The growing challenges of renting for young Spaniards

Half of all Spaniards under 35 who have left the parental home now rent, with most living in large cities where demand is most concentrated. High prices and limited supply are pushing many to peripheral neighbourhoods and municipalities, while rent and associated costs consume a growing share of household budgets.

Abstract: In Spain, renting has become the default option for young adults leaving the parental home, with nearly 50% of under-35s now living in rental housing. Large urban areas host the largest share of young renters, accounting for six out of ten households. At the same time, rental costs, including service charges and utilities, have risen sharply, absorbing roughly 35% of household expenditure and leaving many young adults financially stretched. Non-European immigrant households have also grown to represent more than 40% of young renters over the past decade and are often exposed to the highest levels of financial strain. Additionally, rent overburdening varies significantly based on autonomous community, generally affecting densely populated, wealthy, or touristic regions such as Catalonia, the Basque Country and the Balearic Islands more than less dense and lower-demand regions. Taken together, close to 60% of young renters nationwide continue to devote more than 30% of their spending to housing, highlighting the depth and persistence of Spain’s rental affordability problem.

The rental option: At peak levels among young adults

High house prices have pushed many young people into renting. [1] This option has not improved their access to housing. Since 2019, average rents have increased by around 40% (Idealista, 2025a). [2] However, the purchasing power of young adults under the age of 35, measured by their total expenditure, has increased by 23.5%. This article analyses the financial burden facing the people in this age category when renting somewhere to live. To do that, we use the microdata from the Household Budget Survey for 2015 to 2024. From here on, we identify the household age as that of the main earner.

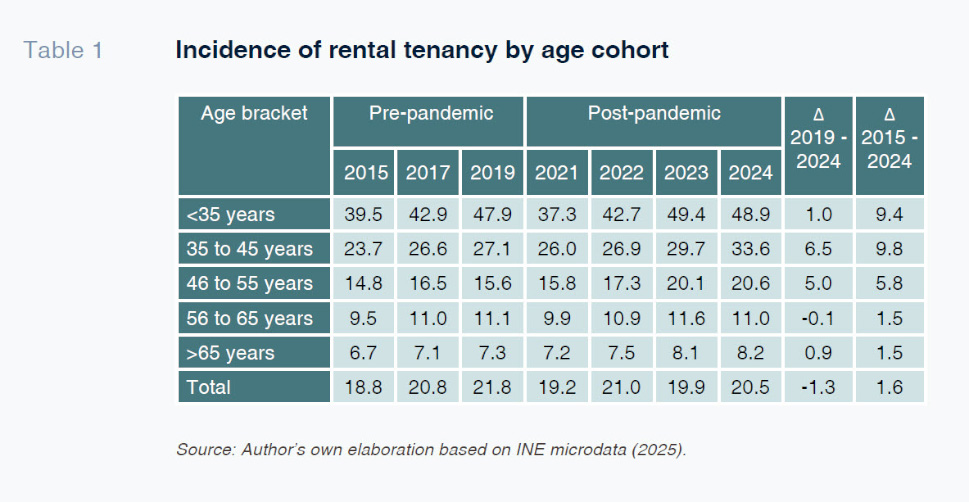

As our starting point, Table 1 shows the trend in the incidence of rental tenancy for each age group. In 2023 - 2024, the percentage of people under the age of 35 living in rentals was close to 50%. That percentage is much higher than for any of the other age brackets. The age group with the next highest incidence of rental living is the 35 to 45 category, where that percentage was 33.6% in 2024. The percentages fall off swiftly the higher the age bracket, falling to 8.2% among those over the age of 65. Looking back over time, the figures for the last decade yield several conclusions for the under-35s. The pandemic abruptly interrupted the growth in the share of rental tenancy, which later resumed. The figure observed for 2024 is actually higher than that of 2019 (48.9%

vs. 47.9%). The figures for 2023 — 2024 point to stabilisation in rentals among the youngest age group, having solidified as the main route for those moving out of the parental home. In 2024, home ownership accounted for 39.8% and free or semi-free tenancy represented 11.3%.

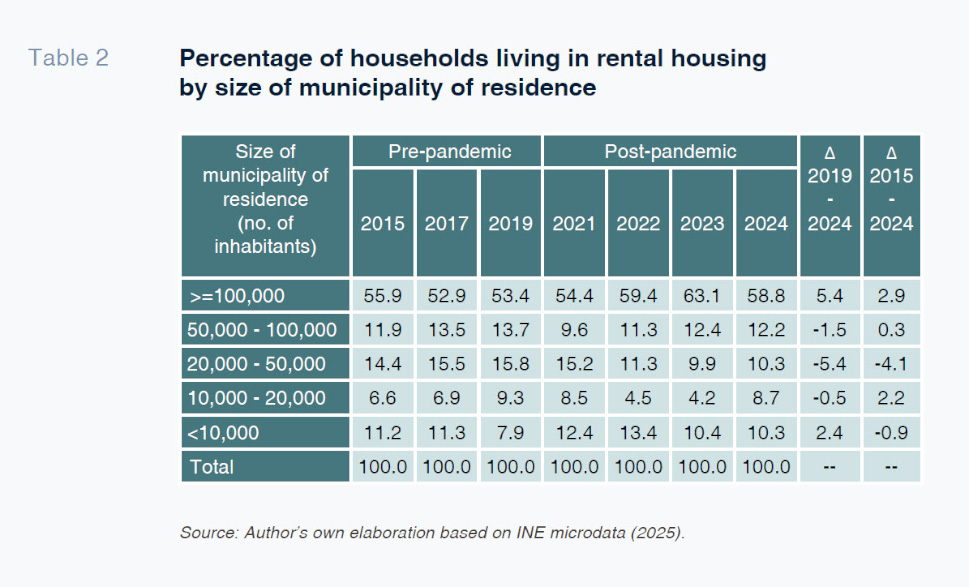

Youth rental is a markedly urban phenomenon, concentrated in large municipalities, especially provincial capitals. In 2024, around six of every 10 young households resided in municipalities with over 100,000 inhabitants, reflecting better job prospects, with roughly half living in provincial capitals.

[3] Since the pandemic, the combined effect of high prices and insufficient supply has been pushing young people out to medium-to-large bordering municipalities (50,000 to 100,000 inhabitants). This shift is allowing them to find less expensive housing without renouncing better job opportunities. However, this alternative is driving prices higher in the municipalities surrounding the largest cities, including Madrid, Barcelona, Valencia and Seville (Marrero, 2025). Displacement to the peripheries of large urban areas is a common phenomenon across the OECD. These large cities are home to as much as 50% of the OECD’s population and have generated 60% of all jobs in the past 15 years (OECD, 2016). To reduce the shortfall of supply for the under-35s, in 2023, Spain’s Right to Housing Act introduced personal income tax relief on up to 70% of rental income for owners who rent homes to people in this age range in the residential markets classified as ‘tight’. As far as we are aware, there is no specific evidence as to how this measure has worked out but the impact is thought to have been small.

[4] The reason is that supply is driven by structural factors which have not been affected by targeted measures. One of the most important factors is the lack of legal certainty for individual landlords in the event of payment default (OCU, 2023).

Immigrant households close to leading demand for rental housing among youths

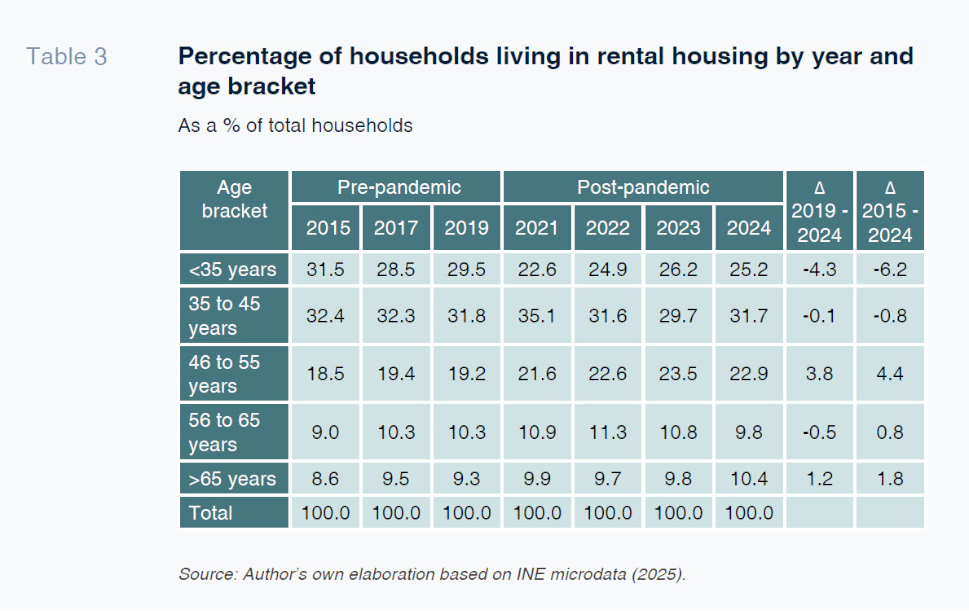

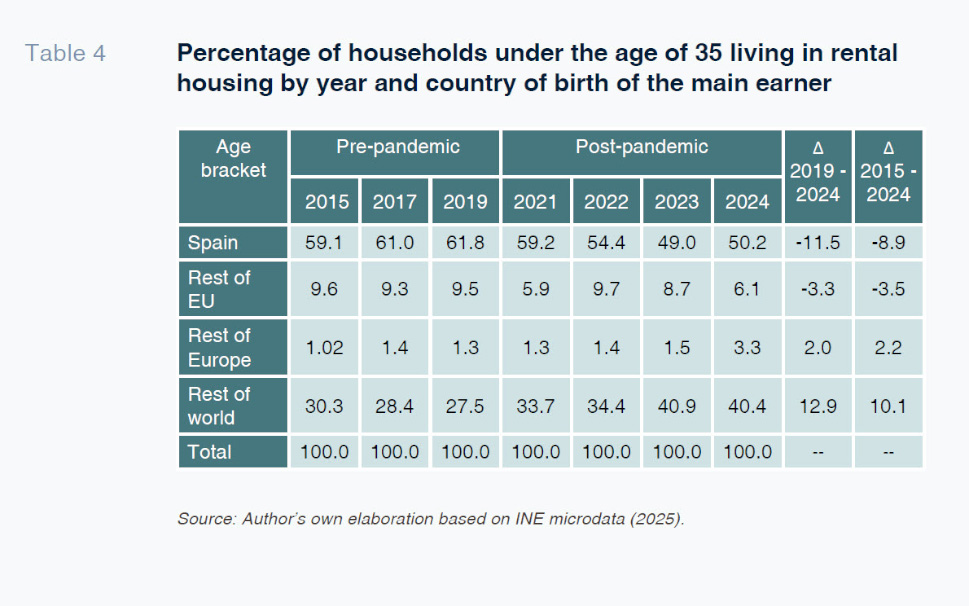

Over the past decade, in terms of households that rent their homes, the under-35s have fallen as a percentage of total households, from 31.5% in 2015 to 25.2% in 2024 (Table 3). Among young households (Table 4), the largest group corresponds to those whose main earner was born in Spain, despite seeing its share fall by nearly 10 points since 2015 (from 59.1% to 50.2%). The share of young households whose main earner was born in the rest of the world (mainly in Latin America and Africa) has increased from 30.3% to 40.4%. Lastly, the group of households whose reference person was born in other EU countries has held steady at around 10%. AIReF (2025) estimates an average annual inflow of immigrants of 288,000 people out to 2050. These demographic changes will reconfigure the share of young households who rent by place of birth. [5] It is foreseeable that over the medium-term horizon the percentage of young non-European immigrant households renting their homes will surpass the percentage of Spanish-born households

in the same situation.

The rental cost overburden has stabilised (for now)

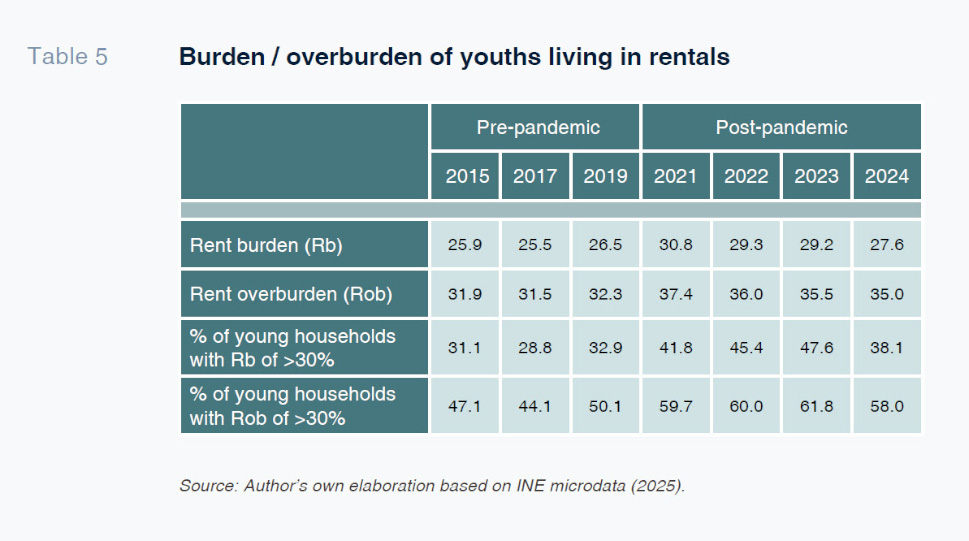

We use two complementary measures to calibrate the percentage amounts households devote to renting their homes. The first is the rental burden (Rb), computed as expenditure on rent over total household expenditure. In addition, as proposed in the Housing Act of 2023, we calculate the cost overburden (Rob) which factors in, in addition to rent, the cost of service charges, water and electricity.

Since the pandemic, around one-third of total household spending (Rb) goes to rent.

[6] The cost overburden (Rob) in the post-pandemic era has averaged 36%, pressured by higher energy and food prices in the wake of the invasion of Ukraine and the ensuing energy crisis. The comparison between the years before and after the pandemic reveals a clear deterioration in the cost burdens/overburdens faced by young households who rent. On average, both metrics have increased by between three and four points. This situation could begin to ease in 2026 if price growth stabilises. Indeed, the December report put out by Fotocasa (2025) maintains that the rental market could be close to reaching peak growth, following three consecutive years of record figures.

In 2024, nearly four out of every ten young households’ rent cost burdens exceeded 30%, so crossing the affordability red line (Table 5). The issue is even more acute considering the cost overburden, a measure by which nearly six out every ten youths cross the 30% affordability threshold. These results evidence the financial vulnerability and crisis facing young home renters. This issue has gotten worse in the last decade. In 2015, around five out of 10 households presented an overburden metric of over 30%. By 2024, that percentage had climbed to close to six out of 10.

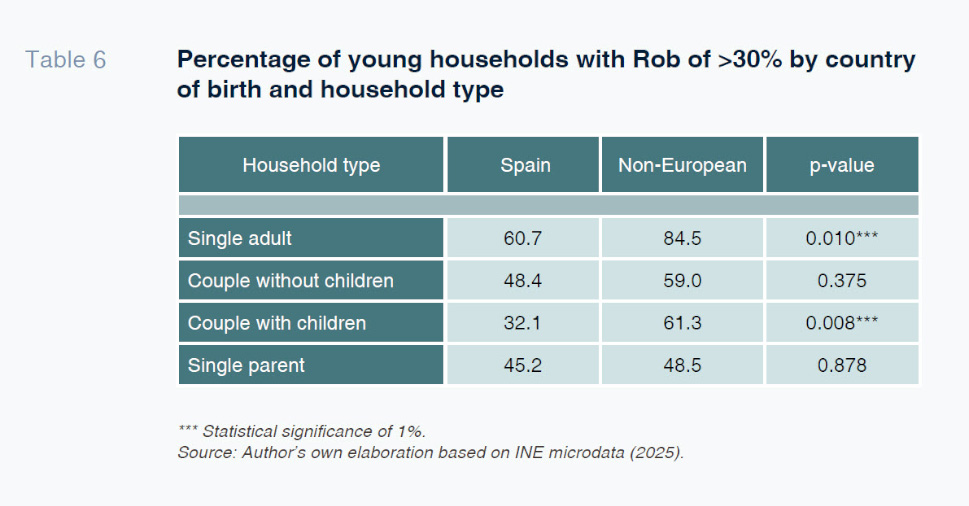

The affordability crisis is most intense among immigrant households, regardless of household type (Table 6). However, the differences are only statistically significant for young people living alone and couples with children. As Table 6 shows, over 84% of young immigrants living alone face an overburden level of over 30%, compared to 60.7% for single householders born in Spain. In the case of couples with children, the percentages are 61.3%

versus 32.1%, respectively. The rising overburden makes it harder for young renters to make ends meet while implying a high barrier for those looking to leave the parental home.

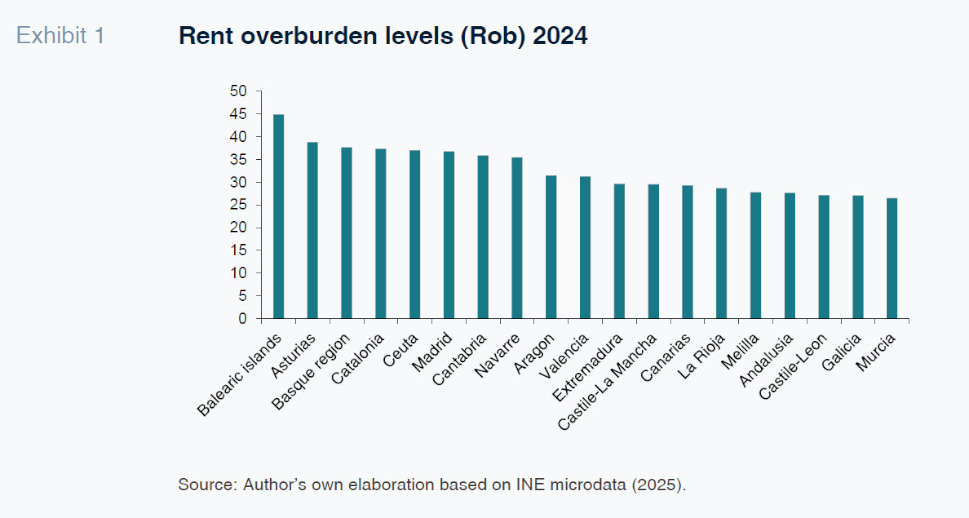

Significant regional differences in the overburden

The cost overburden level, Rob, ranges from a high of 47.6% in the Balearic Islands to a low of 25.9% in Galicia (Exhibit 1). In ten Spanish autonomous regions or cities, the overburden metric is above 30%. They are: the Balearic Islands, Asturias, Catalonia, Basque region, Ceuta, Madrid, Cantabria, Navarre, Extremadura, Valencia, Castile-La Mancha and Aragon. As allowed under Law 12/2003 on the right to housing, Catalonia, the Basque region and Navarre have declared some municipalities within their territories as ‘tight’ residential market regions. [7] The price limits imposed in those regions as a result do not appear to have improved the average cost overburden levels faced by young renters. Indeed, in Catalonia, these measures have only had the effect of reducing the rents charged for the most expensive housing (Montalvo et al., 2023). At the opposite end of the overburden spectrum lie Castile-Leon, Galicia and Murcia, with metrics of under 28%.

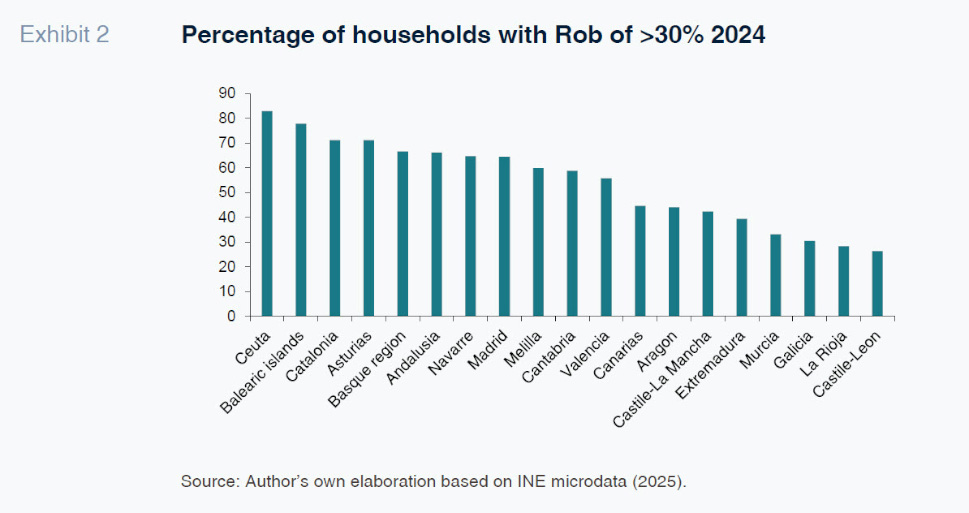

The autonomous cities / regions with the highest percentages of overburdened households are Ceuta (83%), the Balearic Islands (78%), Catalonia (72%), Asturias (71%), the Basque Country (67%), Andalusia (66%), Navarre (65%), and Madrid (64%). At the other end of the spectrum are Murcia (33%), Galicia (30%), La Rioja (28%), and Castile and León (26%). Exhibit 2 shows that a higher average overburden percentage predisposes a region to a higher percentage of households with overburdens of more than 30%. By the same token, the regions with lower average readings likewise present smaller shares of households with overburden levels of over 30%. The regional differences in burden and overburden levels indicate that the cost-of-renting crisis cannot be tackled with one-size-fits-all solutions.

Notes

In Spain, the average age of young people leaving the parental home is very close to 30.

In addition, supply has contracted sharply. In the largest cities, such as Madrid and Barcelona, the stock of permanent rental housing has shrunk by 41% (Idealista, 2025b).

Note that 13 of Spain’s 50 provincial capitals have fewer than 100,000 inhabitants, a threshold also not reached by the two autonomous cities, Ceuta and Melilla. On the other hand, there are municipalities, concentrated particularly in Madrid and Barcelona, with considerably more than 100,000 inhabitants.

Based on this same approach, the Spanish government is planning to launch a deduction from personal income tax of 100% for rental income generated by landlords from leases renewed without putting up the rent.

The gradual ageing of the Spanish population has reduced the population aged between 20 and 35 born in Spain by 870,800 people. In contrast, the immigrant population in that same age bracket has increased by 875,400 thousand.

Total household consumption expenditure includes the full value of goods and services consumed, excluding imputed rent.

This declaration, which the regions themselves have the discretion to make or not make, requires, in addition to an overburden metric of >30%, an increase in rents of at least 3 percentage points more than cumulative CPI in the region in question over the previous five years.

References

Desiderio Romero-Jordán. Rey Juan Carlos University and Funcas