Effects of the introduction of a tourist tax

Tourist taxes are often criticised for undermining the competitiveness of destinations. However, in locations experiencing overtourism, a well-designed tax can help ease congestion, improve the quality of the visitor experience, and support a gradual shift towards higher-value tourism.

Abstract: Overtourism has re-emerged as a major challenge for many European destinations since the end of the pandemic, generating pressure on local infrastructure, housing markets and natural resources. Beyond its social and environmental impacts, excessive tourism can also undermine the visitor experience and weaken a destination’s long-term competitiveness. Tourist taxes are frequently criticised for raising costs and discouraging demand, yet economic theory suggests that a carefully calibrated tax can help correct the externalities associated with tourism activity. By increasing the cost of visiting congested destinations, such taxes can moderate demand and reduce pressure on common resources. If properly designed, they may also encourage a shift in demand towards visitors who place greater value on quality. In practice, this tends to attract tourists who are less sensitive to higher prices. Evidence from the Balearic Islands, one of Europe’s most mature and tourism-intensive destinations, demonstrates this logic. That said, simulations based on tourism demand elasticities suggest that the existing tax would need to increase by between 15 to 20 euros to generate a meaningful reduction in peak-season demand. While not a standalone solution, a stronger tourist tax could play an important role in managing tourism pressure while reinforcing the long-term competitiveness of the destination.

Introduction

Overtourism (Peeters et al., 2018) constitutes a growing challenge for the world’s most popular destinations. The Balearic Islands, along with other European destinations, are dealing with this intensifying and pressing problem. This paper analyses how a tourist tax can help destinations to curb overtourism, while reinforcing their competitiveness in tandem. The debate tends to pivot around a choice between more revenue and employment versus higher social and environmental costs (expensive housing, congestion, degradation). However, that need not be the case: a well-designed tax can alleviate overtourism and generate benefits for both the resident population and the destination’s businesses. If a tourist tax manages to enhance the experience for visitors, the destination will be better able to attract tourists who attach greater importance to quality and are willing to pay for it. (see Calveras, 2026) [1].

Overtourism and its consequences

Since the end of the COVID-19 pandemic, the overtourism phenomenon has re-emerged forcefully as a key issue for many destinations in Europe, including Spain. The term “overtourism” (Peeters et al., 2018) refers to saturation in destinations provoked by overuse of their common resources (beaches, roads, natural spaces and urban areas) as a result of tourism (refer, for example, to Picó et al., 2022).

The existence of overtourism does not depend solely on the absolute number of visitors but also on other factors such as the length of their stay or the destination’s carrying capacity (McCool and Lime, 2001). Therefore, its presence must be diagnosed at the local or destination level and not at the country level, as there may be significant differences from one destination to another within a given country. For example, the situation in Mallorca is clearly nothing like the situation in Asturias. To accurately measure overtourism, a couple of indicators have been put forward, including tourism density (bed-nights or tourists per km²) and tourist intensity (bed-nights or tourists per resident) for better gauging the phenomenon (Peeters et al., 2018).

The impacts of overtourism materialise at several levels. Firstly, they affect local residents directly: mobility issues, more expensive housing, transformation of traditional neighbourhoods and loss of local commerce, among others. Secondly, there is empirical evidence that overtourism reduces tourist satisfaction and may damage a destination’s sustainability. In Yucatán, for example, tolerance for overtourism falls as tourist flows increase, particularly among international tourists, who are more sensitive to environmental quality and tranquillity (Enseñat-Soberanis et al., 2020). Along Spain’s Costa del Sol, 26% of visitors said they felt there were too many tourists and that repudiation may be underestimated because those who perceive it do not come back (Jurado et al., 2013). It is worth noting that those who are more sensitive to overtourism tend to have higher education levels, more purchasing power and higher travel budgets, so that preserving a quality experience is key for competitiveness (Jurado et al., 2013).

Tourism tax and its logic

Logically, tourism sector, in turn comprised of different subsectors such as transportation, accommodation, entertainment, eateries, etc., is subject all the usual taxes borne by the rest of the economy: corporate and personal income tax, VAT, etc. However, VAT on hotels, eateries and domestic air travel is 10%, compared to the general rate of 21%. It is not implausible, therefore, to claim that the sector is, in fact, subsidised.

Regardless, the term tourism tax usually refers to taxes on occupancy in paid accommodation that are charged per person and per night (PwC, 2017). The Impact of Taxes on the Competitiveness of European Tourism report (PwC, 2017) shows how “occupancy taxes make up a small proportion of the overall cost of accommodation” and “range from a minimum of €0.10 (the lowest rate in Bulgaria) to a maximum of €7.50 (the highest rate in Belgium) per person each night, with the average range being between €0.40 and €2.50” (PwC, 2017, 36-37, Table 5).

A tourism tax can serve multiple, compatible goals (Gago et al., 2009):

- Generating public revenue: creating a price payable by tourists for the use of ‘free’ common goods at the destination (security, roads, beaches, etc.).

- Correcting externalities: using the money collected to repair environmental and social damages derived from the negative externalities of tourism (cleaning beaches, investing in public housing, etc.).

- Pigouvian corrections: altering agents’ conduct by forcing the internalisation of externalities and regulating the flow of tourists to the destination (Baumol and Oates, 1988).

Whereas the amount of the tourism taxes in existence suggests that they are not Pigouvian taxes and would, at any rate, have only a very small impact on modifying the conduct of potential tourists, we now highlight the potential implicit in this Pigouvian logic whereby a tourism tax, beyond raising public revenue and mitigating externalities, has the ability to reduce overtourism and reinforce the competitiveness of tourist destinations and their businesses.

Tourism competitiveness and tourism tax

One of more frequent criticism from the corporate sector against the imposition of a tourism tax is its alleged negative impact on destination competitiveness. This is the vision embodied in the Monitur tourism competitiveness index compiled by Exceltur (an alliance of the leading Spanish tourism companies) to measure the tourism competitiveness of the different Spanish regions.

Monitur defines tourism competitiveness as the regions’ ability to build unique and sustainable positioning around tourism in a manner that harmonises economic growth, job creation and social wellbeing. That approach is correct: the competitiveness of a destination is not circumscribed to the competitiveness or profitability of its firms, but also includes social wellbeing in the region and environmental considerations (Ramos and Rey-Maquieira, 2024).

To measure competitiveness, the index uses 90 objective indicators, including the presence, or absence, of tourism taxes, which count negatively where they exist, i.e., assuming they detract from a region’s tourism competitiveness. Catalonia and the Balearic Islands, for example, were penalised in the indices for 2018 and 2023 for having introduced and maintained their respective tourism taxes.

This approach by Exceltur and Monitur is, however, wrong on two counts. The relationship between a region’s or country’s competitiveness and the level of its tax burden depends on several factors, including how the tax receipts are spent or invested, as Paul Krugman already explained years ago (Krugman, 2005; refer also to Medeiros et al., 2019). But not just that. Given that overtourism at a destination undermines both the quality of life of its residents and the satisfaction of its tourists and, by extension, the business of its companies, a tourism tax has the ability to make a positive contribution to destination competitiveness, including that of its businesses.

Calveras and Sakovics (2025) show that in destinations suffering from overtourism, a well-calibrated tourism tax may even be optimal from the perspective of business profitability. By pushing up the total cost of the trip, the tax eases tourism pressure and, along with it, saturation, alleviation that is appreciated in particular by visitors with more spending power. This reduced congestion raises the perceived quality of the destination and could increase the propensity to pay of tourists who attach more importance to the experience, with potentially positive effects for sector revenue and margins. For this mechanism to truly lift competitiveness, it has to bring about demand reconfiguration. Specifically, it needs to discourage the types of tourists who are less inclined to pay and draw tourists who are willing to pay more for a better experience.

In this sense, Exceltur’s Monitur index starts from an erroneous theoretical assumption in assuming a necessarily negative relationship between tax burden and tourism competitiveness without factoring in the degree of overtourism at a given destination. The same can be said of the line of reasoning expressed by PwC (2017) in its Recommendation 1: “Reduced taxes on tourism can increase the competitiveness of tourist destinations and bring wider economic benefits”, by omitting two key considerations. Firstly, the investment and redistribution potential associated with tax receipts; and secondly, the ability of these taxes to reduce overtourism and, thereby, generate economic value and improve destination competitiveness.

Balearic Islands case study

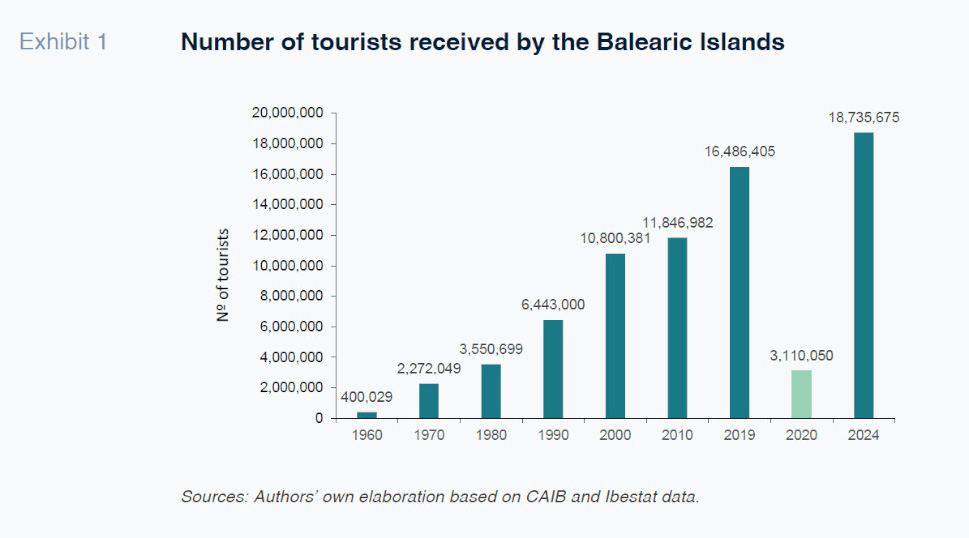

The Balearic Islands are a mature tourist destination. Exhibit 1 evidences the significant growth sustained in both tourism supply and demand; the volume of visitors has multiplied in recent decades. Peeters

et al. (2018) identifies Mallorca as a clear case of overtourism. In 2017, the island (with fewer than one million inhabitants) recorded over 11 million tourists, nearly 46 million bed-nights and more than 1.5 million cruise ship visitors. Tourism intensity was very high: 14.9 daily visitors for every 100 residents and 35.6 tourists per km².

Faced with that reality, what role can and/or should a tourism tax play? The Sustainable Tourism Tax (ITS for its acronym in Spanish) in place in the Balearic Islands was approved by the regional government in 2016 and doubled in size in 2018. The tax currently ranges from €1 to €4 per person and night depending on the type of accommodation and its category (see CAIB, 2025).

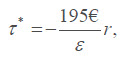

How high should that tax be to combat overtourism in the Balearic Islands, i.e., to reshape demand for tourist services? Note that the goal of this exercise is not to calculate the optimum tax in terms of social wellbeing but rather to estimate the increase in the existing tax ‘needed’ to bring about a targeted percentage decrease in demand.

The analysis follows the approach taken by Rosselló and Sansó (2017) in their assessment of the impact of the creation of the Sustainable Tourism Tax in the islands in 2016. To do that, they used a tourism demand model assuming a constant price elasticity and using the number of bed-nights as their proxy for demand and spending per person and day as their proxy for price.

Turning to the statistics for 2019 and 2024, the data (Ibestat) indicate that the number of bed-nights in the Balearic Islands in those years were 109, 469, 735 and 119, 982, 802 over the entire season, respectively, and 91, 447, 867 and 96, 991, 686 during the peak season. The figures indicate a significant increase in tourism pressure during that span of years, specifically growth of 9.6% in total stays and growth of 6.06% during peak season.

[2] The Ibestat figures yield weighted average spending per person and day during the peak season of 195 euros in 2024.

For this exercise, we contemplate increasing the tourist tax by a fixed amount for all categories for sound reasons in addition to simplicity: increasing the tax on the lower category segments by relatively more encourages the tourism sector to raise the quality of its offering, so reinforcing its competitiveness (Calveras and Sakovics, 2024).

We assume that the tax is only increased during the peak season (May to October), although it could make sense to eliminate it during the off season (during which time it is currently subject to a discount). Simple calculations show that the ‘necessary’ tax increase is

where, as a reminder, €195 is spending per person and day (proxy for the current price of tourism services); ε represents the price elasticity of demand; and

r is the targeted percentage reduction in demand.

[3]

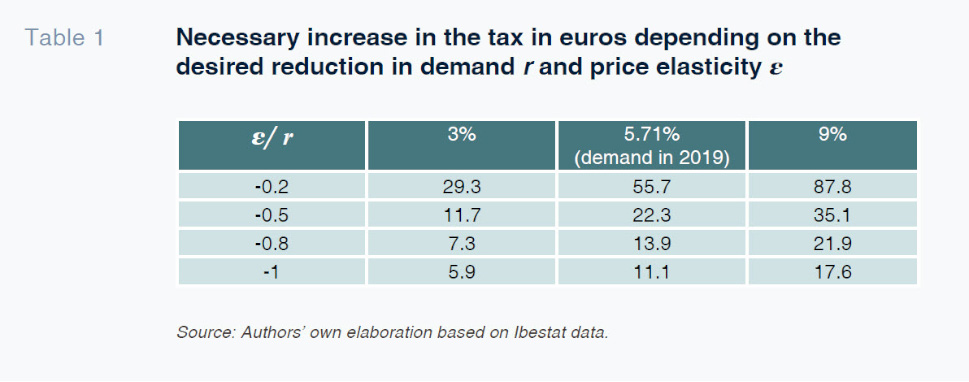

Table 1 shows the results of the different scenarios modelled. For example, reducing the number of bed-nights during the peak season in 2024 to 2019 levels would imply a decrease of 5.71%. Rosselló and Sansó (2016) assume elasticities of -0.5 and -1, whereas the report on the economic impact drawn up by the regional government when approving the tax in 2016 used an elasticity of -0.47. Note that Rosselló and Santana (2024), using visa costs, conclude that the price elasticity of demand is even lower, at between -0.27 and -0.625.

A plausible and conservative scenario would be to assume price elasticities of between approximately -0.5 and -0.8, coupled with a reduction in demand based on the levels observed in the year prior to the pandemic. Table 1 tells us the increase in tax needed to reduce demand by 5.71% (

i.e., to return to 2019 levels) is between 15 and 20 euros, approximately.

[4] Two considerations suggest that Table 1 may underestimate the increase in tax needed to reduce tourist flows. Firstly, assuming that the impact of the tax would be fully passed through to tourists in the form of price increases; and secondly, possible overestimation of the price elasticity of demand by not factoring in the income elasticities of the source markets, which in the case of the Balearic Islands, depict a quality-seeking tourist that is less sensitive to price (refer to CaixaBank Research, 2025, Inchausti-Sintes

et al., 2021).

Conclusion

A tourist tax is not a magic pill for overtourism but it probably is the most effective tool available. For it to have a noticeable impact on demand, it needs to considerably higher in amount than at present. According to our estimates, to impact demand in the Balearic Islands, it would need to be increased by between 15 and 20 euros. Although this figure may seem steep, it is still moderate by comparison with daily expenditure per tourist and the average hotel rate in July 2024 (183 euros, Ibestat). In fact, its magnitude would be similar to the effect of increasing VAT on tourism goods and services from the current reduced rate of 10% to the standard rate of 21%. In addition, its implementation could be staggered over several years, which would allow ongoing assessment of its impact and redesign based on the evidence.

Some final thoughts. Firstly, a significant increase in the tax would need to be accompanied by tighter controls over possible attempts at tax evasion (illegal rentals, fraud), including an assessment of hard-to-avoid collection mechanisms, such as charges at ports and airports. Secondly, it would work best in conjunction with other measures: combining it with limits on hotel capacity and holiday rentals could be more effective, as well as facilitating political consensus. Lastly, more than alleviating existing overtourism, the tax would serve to prevent future saturation. However, it will not, by itself, resolve other structural pressures, such as growth in the resident population and second homes and the boom in digital nomads.

Notes

Forthcoming in Funcas, for a more detailed discussion of this topic.

The bed-night count includes nights spent in paid accommodation (hotels, tourist apartments, etc.) and those spent off market (second residences, friends’ and families’ homes, etc.). The Balearic tourism tax, as currently configured, only affects bed nights in paid accommodation. The Ibestat figures show that the percentage of visitors to the Balearic Islands that use paid accommodation during the high season has not changed meaningfully between 2019 and 2024, ranging from 85 to 90%.

Note that the increased tax would only affect visitors staying in paid accommodation and would not affect those exempted from the tax (such as minors under the age of 16).

References

BAUMOL, W. J., & OATES, W. E. (1988).

The Theory of Environmental Policy (2nd ed.). Cambridge University Press.

BLANCO-ROMERO, A., BLÁZQUEZ-SALOM, M., & FLETCHER, R. (2023). Fair vs. fake touristic degrowth.

Tourism Recreation Research, 50(2), 435-439.

CAIB. (2025).

https://www.caib.es/sites/oie/es/impost_turisme_sostenible/CAIXABANK RESEARCH. (2025). Tourism. The Spanish tourism sector: No signs of cyclical exhaustion.

https://www.caixabankresearch.com/en/tourism/january-2025/tourism-spanish-tourism-sector-no-signs-cyclical-exhaustionCALVERAS, A. (2026).

Tourism tax to tackle overtourism and lift competitiveness: A case study using the Balearic Islands. Investigaciones de Funcas, 31/2026 (forthcoming).

CALVERAS, A., & SÁKOVICS, J. (2025). A tourist tax in a vertically segmented destination with congestion effects.

SERIES, 1-23.

ENSEÑAT-SOBERANIS, F., BLANCO-GREGORY, R., & MONDRAGÓN-MEJÍA, J. A. (2020). Perception of congestion and social dimension of the carrying capacity in Yucatan cenotes.

Cuadernos de Turismo, (45), 93-112.

https://doi.org/10.6018/turismo.426051GAGO, A., LABANDEIRA, X., PICOS, F., & RODRÍGUEZ, M. (2009). Specific and general taxation of tourism activities: Evidence from Spain.

Tourism Management, 30(3), 381-392.

INCHAUSTI-SINTES, F., VOLTES-DORTA, A., & SUAU-SÁNCHEZ, P. (2021). The income elasticity gap and its implications for economic growth and tourism development: The Balearic vs the Canary Islands.

Current Issues in Tourism, 24(1), 98-116.

KRUGMAN, P. (2005). Toyota, moving northward.

The New York Times. https://www.nytimes.com/2005/07/25/opinion/toyota-moving-northward.htmlMCCOOL, S. F., & LIME, D. W. (2001). Tourism carrying capacity: Tempting fantasy or useful reality? J

ournal of Sustainable Tourism, 9(5), 372-388.

MEDEIROS, V., GONÇALVES, L., & CAMARGOS, E. (2019). Competitiveness and its determinants: A systemic analysis for developing countries.

CEPAL Review, (129).

MIRALLES, C. C., BARIONI, D., MANCINI, M. S., JORDÀ, J. C., ROURA, M. B., SALAS, S. P., ... & GALLI, A. (2023). The footprint of tourism: A review of water, carbon, and ecological footprint applications to the tourism sector.

Journal of Cleaner Production, 422, 138568.

PEETERS, P., GÖSSLING, S., KLIJS, J., MILANO, C., NOVELLI, M., DIJKMANS, C., EIJGELAAR, E., HARTMAN, S., HESLINGA, J., ISAAC, R., MITAS, O., MORETTI, S., NAWIJN, J., PAPP, B., & POSTMA, A. (2018). Overtourism: Impact and possible policy responses [Research for TRAN Committee]. European Parliament, Policy Department for Structural and Cohesion Policies, Brussels.

https://op.europa.eu/en/publication-detail/-/publication/30617bd1-29c2-11e9-8d04-01aa75ed71a1/language-enPICÓ GUTIÉRREZ, V., SÁNCHEZ AGUILERA, D., & COLL RAMIS, M. À. (2022). Public policies and overtourism in urban destinations: A comparative analysis between Barcelona and Palma.

Cuadernos de Turismo, 49, 189-207.

https://doi.org/10.6018/turismo.521871RAMOS, V., & REY-MAQUIEIRA, J. (2024). Destination competitiveness. En J. Jafari & H. Xiao (Eds.),

Encyclopedia of Tourism. Springer.

https://doi.org/10.1007/978-3-030-74923-1_54ROSSELLÓ, J., & SANSÓ, A. (2017). Taxing tourism: The effects of an accommodation tax on tourism demand in the Balearic Islands (Spain).

Cuadernos Económicos de ICE, (93).

ROSSELLÓ, J., & SANTANA-GALLEGO, M. (2024). The effect of visa types on international tourism. Economic Modelling, 137, 106757.

Aleix Calveras Maristany. Full professor of the Department of Business Economics University of the Balearic Islands