The limitations of European rearmament

Europe has the economic scale and industrial capacity to build credible military capabilities. Yet, national procurement practices and fragmented industrial strategies continue to slow progress and leave critical capability gaps unaddressed.

Abstract: With a combined GDP of roughly €20 trillion and an industrial base comparable in scale to that of the United States, Europe has the economic capacity to sustain a strong defence posture. Defence spending is rising rapidly, particularly in Germany, Poland, and the Nordic countries, but investment is unequal across the Union and remains predominantly national, limiting its overall effectiveness. Despite higher budgets, critical capability gaps persist in areas such as air and missile defence, space-based assets, and cybersecurity. The preference for juste retour (fair return) arrangements and national champions has undermined collaborative projects, leading to production inefficiencies, delays, and weak incentives to scale proven systems, as illustrated by the slow ramp-up of platforms such as SAMP/T. Achieving NATO-level spending targets—potentially lifting European defence outlays toward €700 billion annually—will not translate into effective military power either, unless spending is redirected toward genuinely joint capabilities. Closing Europe’s most acute gaps will require prioritizing a small number of high-impact projects, reducing industrial fragmentation, and refocusing flagship initiatives such as Iris2 on defence-driven common assets rather than national interests.

Background

The European “Pillar” within NATO represents a large, even if somewhat sluggish economic mass. The combined GDP of the European NATO members amounts to about € 20 trillion, more than 2/3rds of that of the US. The NATO goal of 3.5% of GDP would result in € 700 billion in defence expenditure, about double the current level (of € 350 billion), and, at current exchange rates, not far from the present US total of around € 800 billion (equivalent to 950 billion USD).

There can be no doubt about the economic potential for a strong European defence inside or in support of the alliance.

Moreover, Europe also has the industrial capacity to produce its own weapons. In terms of the value of industrial production, the EU is at par with the US since industry represents a larger share of EU GDP.

The goal of 3.5% of GDP for defence remains distant as the average for the EU is still only slightly above 2%, but even the smaller increase that has materialized since the start of the full-scale invasion of Ukraine has already led to important shifts in relative spending.

Since 2021, defence spending at constant prices (to strip out the effect of the surge in inflation in 2022) has been essentially flat in the US (up only 20 billion in real USD terms) whereas that of EU Members has increased by 150 billion (including the UK and Norway would bring the increase to 170 billion). Most of the additional spending of NATO is thus happening in Europe.

We start with a rough estimate of the macroeconomic impact this increase might have, and how the spending increase has been distributed so far across Member States.

It then turns to the question of whether the fiscal rules under the Stability and Growth Pact might represent an obstacle to further increases.

This paper starts by analyzing Union support schemes for defence investment in various forms (SAFE, EDF, European or EU preference for military procurement, etc.).

This is followed by a critical examination of how joint projects work in practice and how preferences for national champions have slowed down progress in key high-tech areas.

Macroeconomic impact

Achieving the NATO goal of increasing military expenditure to 3.5% of GDP (+ 1.5% in infrastructure) would represent a significant demand boost even if one discounts some reclassification of existing expenditure.

With military spending now running at about 2% of GDP, even achieving the 3.5% of GDP target would represent an increase of 1.5 percentage points of GDP, or about €300 bn more than today. Not all European Member Countries are likely to achieve this goal any time soon. But for the ones that are on course (Germany and the Nordics) this increase will represent a significant boost to domestic demand as a large proportion of the increase is spent at home.

The available research suggests that each 1 percentage point of GDP in military spending increases demand by about 0.5–0.6 points of GDP. The increase still in the pipeline should thus provide a demand boost worth about 1% of GDP (somewhat more for those countries where the increase is largest, i.e. Germany). This is significant given a trend growth rate for the EU of around 1 to 1.5%.

The composition of military spending is changing as well. Up to 2022 procurement accounted for only a small share (typically 20-25%) of total military spending, with the largest part going to personnel (including pensions) and running costs. By contrast, a large part of the increase is now spent on procurement.

The latest EDA report shows that overall EU military expenditure has increased from close to €250 bn in 2022 to over € 350 billion in 2025 (estimated). Discounting for inflation, the increase is less impressive, but still important (from 1.5 to 2.1% of GDP in 2025).

Moreover, investment (equipment plus R&D and R&T) has doubled since 2022 and amounted to about € 100 billion in 2024, or about 30% of total defence spending. These figures also imply that one half of the increase in military spending went to equipment.

This should not be surprising given that past expenditure on equipment had been below NATO targets and European allies have transferred part of their stockpiles and (mostly older) equipment to Ukraine. Equipment is thus likely to dominate the ongoing surge in defence expenditure as in the short run it is easier to increase orders for new tanks, artillery or ammunition than to find thousands of new soldiers.

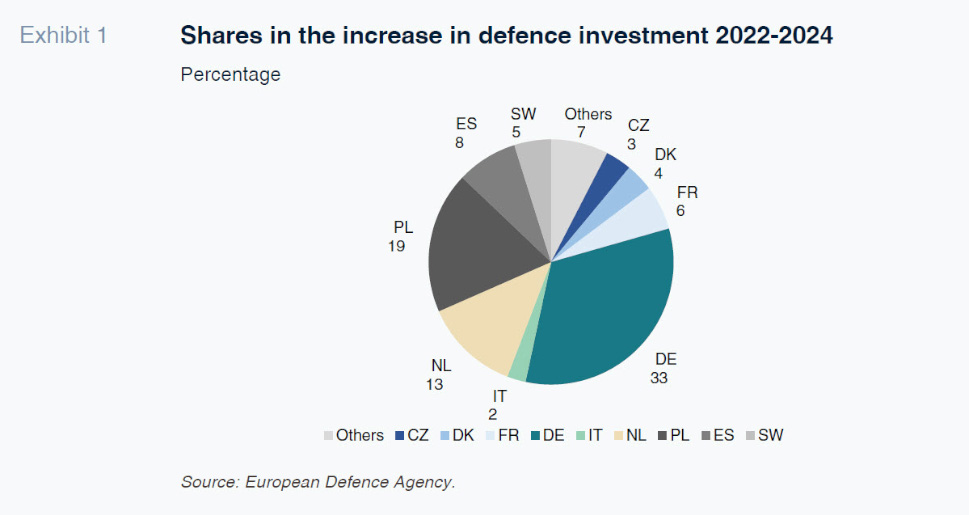

So far, the overall increase is not evenly distributed. According to data published by the European Defence Agency, 3 countries, Germany, the Netherlands and Poland, account together for about two thirds of the EU total increase in investment spending.

The pie chart below shows the percentage distribution of the overall increase in military investment of EU countries between 2022 and 2024. Apart from the German, Dutch and Polish contributions, the Scandinavians are also important relative to their weights in the EU economy.

The German share might rise further over the coming years given the high increase planned for the next few years. By contrast, the Southern Member States have so far increased their defence investment spending very little, with the partial exception of Spain.

Data on military expenditure is always subject to some margin of error given the different definitions adopted by different organisations.

Do the euro area fiscal rules represent a brake on defence spending?

Governments usually find it politically impossible to reduce other spending (or increase taxes) to finance the ramping up of defence expenditure. This implies that much of the increase will result in higher deficits. (Germany even changed its constitution in early 2025 to allow much of its defence spending to be financed outside its “debt brake”.)

Euro area Member States had just agreed in 2024 on a multi-year program to bring deficits down to more sustainable levels. Increasing deficits now because of higher defence spending would have been against the rules of the Stability and Growth Pact and might have led even to fines within the so-called excessive deficit procedure.

This is why the Commission has proposed exempting, at least temporarily, up to 1.5 percentage points of GDP of additional defence expenditure from the country-specific trajectories which Member States had only recently agreed with the Commission. Up to now, 16 Member States have asked for this “National Economic Clause” (NEC), representing about 45% of the GDP of the EU. The impact of this tweak to the fiscal rules is thus likely to be minor.

Existing Union financial support for defence investment

Another mechanism to support increased defence spending is the Security Action for Europe (SAFE) under which the EU will provide 150 billion € in loans to Member States to finance common procurement, i.e. contracts involving at least two EU Member States, or one EU Member State and Ukraine (EEA countries are also eligible). For critical assets SAFE can also finance procurements by individual Member States. Unfortunately, no information is available at present as to the extent to which this has been the case. The overall numbers suggest that a large share went for domestic procurement.

The first advantage of SAFE loans is the low interest rate on EU bonds. The importance of this factor has diminished for countries like Italy as risk premia have fallen. But the interest rates on EU loans are still higher than those paid by Germany and the Nordic countries. This is why these low debt countries have not requested any SAFE loans. Another advantage is the ability of the EU to provide financing at very long-term maturities that are often not available for smaller Member States and those outside the euro area.

The 150 billion € in loans foreseen for SAFE amount to less than 1 % of the GDP of the EU. But this sum looms relative to the still limited amounts spent on defence equipment. 150 billion € is more than two times larger than the annual expenditure on equipment and research of the Member States that have requested SAFE funds.

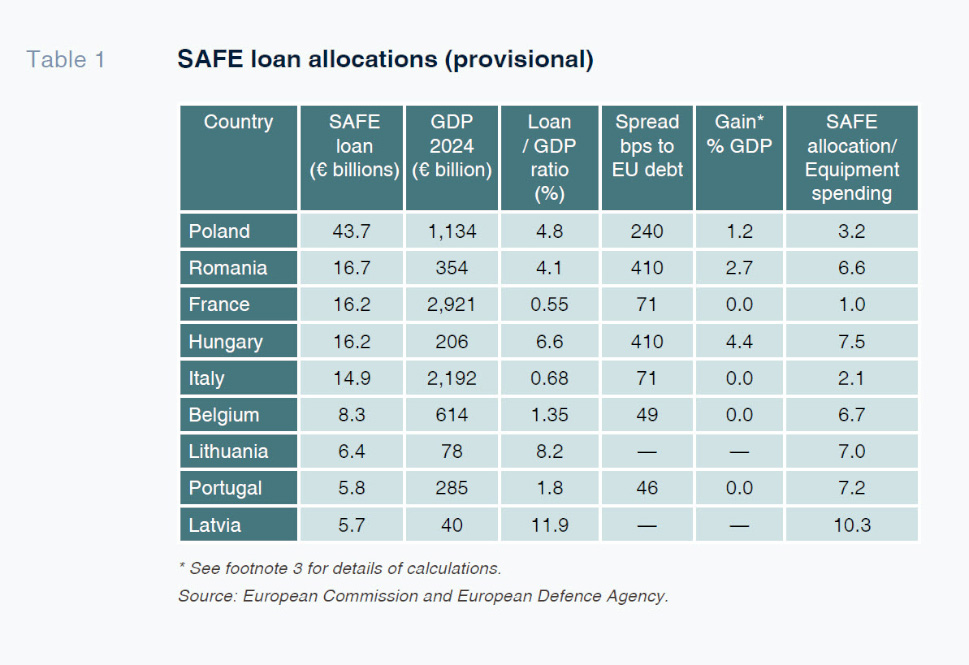

Demand for SAFE loans has been strong with 19 Member States requesting a total of 150 billion €.

[1] All Central and Eastern Member States (including Hungary) have requested SAFE loans plus France and Spain (the two large euro area countries with risk premia above those of the EU). 15 of these national plans reportedly involve cooperation with Ukraine. The long duration of SAFE loans might be the reason why especially smaller Member States have requested very large amounts, often multiples of their present annual expenditure on equipment.

For some smaller Member States like Latvia or Lithuania the SAFE loans represent a considerable share of their GDP (close to 12%) for Latvia. For large countries like Italy or France, SAFE loans are of secondary importance (amounts equivalent to less than 1% of GDP). A better measure of the economic benefit of SAFE loans is the amount of interest payments saved.

For the smaller Baltic countries with low debt ratios, the interest savings are of secondary importance since their governments can finance themselves at low rates. But the amounts requested (and now approved) represent multiples of their (2024) equipment spending.

But for other countries the difference between the interest on SAFE loans and national debt is larger, especially for Hungary, Romania (both of which pay about 4 percentage points more than the EU) and Poland (spread of 2.4%), resulting in higher interest rate savings.

If one uses these interest rates to calculate the interest savings [2] one finds that Hungary is by far the biggest beneficiary of the SAFE scheme, with a gain worth over 4% of GDP. [3] For Romania the interest savings amount to 2.7% of GDP and about 1.2% for Poland.

For all other countries, interest savings are negligible as a fraction of GDP, but SAFE still covers multiples of annual spending. Even for Italy the amount requested is at 15 billion € about twice as large as national equipment spending of around 7 billion.

For Hungary, the large implicit subsidy from SAFE might have been one of the considerations that led it not to veto in the December European Council the issuance of EU bonds for financial support for Ukraine.

The European Defence Fund

The European Defence Fund is mainly symbolic. It has an annual budget of about 1 billion €, until 2027, with one third allocated for collaborative research and two thirds for collaborative capability development projects that complement national contributions.

The problems with joint procurement: Development and production

At this stage, the key problem for Europe seems to be not so much whether enough money and financing will be available, but how it will be spent in a way that closes capability gaps and creates more cohesive European force structures. There are no fully satisfactory solutions to this problem.

Joint procurement is often mentioned as a key to unlock efficiency gains because of economies of scale and the sharing of development costs. However, the gains from joint procurement should not be overestimated.

For most land-based systems (tanks, infantry fighting vehicles, artillery, including mobile anti-aircraft) the development costs are not that large, and economies of scale are exhausted after production runs of a few hundred. In this area European producers seem to be competitive even if one could argue that there are still too many of them.

Development costs as a source of efficiency gains are much higher relative to the final price for high tech platforms, such as airplanes, space-based assets and ships. It is in these areas that joint procurement could potentially lead to large cost savings.

However, many multi-country development projects are plagued by delays and cost overruns. This is due to the incentives facing individual countries participating in these projects, both in the development and the production stage.

Development: Every single participating country (Ministry of Defence, often pushed by national champions) has an incentive to insist on adding a further capability of the joint aircraft or ship. The cost of additional features, and the resulting delays, are borne by everybody whereas the benefit of having the aircraft being able to perform a role that is important for one country remains at the national level. The national representatives that steer these projects naturally have a tendency to propose capabilities that correspond to their idiosyncratic needs and the technology of their national champions.

Production: The juste retour principles lead to inefficient production lines in which enterprises of all the participating countries must have their ‘fair’ share.

Two examples, one from the past and the other from the present illustrate these two fundamental handicaps of collaborative projects.

The A300 transporter project was years late and its development cost was at €30 billion over €10 billion above budget, shows the problems that can arise in the development phase when 7 participating nations have widely different requirements. With less than 200 planes built so far, the development costs amount alone to 150 million per plane, the same order of magnitude as the production costs, and the price at which these planes are sold. Given this experience, the split between France and Germany over the big European Fighter Project FCAS [4] might be a blessing in disguise. The competition between France and the smaller remaining consortium might produce two better aircraft at a lower cost than would have been likely under an unwieldy consortium with constant internal tensions.

The other example of the disadvantages of government to government projects concerns the SAMP/T, the land-based version of a family of theatre air defence systems based on the Aster missiles, a project that started in the early 1990s. [5] Here only 2 countries (France and Italy) were involved in the development phase (for the terrestrial versions) and that might have facilitated the relative success in developing an advanced system, which is reportedly similar in capabilities to the Patriot (except against medium range missiles). Developing and producing this system at scale should have been an absolute priority to close a key capability gap and would have been of critical importance for Ukraine. But no additional systems have been produced in 4 years of the war.

In this case the problem lies in the production phase. The system is produced by Eurosam, [6] a joint venture of MBDA France, MBDA Italy, and Thales Group. MBDA has stated that it takes 22 months to produce additional missiles and 3-4 years for new systems. One key reason is that many components must be sourced from specific suppliers in the two participating countries (France and Germany). With different parts allocated to different countries some components must be shipped multiple times across frontiers which creates additional delays given the national export control procedures that have to be satisfied each time.

The Member States behind Eurosam (mainly FR and IT for the land-based variant) have so far not opened up to a more flexible production structure for fear of losing industrial capacities. Despite the urgency of the needs of Ukraine and the geopolitical imperative to have a European alternative to the Patriots a contract to accelerate production was signed only early 2025. [7] The main reason for this delay was that it was necessary to reach agreement among three governments (from countries with frequent government changes) to amend the original agreement that led to the development of the system. Moreover, the two lead countries have little fiscal space and were neither able nor willing to provide the financing for the necessary investment in additional production capacity.

Unfortunately, SAFE does not contain any provisions on competitive tendering. Member States routinely invoke Article 346 TFEU to avoid putting military contracts to open tenders.

[8] As SAFE funds go to governments it thus cements the government-to-government structure of the European defence industry. While full competitive tendering might be difficult for complex systems, it should have been possible to make SAFE loans conditional on the establishment of more than one production line for critical components – preferably outside the recipient countries.

The industrial logic behind juste retour

The key problem bedevilling large joint projects is not only sovereignty in military matters, but also the prevailing industrial logic. Defence planners regard it as their duty to preserve certain industrial capacities (and intellectual property) at home. This tendency is of course stronger in the larger EU Member States (and the UK).

It is this industrial logic that is behind the insistence of the juste retour principle. The desire to keep certain industrial capabilities at home is strongest in high tech areas, especially electronics. This leads to a conundrum: the areas where Europe lags behind the US (e.g. avionics and missiles) are the areas where collaborative projects are most needed, but these are also the areas where countries are most reluctant to abandon the juste retour.

A new approach to joint projects: Separate development but European production

Experience suggests that smaller groups of countries, or even one country alone, work better for the development of new weapon systems. However, once the new technology has been developed and tested other countries should consider buying and production should then be competitive, at least at the suppliers and components level to put the industrial capacities of the entire EU to work. The country, or small consortium, that has developed the new product should of course be compensated for the development costs, and can retain the intellectual property, but when other countries buy the system, the value chain should not be limited to the one country or the group that has developed it.

At first sight it seems more ‘European’ to announce large joint projects. But, as the problems with the ambitious Future Combat Air System (FCAS) show, these large multi-country projects create rifts between countries that have different needs. Moreover, the resulting delays and cost-overruns create a public image of a Europe that does not work. It would thus be better to be less ambitious in developing ‘European’ systems and concentrate on getting countries to buy the best system, rather than from their national champions.

Conclusions

Europe has the economic wherewithal to strengthen rapidly its military and develop a competitive defence industry. But this requires more than ramping up spending at the national level. European producers are competitive in many mid-tech, mostly land based systems. The private sector is now investing heavily in these areas and expanding production at a rapid pace.

However, there remain multiple military capability gaps, mostly in high-tech areas like air and missile defence, cyber and space-based intelligence. Promising systems, capable of closing these gaps, exist in a number of cases, but they are not being scaled up sufficiently quickly because Member States are not willing to lose control over them, preferring that their national champions remain big fish in a small pond, rather than making them fit for a more competitive and much larger EU market.

The recent tensions over Greenland have once more illustrated the geopolitical cost of Europe not having key capabilities to defend itself and keep Ukraine in the field. But it remains to be seen whether this common imperative can overcome national interests.

Notes

The interest savings were calculated as 15 years of annual savings at the amount of SAFE loans allocated times the difference between the interest rate on EU bonds and national bonds.

The figures reported here are the initial allocations. It remains to be seen whether the Commission can subject SAFE payments to any conditionality.

Daniel Gros. IEP Bocconi