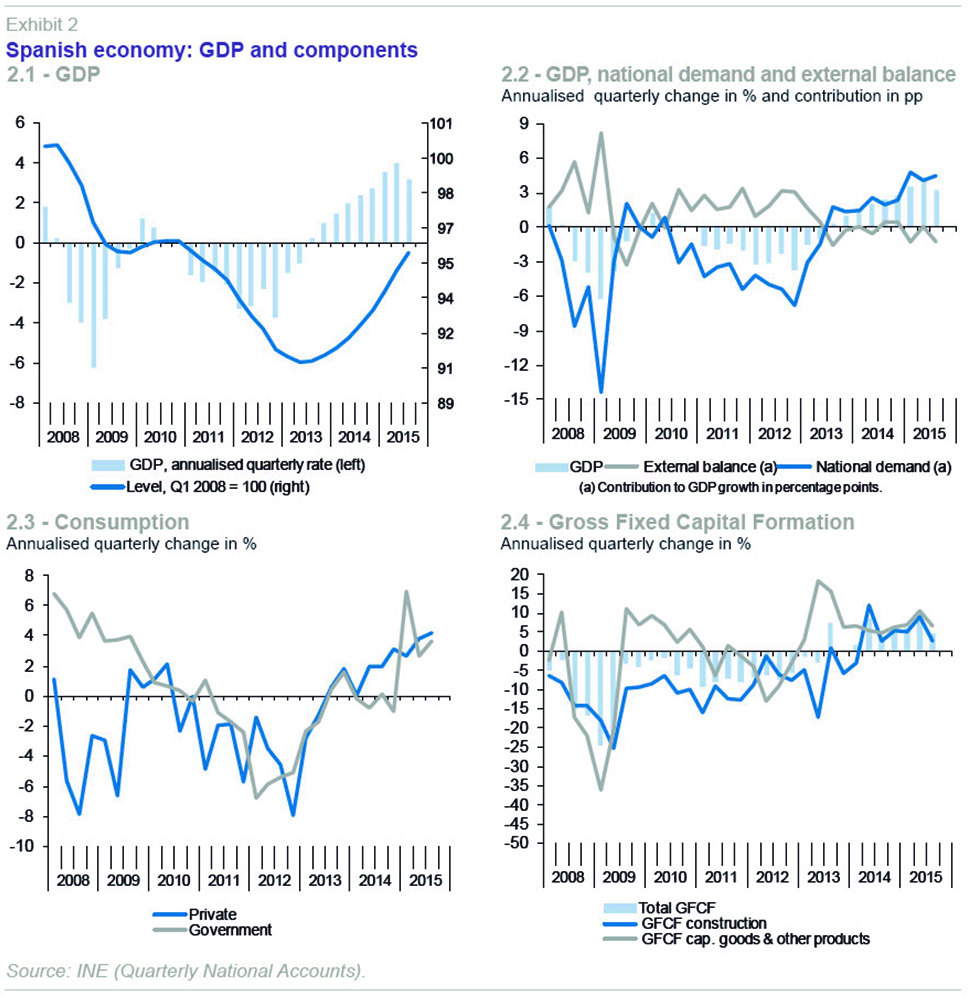

Spain´s growth was highly dynamic in 2015. Although complete data for the final quarter of the year are not yet available, it may be estimated at 3.2% – the highest among the main euro-area economies (Exhibit 2.1). This performance far exceeded expectations. Thus, in September 2014, Funcas predicted growth of 2.2%, although the consensus forecast was even lower: the international consensus forecast was 1.8% [1] and the consensus forecast among Spanish institutions was 2%. [2] The government’s forecast in the General State Budget submitted that month was 1.8%.

The reason why the final result exceeded the forecasts so widely was due to a confluence of various unexpected exogenous shocks, which had a transient impact on growth. These included: the gain in real income deriving from the sharp drop in the oil price; a considerably less restrictive fiscal policy than expected – the unexpected adoption of a tax cut in July, in addition to that which came into effect in January, in conjunction with higher public spending than expected; and, the quantitative easing introduced by the ECB having a more powerful effect than anticipated on interest rates and on the euro exchange rate.

As a consequence of the impact of these factors, growth in domestic demand beat expectations and also resulted in higher-than-expected imports. Thus, domestic demand contributed an estimated 3.6 percentage points (pp) to GDP growth, while the external sector’s contribution was negative (-0.4 pp.), in contrast to expectations of a positive contribution (Exhibit 2.2).

Private consumption grew strongly, by around 3.1%. Part of this growth was the result of the impact of the exogenous factors mentioned, together with a number of endogenous factors. These include increased wages, due to higher employment rather than rising wages per capita; improved confidence; improvements in many households´ financial situation, enabling them to make spending decisions postponed during the crisis years; and, the normalisation of new credit availability, which has started growing again, although from very low levels in comparison with its peak in 2007. The upturn in public consumption was one of the most striking results. Public consumption grew by around 2.3% in real terms –2.8% in nominal terms– while the government forecasts in the General State Budget projected a drop in real terms of 1%. This deviation was a consequence of the electoral cycle (Exhibit 2.3).

Investments in capital goods grew by around 6.9%, in line with forecasts. This variable has grown strongly for three consecutive years, although its volume still falls short of the peak reached in 2007. Investment in housing construction began to recover in the second quarter of 2014, although 2015 was the first year with a positive annual growth rate (3%). This component of demand was that which suffered the biggest adjustment during the crisis, with its volume in 2015 being just half of its 2007 peak. Its progress reflects the recovery in the property market that began in 2014. The rate of housing sales accelerated in 2015, and prices also began to recover, with a year-on-year rise of 4.5% registered in the third quarter of 2015. Nevertheless, it was non-residential construction that grew fastest in 2015, at 7.6%. This may be largely due to an increase of public works driven by the electoral cycle (Exhibit 2.4).

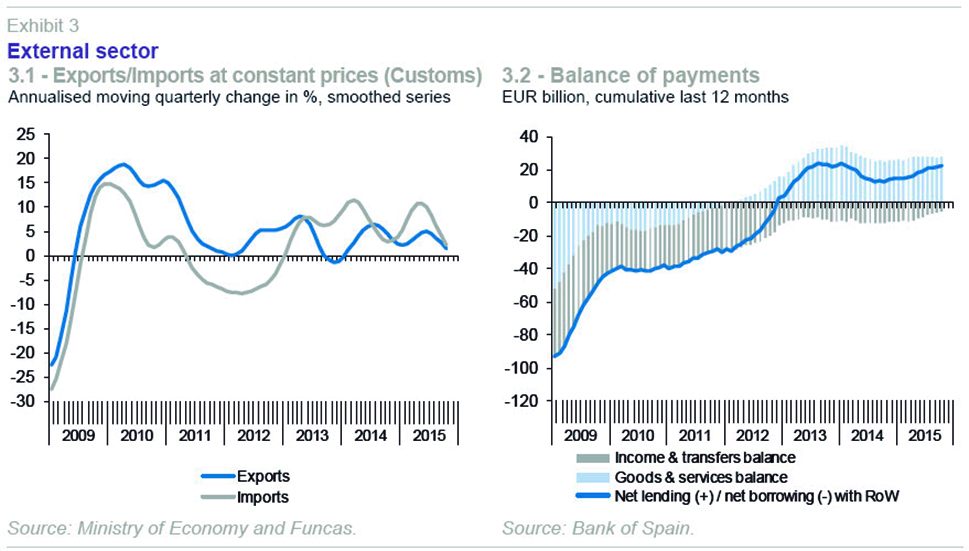

Exports of goods and services grew by almost 6% in 2015, in real terms, with goods exports alone growing by 5.1%. This growth rate exceeds that of global merchandise exports, implying Spanish exports have increased their market share. The biggest increase was in exports to other EU countries. Imports of goods and services grew by around 7.7%. Nevertheless, in current prices, goods exports grew faster than imports, basically due to the lower price of energy imports. This fact has made it possible for the current account surplus to improve in 2015, despite the external sector’s negative contribution to growth in real terms.

All productive sectors presented an increase in their gross value added. Construction grew most, posting its first positive growth rate since 2008, followed by manufacturing and market services. The strength of the manufacturing industry stands out in particular, as evidenced by the progress of various economic indicators, such as the industrial production index, PMI, industrial climate index, and employment growth. These indicators improved over 2015 as a whole at rates significantly higher than the averages seen in the pre-crisis expansionary period.

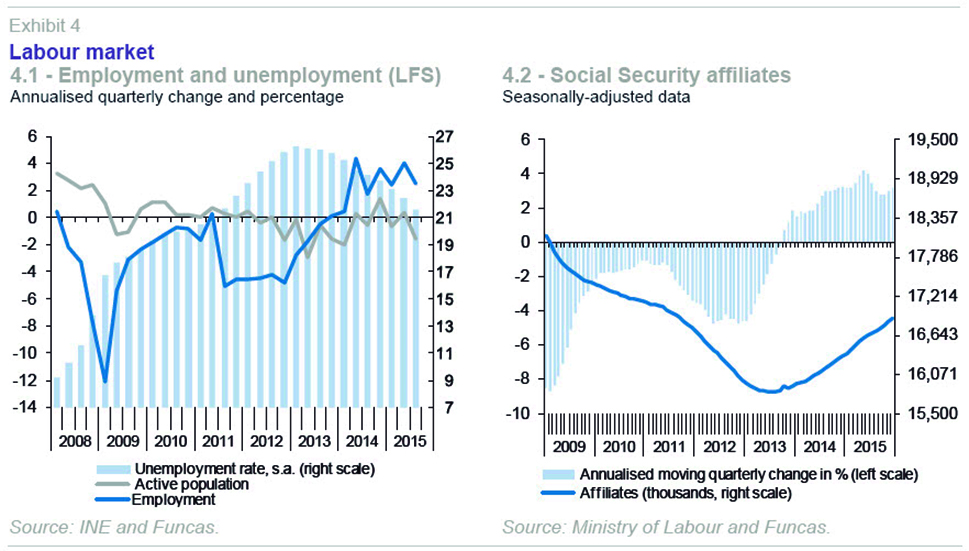

Employment, measured in terms of full-time equivalent jobs, is estimated to have grown by 3%, representing an increase of 490,000 jobs on an annual average basis. The number of workers affiliated to the social security system rose by 3.2%. Employment growth in the manufacturing industry was 2.2%, the highest percentage in the historical series, which currently dates back to 2001. The number of social security affiliates in the construction industry also recovered strongly in 2015. Growth was particularly strong in this sector in the first two quarters of the year, slowing in the third, probably following the trend in public works driven by the electoral cycle (Exhibit 4.2).

According to the Labour Force Survey, and using estimates for the third quarter, the decline in the active population registered in 2013 and 2014 slowed in 2015. This was a consequence of slower contraction of the working-age population – due to the drop in the number of immigrants returning to their countries of origin – in combination with a slight rise in the activity rate. The number of people out of work fell by approximately 515,000, bringing the unemployment rate down to an annual average of 22.2% from 24.4% the previous year (Exhibit 4.1). One positive development was that employment among young people began to rise in 2015, and at a rate significantly higher than that among older workers.

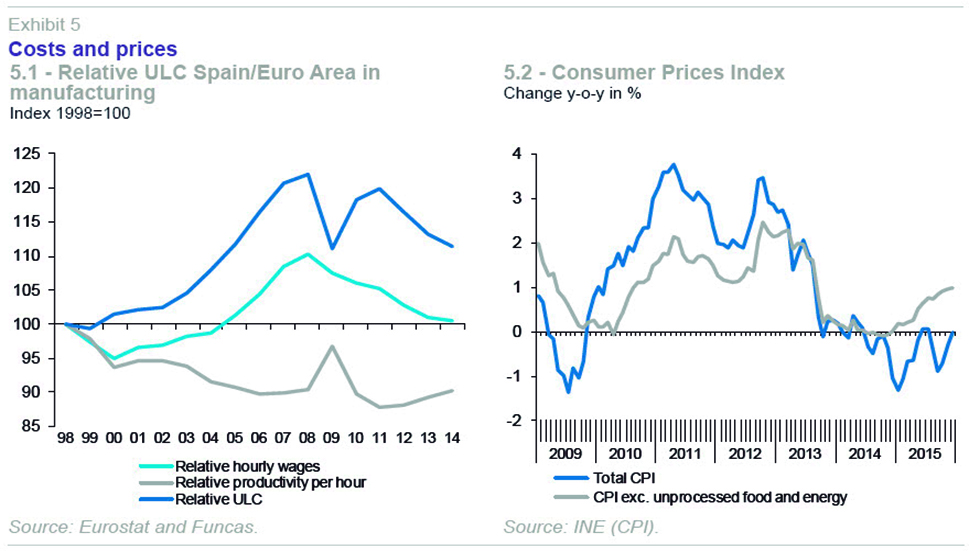

Compensation per employee, according to national accounts figures, grew by 0.5% in 2015. Combined with the increase in productivity of 0.2%, this caused unit labour costs to rise by 0.3%. This is the first time this variable has risen since 2009, although the increase was lower than that registered by euro-area average ULC, which means that the Spanish economy has continued gaining in cost competitiveness (Exhibit 5.1). Negative consumer price inflation meant this was possible without a reduction in the purchasing power of wages.

Annual inflation was -0.5% in 2015, negative for the second consecutive year, due to the drop in energy prices, as a result, in turn, of lower oil prices. All the other components of the CPI presented positive, albeit modest, growth. In particular, core inflation was 0.6%, with the trend being clearly upwards since the end of previous year (Exhibit 5.2). This is explained by the greater dynamism of consumption and the depreciation of the euro. Spain’s inflation rate was again lower than the euro-area average, in the case of both headline and core rates.

The surplus on the current account of the balance of payments to October 2015 came to slightly more than 10 billion euros, compared with

3.3 billion euros in the year-earlier period. This was a result of the bigger trade surplus in goods and services and the smaller deficit in the income balance. In turn, the trade surplus increased due to the reduction in the goods deficit – thanks to the lower oil price, as the balance excluding energy products worsened – and the bigger surplus on the services balance. For the year as a whole, the current account balance can be estimated at around 1.6% of GDP, compared with 1% the previous year, and financing capacity rose to 2.2% of GDP from 1.6% (Exhibit 3.1 and 3.2).

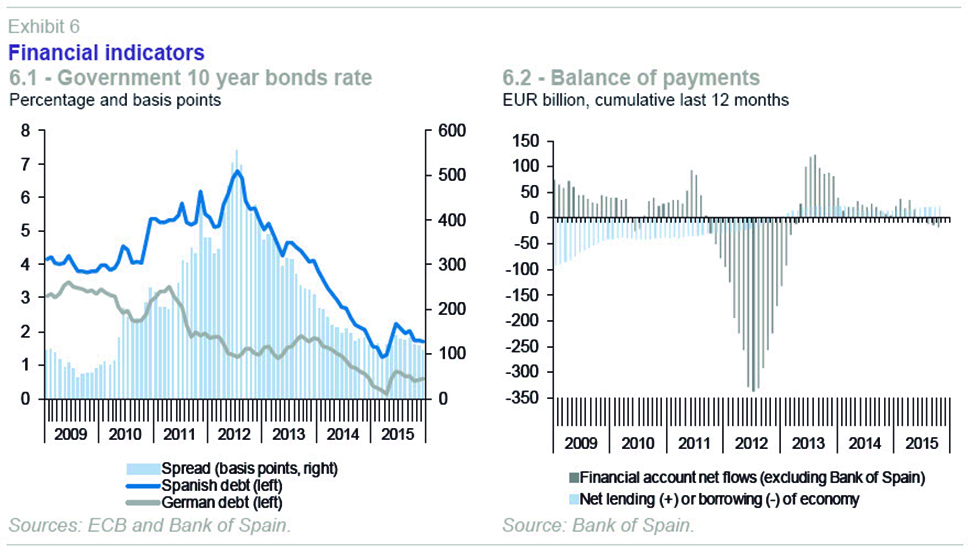

The balance on the financial account, excluding the Bank of Spain, posted a deficit (net capital outflow) of 41 billion euros to October, significantly higher than the 17 billion registered in the year-earlier period. This was a result of the drop in foreign investment in Spain and, above all, the increase in Spanish investment abroad (Exhibit 6.2).

The improvement in the economy’s net lending position was due to the fact that the national savings rate rose faster than the investment rate. With data to the third quarter, the increase in the savings rate came from firms and the general government – the latter presenting a less negative savings rate than in the previous year – while households reduced their savings.

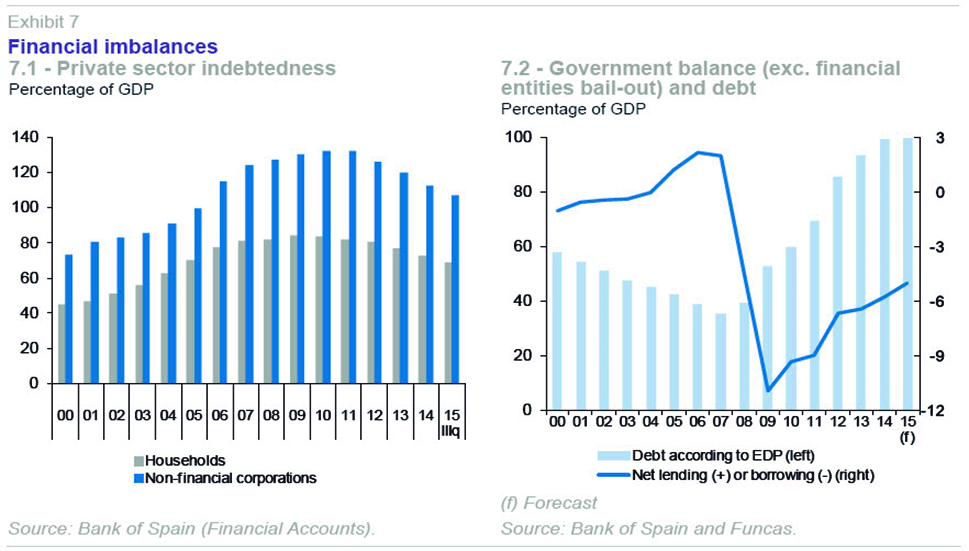

The general government, excluding local authorities, posted through October a deficit of 3.4% of GDP estimated for the year as a whole. This was five percentage points less than in the same period of the previous year (Exhibit 7.2). The target for the year as a whole is a reduction of 1.6 percentage points from the previous year’s level, bringing the deficit down to 4.2% of GDP. The deviation from this target is therefore likely to be significant. The sharp drop in interest rates (Exhibit 6.1) made it possible for interest expenditure to drop to 34.2 billion euros in 2015, a billion euros less than the previous year, despite public debt reaching over 99% of GDP. Interest expenditure represented 3.2% of GDP and 7.3% of total public expenditure.

Households presented a financial surplus again in 2015, as has been the case since 2009. In the period to September, households’ gross disposable income rose by 1.9% compared to the year-earlier period, due, in particular, to the increase in salaries. This surplus was used partly to purchase financial assets and partly to pay off debt, which in the third quarter stood at 107.7% of gross disposable income, compared to the maximum of 135% in 2008 (Exhibit 7.1).

Non-financial corporations also registered a positive financial balance, as a result of GVA growth, lower interest payments, and other payments from property. In this case as well, this surplus was used to purchase financial assets and pay off debt contracted in the form of loans. The sector’s total debt amounted to 107.2% of GDP in the third quarter of the year, compared with a peak of 132% in 2011.

Private agents’ deleveraging is not incompatible with growing levels of new credit. Credit to households, both for consumption and housing purchases, and business loans of less than a million euros – basically aimed at small and medium-sized enterprises – had already begun to grow in 2014. Growth continued in 2015, and the number of business loans of more than a million euros also began to increase. Total new credit in the period up to November grew by 15.6% compared to the year-earlier period. However, it should be borne in mind that this growth was from a very low starting point in comparison to the peak reached before the crisis – the total volume of new credit in 2015 was barely a third of that registered in 2007.

In short, the effects of permanent factors – balance sheet clean-up, completing the adjustment of the various demand components, availability of credit, and structural reforms – combined in 2015 with the impacts of a number of short-term factors, some of which were unforeseen – income tax cut, lower oil prices, falling interest rates, easing of fiscal policy – to give a strong stimulus to domestic demand. This made it possible for GDP to grow significantly faster than expected. The biggest cause for concern was the deviation of the public accounts from their target.

Outlook for the Spanish economy in 2016 and in the medium term

It is unlikely that 2015’s excellent result will be repeated in the next few years, as it was largely the outcome of the transitory exogenous shocks mentioned. Moreover, the protracted crisis seriously damaged Spain´s potential growth rate, which is what ultimately determines longer-term growth.

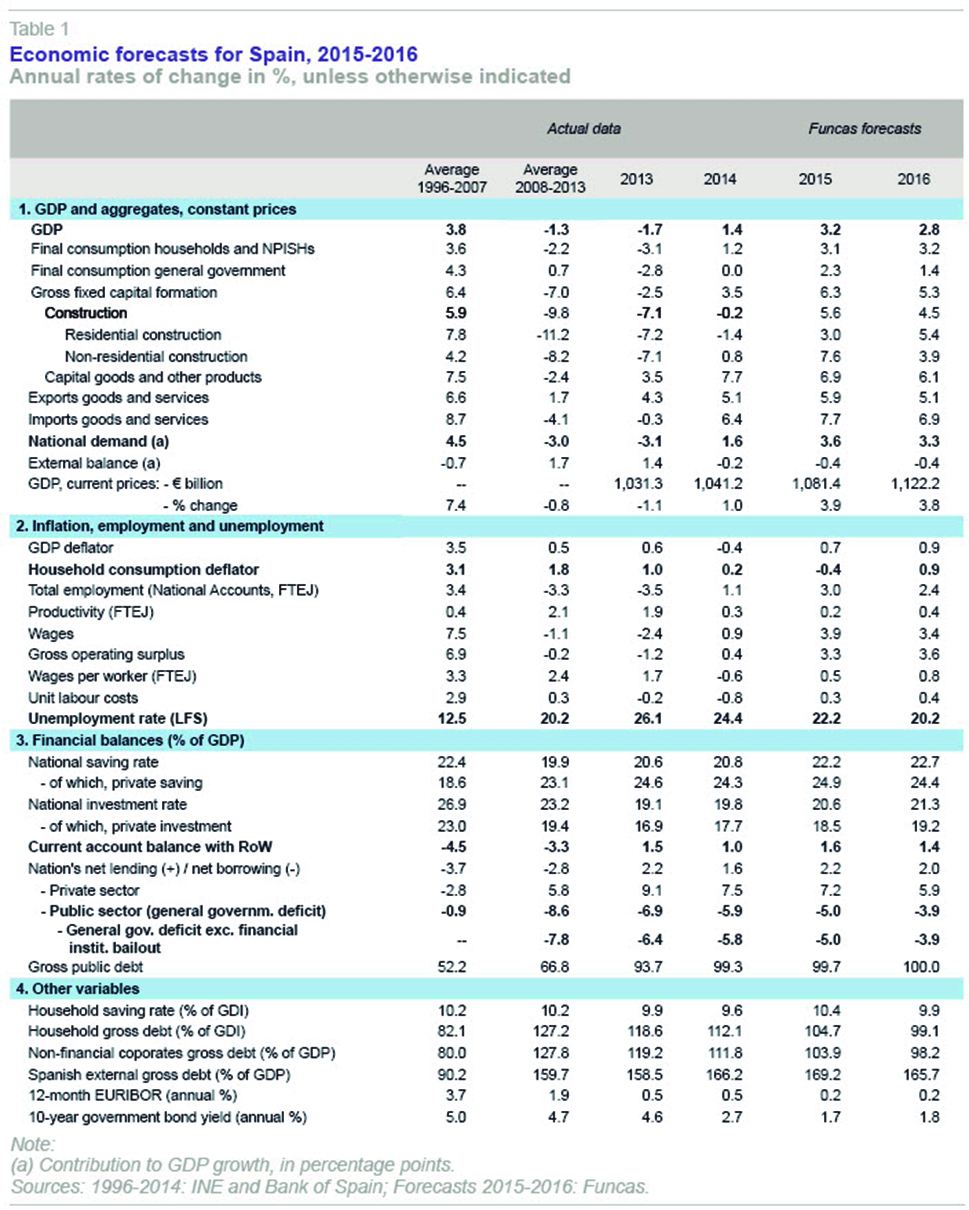

GDP growth of 2.8% is expected in 2016 (Exhibit 8.1 and Table 1). The key downside risks to this forecast being met derive from a worse than expected deterioration of the international context. The possible worsening of internal political uncertainties is another source of risk. These uncertainties may have an impact on growth, fundamentally through economic agents’ more pessimistic expectations and the potential impact on the risk premium and access to external finance. However, in the case of the latter, the European Central Bank’s current policy means a credit crunch such as that seen in the depths of the crisis can be ruled out. There is also an upside risk, basically the possibility of the oil price dropping below the reference value of 49 dollars (per barrel of Brent crude) used in this forecasts scenario.

Once again, economic growth will be driven by domestic demand, which will contribute 3.3 percentage points, while net exports will contribute -0.4 percentage points (Exhibit 8.2).

Private consumption is expected to rise by 3.2%. Although this is one tenth of a percentage point higher than was estimated for 2015, in reality the forecast is for a gradual deceleration in this component of demand’s quarter-on-quarter growth rates. However, the level reached following its rapid growth in the second half of 2015 has resulted in an acceleration when averaged over the year.

Equipment investment will slow to 6.1%, as it runs out of momentum after three years of strong growth. It will also be held back by the uncertainties looming over the global and Spanish economies. Construction investment will grow by 4.5%. The composition of the latter’s growth will be the opposite to that in 2015, i.e., the component playing the biggest part in the rise will be residential construction, which will gradually pick up speed as the property sector returns to normal, whereas non-residential construction will no longer be boosted by the electoral cycle (Exhibit 8.3).

Finally, both exports and imports will slow in 2016, to rates of 5.1% and 6.9%, respectively. Exports grew faster than global trade in 2015, which will continue to grow only moderately in 2016, such that the most likely outcome is a deceleration. For their part, imports will slow due to lower final demand growth.

As regards the labour market, employment is expected to rise by 2.4%, equivalent to 410,000 full-time equivalent jobs, while the average annual unemployment rate will come to 20.2% (19.5% in the last quarter) (Exhibit 8.4). Productivity will therefore grow somewhat faster in 2016 than in 2015, but compensation per employee will also rise, such that unit labour costs will progress at a similar rate.

The current account surplus and net external lending will drop to 1.4% and 2% of GDP, respectively, in 2016, due to the faster growth of imports than exports in real terms, which will no longer be offset by lower prices for imported energy (Exhibit 8.6).

Finally, the autonomous regions’ deficit will be situated at 3.9% of GDP, i.e., overshooting the official target (2.8%), and raising public debt to 100% of GDP. It should be noted that this forecast, like those for the economy as a whole, was made based, among other factors, on policies and measures known at the time. Obviously, significant changes to those policies once a new government has been formed would affect these forecasts, particularly as far as the budget is concerned.

As regards forecasts for future years, estimates of potential GDP growth, which is what determines the capacity for long-term growth, are very moderate (less than 1% per the European Commission’s estimates) as a result of two main factors. The first is the stagnation, or perhaps even decline, in the net capital stock resulting from the contraction of public and private investment during the crisis. And the second, the high percentage of long-term unemployment and the unsuitability of the qualifications of many of those out of work. In addition, other constraints on growth persist, such as the still high level of private debt, and the need for budgetary consolidation and to reduce the high level of public debt, which will make it necessary to maintain a restrictive fiscal policy over the next few years, limiting the growth of the stock of public capital.

However, these limiting factors will probably not prevent the Spanish economy from growing at rates of between 2.5% and 3% over the next three or four years. First of all, there is a lot of uncertainty in the calculations of potential GDP, particularly the rate of structural unemployment. This increases after a long period of recession or low growth – a phenomenon known as hysteresis – but in Spain’s case this may be offset by the effects of the labour-market reform undertaken, which has made labour relations more flexible, and thus reduced the structural unemployment rate. Unemployed workers’ qualifications may also be improved through active employment policies, which are currently being enhanced. In any event, hypothetical restrictions on the labour supply could, as has happened in the past, be alleviated with the right immigration policies.

The capital stock and its medium-term trend are also debatable, as the perpetual inventory method normally used may not be the most appropriate in the current circumstances. It is possible that the crisis has destroyed a high percentage of capital stock (by making early depreciation necessary) thus sharply reducing potential GDP growth. However, subsequently this depreciation (for reasons of age or technological obsolescence) has taken place more slowly and in smaller volumes than new gross capital formation, thus leading to a situation in which the capital stock is growing more than estimated in the production functions.

However, even if the modest potential GDP growth estimates are valid, it should not be forgotten that there is an output gap that will allow the economy to grow at faster-than-potential rates while it is being narrowed. With growth of around 2.5% this gap would not close until 2018.

In short, in the near term there are no major constraints on robust and sustained growth. In the medium term, the key is to increase the capital stock of existing firms or create new ones, which means maintaining or increasing business profitability and having low interest rates for an extended period, which seems within reach. In this regard, the current moderation in unit labour costs needs to be maintained, which is foreseeable while the unemployment rate remains high. The restrictions on labour supply seem to be smaller, despite which it is important to bolster active employment policies. Finally, an important issue in Spain remains improving total factor productivity. Economic policy needs to create incentives to raise TFP by supporting human capital formation, innovation, internationalisation, and better business management.

Notes

Consensus Forecast, by Consensus Economics Inc.

Spanish Economic Forecasts Panel, by Funcas.

Ángel Laborda and María Jesús Fernández. Economic Trends and Statistics Department, Funcas