Inheritance and inequality: Spain’s widening wealth divide

Wealth inequality in Spain has intensified along both intergenerational and intragenerational lines, driven largely by housing market dynamics and uneven income trajectories since the financial crisis. Looking ahead, demographic shifts will increase the volume of wealth transferred across generations, but have the potential to amplify, rather than reduce, existing disparities.

Abstract: Wealth inequality in Spain has increased markedly since the early 2000s, with divergence both across age groups and within generations. Older households have consolidated their position through asset revaluation, while younger cohorts face lower homeownership rates and weaker income growth, limiting their capacity to accumulate wealth. Housing plays a central role in this process, amplifying disparities between owners and non-owners and reinforcing differences across generational cohorts. At the same time, intragenerational inequality has intensified, particularly among younger households, where wealth is increasingly concentrated at the top of the distribution. Intergenerational transfers are set to become more significant as population ageing progresses and cohort sizes shift, raising average inheritance per capita. However, these transfers are unevenly distributed and closely tied to existing wealth concentration. As a result, inheritance may reinforce rather than reduce intragenerational disparities.

Introduction

In recent decades, economic inequality has returned to the fore of academic and economic policy debate. Although this debate often focuses on income distribution, the evidence available suggests that the wealth inequality phenomenon has its own scale and dynamics, with more persistent implications for social mobility and equal opportunities. Specifically, wealth tends to become more concentrated than income and that concentration tends to become stickier with time due to wealth accumulation, asset revaluation and intergenerational transfer mechanisms (Anghel et al., 2018; Palomino et al., 2021).

Spain is a case of particular interest for two reasons. Firstly, household wealth in Spain is characterised by the significant weight accounted for by property, so that house prices are a key factor in wealth accumulation dynamics. Secondly, the period following the financial crisis was marked by income adjustments and conditions that made it harder for young people to get on the property ladder, curbing their ability to save and, by extension, accumulate wealth.

From a generational perspective, recent evidence points to a widening wealth gap between age brackets. The older generations are accounting for a growing share of total wealth, while the younger generations have seen their ability to build wealth impaired by greater difficulties in buying a house, income corrections in the wake of the financial crisis and growing reliance on rental tenancy. In parallel, within each generation, we are seeing an increase in wealth inequality, particularly among younger households, suggesting that the wealth gap is not only intergenerational but also intragenerational.

Beyond these wealth accumulation dynamics, intergenerational wealth transfer is emerging as a key factor for understanding where inequality may be headed. Population ageing and the demographic configuration of the age groups affected shape the volume of wealth available to pass on, as well as its distribution among recipient households. However, the impact of these transfers is not neutral from the distributive perspective and can, in certain circumstances, help exacerbate existing inequalities.

The aim of this paper is to comprehensively analyse the inter- and intra-generational wealth gap in Spain and the role played by the transfer of wealth among generations. Using microdata from the Survey of Household Finances, we examine the factors that have contributed to the widening of these gaps in recent decades and explore, looking forward, the demographic and distributive implications of the wealth transmission process currently underway.

Data and empirical approach

The empirical analysis contained in this paper is based on the microdata from the Survey of Household Finances (the Survey) compiled by the Bank of Spain. The Survey is the main source of information for studying Spanish household wealth as it provides detailed information about the composition of that wealth, household indebtedness, income and sociodemographic characteristics; moreover, the data are very conducive to comparisons over time.

The Survey is carried out every two years and follows a sample structure that is particularly suited to analysing wealth inequality due to the relative over-representation of the households in the upper wealth distribution brackets, which represent a small percentage of the total population. In addition, it features a longitudinal panel design whereby some of the households can be monitored over time, which is particularly useful for analysing the trend in wealth, and how wealth is accumulated and depleted, over the course of our lives.

Our approach combines two complementary strategies. Firstly, we conduct an analysis by the age of the household reference person, which allows us to examine the distribution of wealth among generations and compare generations’ stock of wealth over the years at equivalent stages of their life cycle. Secondly, we analyse the internal distribution of wealth within each age bracket using concentration indicators and comparisons by deciles in an attempt to capture the intragenerational dimension of the inequality phenomenon.

This analysis is complemented by hypothetical intergenerational wealth transfer simulations. Without intending to estimate structural causes, these exercises do facilitate transparent and quantitative assessment of the relative role of two factors: (i) the amount of wealth accumulated (including asset revaluation); and (ii) demographics (relative size of the benefactor and recipient cohorts) in the volume of wealth transferred per person.

The paper therefore follows a descriptive, analytical approach designed to characterise the economic and demographic mechanisms underlying the trend in wealth inequality in Spain and enable informed debate about its economic and social implications.

Intergenerational wealth gap: Wealth accumulation, property revaluation and generational divergence

The empirical evidence available for Spain reveals that intergenerational wealth inequality has intensified significantly since the start of the twenty-first century. Beyond the normal differences expected over the life cycle (by which households accumulate wealth as they age), the widening of the intergenerational gap also reflects structural dynamics that have favoured uneven wealth accumulation across cohorts.

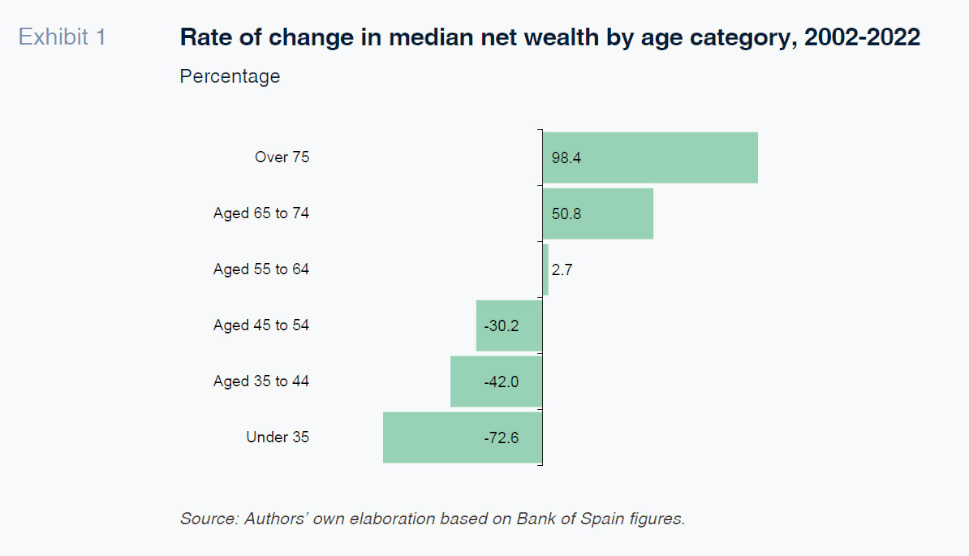

A first indicator of this divergence is the trend in net wealth concentration by age category. Since the beginning of the century, the households headed up by persons over the age of 65 have seen their share of total wealth increase consistently, while the younger age categories have lost share. This displacement cannot be explained solely by population ageing as it also reflects very different trends in the stock of wealth among different generations. In real terms, between 2002 and 2022, median net wealth fell for all households under the age of 54 but increased significantly for households over the age of 65.

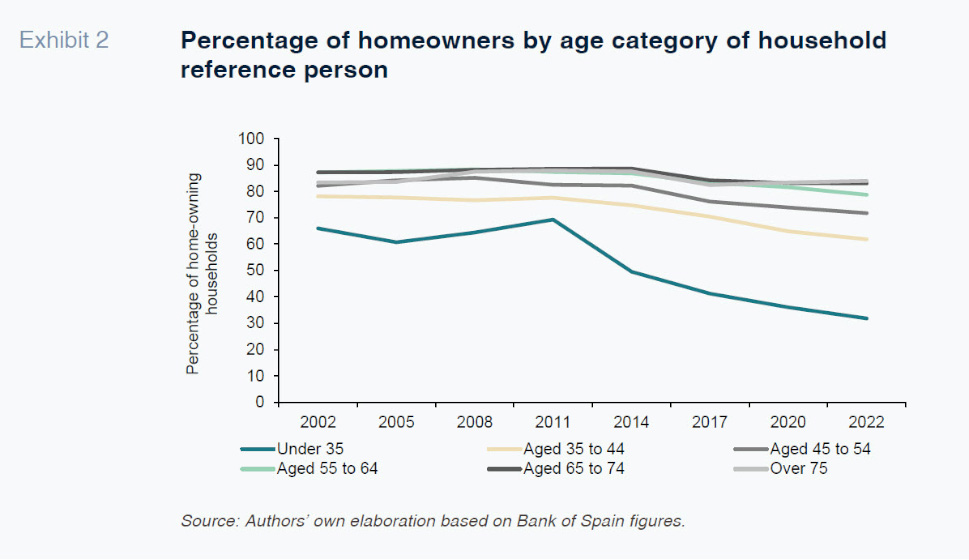

Housing plays a central role in this dynamic. In Spain, property constitutes a core component of household wealth, such that differences in tenure status and in the age that households get themselves on the property ladder have persistent effects on wealth accumulation. The older generations report systematically high primary home ownership rates and tend to also report a higher incidence of second homes and other real estate assets. In contrast, the younger generations have seen the percentage of homeowners fall sharply.

This divergence in property ownership has significantly amplified the intergenerational wealth gap. The house price growth recorded at different times since the turn of the century has handed the households that already owned property a disproportionate benefit, inflating their wealth, while those excluded from the home ownership market have been left out of this asset appreciation process. As a result, housing operates as both cause and effect in intergenerational wealth inequality: price growth makes it harder for young people to buy a house, while simultaneously enriching those who already own property.

On top of these asset dynamics, income comes into play. Although income inequality is narrower than wealth inequality, income patterns have also contributed to a wider generation gap. The older age categories are the only ones whose real median income is currently higher than was observed at the turn of the century, whereas younger households have seen their income deteriorate since the financial crisis, persistently impairing their ability to save. This combination of lower disposable income and less affordable housing has structurally impeded the younger generations’ ability to accumulate wealth.

The aggregate result is an intergenerational gap that is bigger than would be expected considering age factors only. A comparison across generations at the same juncture of their life cycle shows that today’s young households accumulate less wealth than the generations before them did at their same age. This unequal starting point is the scenario in which, as we analyse in the next sections, both intragenerational inequality and intergenerational wealth transfer come into play.

Intragenerational gap: inequality within generations and the impact of home ownership

Our analysis of the intergenerational wealth gap reveals considerable differences across the different age groups but only offers a partial vision of the wealth inequality dynamic. To fully understand its scope, we need to examine how wealth is distributed within each generation, in other words, to analyse the intragenerational wealth gap. The recent evidence for Spain indicates that this dimension of inequality is not only meaningful, it has intensified considerably in recent decades, especially among the younger generations.

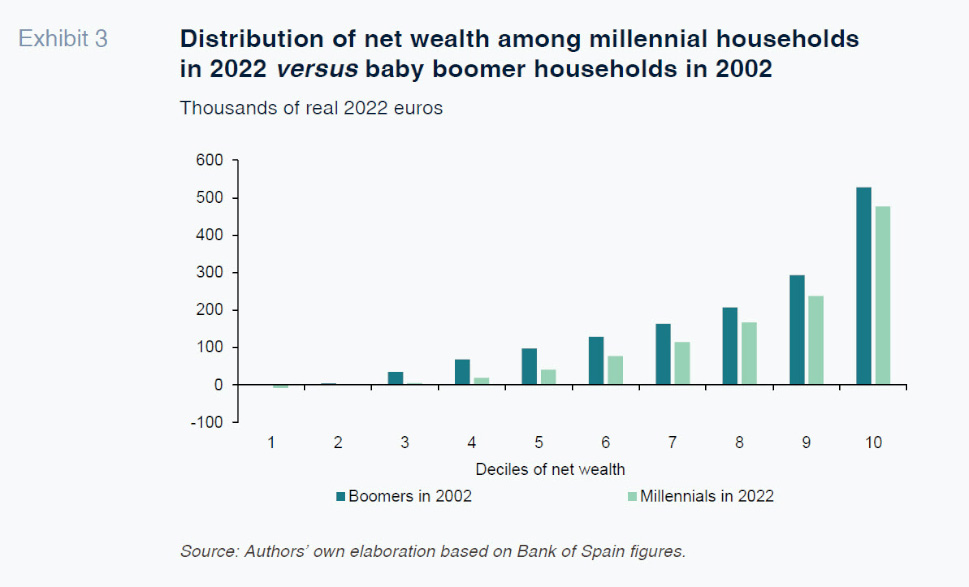

A first illustrative exercise consists of comparing the distribution of wealth for different generations at the same age. Analysing the net wealth of households headed up by people over the age of 45, we see that the millennials present clearly lower levels of wealth than reported by the baby boomers when they were the equivalent age at the start of the century. This difference is on display throughout the wealth distribution for this cohort and is not circumscribed to the lower wealth categories, suggesting widespread deterioration of the millennials’ wealth relative to the generations that went before them.

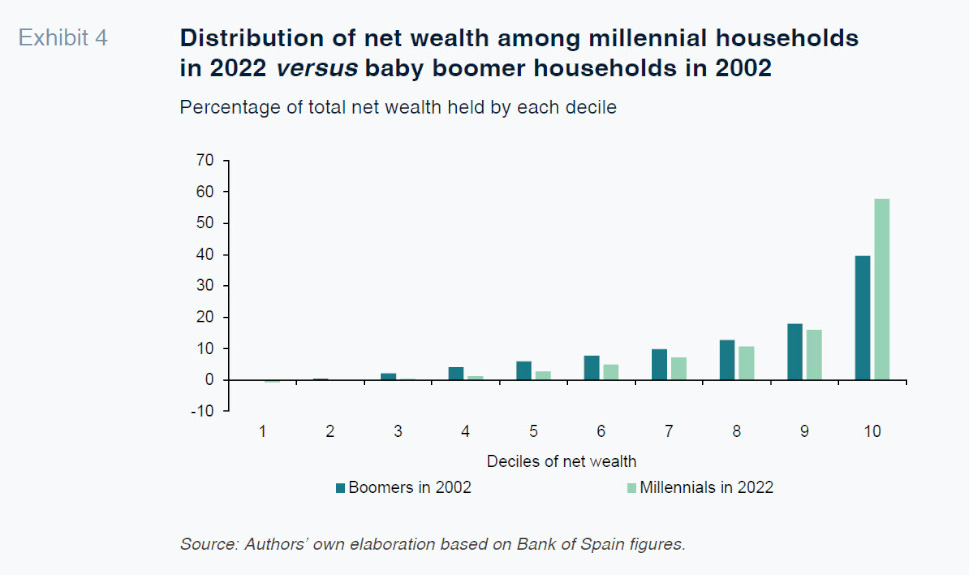

In addition to this comparison in absolute terms, it is insightful to analyse the internal wealth distribution within each cohort. The evidence reveals that wealth is more concentrated among the millennials in 2022 than it was among the baby boomers when they were at a similar stage of their life cycle (2002). Specifically, 58% of the millennials’ stock of net wealth is concentrated in the top decile of the distribution, whereas the bottom half combined accounts for less than 4% of the total wealth accumulated by their generation.

If we compare this intragenerational gap with that presented by boomer households in 2002, the distribution by decile was much more equitable. In that generation, the richest 10% of households held less than 40% of the net wealth of their generation, while the bottom half accounted for 12.2%.

Housing also plays a central role in the intragenerational inequality dynamic. Given the predominant weight of property or housing wealth, being a homeowner or not emerges as a key wealth differentiation factor. Young households that have managed to get on the property ladder, often with help from families or via inheritance, benefit in two ways: they become wealthier as asset prices increase and they are able to save more thanks to not being exposed to the high cost of renting.

In contrast, a growing percentage of young households is being forced into the home rental market. The sustained growth in rents in the main urban areas has increased the burden of renting for these age groups, reducing their ability to save and, by extension, undermining their ability to accumulate wealth. This mechanism generates a negative loop in terms of inequality: households who do not buy their homes get stuck in rents that limit their ability to build wealth, gradually widening the gap with respect to homeowners.

In this context, the growing share of the population born outside of Spain in the younger age categories takes on additional relevance as these households present, on average, lower levels of wealth and a lower probability of receiving intergenerational transfers. In short, the growing inequality within generations, particularly among the millennials, conditions the impact intergenerational transfers will have on wealth in the decades to come.

Intergenerational wealth transfer: Demographics, inheritance and outlook for the next generations

The widening of the wealth gap between generations is not caused solely by differences in accumulation processes throughout our lives but is also related to the dynamics by which the wealth accumulated by the previous generation gets passed along to the next generation. In Spain, this process is shaped by two key factors: the high starting concentration of wealth and the demographic structure of the cohorts involved in this wealth transfer.

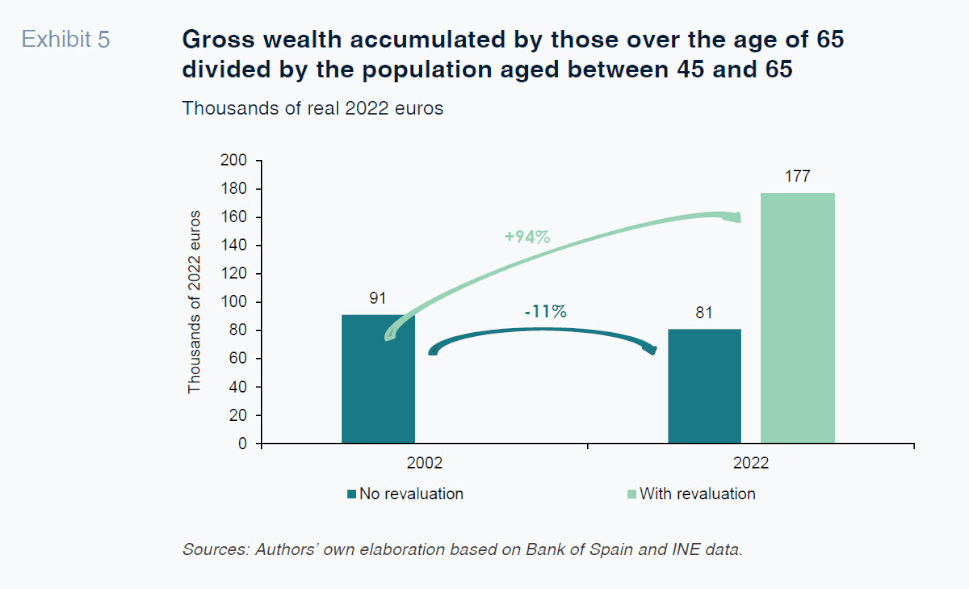

Looking back in time, it is possible to illustrate the relative weight of both factors using stylised analytical exercises based on the Survey microdata. Specifically, we calculate the hypothetical inheritance that would be received by people between the ages of 45 and 65 (recipients) if we were to distribute in one year the wealth accumulated by those over the age of 65 (benefactors). This simulation of hypothetical wealth distribution across generations allows us to quantify the importance of demographics on the transfer of wealth, and the role played by asset revaluation.

Comparing the situation in 2002 with that of 2022, the average inheritance so calculated increases from 91,000 real euros at the beginning of the century to 177,000 euros in 2022, growth of 95%, which is attributable, essentially, to the revaluation of the wealth accumulated throughout this period by those comprising the donor generation (those over the age of 65 in 2022). Indeed, in the absence of such extraordinary asset revaluation, the average inheritance would have decreased, to around 81,000 real euros in 2022, which is 11% less than would have been received by the preceding generation in 2002.

This latter phenomenon reflects the fact that the recipient generation, today’s baby boomers, is far more numerous than the previous generation: the ratio of recipient to benefactor has increased from 1.30 in 2002 to 1.51 in just 20 years. In other words, the increased size of the recipient generation relative to the donor generation has a negative impact on the average volume of wealth transferred per capita.

This exercise highlights a key question: the transfer of wealth across generations does not create equality. In the absence of real asset revaluation, mere growth in the relative size of the recipient generations reduces the amount of wealth transferred per capita. Therefore, in the case illustrated here, asset price dynamics, particularly house price dynamics, more than mitigated the adverse demographic effect observed in the recent past.

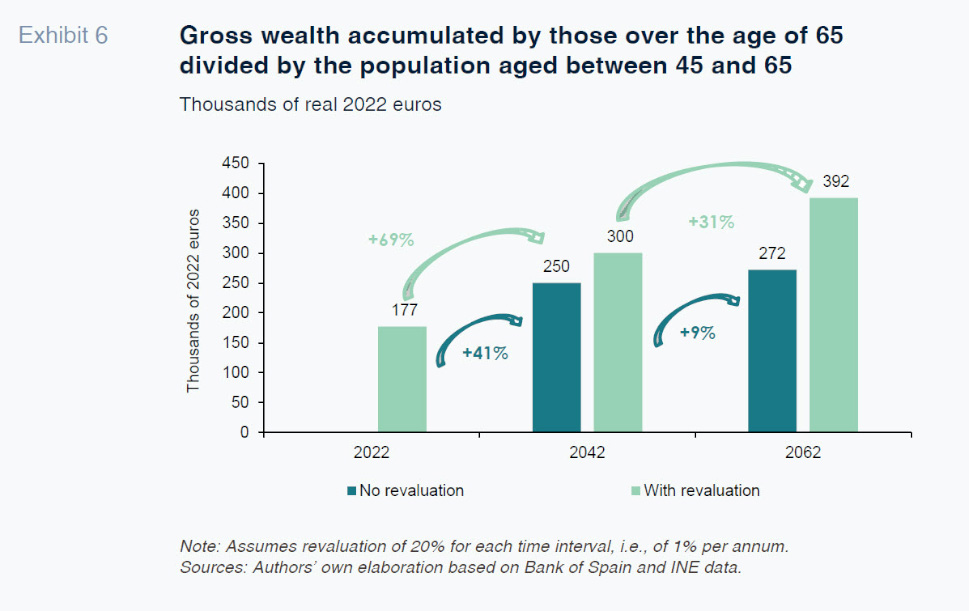

Looking ahead, the demographic effect will work the other way. Current projections suggest that the generations following the baby boomers will be considerably less numerous. If we conservatively assume that real wealth will be stable,

[1] this reduction in the relative size of the recipient cohorts will imply a significant increase in hypothetical wealth transferred per person to the millennials and Gen Z.

The results of this exercise show that the reduction in the ratio of recipients per benefactor, from 1.51 to 1.07, would increase the average inheritance received by the millennials by 41% between 2022 and 2042. And assuming asset revaluation of just 1% per annum, that average inheritance could increase by nearly 69% with respect to that received by the previous generation in 2022.

However, these figures need to be interpreted with caution. Firstly, because they rely on averages that mask considerable heterogeneity in the distribution of wealth. The evidence shows that wealth accumulation is sharply concentrated at the upper end of the distribution so that a significant percentage of households do not have meaningful amounts of wealth to pass along. In this context, inheritance and donations tend to reproduce and amplify initial inequalities, benefitting the descendants of the richest households disproportionately.

Secondly, growing intrageneration inequality further exacerbates this effect. As the concentration of wealth in the upper deciles increases, intergenerational wealth transfers cease to act as a broad redistributive mechanism, instead becoming an additional driver of wealth polarisation. Consider then the rising number of young people living in Spain who were born outside the country: because of their lower average wealth levels and lower propensity to inherit, their growing share of the population increases the dispersion of wealth per capita within a given age cohort.

Overall, the evidence suggests that although population ageing and the shrinking size of future generations could favour higher average wealth transmission, this process will not automatically correct existing inequalities. To the contrary, in the absence of offsetting mechanisms, the combination of wealth concentration, intragenerational inequality and demographic trends could reinforce the polarisation of wealth in the coming decades.

Conclusions: Wealth transfer and inequalities

The analysis carried out in this paper shows that wealth inequality in Spain has intensified sharply since the start of the twenty-first century, with both the intergenerational and intragenerational wealth gaps widening. Unlike income inequality, wealth inequality tends to be more persistent and to amplify with time due to asset accumulation and revaluation dynamics and intergenerational wealth transmission mechanisms.

From the intergenerational perspective, the evidence confirms a growing divergence in wealth accumulation across the different age categories. The older generations have been accumulating a growing share of total wealth, fuelled primarily by the revaluation of their property assets, as well as relatively more favourable income dynamics. In contrast, the younger generations have seen their ability to build wealth impaired by greater difficulties in getting on the housing ladder, income deterioration in the wake of the financial crisis and growing reliance on rental tenancy.

The intragenerational analysis reveals that, in addition, inequality is not only widening across generations but also within them, particularly among the millennials. The growing concentration of wealth among the top end of the distribution and the home ownership-rental divide are generating increasingly divergent wealth trajectories from early ages.

The intergenerational transfer of wealth, far from automatically alleviating these inequalities, could help amplify them. Although demographic projections suggest that the future generations could receive more wealth on average per capita, this forecast masks sharp heterogeneity associated with the initial concentration of wealth and biased distribution of inheritances.

Overall, the results suggest that the outlook for wealth inequality in Spain will depend not only on the volume of wealth transferred between generations but also on the terms of access to the assets by which wealth is accumulated, particularly housing. Understanding these mechanisms is essential to anticipating the economic and social challenges associated with population ageing and generational succession and to being able to design public policies that foster more equal opportunities in a context of growing wealth concentration.

Notes

The “no revaluation” scenario assumes there is no accumulation of wealth in real terms in order to isolate the demographic factor. The second scenario, “with revaluation”, assumes annual asset revaluation of 1% in real terms. This second scenario is not an attempt to estimate the scope for asset revaluation but rather aims to simulate how much each percentage point of wealth accumulation would add to the demographic effect derived from the shrinking size of future recipient generations.

References

ALVARGONZALEZ, P., ASENSIO, M., BARCELÓ, C., BOVER, O., COBREROS, L., CRESPO, L., EL AMRANI, N., GARCÍA-URIBE, S., GENTO, C., GÓMEZ, M., URCELAY, P., VILLANUEVA, E. & VOZMEDIANO, E. (2024). The Spanish Survey of Household Finances (EFF): Description and methods of the 2020 wave.

Occasional Papers, No. 2405. Bank of Spain.

ANGHEL, B., BASSO, H., BOVER, O., CASADO, J. M., HOSPIDO, L., IZQUIERDO, M., KATARYNIUK, I. A., LACUESTA, A., MONTERO, J.M. & VOZMEDIANO, E. (2018). Income, consumption and wealth inequality in Spain.

Series, 9, 351–387.

https://doi.org/10.1007/s13209-018-0185-1FUNDACIÓN AFI EMILIO ONTIVEROS. (2023).

Finanzas de los hogares 2000-2022: Escaso ahorro y mayor brecha generacional [Household finances, 2000-2022: Scant savings and growing generational gap]. Madrid: Afi Foundation.

FUNDACIÓN AFI EMILIO ONTIVEROS. (2024).

Demografía, vivienda y brechas de riqueza [Demographics, housing and wealth gaps]. Madrid: Afi Foundation.

PALOMINO, J. C., MARRERO, G. A., NOLAN, B., RODRÍGUEZ, J. G. (2022). Wealth inequality, intergenerational transfers, and family background.

Oxford Economic Papers, 74(3), 643-670.

https://doi.org/10.1093/oep/gpab052

Marina Asensio and Daniel Manzano. Afi