Geopolitical risks and the outlook for Spain’s growth cycle

The Spanish economy is expected to continue growing faster than the eurozone in the coming years, although the expansionary cycle is likely to lose momentum as some of its recent drivers fade. A sustained increase in energy prices linked to the Iran conflict represents the most immediate risk to this baseline scenario.

Abstract: The Spanish economy has shown remarkable resilience in recent years, maintaining strong growth despite a succession of external shocks. This performance has been supported primarily by robust domestic demand and strong population growth, while the contribution from foreign trade has weakened. Under the baseline scenario, economic activity is expected to continue expanding at a solid pace over the next two years, although gradually slowing as the effects of immigration, tourism and the European recovery funds begin to fade. GDP growth is forecast at around 2.4% in 2026 and 1.8% in 2027, still above the eurozone average but increasingly reliant on internal demand. This growth pattern is also likely to keep inflation somewhat higher than in the rest of the euro area. The main downside risk to this outlook stems from the outbreak of a new conflict in the Middle East and its potential impact on energy prices. A sustained increase in oil and gas prices would push inflation higher and erode household purchasing power, weakening private consumption, the main engine of current growth. Under such a scenario, the economic slowdown would be more pronounced than expected, demonstrating the vulnerability of the current expansion to external energy shocks.

Foreword

The Spanish economy has continued to perform well, judging by the preliminary growth figure for 2025 (2.8%, compared to the eurozone average of 1.5%), coupled with strong job creation. However, this healthy headline result masks an increasingly imbalanced profile: growth currently depends entirely on domestic demand, while foreign trade has gone from making a positive contribution at the start of the current expansionary cycle to a negative one. Domestic demand led growth has also made inflation somewhat sticky, with CPI rising faster than the eurozone average.

Against this backdrop, the eruption of the conflict in Iran ushers in a new threat to the goals of sustaining growth while curbing inflation. This paper presents our baseline scenario for the Spanish economy for the next couple of years, as we envisaged it before the onset of the hostilities in the Middle East. It then analyses the impact on inflation and GDP of a sustained increase in energy prices, the main channel through which the armed conflict is likely to affect the real economy.

Baseline scenario

Our baseline scenario is predicated on certain assumptions around macroeconomic policy and immigration; the latter having played a crucial role in explaining the Spanish economy’s recent outperformance. In terms of macroeconomic policy, we assume that the cycle of rate cuts has come to an end and that the deposit facility rate, the ECB’s most important benchmark, will remain at 2% throughout the projection period. The eurozone’s central bank believes that current settings are compatible with its inflation target and a slight recovery in the eurozone economy, while leaving it with some room to react in response to shocks.

Secondly, we assume that fiscal policy will go from being expansionary thanks to the disbursement of the Next Generation EU funds to neutral, as those funds are depleted. This inflexion point is expected to come into sharper focus from next year.

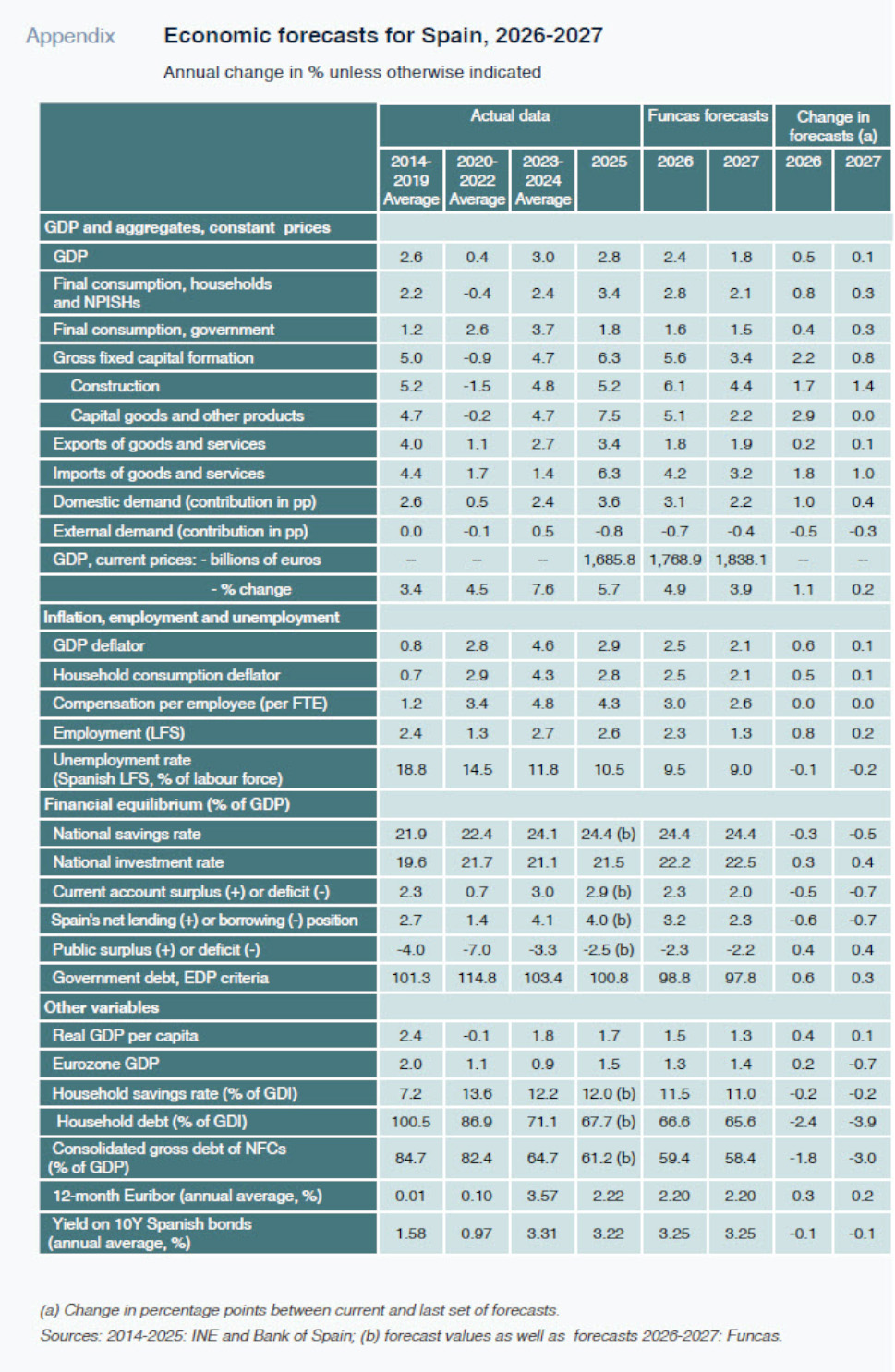

As for immigration, we assume the slowdown in the number of foreign arrivals to extend throughout the forecast horizon. The foreign labour force would grow by 5% this year and by 4% in 2027 (compared to 8.2% in 2024 and 6.3% in 2025) (

Exhibit 1). This assumption presupposes that the recently announced scheme for the legalisation by undocumented workers will affect employment only (as we will see below) and not inflows of foreign labour, at least not in the short term.

Underpinned by these assumptions, the Spanish economy is expected to continue to grow at a healthy rate, albeit tending to slow. In 2026, GDP growth is forecast at 2.4%, up 0.5 percentage points from Funcas’ October projection, attributable above all to the carryover effect from last year (Appendix). This carryover effect alone accounts for 0.3 points of the upward growth revision.

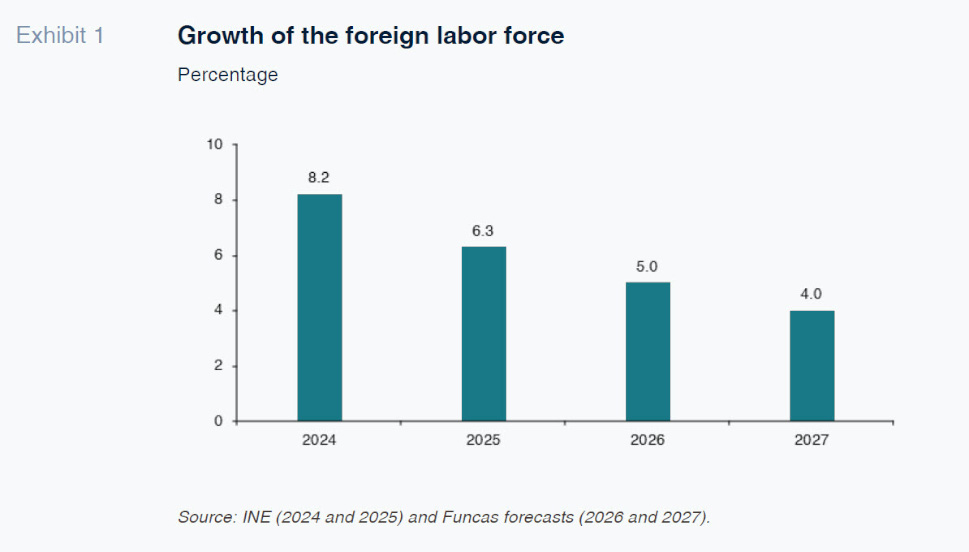

The expansion will be driven solely by domestic demand, which is expected to contribute 3.1 points, up one point from our October projection. Private consumption stands out, buoyed by job creation and, to a lesser extent, increased real earnings. Investment is expected to continue to grow, thanks to the recovery in residential construction (still insufficient to close the housing gap) and the need to accelerate execution of the remaining Next Generation EU funds. However, corporate investment is expected to remain the slowest-growing component of total investment.

On the other hand, the foreign sector is expected to detract 0.7 points from GDP growth, which is more pessimistic than in our previous projections (Exhibit 2). This outcome is the result of the slowdown in exports in the context of European economic weakness, global trade tensions and, in Spain, overtourism and reduced competitiveness at some of the most popular tourist destinations. In parallel, imports are expected to grow by more than internal demand, revisiting long-run elasticities and exacerbating the foreign sector’s negative contribution to GDP growth. Imports from China are expected to be particularly strong as Chinese companies strive to accelerate their exports to mitigate an increasingly sluggish home market.

In 2027, the Spanish economy will again register above-average performance, with GDP growing by 1.8%, up 0.1 point from our previous projections. The upward revision reflects the persistence of relatively strong domestic demand, while the foreign sector would continue to undermine growth. Overall, the drop-offs in tourism and in the fiscal stimulus derived from the end of Next Generation EU funds, along with weaker population growth —i.e., the factors underpinning the ongoing growth cycle— will be felt more acutely next year.

The growth pattern, dominated by domestic demand and a weak foreign sector, will drive a reduction in the current account surplus to 2% of GDP in 2027, down nearly one point from 2025. That is still a solid surplus, however, in addition to reflecting an improvement in investment (thanks to the residential segment, mainly) rather than a drop in national savings.

The momentum in domestic demand also explains the fact that inflation is expected to remain at around 2.5% this year, whereas the eurozone average is forecast at under 2%, suggesting a loss of competitiveness. This unfavourable inflation gap is expected to continue in 2027, albeit narrowing, due to the above-mentioned slowdown in domestic demand.

Despite being less balanced than at the start of the growth cycle, economic growth should lead to the creation of around 800,000 net new jobs in the next two years, allowing unemployment to dip below 9%, down 0.2 points from the previous projections. In addition to the jobs created by sheer economic momentum, the legalisation of undocumented workers will have the effect of increasing employment, as happened during a previous amnesty episode back in 2005, which has been used as a benchmark for the present projections.

Economic growth should also help rein in the current budget imbalances, which will improve thanks to higher tax receipts –an effect which is basically cyclical, rather than reflecting any structural improvement. We are forecasting a reduction in the public deficit to 2.3% of GDP in 2026. Stripping out interest payments, Spain would report a surplus (of 0.1% of GDP) for the first time since 2007. In light of the anticipated slowdown in growth, the additional improvement in 2027 is expected to be very small. At the end of next year, government debt is forecast at 97.8% of GDP, which is still a relatively high figure.

Conflict in Iran

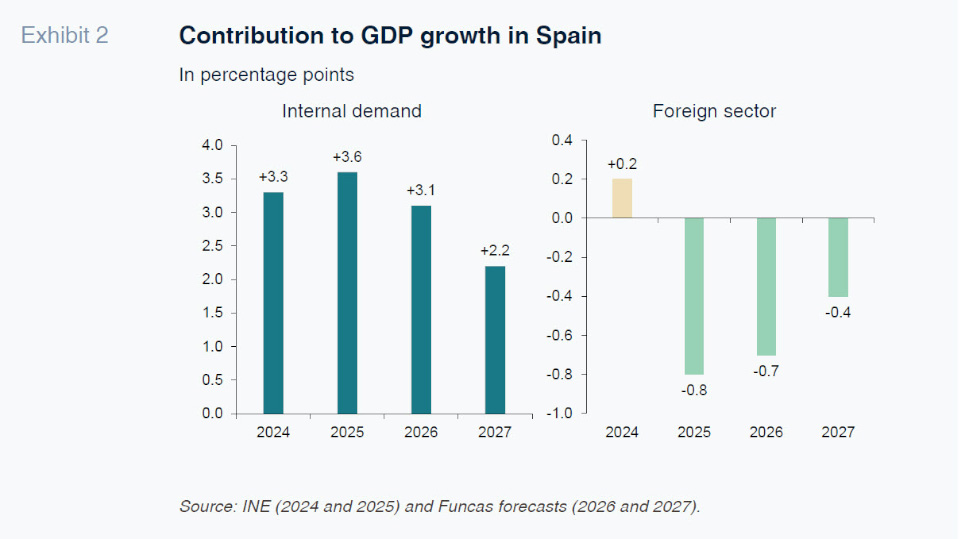

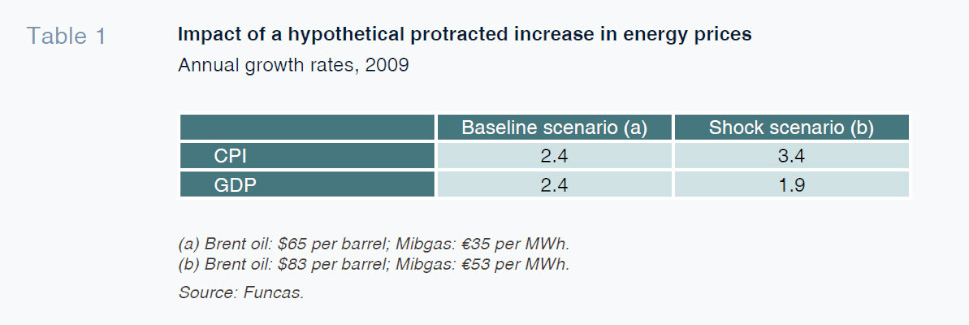

Energy prices are a factor to be considered in any scenario. Their moderation over the past few years has been one of the key factors behind the subsequent drop in inflation and boom in consumption. Our baseline scenario is underpinned by the assumption that Brent oil prices will remain at around $65 per barrel throughout the projection period, that Mibgas gas prices will remain at the levels they started the year at (€35 per MWh) and that one euro will continue to trade around $1.17.

However, in the days following the onset of the war in Iran (the last weekend of February), oil prices rose above $80 and Mibgas prices topped €53, while the euro slid to $1.16. If this situation were to persist, it would imply a significant change with respect to our baseline scenario (Exhibit 3).

If Brent and Mibgas prices observed at the time of writing were to remain at current levels for the rest of the year, the average inflation rate would rise to 3.4% and core inflation would increase to 2.8%, one and 0.3 points above the baseline forecasts, respectively. An increase in the cost of these energy products hits consumer wallets directly and immediately via the impact on fuel and electricity bills. It also implies an increase in production costs, which, if persistent, would be passed along the production chain and ultimately to end consumers, giving rise to a second round of price increases, which would be reflected in core inflation.

The higher cost of fuel and electricity would weigh on private consumption, the main engine of growth in the short term. Exports would also be affected by the negative fallout on other countries’ economies. Tourism would be another transmission channel via the higher cost of flights and the general impact of inflation on visitors’ purchasing power; however, it is possible that this impact would be partially mitigated by a perception of Spain as a more attractive, specifically a safer, destination than competitor destinations near to the Middle East. One last possible transmission channel would be investment. Indeed, investment decisions could be put on hold or postponed as a result of the uncertainty.

The sum of all of these effects, factoring in the small mitigating effect of slower growth in imports, could detract around half a percentage point from GDP growth in 2026. The impact would be, therefore, stagflationary, i.e., an increase in inflation and, in parallel, a slowdown in economic activity.

Upside and downside

Uncertainty continues to dominate the international context, marked by the transition from a rules-based multilateral system to an asymmetric power-based order. The latest episode is the conflict in the Middle East, which could lead to new threats for trade and transatlantic relations in general. Moreover, the EU has failed to agree on a strategy for counteracting the initiatives emanating from the Trump administration and does not seem to be making progress on strengthening the single market. Domestically, tourism could be affected by more than anticipated due to a loss of competitiveness. Elsewhere, uncertainty continues to weigh on corporate investment and as the European funds run out, this weakness could become more apparent than we are forecasting.

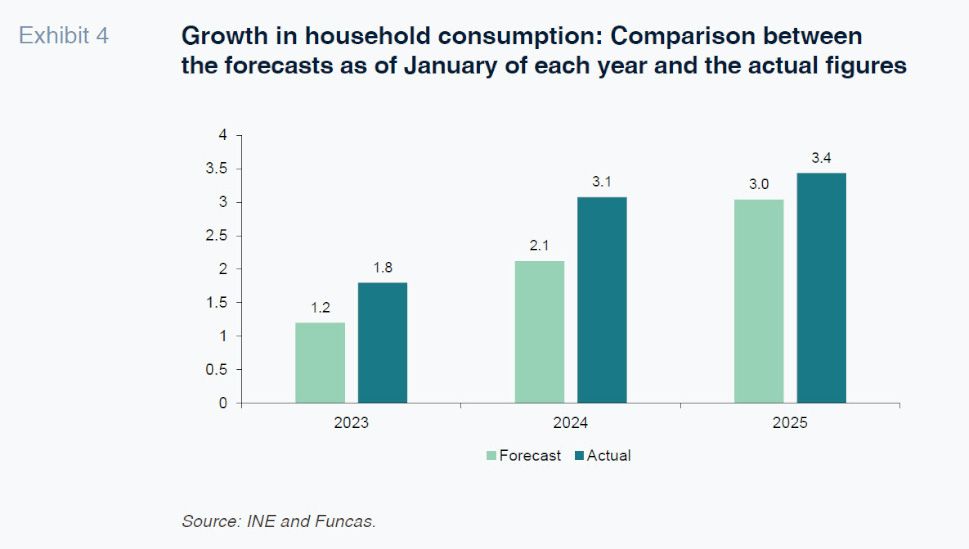

As for the upside, household consumption could increase by more than we are forecasting. Indeed, in recent years, private consumption has proven consistently stronger than anticipated. Between 2023-2025, it registered real growth of 8.5%, topping our forecasts every year (Exhibit 4). The deviations with respect to our forecasts were shaped by (i) higher than expected growth in consumption per capita; and (ii) higher than forecast population growth. The higher growth in consumption per capita was in turn the result of higher than expected growth in gross disposable income, in spite of the fact that the savings rate came in higher than planned.

Going forward, foreign worker arrivals could be stronger than anticipated, which would stimulate consumption and activity in the sectors where labour is in higher demand. In addition, there is some uncertainty around the sustainability of the current savings rate, which is projected at 11% at the end of the forecast horizon, i.e. well above the levels considered normal a few short years ago. In this set of forecasts, we assume that this change is structural, shaped by factors such as immigration or the need to save more to purchase a home. We are forecasting a reduction in the savings rate in the coming years, in line with this hypothesis. However, certain circumstantial factors, which will wane with time, could prevail, pushing consumer spending higher.

Raymond Torres. Head of macroeconomic and international analysis, Funcas

María Jesús Fernández. Economist, Funcas