Improving valuations for Spanish and European banks

After years of trading below book value despite solid fundamentals, Spanish and European banks have seen a marked revaluation since late 2024, surpassing price to book value (P/BV) ratios of 1x. Improved margins have supported a strong recovery in valuations, narrowing the profitability gap with U.S. peers; however, structural and regulatory differences continue to explain the persistent valuation gap between European and U.S. banks.

Abstract: The Spanish and European banks have long traded at lower valuations than their U.S. peers, trading at significant discounts to book value. The fact that they traded at price-to-book ratios of less than 1x for 2022, 2023 and much of 2024 was hard to explain in light of the fact that the Spanish and European banks were reporting returns on equity (ROE) clearly above their cost of capital, as estimated by the supervisors, the entities themselves and market analysts. Possible explanations for this anomaly included a higher cost of capital than estimated by the sector itself or doubts about the sustainability of the ROE levels reported in 2022 and 2023. This situation has reversed since the end of 2024, with most of the Spanish and European banks currently trading above book value. Improved margins have supported a strong recovery in valuations, but structural and regulatory differences continue to explain the persistent valuation gap between European and U.S. banks. That said, margin gains have been priced in, and future margin stability is now expected, making sustaining fundamentals the key challenge going forward amid an increasingly uncertain global geopolitical environment.

ReArm Europe breathes life into bank valuations

Towards the end of 2024, and especially in early 2025, European and Spanish banks have seen sharp share price gains, in a highly uncertain geopolitical context that shaped both the rally and the subsequent correction. Specifically, this was driven by the new Trump administration’s stance on the conflict in Ukraine and European defence and, as a derivative, Europe’s strategic repositioning. This repositioning is articulated in the ReArm Europe programme and Readiness 2030 roadmap, a joint defence investment effort designed to deliver greater strategic autonomy, alongside a growing consensus around the need for capital markets integration and enhanced competitiveness.

This environment translated into markedly different financial market performances in Europe and the U.S. in the first quarter. The spike in uncertainty, the potential impact of Trump’s agenda on the economy and the reaction by third countries eliminated the “Trump trade”, a phenomenon coined in 2016. This phenomenon, characterised by heavy portfolio rotation into U.S. assets, faded away in the first quarter of 2025, reversing the trend observed throughout 2024.

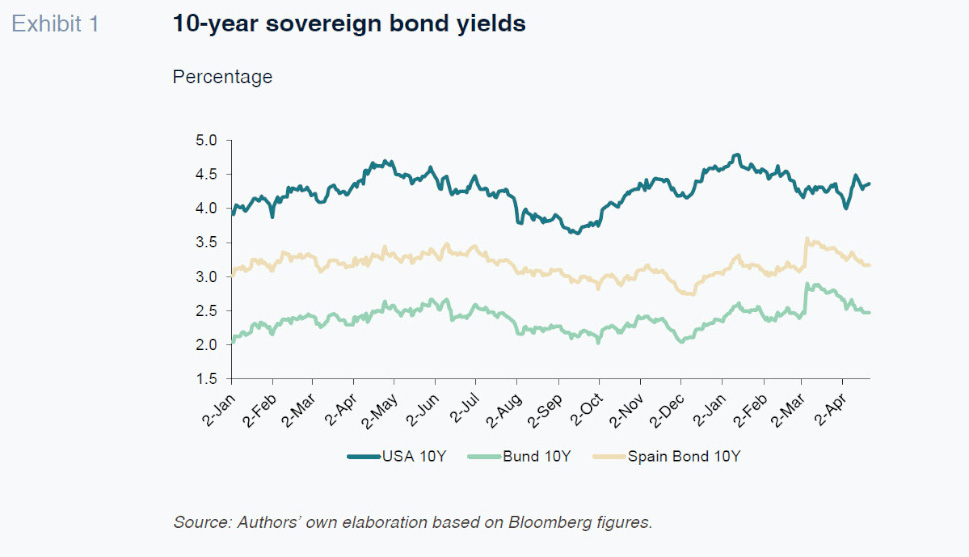

As shown in Exhibit 1, long-term U.S. sovereign bond yields traded lower from the start of Trump’s new mandate, as the markets began to price in an increasingly plausible economic slowdown. In contrast, 10-year Spanish and German bond yields intensified their uptick on the back of expectations for fiscal expansion spurred by ReArm Europe and the stimulus package announced by the German government.

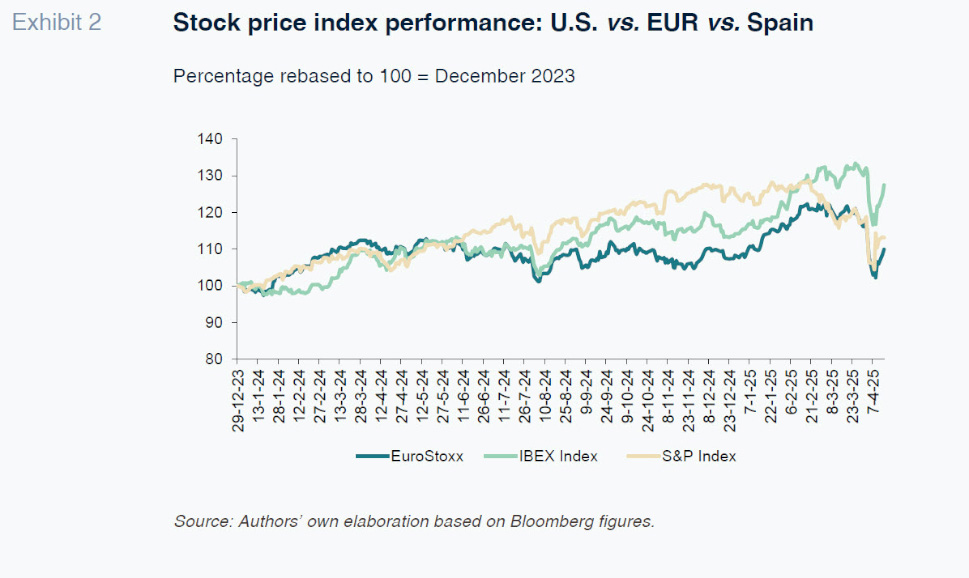

The stock markets have similarly etched out different paths on either side of the Atlantic, with the S&P 500 correcting since the start of the Trump mandate, while the Eurostoxx and IBEX have recorded valuation gains, more so in the case of Spanish stocks (Exhibit 2).

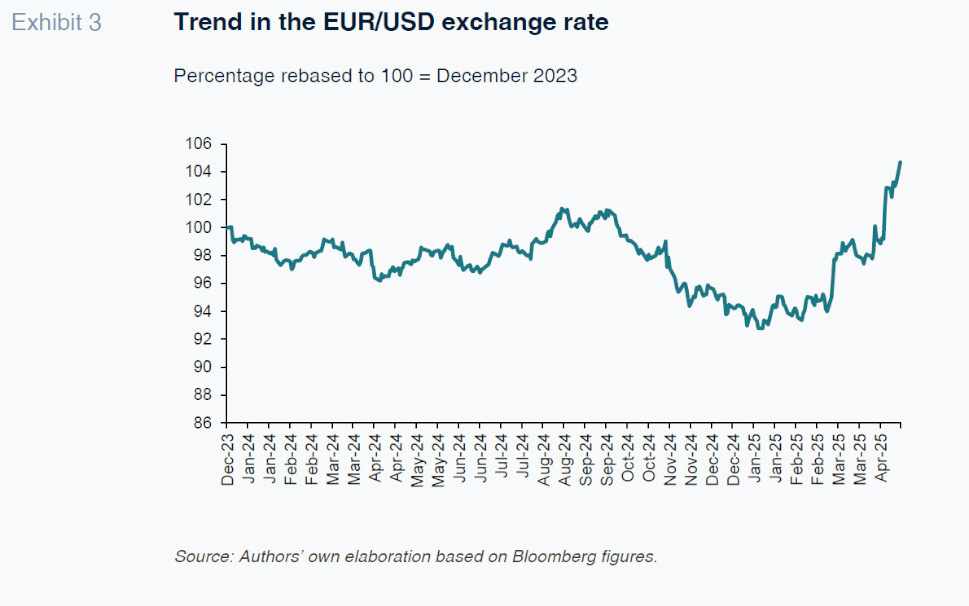

Elsewhere, Exhibit 3 depicts the resilience of the euro against the dollar since the onset of political and economic uncertainty in the U.S.. The rebound in the European currency suggests that the market is no longer pricing in U.S. economic hegemony as strongly as before.

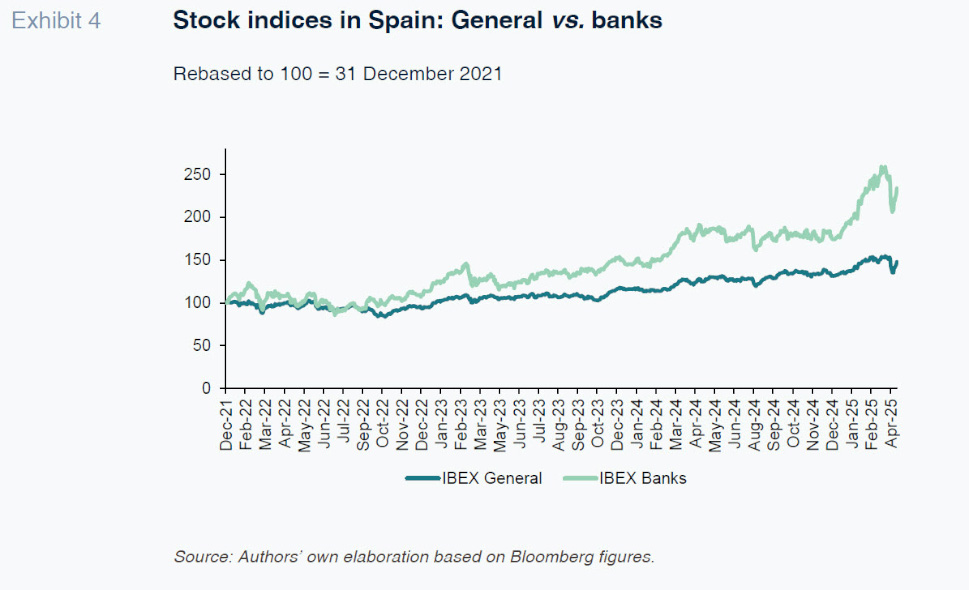

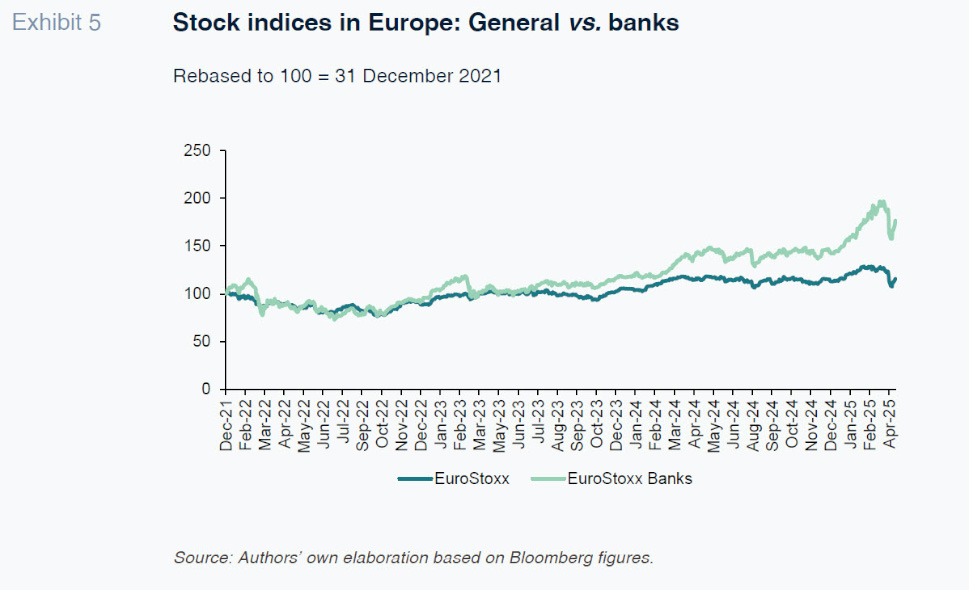

In this sort of European awakening, the sector experiencing the strongest rally has been defence, spurred by the ReArm Europe programme. Closely followed by the banking sector, which has notched up similarly noteworthy gains, significantly outperforming the general indices, with the Spanish sector performing even more strongly. In Europe, as of March 2025, the bank sector index had gained 85% since December 2021, compared to a gain of 22% in the general index. This valuation differential to March is even more pronounced in Spain, where the bank index was up by 143%, almost triple the gain registered by the IBEX over the same period (51%) (Exhibits 4 and 5).

This excellent first-quarter performance was followed by a bout of significant volatility at the beginning of April as a result of erratic communication by the Trump administration of its tariff policies based on bilateral deficit calculations, as well as its interference with monetary policy and the independence of the Federal Reserve. Both developments sparked episodes of pronounced volatility in the equity markets, but even more so in the two markets most sensitive to anything that could jeopardise financial stability: U.S. Treasuries and the dollar. Doubts have emerged in both of these markets about their continued status as safe-haven assets, and these concerns have unquestionably put pressure on the U.S. administration to soften its rhetoric on both tariffs and interference with the Fed, nuances that have, at least for now, calmed the extreme volatility observed throughout the first half of April.

European and Spanish banks: Downtrend in P/BV ratios

Despite the European banks’ strong performance over the past decade in terms of solvency, asset quality and, more recently, return on equity, thanks to Banking Union progress, they traded at a discount to their book values throughout that entire period. That valuation gap was being watched with interest, and some concern, by the regulators and supervisors, as it means that the market is applying a significant discount to the value of the banks’ own funds for accounting purposes, which are the basis of their capital adequacy ratios. In other words, the solvency perceived or priced in by the market is substantially lower than their solvency for regulatory purposes, which means that in the event of having to raise equity urgently, the cost would be very high in terms of dilution for existing shareholders.

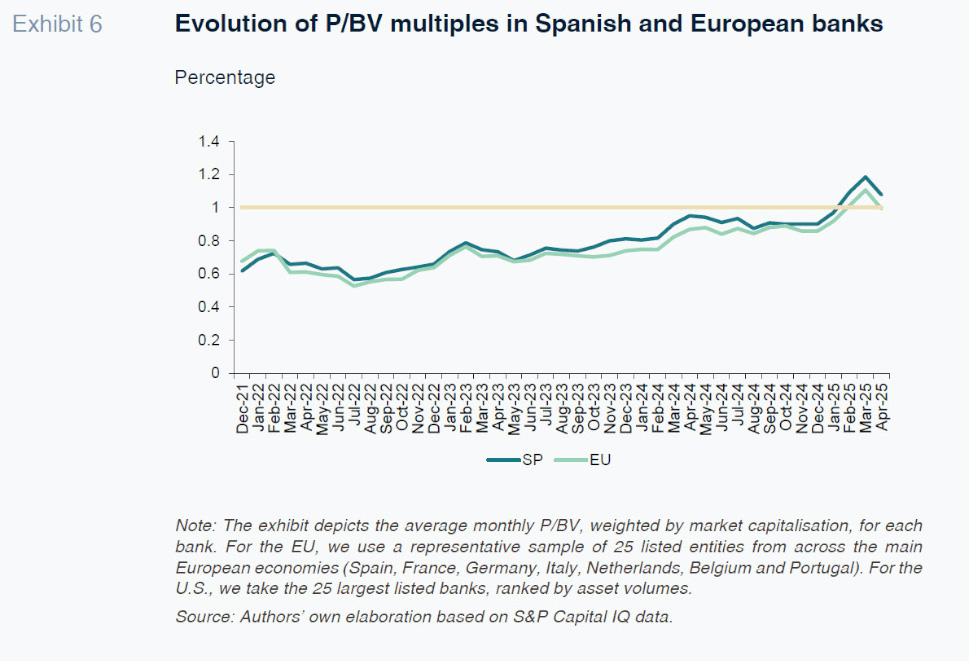

The good news is that the rally in European and Spanish bank stocks from the end of 2024 and through early 2025 closed that valuation gap, with many entities now trading at price to book value (P/BV) ratios of above 1x, casting off more than 15 years of undervaluation (Exhibit 6).

Spanish and European banks versus U.S. banks: The profitability gap is closing, especially in margins, but the valuation gap persists

Between 2022 and 2024, marked by the shift in monetary policy and the end of a prolonged period of ultra-low and even negative rates, the net interest margin has emerged as a key driver of the recovery observed in earnings across the European banks in general and the Spanish banks in particular, the result being a significant increase in profitability.

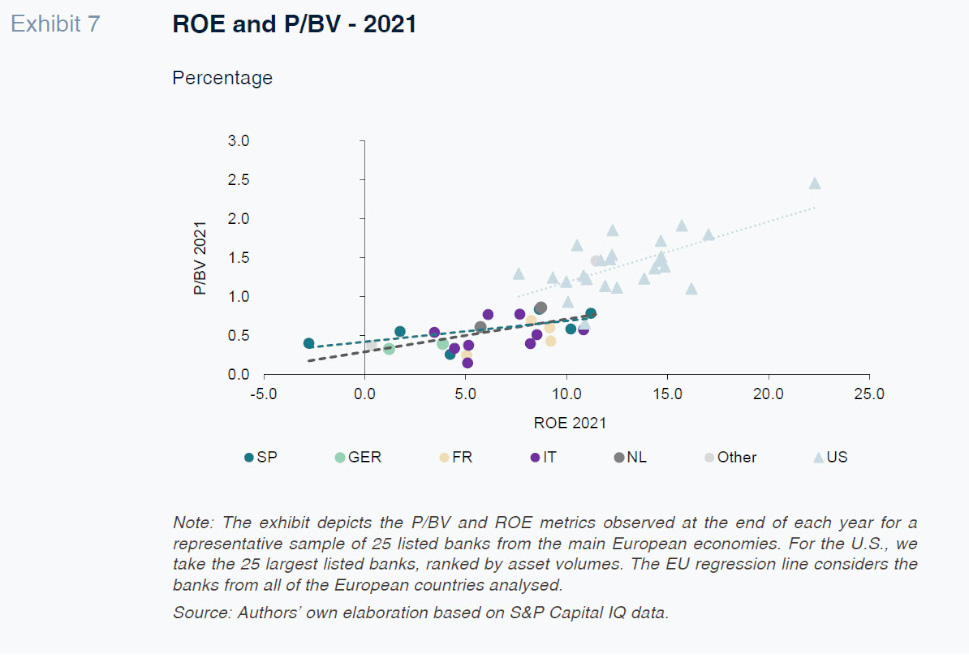

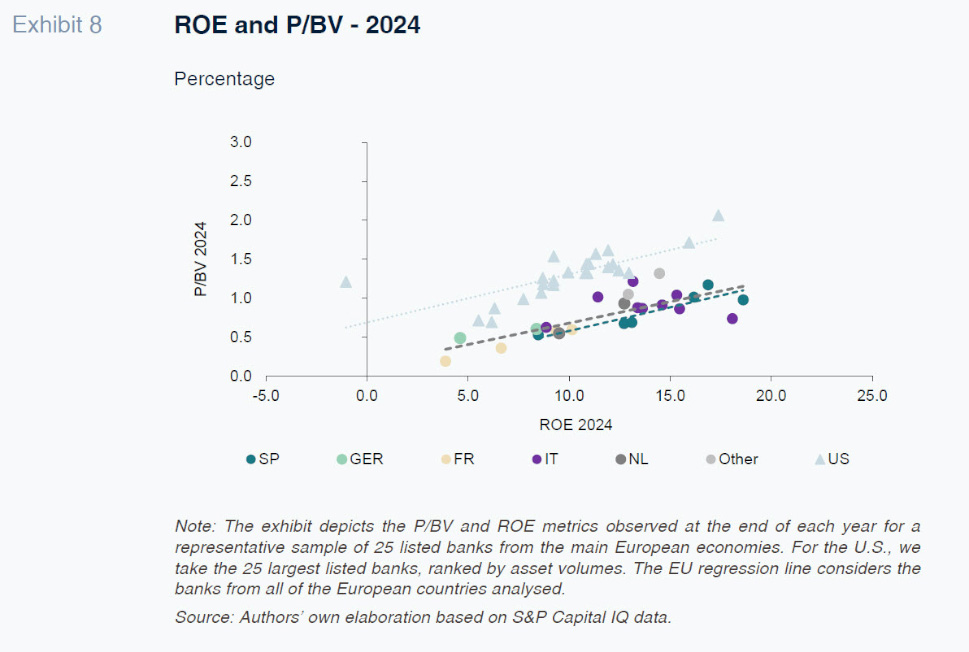

During the period of low rates, prior to the inflationary episode that began in 2022, the European and Spanish banks were posting much lower returns on equity (ROE) than their U.S. peers (Exhibit 7). The positive impact of rising interest rates on profitability, evident since the end of 2022, led to a notable improvement in returns across the European banking sector by the end of 2024. As gleaned from the comparison between Exhibits 7 and 8, the European banks have shifted to the right in terms of ROE (shifting more intensely in the case of the Spanish banks), narrowing the gap with the range of returns reported by the U.S. banks (Exhibit 8).

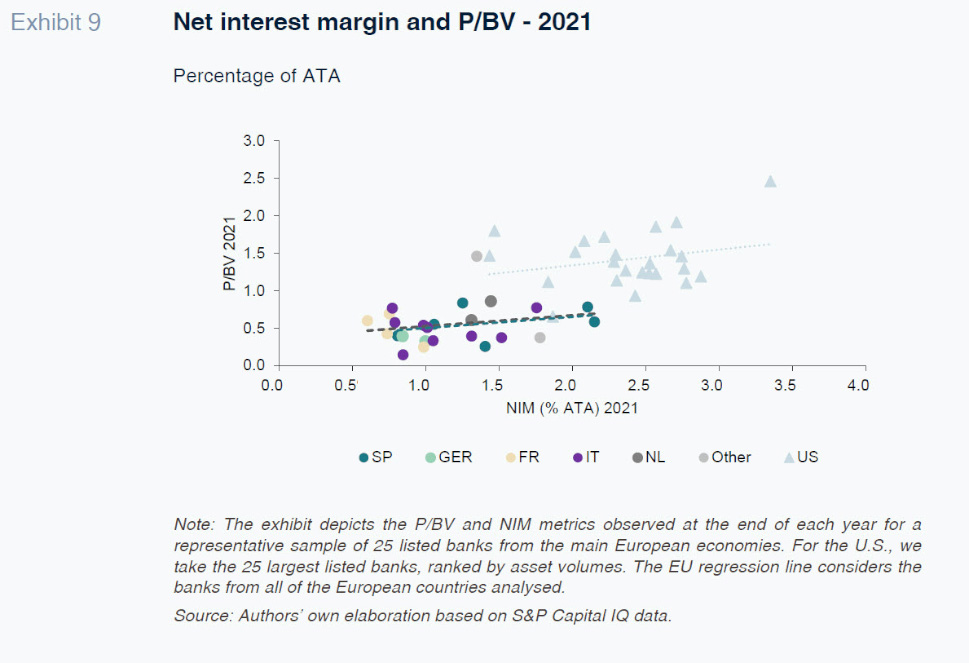

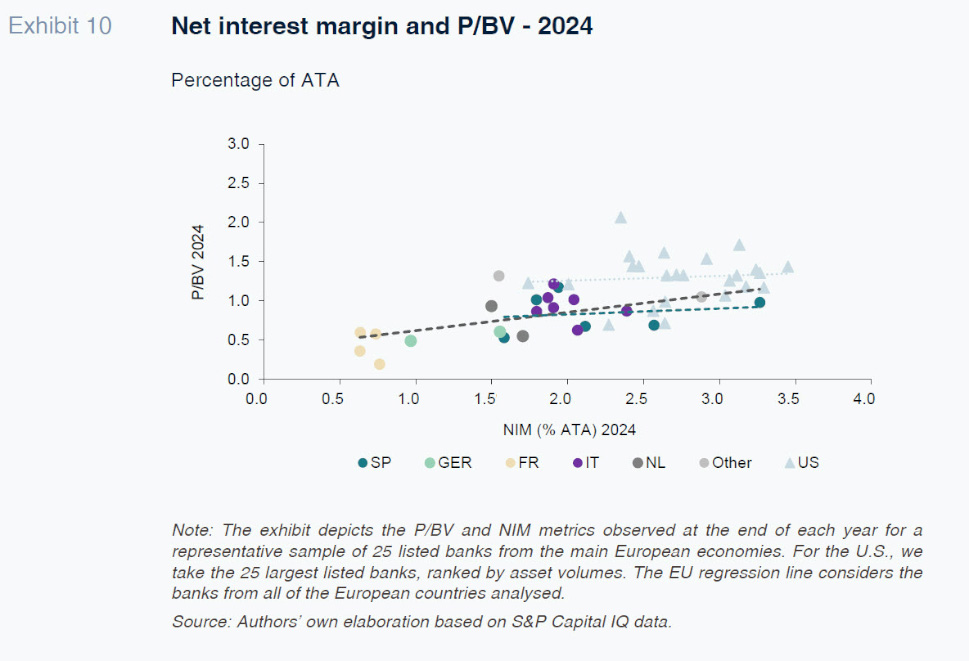

This shift (increase) in the European banks’ ROE mirrors the increase in their net interest income over average total assets (ATA), where the range for the European banks already virtually matches that of the American banks (Exhibit 10). This improvement in net interest margin (NIM) has been widespread across all the European economies, albeit more muted in certain markets, like France, where it has lagged due to country-specific structural factors, specifically the high share of fixed-rate loans and the existence of regulated savings products which have limited the banks’ ability to reprice their assets and kept deposit costs higher, a situation aggravated by intense price competition.

This widespread improvement in profitability – driven by net interest margins – across European and Spanish banks, combined with interest rate expectations at the end of the first quarter that pointed to greater margin stability, has been priced in by the market, translating into higher P/BV ratios. This trend has maintained the observed correlation between P/BV multiples and other fundamental variables such as ROE and the net interest margin, as is evident in the slope of the regression line.

Note, however, that despite the recent convergence in returns and margins with respect to the U.S. banks, the latter continue to command higher multiples than the European and Spanish banks. In fact, for U.S. banks, the regression lines between P/BV and ROE or P/BV and NIM are clearly steeper, suggesting that the market continues to assign greater value to each point of ROE or margin at those banks.

The persistence of this valuation gap relative to the U.S. banks, despite the narrowing of the profitability and margin gaps, may be related with structural differences between the two economies, as well as other considerations particularly relevant to the banking sector, such as the existence of laxer regulatory requirements in the U.S. and, above all, the expectation that those rules could be loosened even further under the new administration, which has already signaled its intention in this direction.

Conclusions

European and Spanish banks’ equity valuations have recovered considerably, correcting a prolonged anomaly where their stock prices systematically trading below book value, despite reporting returns above their estimated cost of capital. This revaluation was particularly pronounced between the end of 2024 and the first quarter of 2025, against the backdrop of the prospect of a coordinated European effort to enhance the region’s strategic autonomy and competitiveness, with the banking sector playing a key role in this process.

The convergence in terms of ROE and margins with U.S. banks reinforced this trend. However, a valuation gap persists, which may be attributable to structural differences between the two economies, regulatory factors and the expectation of loose regulatory requirements in the U.S. under the new administration.

Nevertheless, this new environment faces growing volatility and uncertainty as a result of the financial market stress triggered by the erratic stance of the U.S. Administration on tariff policies. In this context, the challenge for European banks lies with sustaining the improvement in their fundamentals and holding on to the market’s confidence in an increasingly unpredictable global landscape, with potential rate cuts and downward revisions to growth forecasts that could once again impact the banks’ business performance and margins.

Marta Alberni, Ángel Berges and Lucía Ibáñez. Afi