Structural adjustments and stability in European sovereign debt markets

European sovereign debt markets are undergoing significant structural shifts that simultaneously reduce demand and increase supply. Yet pricing stability has persisted amid geopolitical uncertainty, reflecting clearer policy signals and more predictable institutional responses.

Abstract: European sovereign debt markets are entering a period of structural change, with declining demand from the ECB and pension systems intersecting with rising supply linked to the green and digital transition, increased defence spending, and support for Ukraine. While these shifts imply hundreds of billions of euros in reduced demand and increased issuance, sovereign spreads have tightened and market functioning has remained notably stable by historical standards. This reflects clearer policy frameworks, greater transparency around ECB portfolio normalization, and more credible government signalling, which have allowed market participants to incorporate evolving demand–supply dynamics into pricing models. This relative stability is reassuring when compared to recent performance during moments of crisis. Market participants should continue to pay attention to the structural changes underway in European sovereign debt markets, but there is currently no cause for alarm.

Introduction

European sovereign debt markets have entered a period of unprecedented stability for the first time since the global economic and financial crisis. The difference (or spread) in Italian government bond yields over their German counterparts halved, from over 1 percent (or 100 basis points) to just over 60 basis points – the lowest in more than a decade. The spread over Germany for Spanish bonds also fell from over 70 basis points to just under 40 basis points – again the lowest in more than a decade. And the spread for French bonds fluctuated between highs near 85 basis points and lows near 65. [1]

The French spread is higher than France has experienced over the past decade, but still low in context. France has lacked a coherent government since French President Emmanuel Macron dissolved parliament in June 2024, French public debt is over 116 percent of gross domestic product (GDP), the minority cabinet is struggling to pass a budget, and the right-wing Rassemblement National has a strong chance to win the upcoming 2027 Presidential elections.

[2] Bond market participants are clearly aware of these facts and yet they do not appear to be pricing in the same kind of turmoil as they have in the past. That stability is interesting because European sovereign debt markets are also changing both in terms of demand and supply.

Demand for European sovereign debt is expected to shrink. The European Central Bank (ECB) is running down its large-scale asset portfolio holdings as it moves toward a new operational framework for connecting changes in the policy through the financial system to the performance of the European economy. [3] In that new framework, the ECB will hold more debt on its portfolio than it did prior to the global economic and financial crisis, but less than it held during the sovereign debt crisis or in the aftermath of the pandemic. At the same time, many pension companies and national pension systems are moving from defined benefit to defined contribution schemes. This changeover will reduce demand for sovereign debt as very long-term assets to match against equally longer-term obligations. Together these moves will subtract demand for sovereign debt worth hundreds of billions of euros. [4]

Meanwhile, the supply of European sovereign debt is expected to rise. Both national governments and European institutions need to issue new debt to cover the costs of the green and digital transition in line with the recovery and resilience programme (Next Generation EU) agreed in July 2020 (European Commission, 2025b). At the same time, Europe is taking on a greater share of the cost of supporting Ukraine in its efforts to defend itself after Russia’s February 2022 full-scale invasion and the Donald Trump administration’s decision to cut American support (European Commission, 2026). European governments are also planning to increase defence spending in light of efforts to stabilise relations within the NATO alliance and concerns about the need to assume responsibility for European security in the event the United States withdraws some or all of its security guarantees. The European Commission’s ‘White Paper for Defence – Readiness 2030’, calls for an additional €800 billion in defence spending (European Commission, 2025c). Although the precise formula for financing this expenditure remains to be seen, net supply of sovereign debt should rise by hundreds of billions across Europe as a result.

These factors are well known among financial market participants. Yet an expected fall in demand and rise in supply does not seem to be adding pressure into European sovereign debt markets. If anything, those markets are moving the other way. This suggests that although there are good reasons to pay attention to these structural changes in European sovereign debt markets, they are not cause for alarm. On the contrary, other factors may be more important.

Demand

The changes in demand for European sovereign debt have been underway for a long time. The Governing Council used the large-scale asset purchase programme to support European economic performance during the sovereign debt crisis and a separate pandemic emergency purchase programme in response to the economic shock caused by COVID-19. At their peak, these two programmes respectively pulled €2.6 trillion and €1.7 trillion in sovereign debt instruments out of the markets. The Governing Council of the ECB decided to end new purchases and then stop reinvestment of maturing principal on the asset purchase programme in July 2023 and the pandemic emergency purchase programme in December 2024. By the end of 2025, the sovereign debt holdings on those programmes had shrunk to €1.9 trillion and €1.5 trillion. In other words, the ECB has already returned close to €1 trillion in sovereign debt to the markets by allowing them to mature so that they are rolled over elsewhere. [5]

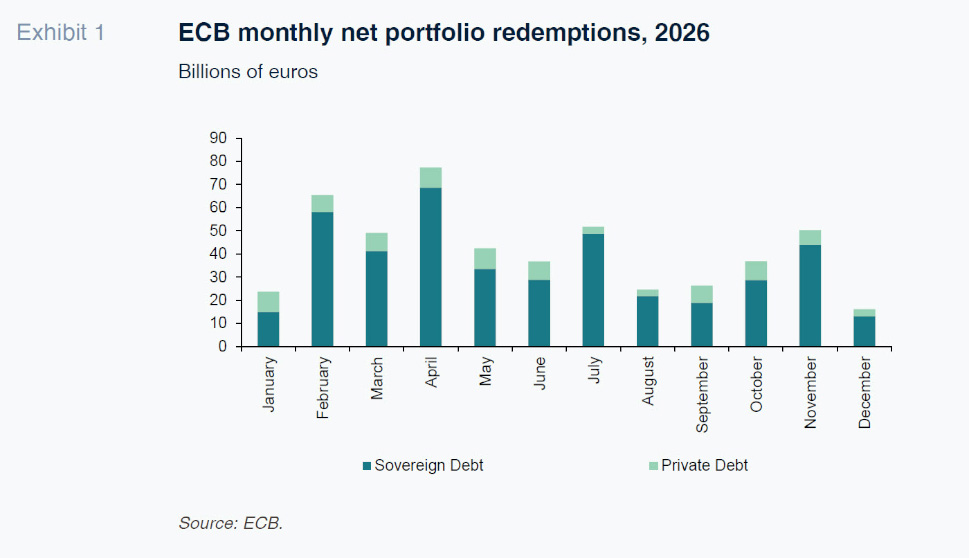

The expectation is that the ECB will return another €420 billion in sovereign debt from those two programmes to the market in 2026 – with €250 billion running off the large-scale asset programme and the rest coming from the pandemic emergency programme (See Exhibit 1). This is on top of €80 billion in private assets that will be allowed to mature on both sets of accounts. [6] These numbers are important, but the expectation is that actors in the private sector will make good use of the sovereign debt instruments that are released. Much will be reabsorbed for use as collateral both in routine treasury operations made by financial and non-financial institutions and eventually with the ECB. This transition is part of a strategy for the ECB’s Governing Council to wean financial institutions off their dependence on central banks to meet their regulatory liquidity requirements and provide a buffer of excess liquidity.

The scale of that dependence is clear from the daily liquidity reporting that the ECB provides. On 7 January 2026, for example, European financial institutions had regulatory reserve requirements worth €170 billion. The consolidated accounts show that the current account balance for those institutions stood at €157 billion, they borrowed another €22.7 billion through open market operations, and some banks even requested loans worth €69 million from the ECB’s marginal lending facility. Meanwhile, that same collection of financial institutions had central bank deposits worth €2.49 trillion. By implication, the ‘excess liquidity’ in the banking system – which is the sum of holdings on the current account and deposit facility, less reserve requirements and any money borrowed on the marginal lending facility – stood at €2.48 trillion. That excess liquidity comes from the ECB’s asset holding.

By returning those assets to the market, the Governing Council hopes to draw down that surplus liquidity and restart inter-bank lending markets. Governing Council members do not expect those interbank markets to return to what they were before the financial crisis, but they see significant room for growth, particularly in collateralised lending. There is space for the ECB to engage in more collateralised lending as well, using a mix of shorter- and longer-term refinancing operations to ensure financial institutions have access to sufficient buffers in case of stress. If those banks decide they need large volumes of excess liquidity, they can always borrow from the ECB and those same sovereign debt instruments currently held as assets will show up on the ECB’s balance sheet as collateral. That changeover could start as soon as the second or third quarter of 2026, though it is expected to begin later. In either case, the sovereign debt instruments being released into the markets will be put to good use. Toward the end of that process, the ECB will create a structural portfolio of bonds that it holds outright to complement these refinancing operations in a process ECB Executive Board Member Isabel Schnabel calls ‘quantitative normalisation´. [7] The final arrangements are still to be worked out, but the plan for doing so is well in place.

The pension case is less complicated. A shift from a defined benefit to a defined contribution regime does reduce the demand for ultra long-term debt. But those debt markets are relatively small. To give a sense of relative magnitudes, the Italian government had €2.5 trillion in government bonds outstanding with a maturity of one year or more. The vast majority of those bonds – 78% or €1.95 trillion – had a residual maturity of ten years or fewer. This number contains some older or ‘off-the-run bonds’ that were issued with longer maturities. The next 14%, or €340 billion, had residual maturities between 10 and 20 years. And the last 8%, or €210 billion, had residual maturities between 20 and 50 years (Bank of Italy, 2026: 1).

While these might look like significant numbers, the implication is that the average volume of debt issued by the Italian state in any given year with a maturity greater than 10 years is just under €14 billion. This means that the share of off-the-run bonds that started off with long maturities and now has a residual maturity of ten years or fewer is no more than €140 billion out of €1.95 trillion. The pension funds may not roll these bonds over like-for-like, but the extra €14 billion in average annual refinancing is just a small fraction of the €250+ billion that turns over on an annual basis. More importantly, the shift from defined benefit to defined contribution only affects the appetite for pension funds to hold debt obligations with very long maturities. It does not affect their appetite for sovereign debt. Hence this regulatory change is more likely to influence what kind of sovereign debt pensions buy than to take significant demand from the markets.

Meanwhile, the result is likely to lower debt servicing costs for the Italian state. When much of existing very long debt was issued over the past 15 years, the yield curve was relatively flat. As inflation accelerated after the pandemic, that yield curve steepened. In January 2022, for example, the difference in yield between 10-year and 30-year AAA bonds was just 29 basis points, or 0.29 percent. By January 2026, the gap had increased to 56 basis points.

[8] Italian bonds trade at a discount to AAA and so the increase would be greater because the premium charged to cover risk to maturity would increase over time. Italian Treasury officials might prefer to issue longer bonds to lengthen the average maturity of their outstanding debt, but the trade-off in terms of debt servicing costs is positive – even if marginal, given the very low volumes involved.

Supply

The supply-side issues are less straightforward than they seem as well. It is true that both national governments and European institutions will issue new debt to cover expenses related to the recovery and resilience facility created during the pandemic. The point to note, however, is that while the amount to be borrowed is significant, it is also much less than the Next Generation EU programme originally promised. When the programme was announced in 2020, the headline number was €750 billion, with €390 billion in grants and another €360 billion in loans – all of which would be financed in the markets. When they adjusted the base year to the start of the project in 2021, the total came to €800 billion.

That adjustment was before the acceleration of inflation after the pandemic in 2022. It was also before the member states ran into expected troubles building coalitions to support specific programmes, finding relevant projects, working through bureaucratic procedures, or translating that money into spending (Jones, 2021a). Along the way, the European Commission made it possible to redirect some of the funds to support a transition away from Russian energy and to purchase military equipment related to the European response to Russia’s full-scale invasion of Ukraine. Even so, the total amount that was disbursed by the end of 2025 was ‘just’ €362 billion.

[9] Moreover, because of inadequate take-up of the funds being offered, the overall envelope shrank to €637 billion – in post-inflation euros.

[10] Whether that money can be committed before the end of September 2026 or spent before the end of December is an open question. Given historical precedents in terms of Member State absorption of regional and structural funds, it is unlikely.

This accounting is not meant as a criticism of the recovery and resilience facility. On the contrary, that proposal played a vital role in stabilising European bond markets during the pandemic (Jones, 2021b). It has also fostered important investments in green and digital technology, energy independence, and European security. The point is simply that financial market participants had already imagined a much larger level of borrowing. Even the addition of €90 billion for Ukraine does not bring the total up to the original headline figures. Meanwhile, national borrowing to accompany the programme is similarly reduced.

The real challenges this new borrowing represents are not an increase in supply of sovereign debt instruments but rather the lack of promised productive investment (European Commission, 2025b). The Next Generation EU programme had greater potential than EU governments have been able to realise. It is also worrying that Member State governments did not agree on the necessary financing that was originally promised. As a result, servicing the debt is threatening to take away resources from the European budget. That issue will need to be dealt with in the negotiation of a new multiannual financial framework for the European Union to be implemented starting in 2027. In the meantime, it would be helpful if European officials – including heads of state or government – would agree to roll over existing EU debt to avoid cutting back even further on productive spending of shared resources (Busse et al., 2025).

A similar point could be made about borrowing for defence spending. The borrowing involved is significant. The concern is about contribution to growth and hence also debt sustainability. Defence spending has a highly variable fiscal multiplier. A euro of defence spending can generate just €0.60 in additional economic output, or something closer to €2.40 (Erken et al., 2025: 7). From a debt sustainability perspective, a higher multiplier is better, because it implies that each euro spent on defence generates more than a euro in gross domestic product (GDP) and hence also a positive contribution to longer term tax revenues and therefore also government ability to pay down the resulting debt. This creates a seemingly paradoxical situation where borrowing the money for increased defence outlays up front results in a more stable fiscal situation over the medium term (Ilzetzki, 2025: 34-36).

The policy challenges associated with a rapid military buildup are significant. Moreover, European policy makers are aware of the concerns. In its spring economic forecast, the European Commission concluded that the net result of increases in defence spending would be a modest increase in growth with little impact on underlying inflation. The Commission also made recommendations for how those macroeconomic outcomes could be strengthened to ensure greater productivity gains (European Commission, 2025: 81-86). This analysis did not include all of the commitments made in the rest of the year, but the Commission’s analysis and similar arguments set a solid baseline for market participants to interpret the outcomes. [11]

Conclusion

European sovereign debt markets are changing in structural terms to rely less on demand from the European Central Bank and due to new requirements on large institutional investors while at the same time accommodating an increase in borrowing both of needed investment and to reinforce European security. These adaptations are taking place against a backdrop of heightened geopolitical risk and uncertainty. Nevertheless, European bond markets are adapting smoothly to the new conditions. The smoothness of this adaptation suggests important improvements in European financial market performance when compared to the turmoil that surrounded the global economic and financial crisis, the sovereign debt crisis, the pandemic, and Russia’s full-scale invasion of Ukraine.

The explanation is probably that market participants have known for a while now that these structural changes were coming. The European Central Bank could not maintain such a large asset portfolio indefinitely. Large pension funds could not remain committed to defined benefit programmes. European governments needed to invest in the digital and green transition while at the same time adapting to other shocks, even if they have yet more to accomplish. And Europe needs to provide for its own security in a troubled and uncertain international climate. That European policymakers recognize and are acting on these concerns is reassuring – or at least that seems to be what sovereign debt market participants are telling us.

Notes

Data for France´s debt-to-GDP ratio is taken from the AMECO database of the European Commission.

These numbers are based on own calculations using ECB data. Those calculations are available upon request.

These data come from the ECB.

References

BANK OF ITALY. (2026). Quarterly Bulletin: Detail on Public Debt Issuance Activity – IV Quarter 2025. Rome: Ministry of Economics and Finance, Department of the Treasury, January.

BUSSE, M., HUIDAN, L,., NABAR, M., and YOO, J. (2025). Making the EU’s Financial Framework Fit for Purpose. IMF Working Paper 25/114. Washington, D.C.: International Monetary Fund, 2025.

ERKEN, H., VAN ES, F., DE GROOT, E., and DE JONG, L. (2025). Europe in the New NATO Era. SUERF Policy Note, no 372. Vienna: SUERF – The European Money and Finance Forum (July).

EUROPEAN COMMISSION. (2025a). European Economic Forecast, Spring 2025. Institutional Paper 318. Brussels: European Commission, May.

EUROPEAN COMMISSION. (2025b). NextGenerationEU – The Road to 2026. Brussels: European Commission, COM(2025) 310 final/2, 4 June 2025.

EUROPEAN COMMISSION. (2025c). White Paper for European Defence – Readiness 2030. Brussels: European Commission, 28 March 2030.

EUROPEAN COMMISSION. (2026). Proposal for a Regulation of the European Parliament and of the Council Implementing Enhanced Cooperation on the Establishment of the Ukraine Support Loan for 2026 and 2027. Brussels: European Commission, COM(2025) 20 final, 14 January 2026.

ILZETZKI, E. (2025). Guns and Growth: The Economic Consequences of Defense Buildups. Kiel Report 2. Kiel: Kiel Institute for the World Economy (February).

JONES, E. (2021a). Did the EU’s Crisis Response Meet the Moment? Current History, 120 (2021), 93-99.

JONES, E. (2021b). Next Generation EU: Solidarity, Opportunity, and Confidence. European Policy Analysis 2021:10epa. Stockholm: Swedish Institute for European Policy Studies (SIEPS), June 2021.

Erik Jones. Director of the Robert Schuman Centre for Advanced Studies at the European University Institute and Nonresident Scholar at Carnegie Europe