Shadow banking and financial stability in an era of private credit

The rapid expansion of non-bank financial institutions is reshaping the geography of financial risk in Europe and globally. High leverage, liquidity mismatches, and growing interconnections with traditional banks raise the probability that future episodes of stress originate outside the regulated banking perimeter.

Abstract: The non-bank financial institution (NBFI) system, commonly referred to as shadow banking, has reached systemic scale and is now a central feature of global financial intermediation. In Europe, non-bank financial institutions manage more than €50 trillion in assets, around 42% of the financial system, while global private credit has surpassed $3 trillion, expanding rapidly outside the traditional regulatory perimeter. This growth is accompanied by structural vulnerabilities linked to high leverage, liquidity and maturity mismatches, and increasingly dense interconnections with banks. Exposures between banks and non-bank entities already amount to trillions of dollars, concentrating risks in a small number of systemic institutions and increasing the potential for two-way contagion. Spain shows a lower domestic weight of non-bank finance, at roughly 34% of the system, but remains exposed through international funds, leveraged credit markets, and indirect banking channels. Shadow banking has become a durable source of both diversification and fragility, strengthening the case for integrated monitoring, cross-sector stress testing, and coordinated regulatory responses.

Introduction: Boom in the non-bank financial system and echoes of 2008

In recent years, the non-bank financial system—also known as shadow banking or NBFS—has experienced rapid growth globally. According to the latest data from the Financial Stability Board, the total value of shadow banking assets amounts to $238.8 trillion, representing around 49.1% of total global financial assets. Organizations such as the International Monetary Fund (IMF), the Financial Stability Board (FSB), and the Bank for International Settlements (BIS) have recently warned that this boom is accompanied by structural vulnerabilities reminiscent of the imbalances that preceded the 2008 crisis. Although there are differences between the current context and that of fifteen years ago, some similarities are cause for concern: increasing leverage, opacity in certain investments, dependence on private credit ratings, and high financial interconnection between banks and non-bank entities.

The IMF´s Global Financial Stability Report (October 2025) highlights that the expansion of private financing funds and leveraged credit markets is taking place outside the traditional regulatory perimeter, with less transparency, more lax lending standards, and liquidity structures that are susceptible to amplifying tensions. This "private financing ecosystem" is no longer marginal but has become a structural component of the global financial system, capable of transmitting shocks through its growing interconnectedness with banks and markets. Even the role of rating agencies shows parallels with 2008: before the great crisis, they assigned high ratings to complex products (CDOs, ABSs, RMBSs) whose real risk they underestimated. Today, the BIS warns that some smaller agencies may be assigning excessively favorable ratings to private debt issues, incentivized by commercial reasons, which may conceal risks of illiquidity or overvaluation. In addition, there are also doubts about other new ratings, such as those based on sustainability criteria. The relevance of these ESG ratings has been increasing. They currently condition the investment flows of many NBFI entities such as investment funds, pension funds, and insurers. The opacity of the criteria and metrics used to assign these ratings, coupled with their heterogeneity, adds an additional layer of uncertainty and risk to the financial system. In short, while not identical to that of 2007–2008, the current situation shares certain mechanisms of fragility that warrant close monitoring.

In this article, we analyze the magnitude of this phenomenon on a global and European scale, and its implications for financial stability, paying specific attention to the Spanish case.

Global outlook: The rise of private credit and leveraged credit

Non-bank credit intermediation has become one of the main drivers of global financial growth. In particular, private credit (direct private financing to companies by investment funds, outside the traditional banking circuit) has emerged strongly. Unlike banks, private credit funds operate with "locked-in" investor capital (they do not have demand deposits), which eliminates the risk of bank runs but implies less supervision and possible liquidity mismatches. Their flexibility in structuring loans tailored to borrowers has made them formidable competitors to banks in certain niches (e.g., financing leveraged buyouts [LBOs]), while also making them partners in others (e.g., jointly financing large transactions).

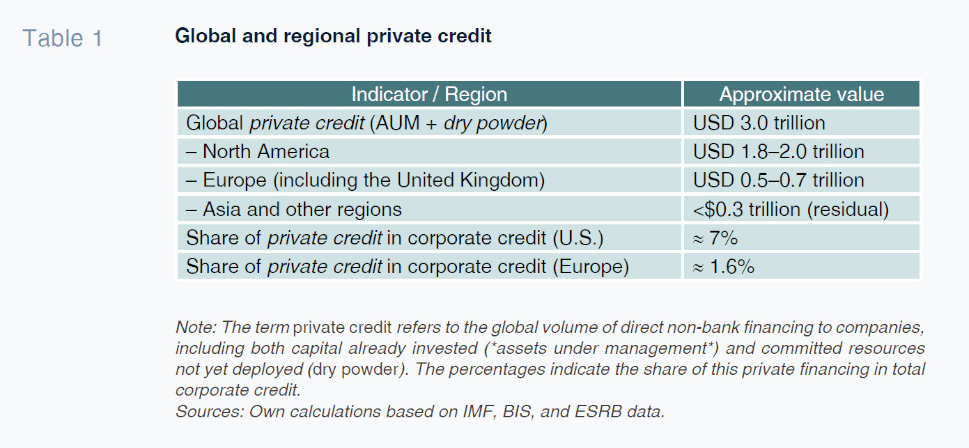

Global figures: Private credit by region

Aggregate data reveal that the

private credit market has already reached systemic dimensions. According to recent estimates, assets under management plus committed capital pending investment (known as "AUM + dry powder") will exceed $3 trillion by the end of 2024. This figure contrasts with just $2 trillion in 2020, reflecting rapid growth in just a few years. Table 1 summarizes the global and regional scale of this market, as well as its relative weight in corporate financing.

Two structural trends stand out from these figures: (a) The global private credit market rivals traditional segments such as high-yield bonds and leveraged loans in size, especially in the United States. In fact, in this country, the volume of private credit in circulation (around USD 1.8–2 trillion) is comparable to the entire market for syndicated bank loans or junk bonds; (b) Europe, although lagging in absolute volume, is demonstrating accelerated growth dynamics. Capital managed by private credit funds in Europe has tripled in the last decade, exceeding €0.4 trillion in 2024, and continues to rise. However, its share of total European corporate credit remains modest (around 1–2%), reflecting the fact that corporate financing in Europe still relies overwhelmingly on traditional banking.

Leveraged credit: High yield and leveraged loans on the rise

Beyond pure private credit, the universe of leveraged credit—which encompasses high-yield debt (speculative-grade high-yield bonds) and leveraged loans to highly indebted companies—continues to expand outside the banking sphere. This type of credit played a central role in the spread of the subprime shock in 2007–2008 and is once again the focus of attention today. In the United States, the sum of the high-yield bond markets (USD 1.8–2.0 trillion) and leveraged loan markets (USD 1.0–1.5 trillion) is around USD 2.8–3.0 trillion. This figure equals or even slightly exceeds the size of global private credit, illustrating the magnitude of higher-risk credit circulating in the system. Each segment accounts for approximately half: for example, the U.S. leveraged loan market is estimated at around USD 1.4–1.5 trillion (an all-time high), while the U.S. junk bond market is around USD 1.5–1.8 trillion. In Europe, the leveraged credit market is less than half the size of the U.S. market, with total estimates of around €1.1–1.3 trillion (including high-yield bonds issued in euros and leveraged syndicated loans).

One warning sign highlighted by the IMF is the deterioration in underwriting quality in recent leveraged credit. Specifically, there is a growing proportion of loans with lax covenants (covenant-lite, with fewer financial restrictions on the borrower), optimistic valuations, and lower average credit quality, especially in transactions originated by non-bank funds. In fact, several analysts point out that defaults on leveraged credit could rebound after years of prosperity: if we reach an environment of higher interest rates and lower liquidity, highly indebted companies and the funds that financed them will be put to the test.

Traditional banks´ exposure to the NBFI boom

One of the key questions is to what extent the risks of the non-banking system can spread to traditional banks. The main channel is banks´ credit exposure to non-bank financial intermediaries (NBFI). Large global banks provide financing to investment funds, market vehicles, and other shadow entities through multiple channels: direct bilateral loans, committed credit lines, repo transactions (securities-backed loans), derivative positions (providing leverage or hedging to funds), and even investments in instruments issued by NBFI. This network of relationships creates significant interdependencies. According to the IMF, U.S. and European banks have accumulated around USD 4.5 trillion in credit exposure to NBFI entities, equivalent on average to 9% of their loan portfolios.

Not all banks participate equally in this business: there is a marked concentration in systemic banks. In the U.S., approximately 50% of total banking assets belong to banks whose exposure to NBFI exceeds their own Tier 1 capital—an indication of risk concentration. The 10 largest U.S. banks alone account for some $710 billion of exposure to NBFI, of which, $300–400 billion is directly linked to private equity/credit funds. In total, U.S. banks are estimated to have $1.2 trillion of exposure to NBFI entities. European banks as a whole account for the remainder of the USD 4.5 trillion (approximately USD 3 trillion), although with a more heterogeneous and often less transparent distribution. Some large European banks have pockets of high exposure—for example, through loans to real estate or private equity funds domiciled in European financial centers—although on average European banks are somewhat less involved than their U.S. counterparts.

It is not surprising, then, that authorities warn of risks of two-way contagion: problems in NBFI can affect banks (via the aforementioned exposures), and conversely, banking tensions could reduce banks´ willingness to support the liquidity of non-banks. The IMF estimates that, under an adverse scenario in which funds withdraw 100% of their lines and collateral assets are devalued, the CET1 solvency ratios of a significant group of banks (in the case of Europe, 30% of the banking sector) could fall by more than 1 additional percentage point. This could significantly exacerbate an episode of systemic stress.

European perspective: Size, risks, and links to banking

Europe is experiencing a remarkable expansion of its non-bank financial system, although it started from a lower penetration than the United States. According to the ESRB (European Systemic Risk Board) Non-bank Financial Intermediation Risk Monitor 2025, the aggregate assets of the European NBFI sector reached €50.7 trillion at the end of 2024. This figure represents approximately 42% of the assets of the European financial system (a calculation that usually includes investment funds and other non-bank financial intermediaries, excluding banks; if insurers and pension funds are included, the proportion would be closer to 60%). In any case, European shadow banking already rivals traditional banking in size in many markets.

The NBFI sector in Europe encompasses a variety of entities: investment funds (including harmonized UCITS funds and alternative hedge funds), venture capital and private equity funds, structured finance vehicles, insurers, pension funds, and other non-bank financial institutions (OFIs). Over the last decade, many of these segments have grown, driven by the integration of capital markets in the EU and the adaptation to stricter banking regulatory frameworks after 2008. In fact, part of the growth of NBFI reflects a transfer of activity from banks to markets: for example, the weight of non-bank financing in euro area corporate debt has increased steadily (in 2024, around 30% of credit to non-financial companies in the euro area comes from market funds, compared to 20% in 2010). This increased financial disintermediation has benefits (it diversifies sources of financing), but it also introduces new vulnerabilities.

There are some key vulnerabilities in Europe. The ESRB, the IMF, and the ECB all agree on four areas of structural risk in the European NBFI sector:

- High leverage, which is often difficult to measure. This is particularly noticeable in certain alternative funds (global hedge funds based in the EU, some UCITS fixed income funds with absolute return strategies that allow them to leverage heavily, etc.). For example, the ESRB found that a subset of UCITS funds use techniques that raise their gross leverage even above that of many hedge funds. This leverage amplifies potential losses and can be hidden off-balance sheet (derivatives, synthetic positions), making it difficult to track.

- Maturity transformation and liquidity risk. Many open-end funds offer daily liquidity to investors but invest in illiquid assets (private credit, real estate, emerging market debt, etc.). This creates a liquidity mismatch: in the event of massive outflows (redemptions), managers could be forced to sell illiquid assets at a discount, amplifying the price decline. Recent episodes—such as the sales of real estate funds in the United Kingdom in 2016 or the global dash for cash in March 2020—highlighted this vulnerability: funds with illiquid assets suffered heavy redemptions and had to activate liquidity management tools (suspensions, gates, swing pricing) to avoid collapse.

The ESRB warns that liquidity and maturity mismatches remain a critical risk that could trigger systemic stress similar to that seen in 2007–2008, when supposedly liquid structures (ABCP vehicles, SIVs) froze.

- Financial interconnectedness and dependence on banks. The financial ecosystem is highly interrelated: European NBFI maintains strong links with banks and with each other, via cross-shareholdings, loans, repos, derivatives, and liquidity lines. In particular, many funds rely on wholesale bank funding (e.g., contingent credit lines from banks to manage redemption peaks, or repo loans obtained from banks using assets in their portfolios as collateral). This dependence creates a direct channel of contagion: if a fund gets into trouble and needs liquidity, it will draw down its bank lines and/or sell assets, which may affect its banking counterparties; conversely, if a bank limits lines or experiences stress, funds may find themselves without backup liquidity. In addition, there are conglomerates where a banking group owns asset managers that may require support in the event of problems (the so-called step-in risk of the bank towards its non-banking subsidiary). All of this means that idiosyncratic shocks can be transmitted through the financial-banking network.

- Concentration of risks in a few entities or jurisdictions. Although the NBFI sector is diverse, certain exposures are highly concentrated. For example, the ESRB notes that a large fraction of European fund investment is concentrated in U.S. assets (especially technology stocks), which could amplify a sharp adjustment in that segment. Similarly, in the context of real estate funds in the EU, a handful of funds account for most of the sector´s bank debt (1% of real estate funds account for >40% of bank debt), and a few large banks are the main lenders. This concentration means that problems in a large fund or a bank with excessive exposures could trigger a cascade effect. There is also geographical concentration: certain countries (Luxembourg, Ireland, the Netherlands) are home to a huge portion of the European NBFI network, sometimes for tax or regulatory reasons, which can transfer risks across borders.

Taken together, these vulnerabilities could amplify cyclical risks in Europe. The ESRB warns that, given the current macrofinancial conditions (high inflation, interest rate hikes, geopolitical volatility), a scenario of significant asset losses—for example, defaults on low-quality corporate credit or declines in commercial real estate—could put pressure on indebted or liquidity-fragile NBFI, triggering forced sales and second-round effects throughout the system. For this reason, European authorities emphasize the need to close data gaps (regulations currently lack full visibility of leverage in certain funds) and implement pending reforms in areas such as money market funds (already reviewed after the tensions of 2020) and open-ended investment funds (where stricter liquidity rules are being discussed).

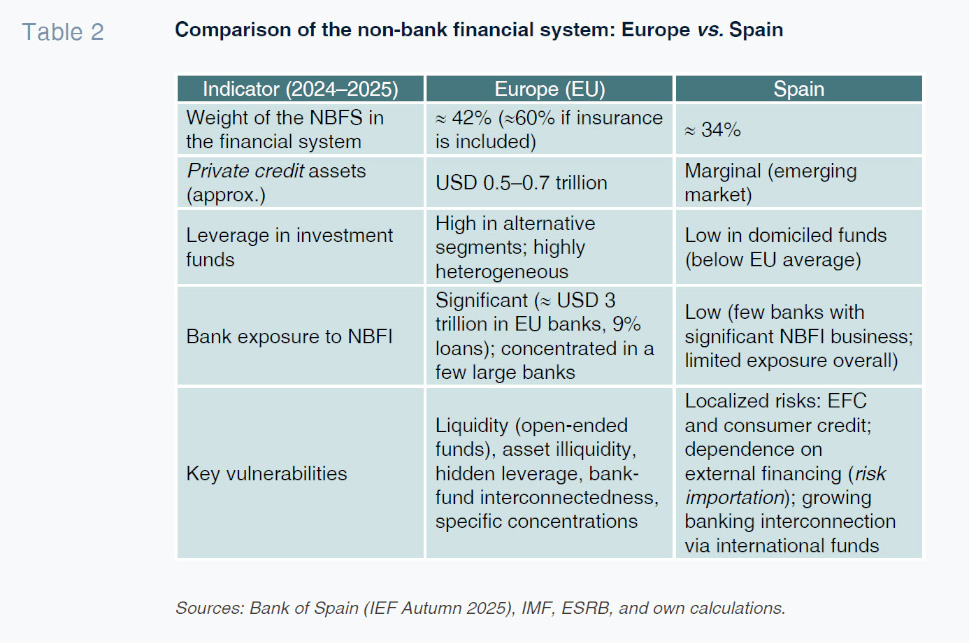

The Spanish case: lower relative weight, but non-negligible risks

Spain has a unique profile compared to the rest of Europe: its financial system continues to be dominated by traditional banking. According to estimates by the Bank of Spain (Financial Stability Report, Autumn 2025), the non-bank financial system (NBFS) in Spain represents around 34% of total national financial assets, compared to ~42% (funds+OFIs) – or up to 60% including insurers – in Europe. In other words, approximately one-third of the Spanish system is "shadow banking," a proportion that has grown slightly (it was 31% in 2015) but remains significantly below the European average. Total assets managed by investment funds have increased by 79.9% in Spain and 92.7% in the euro area since 2015. Table 2 compares some key indicators between Europe and Spain.

The table shows that Spain has a smaller and, in principle, less complex shadow sector than Europe. However, this should not be interpreted as meaning that Spain is isolated from global risks. In more detail, the Spanish system stands out for:

- Predominance of traditional institutions and limited activity by domestic alternative funds. The Spanish NBFS is mainly composed of traditional domestic investment funds, some credit companies (CFIs) specializing in consumer credit, and international funds operating in the country. Unlike markets such as Luxembourg or Dublin, Spain is not a hub for hedge funds or large private equity vehicles; domestic private credit funds are scarce and small in size (domestic direct lending is very limited). In fact, the private credit that reaches Spanish companies usually comes from foreign funds (e.g., British or American funds financing corporate transactions in Spain) rather than from local managers. This implies an "import" of risk: developments in the London or New York private equity/credit markets can be transmitted to Spain via the portfolios that these funds hold in Spanish companies.

- Low leverage and conservative profile of Spanish funds. The Bank of Spain highlights that investment funds domiciled in Spain maintain very low levels of leverage, below the euro area average (e.g., 102.8% for Spanish hedge funds, compared to 156.2% for those in the euro area). Due to regulation and practice, Spanish funds—especially those aimed at retail investors—use debt marginally and tend to have high positions in liquid assets (5.6% for domiciled equity funds compared to 2.2% in the euro area). This reduces their immediate vulnerability to redemptions (fewer forced sales). Likewise, these funds´ exposure to illiquid or high-risk assets is relatively low compared to other countries (most invest in high-quality public/private fixed income, liquid equities, etc.). This prudent nature of the Spanish fund sector is a structural strength. However, it does not guarantee immunity in the event of external shocks: for example, Spanish fixed income funds suffered significant outflows during the March 2020 turmoil in global markets, although they managed to handle them without problems due to their liquidity.

- Localized vulnerabilities: CFIs and consumer credit. One segment to watch is credit institutions (CFIs)—non-bank entities that grant consumer credit, credit cards, leasing, etc. CFIs in Spain have recently experienced a rise in delinquency: the non-performing loan ratio in their consumer credit portfolio rose to 3.7% in June 2025, marking four consecutive quarters of increases. Although this ratio remains below the equivalent delinquency rate in banks (4.1% in consumer credit), it indicates a deterioration after years of improvement. In addition, CFIs have seen their market share in consumer loans decline compared to banks, possibly due to greater selectivity in the face of risk. Spanish household consumer debt is moderate, but an economic downturn could put pressure on these specialized intermediaries.

- Dependence on international markets and foreign funds. As mentioned, much of the non-bank financing for Spanish companies comes from international funds. This means that certain risks can "seep in" from outside: an Anglo-Saxon fund with global liquidity problems could decide to liquidate assets in Spain (e.g., sell Spanish bonds or not renew loans to local SMEs) to cover needs in its main market. Likewise, wholesale financing of international funds by banks in Spain has been increasing slightly—for example, banks established in Spain participating in syndicated loans to infrastructure funds or providing subscription facilities to locally operating managers. Although this activity is limited at the moment, it indicates a growing interconnection. The Bank of Spain characterizes the interrelationship between banks and funds in Spain as "limited but growing," with the banking sector´s interconnections with the NBFS being greater on the asset side than on the liability side. While financing granted to SFNB intermediaries accounts for 7.9% of the total assets of the main Spanish banks, financing received remains at 7% of assets.

Conclusions

The rise of shadow banking—particularly private credit and leveraged credit outside the traditional banking perimeter—is one of the emerging sources of global systemic risk. Although it is more pronounced in the United States, Europe is also involved, and Spain is no stranger to this dynamic. The comparison with 2008 is not empty alarmism: we find parallels such as rapid growth in leverage outside banking regulation, opaque and illiquid structures sold as daily liquidity, and growing dependence on rating agencies (credit and ESG) that could underestimate the risk of complex assets. In addition, the growing role of NBFI in the financial system also poses challenges for central banks´ operational frameworks, which are traditionally bank-oriented, potentially leading to reduced effectiveness of traditional monetary policies in the event of liquidity strains or episodes of financial stress. These elements warrant extreme attention from the authorities.

The analysis gives rise to several policy proposals to strengthen the resilience of the financial system to these risks:

- Improve metrics and monitoring of leverage and liquidity in NBFI. It is essential to expand and refine the collection of data on non-bank funds: debt levels, cross-exposures, portfolio liquidity, counterparty concentration, etc.

- Implement integrated banking-NBFI stress tests and macroprudential analysis of systemic risks. Stress tests must be adapted to the new interconnected reality. The ESRB and the ECB advocate exercises that simulate combined adverse scenarios, where not only the direct impact on individual banks or funds is calibrated, but also the feedback between them. For example, regulators in the United Kingdom and Australia have begun to integrate stress tests designed to better understand the interactions between banks and non-bank entities.

- Increase transparency and reporting requirements for private credit and alternative funds. One specific recommendation is to require private credit managers to report their portfolios and liabilities more frequently and in greater detail, perhaps by extending the AIFMD regulation or creating specific registers.

- Strengthen regulatory and supervisory coordination and reduce potential regulatory arbitrage. Many shadow banking players operate globally and will take advantage of any divergences between jurisdictions.

- Consider financial digitization and new channels of intermediation. Finally, we cannot ignore that the fintech revolution and innovation (including DeFi, cryptoassets, peer-to-peer platforms, etc.) are creating new forms of "shadow banking."

In conclusion, shadow banking plays a valuable role in diversifying the sources of financing for the economy—filling the gap left by traditional banking after the financial crisis, as some experts point out—but its collateral risks cannot be ignored. Financial stability requires a comprehensive view: understanding the complex financing chains that today connect banks, funds, and markets, and implementing proactive policies to make the system as a whole more transparent, resilient, and prepared. Only then will we prevent the next crisis from finding its origin in the poorly lit shadows of the financial system.

Pedro Cuadros-Solas. CUNEF University and Funcas

Francisco Rodríguez-Fernández. University of Granada and Funcas

Nuria Suárez. Autonomous University of Madrid and Funcas