Reforming Spain’s regional financing regime

The Ministry of Finance’s 2026 proposal seeks to overhaul the common financing regime, reduce disparities, and expand regional resources. But its fiscal cost and asymmetric effects on regional revenues complicate both budget sustainability and political viability.

Abstract: [1] Spain’s latest proposal for reforming the regional financing system marks a shift away from more disruptive, bilateral models towards a more standardized federal framework. The reform aims to meet a range of regional demands, including calls from some territories to increase resources for underfunded regions, to address disparities in per-capita funding, and to expand total revenues for the regional fiscal tier. The proposal also introduces several new funding mechanisms, which add complexity and raise questions about transparency, fiscal co-responsibility and the overall distribution of resources across territories. The reform would generate close to 21 billion euros in additional resources for the regions in 2027. However, the increase relative to a no-reform scenario would be significantly lower, as part of this amount reflects taxes already being collected and revenue growth that would occur under the current system. Even so, the fiscal impact would constrain the central government’s room for manoeuvre under increasing spending pressures for pensions, defence, and debt servicing. Simulations show that the distribution of additional funding benefits both territories that have argued they are under-financed and regions with stronger fiscal capacity. However, the combination of high fiscal cost, uneven distributional effects, and the need for an absolute majority in Congress makes the political path to reform and its ultimate viability uncertain.

Foreword

On 30 July 2024, two Catalan political parties, Partit dels Socialistes de Catalunya (PSC) and Esquerra Republicana de Catalunya (ERC) struck an agreement to support the appointment of the socialist party’s candidate, Salvador Illa, as the president of the regional government of Catalonia. That agreement implied a radical change in the so-called “common” regional financing regime. As argued by Lago Peñas (2024), the wording of that document placed Catalonia on par with the confederate-style models, such as those of the Basque region and Navarre, under which regional governments collect and manage most taxes themselves and transfer an agreed contribution to the central government in exchange for national services.

Although that agreement did not come into effect, it has served as the basis for the Ministry for Finance’s effort to formulate a proposal applicable to the common-regime governments as a whole. The proposal was presented by the Minister on 9 January 2026 (Ministry for Finance and Civil Service, 2026). The goal of this paper is to analyse its fundamental elements and possible effects and outcomes. To that end, the rest of the article is structured into three sections. The first section provides an overview of the most noteworthy aspects of the proposal; the second section analyses its impact on central and regional government funding; and the third addresses the political economy underlying the proposed reforms.

Key aspects of the proposal

First, the draft moves away from the disruptive and confederate approach derived from the agreement of 2024, instead proposing to reform the existing model. In contrast to tax coordination and asymmetric bilateralism, the proposal returns to the logic of a federal-style regional financing regime, in which tax revenues are shared between central and regional governments and redistributed through common equalisation mechanisms applied to all regions.

The second positive takeaway is that the proposal would substantially reduce dispersion in funding per adjusted inhabitant compared to the prevailing model.

[2] This would materialise in two ways: firstly, because the regions currently presenting below average funding (Valencia, Murcia, Castile-La Mancha and Andalusia) would receive significantly more; and secondly, because the regions furthest removed from the average (La Rioja, Cantabria and Extremadura) are among the four regions that would receive fewer additional funds in per-capita terms.

After that, things become less clear. Elimination of the so-called “convergence funds” and

ad-hoc adjustments constitutes progress in terms of simplicity and transparency. The same applies to the decision of bringing fund accrual and collection closer together in time, doing away with the distortions and perverse incentives triggered by the outgoing system of settlements two years after accrual.

[3] Unfortunately, new pieces have been tacked on to the model which do the opposite. The climate fund and SME VAT tranche are cases in point.

[4]

The first mechanism seeks to reinforce the financial resources of the regions affected the most by extreme events, but does so by injecting unconditional funding, resorting to an allocation rule based on an unsubstantiated measure of regional impact and in the absence of a comprehensive national readiness and response strategy. It would be more reasonable to base it on a thorough and complete prior needs assessment vis-a-vis foreseeable extreme events (floods, storms, fires, etc.) and more appropriately designed tools. Only at the end of such a process would it make sense to identify the need to transfer additional funds to the regional treasuries, funds which should be conditional and compensatory so as to guarantee additionality and be awarded in amounts aligned with the estimates so formulated.

As for the SME VAT tranche, here the advantages in terms of regional financing autonomy and shared responsibility are not clear. It appears to be a mechanism ultimately intended to guide the distribution of funds within the system: one single region would receive three-quarters of the funds allocated under the scope of this mechanism.

The proposal increases the shares of the main taxes collected by the regional treasuries and integrates or reorganises taxes that, in the current model, function as add-ons, outside of the main allocation system: taxes on wealth, bank deposits, gaming activities, and waste deposits. However, the SME VAT tranche complicates the system and does little to strengthen shared fiscal responsibility, which is similarly true of the increased share of VAT receipts. Moreover, surpassing the symbolic payout threshold whereby regional governments receive half of the revenues from personal income tax also raises questions, as the latter is a fundamental taxation tool for the central government.

Lastly, the Ministry of Finance intends to update the regulatory tax collection calculations, i.e., the theoretical amount of tax revenue that would be received by each region if they all applied the same tax rules and managed their collection in the same manner, which would improve the accuracy of the calculations used to determine the amounts of the equalization grants. Today, taxes such as inheritance and gift tax and stamp duty are outdated: tax regulations are obsolete and misaligned with economic reality (in both directions), and it is necessary to run the calculations for the newly integrated taxes.

The financial consequences of the proposal

According to the Ministry of Finance, in 2027 (the year the reforms are due to take effect), the model would yield the regional governments an additional nearly 21 billion euros (net) of funds, which is around 1.2% of the nominal Spanish GDP forecast that year. Never was so much additional financing on the table in a reform process. Without question, this volume of transfers would limit the central government’s room for manoeuvre at a time of growing pressure on spending, especially on pensions, defence, and debt servicing. The need to continue to reduce the structural deficit to prepare for a less benign economic and tax revenue scenario than Spain has been enjoying for the last three years requires analysing the impact against the backdrop of already tight medium term fiscal planning: AIReF is projecting that under the current European fiscal rules, Spain would breach both the annual and cumulative spending growth limits in 2027, triggering the need for additional cuts (Lago Peñas, 2025b).

Nevertheless, there are two nuances when it comes to putting the proposed increase in regional financing into context. The first is that some of the increase would come from the collection of taxes that are already being diverted to the regions, specifically approximately 3.2 billion euros, which reduces the figure above to under 18 billion euros. The second is that even in the absence of reforms, the system is already providing substantially increased funding. According to Ministerial figures, payments on account have been increasing at an average of 10.9 billion euros year-on-year for the last three years (2024–2026). In that sense, if the contrafactual scenario is how much more the regions would receive in 2027 relative to a no-reform scenario, the net difference narrows to around 10 billion euros, even assuming that the growth in payments on account is likely to slow relative to the trailing 3-year average due to the slowdown in GDP growth.

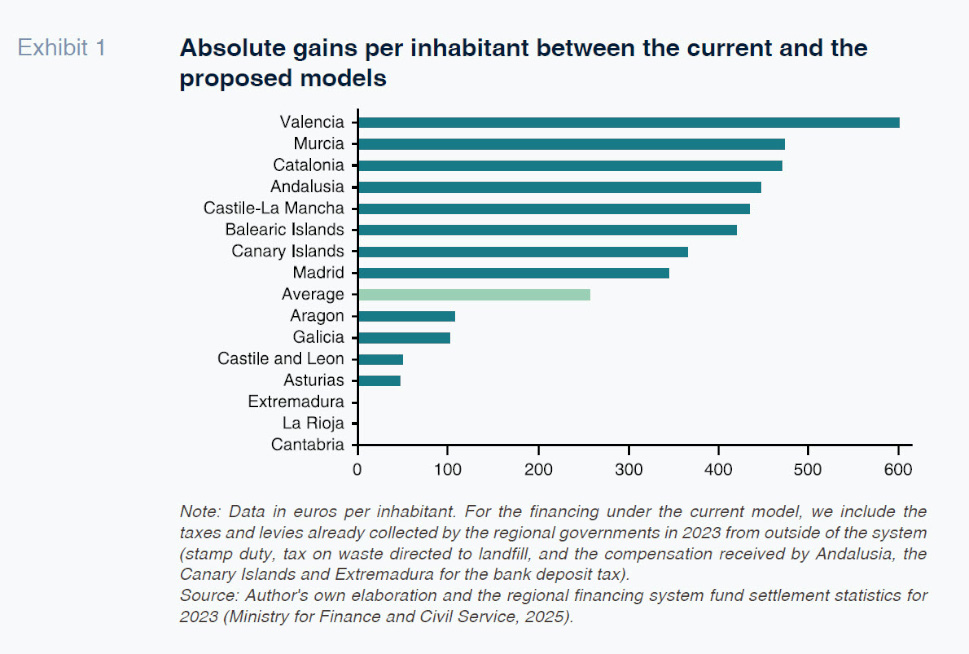

Turning our attention to how those additional funds are to be allocated among the regions, stark differences emerge. Exhibit 1 shows how no region loses funds in per-capita terms due to the application of the

status quo criterion. However, the gains are very different, running as high as 600 euros per inhabitant in Valencia. In other words, the proposed reforms imply a considerable shift in relative shares of financing for the majority of regions.

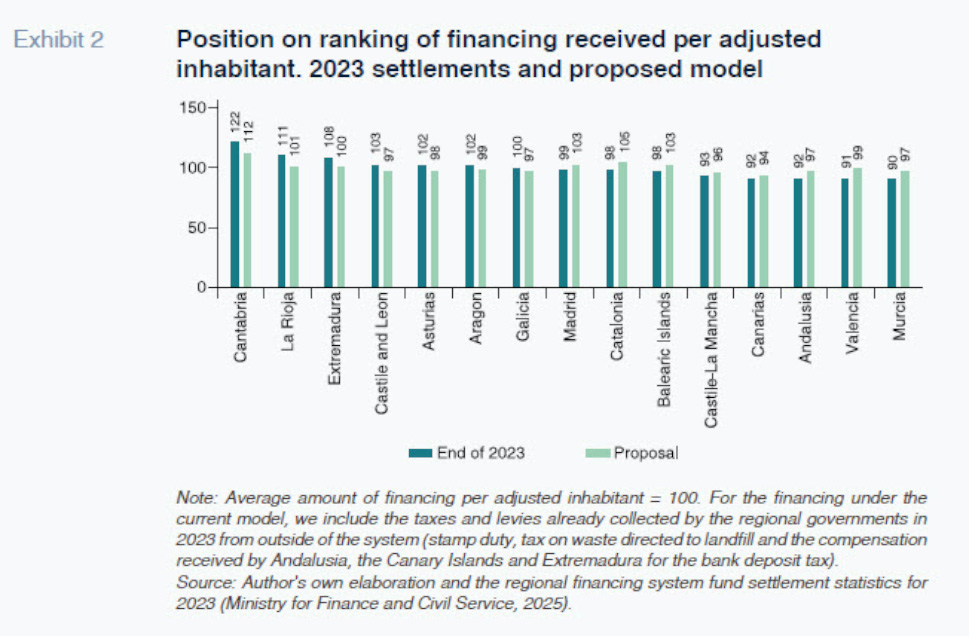

Exhibit 2 better illustrates the movements in ranking; here, the numbers are weighted by adjusted inhabitants. Two patterns emerge. The first is that the regions that were further from the average, represented by 100, in either direction, converge towards that average. That is true of Cantabria, La Rioja and Extremadura, at one end of the ranking, and Valencia, Murcia, Andalusia and Castile-La Mancha at the other end. The range narrows from 90-122 to 96-112, excluding the Canary Islands on account of the idiosyncrasies derived from its special tax regime. The second pattern is that the regions with bigger tax capacity, Catalonia, the Balearic Islands, and Madrid, are among those that stand to benefit the most, apart from the under-financed regions, and this effect is clearly stronger for the first one. The “no re-ranking principal” holds that interregional solidarity should not alter the regional ordering of wealth. That criterion is still not upheld for the most part in these reforms (it is for Catalonia) but they are a step in that direction. That outcome is helped by the loss of relative funding of other regions with below-average fiscal capacity such as Castile and Leon, Asturias and Galicia.

The political economy underlying the agreement

The political economy surrounding the Ministry of Finance’s proposals suggests it will be hard to push the reforms through for one key reason: although it is designed to avoid nominal losses, the gains are very asymmetric, and the agreement will therefore inevitably generate “political losers”. Opting for an essentially quantified and closed proposal facilitates its technical scrutiny but also activates immediate stock-taking: each region can calculate its gain and take a position framed by a zero-sum mentality, even if its aggregate improves.

The big winners are the regions that are currently at the bottom end of the ranking of financing per adjusted inhabitant, as well as Catalonia. The pressure exerted by Catalonia in favour of the “no re-ranking principal” means it would climb several spots on the ranking of financing per adjusted inhabitant. This thrust also benefits Madrid and the Balearic Islands, albeit to a lesser degree. Following equalisation, the regions with more fiscal capacity will retain a bigger portion of their initial advantage, reinforcing the correlation between fiscal power and retained funds. Insofar as a considerable number of regions are against application of the no-ranking principal, conflict looms around this vector.

Notes

The author would like to thank Xoaquín Fernández Leiceaga and María Cadaval Sampedro for their feedback and Alejandro Domínguez for his assistance researching this topic.

The way in which the Spanish model factors in interregional differences in public service costs and spending needs is the so-called adjusted inhabitant′s calculation: a measure of the population which adjusts the number of residents in each region by weighting it by variables such as the age of the population, dispersion, surface area and island status.

To the extent that the collection of the main taxes (VAT, personal income tax, excise duties) is carried out by the central administration and that the main blocks of transfers also depend on the evolution of tax revenues, the funds are advanced to the autonomous communities based on revenue forecasts. Once the actual collection is known, the differences are settled.

The SME VAT tranche is a voluntary mechanism by which a region can opt to receive a portion of the VAT generated by the SMEs located in that region, calculated as the difference between the share of VAT paid by those SMEs and the region′s share of final consumer spending.

References

Santiago Lago Peñas. University of Santiago de Compostela and Funcas