Spanish economic forecasts panel: May 2025*

Growth in 2025

GDP growth estimate for 2025 remains at 2.5%

In the first quarter of 2025, GDP grew by 0.6%, according to the INE’s provisional advance, in line with expectations in the previous Panel. In addition, the INE revised quarter-on-quarter growth for the third and fourth quarters of 2024 from 0.8% to 0.7%, although with no effect on the annual growth rate, which remains at 3.2%.

The contribution of domestic demand to growth in the first quarter was four tenths of a percentage point, driven mainly by private consumption and investment. The foreign sector contributed two tenths of a percentage point, as a result of an increase in exports of services – especially non-tourist services – which more than offset the increase in imports.

With respect to the beginning of the second quarter of this year, some of the available indicators point to a slight slowdown. However, due to the outcome of the first quarter, in line with expectations, the consensus estimate of GDP growth for 2025 as a whole remains at 2.5%. Also, as in the previous Panel, the forecast for the contribution of domestic demand is 2.6 percentage points and that of the foreign sector is negative two tenths of a percentage point (Table 1). As for the quarterly profile, quarter-on-quarter rates of 0.5% are forecast for the second and third quarters, and 0.4% for the last quarter of the year (Table 2).

The majority of the panelists believe that the risk of their forecasts is balanced, i.e., they give similar probability to the deviation being upward as downward. Three panelists think the risk is to the upside and six to the downside.

Growth in 2026

GDP growth forecast for 2026 remains at 1.9%

The consensus forecast for GDP growth in 2026 remains at 1.9%. This figure is in line with both Bank of Spain and IMF projections, and below those considered by the Government, the European Commission and OECD (Table 1).

The deceleration with respect to 2025 reflects the expectation that domestic demand reduces its contribution to 1.9 percentage points (two tenths less than in the previous forecast), while the foreign sector would subtract one tenth from growth (instead of the negative two tenths predicted by the March Panel). Quarter-on-quarter GDP growth rates are forecast to be around 0.5% (Table 2).

Inflation

Inflation rate to remain above 2% during 2025

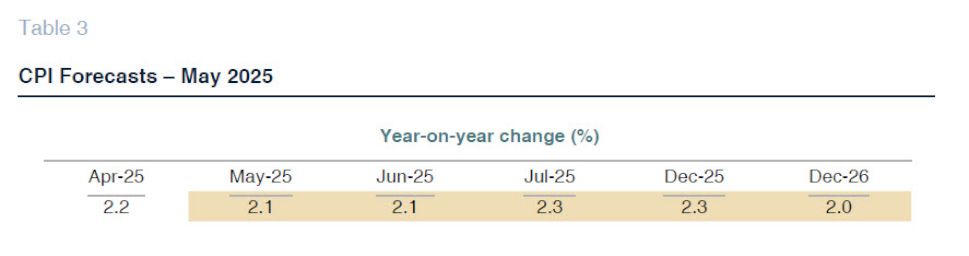

Headline inflation slowed, after rebounding in the first two months of the year, to 2.2% in April. Panelists believe that it will bottom out in the middle of the year and will pick up thereafter (Table 3). Core inflation, meanwhile, after standing at 2% in March (the lowest value recorded since the end of 2021), rose again to 2.4% in April.

For the year as a whole, an average annual rate of 2.5% is predicted for the general rate and 2.3% for the core rate, both unchanged with respect to the previous consensus forecast. For 2026, the projection for the general rate is 2% (one tenth less than the previous Panel) and 2.1% for the core rate (Table 1).

The year-on-year rates of the general index in December are forecast at 2.3% for this year and 2.0% in 2026 (Table 3).

Labor market

No signs of cooling in the labor market

The labor market continues to improve. According to the Labor Force Survey, employment increased by 0.7% in the first quarter, controlling for seasonal effects. The unemployment rate stood at 11.4%, nine tenths of a percentage point lower than in the same period of the previous year. The Social Security enrolment also maintained its positive trend.

The employment growth forecast for 2025 and 2026 remains unchanged at 1.9% and 1.4%, respectively. As a result, the unemployment rate would stand at 10.7% in 2025 (unchanged from the previous Panel) and would be reduced by three tenths to 10.4% in 2026, which is one tenth more than the previous forecast (Table 1).

Productivity and unit labor costs (ULC), calculated based on GDP growth forecasts, wage compensation and employment in LFS terms, would be 0.6% (the same as in the previous Panel) and 2.5% (one tenth of a percent lower), respectively, for 2025. For 2026, the forecast is 0.5% and 2.1%.

Balance of payments

Slight reduction in surplus at the beginning of the year

According to the revised figures, the current account balance recorded a surplus of 48.1 billion euros in 2024, which is the best outcome in the historical series in nominal terms, and one of the best results in relation to GDP, which was 3%, only below the historical maximum of 2016. The current account remained in surplus in the first two months of 2025, though slightly less than in the same period of 2024 (with a worsening of 3.6 billion euros).

The consensus forecast for the current account surplus is 2.4% of GDP by 2025 and 2.3% by 2026, which is three and two tenths of a percentage point lower, respectively, compared to the previous consensus projections (Table 1).

Public deficit

Government deficit forecast for 2026 has been lowered

The General Government recorded a deficit of 3.2% of GDP in 2024 (excluding DANA-related expenses, the deficit was 2.8%), compared to 3.5% in the previous year. In the first two months of 2025, a significant deterioration was recorded in the Central Administration accounts, while the Autonomous Communities and the Social Security funds improved their records. These results, however, should be interpreted with caution, as the first months of the year are typically not very representative.

The panelists expect the general government deficit to continue to shrink over the next two years, with a forecast of 2.9% for this year (unchanged from the March Panel) and 2.7% for 2026, two tenths of a percentage point lower than the previous consensus forecast (Table 1).

International context

An external environment marked by the trade war

The climate of global uncertainty has intensified, particularly since the announcement of strong trade restrictions by the Trump Administration on April 2nd (so-called “liberalization” day). After decreeing a general tariff of 10% and specific tariffs on each trading partner, the U.S. executive decided to suspend the latter to make way for a 90-day negotiation period. Since then, the U.S. has sealed agreements with the United Kingdom and China, resulting in a lower level of customs protection than announced last month, which, however, does not dispel all doubts. Trade negotiations with the European Union, meanwhile, have barely started.

In the face of the protectionist turn and the uncertainty surrounding the direction of U.S. economic policy, business confidence indicators have deteriorated and consumer inflation expectations have moved upwards. The decline in U.S. GDP in the first quarter (-0.1% quarter-on-quarter) is a first sign of the change in macroeconomic expectations – although the result probably magnifies the underlying trend, as it partly reflects a transitory rebound in imports.

In its spring round, the IMF reduced its growth forecasts for the world economy by half a percentage point for this year, and by three tenths for 2026. The U.S. and China would be among the economies most affected by the trade war. The eurozone should be less exposed, although the impact would reduce its already modest growth prospects. Among the large economies, the Spanish economy is projected to be the one that best withstands the shock, a prediction that coincides with the recently published forecasts of the European Commission.

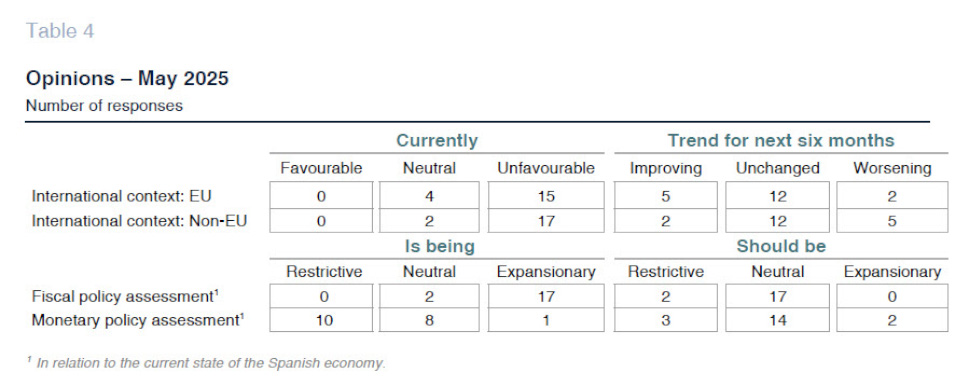

The turbulent international outlook is reflected in the Panel’s assessments. Of the 19 panelists, 17 are pessimistic about the global context, compared to 14 in the previous Panel, and most believe that this context will continue to prevail in the coming months. A majority of analysts also believe that the European environment is unfavorable and that this situation will persist in the short term, although in this case the number of negative opinions is slightly lower than in the March round (Table 4).

Interest rates

Financial market volatility and lower Euribor

Tariff escalation has been accompanied by increased volatility in financial markets. The U.S. stock market, after suffering heavy losses in the weeks following liberation day, has recovered as the executive’s position has softened. However, a certain amount of mistrust remains, generating a portfolio adjustment to the detriment of U.S. investment. The financial turmoil and economic slowdown, along with the prospect of a pickup in inflation, have complicated the task of monetary policy. For the time being, the Federal Reserve has opted to hold interest rates steady.

In Europe, the appreciation of the euro, lower oil prices and weak demand point to a disinflation scenario. Since the previous Panel, the ECB has cut its key interest rates further, leaving the deposit facility at 2.25%. Panelists anticipate a decline in the deposit facility to around 1.75% by the end of 2026, a quarter point below the previous Panel (Table 2). The slight downward trend in ECB rates is expected to be reflected in the one-year Euribor, whose rate is forecast to fall from the current 2.1% to 1.9% by the end of the year, two tenths of a point lower than in the March Panel (Table 2).

Spanish 10-year bond yields are expected to remain around 3.1-3.2% throughout the forecast period, with no major changes compared to the panelists’ previous assessment (Table 2).

Foreign exchange market

Appreciation of the euro against the dollar

The episode of financial stress that took place at the beginning of April following the restrictive turn in U.S. trade policy generated an outflow of financial capital to the euro zone and an appreciation of the common currency, which traded at around 1.15 dollars. Subsequent counter-announcements helped to ease tensions, so that the euro has fallen back to between 1.11 and 1.12 at the time of writing, which still implies an appreciation of close to 5% against the previous Panel. Analysts forecast the exchange rate to hover around current levels over the forecast period (Table 2).

*

The Spanish Economic Forecast Panel is a survey conducted by Funcas among the 19 analytical services listed in Table 1. The survey, which has been carried out since 1999, is published bimonthly in January, March, May, July, September and November. Based on the responses to the survey, “consensus” forecasts are provided, which are calculated as the arithmetic mean of the 19 individual forecasts. By way of comparison, although not forming part of the consensus, the forecasts of the Government, AIReF, the Bank of Spain and the main international organizations are also presented.