Bank valuations and the effects of excess capital

European banks are holding capital well above supervisory requirements, even as regulatory simplification rises up the policy agenda. Yet this may be counterproductive, as excess capital —absent clear improvement in risk or profitability— is linked to lower returns and weaker market valuations.

Abstract: European banking has entered a new phase in which the policy focus has shifted from strengthening resilience to simplifying an increasingly complex regulatory framework. Banks continue to hold capital levels well above minimum requirements, raising the question of whether excess capital acts as a buffer that enhances stability or as a drag on profitability and shareholder value. From a valuation perspective, bank market performance depends on the spread between return on equity and the cost of equity, making capital accumulation without a corresponding increase in profits potentially dilutive. Empirical analysis of large euro area banks shows a negative relationship between capital levels and valuation multiples, which becomes more pronounced when focusing specifically on capital held above regulatory and supervisory thresholds. The evidence suggests that markets distinguish between required capital, which underpins resilience, and excess capital, which carries an opportunity cost unless it reduces risk or supports sustainable growth. As such, holding capital beyond prudential needs may weigh on returns and valuations, particularly when it does not translate into lower funding costs or higher earnings.

Paradigm shift in bank supervision

Nearly two decades on from the Great Financial Crisis, bank regulations in Europe have moved, remarkably successfully, from a paradigm centred on sealing cracks through successive layers of regulatory requirements to one in which the key challenge is no longer that of raising the resilience bar but rather ensuring that the resulting complexity does not distort incentives, dim the regulatory signal or erode efficiency. This shift is the backdrop for the political and institutional push for simplification: in March 2025, the Governing Council of the ECB set up a High-Level Task Force on Simplification (HLTF) to develop proposals for making the prudential, supervisory and reporting framework less complex for fear it may be disproportionately burdening the banks and, ultimately, limiting the system’s ability to finance the real economy. The endorsement by the Governing Council of the HLTF’s recommendations last December marks a milestone: simplification is no longer a rhetorical aspiration but rather an explicit aim of supervisory policy.

The HLTF is not proposing a counter-reform that would jeopardise the maxim of preserving financial system stability but rather fine-tuning of the regulatory framework framed by a series of governing principles that delimit the scale of the simplification thrust: (i) maintaining current resilience levels; (ii) ongoing effectiveness in meeting microprudential, macroprudential and resolution objectives; (iii) fostering European harmonisation and financial integration; and (iv) upholding international cooperation and implementation of Basel III. In other words, the “paradigm shift” does not consist of lowering the bar but rather changing the manner in which it is upheld: less complexity, more consistency, more predictability for banks and investors and, above all, more select and risk-based supervision to channel resources (those of the supervisors and of those supervised) towards material and emerging risks.

This ambition translates into three major areas of action —regulation, supervision and reporting— which, taken together, point to a common goal: making the prudential signal clear again.

On the regulatory front, the HLTF flags the need to reduce “the number of capital stack elements”, which exceeds those foreseen by the Basel standards, and ensure uniform application across jurisdictions. Hence the recommendation to cut the number of elements by, for example, merging the different capital buffers into two (a non-releasable buffer and a releasable buffer) and simplifying the leverage ratio framework, where the EU introduces more elements than the Basel III framework. The underlying thesis is that when the capital buffers are multiplied through potentially overlapping calibrations, uncertainty around effective stringency increases and it becomes harder to externally assess the amount of “usable” capital and the margin for manoeuvre (the “distance to MDA”). In other words, complexity is not neutral: it can hinder capital planning, encumber dialogue between the banks and their supervisors and cloud market interpretations.

In terms of the supervisory framework, the proposal is to move towards greater proportionality and a more risk-based approach. The HLTF proposes increasing the scope of the supervisory regime for small and non-complex institutions (SNCIs) and revising the mandatory nature of certain requirements, replacing them with more flexible rules, without jeopardising prudential targets. In parallel, the Governing Council itself has tied this reform agenda to its reform of the Supervisory Review and Evaluation Process (SREP). It wants to extend the objectives of the SREP reform to new areas by promoting a unified supervisory culture within the SSM and improved analytical tools to better assess the impact and effectiveness of its supervision.

On the reporting front, the HLTF has proposed a “single request / report once” ecosystem. The notion of an integrated system in which the same repository of information can be used for statistical, prudential and resolution purposes is a bet on standardisation so as to reduce overlap and prioritise data reuse and traceability, accompanied by materiality thresholds for public inventories of non-market sensitive reporting requirements and periodic reviews.

In sum, this reorientation of the regulatory and supervisory framework seeks to leave the stability of the financial system intact while increasing transparency, proportionality and introducing a more risk-based approach. All of which ushers in a debate about the advisability of a widespread industry practice: the accumulation of more capital than required by the supervisors by way of de facto prudential rule.

It is against the backdrop of this debate that this article addresses, from an empirical perspective, whether there is a gap between the amount of capital the prudential framework deems sufficient and the additional capital that the banks decide to hold as a discretionary buffer and how that excess ultimately translates into value creation or destruction for shareholders.

The structural link: ROE, COE and shareholder value creation

From the bank valuation perspective, the market value of a bank is the present value of its expected ability to generate future profits from the capital the market has provided it with.

Metrics such as the price-to-book value (P/B) multiple —the relationship between a bank’s share price in the financial markets and its book value per share— tell us whether the market is valuing a bank at more or less than its accounting book value and, by extension, represents an increasing function of the spread between the return generated by the bank (ROE) and that required by its shareholders (COE).

It is more expensive for all firms to finance themselves with equity than third-party borrowings. The reason is that equity not only carries out a financing function, like all other liabilities, but also performs an economic or guarantee function as shareholders are first in line to absorb losses in the event they materialise.

This absorption of first losses is precisely the reason why the return required by shareholders (expressed as the cost of equity, or COE) incorporates a higher risk premium than other sources of financing. The fact that the banks, unlike other sectors of the economy, are bound by minimum capital requirements, increases asymmetry for investors and has a direct impact on bank valuations.

As a result, when the bank sector does not reach a minimum return that compensates for this higher equity risk premium (ROE below the COE), its stock market value falls below its book value (P/B below 1x).

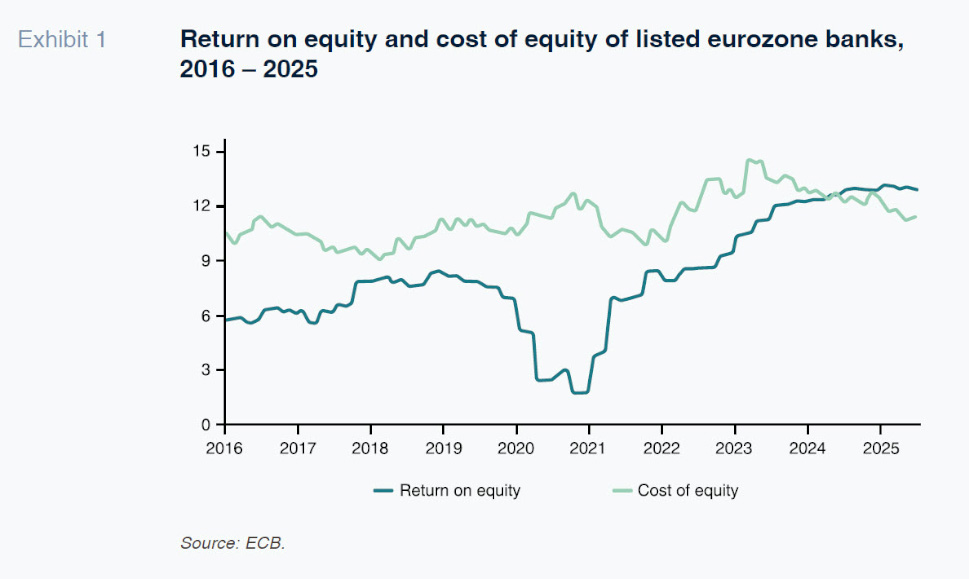

Exhibit 1 shows how for many years the European banks generated a much lower return on equity (ROE) than what the markets expected (COE). In the new rate environment that emerged in the wake of the spike in inflation in 2022, their ROE began to climb steadily higher, clearly exceeding the COE for the last two years. The market’s response has been a sharp increase in valuation multiples (P/B), from levels well below 1x to well above, with the highest-valued banks, including the Spanish banks, closing in on a multiple of 2x.

It is important to underscore that P/B multiples do not react merely to prevailing ROE levels but mainly to expectations about their sustainability, discounted to present value at the COE. That is why, even in years of fleeting improvements, if the market does not perceive a structural change in the ability to generate profits, valuations remain depressed. This conceptual framework provides the background for reopening the debate about excess capital. When a bank increases its stock of capital in the absence of an equivalent increase in profits, the impact is automatic ROE dilution (higher denominator).

For the P/B ratio not to suffer, this movement needs to be accompanied by a sufficient decrease in the COE (shaped by lower perceived risk, less volatile earnings or a lower probability of tail events) and/or an increase in the structural rate of growth. If the additional capital does not meaningfully produce either of those two effects, the discounted cash flows will trend lower, exerting downward pressure on the P/B multiple. The correlation between ROE, COE and P/B therefore expresses the logic underpinning value creation in the banking sector: the market does not attach a premium to capital per se but rather to the ability to turn that capital into profits that are sustainable in the long term.

Excess capital and impact on valuation

Considering the fact that, in practice, the majority of banks in the eurozone present higher levels of tier 1 (CET1) capital than they are required to under the prudential framework or by the supervisor, including all of their idiosyncratic requirements under the forward-looking and risk-adjusted SREP, the question is whether that additional, discretionary buffer is interpreted by the market as an efficient insurance policy (reduction of risk and the COE) or, to the contrary, as idle capital with a cost of opportunity (dilution of the ROE and compression of the ROE-COE spread).

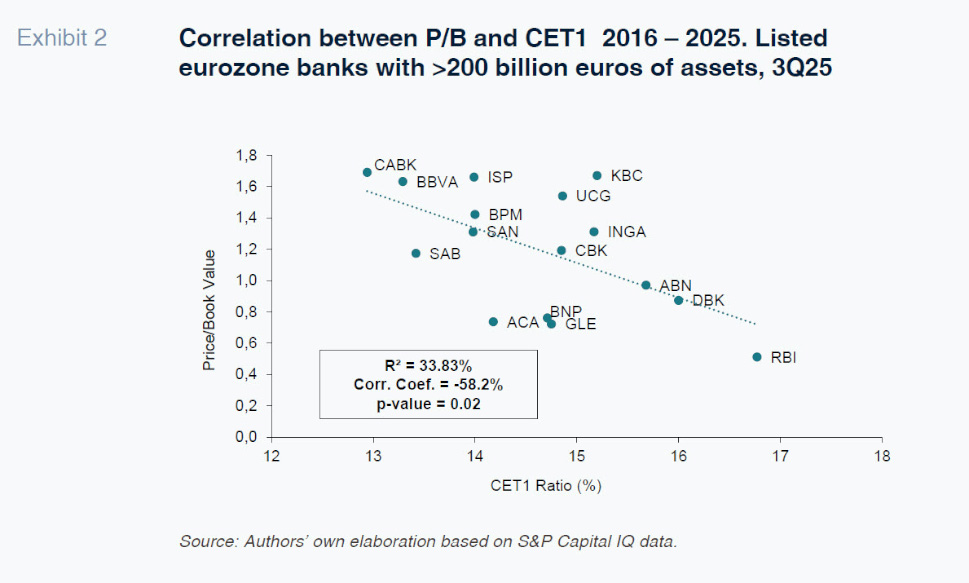

To explore this correlation empirically, we analysed a sample of the largest listed banks in the eurozone, including the 16 banking groups with over 200 billion euros of assets, which represent approximately 54% of bank assets in the eurozone.

In a first exercise (Exhibit 2), we correlate the valuation multiple (P/B) with tier 1 capital (CET1). Due to how it is constructed, this metric mixes three components: (a) the amount of capital needed to meet the banks’ minimum requirements; (b) the capital buffer kept by the banks out of precaution or strategically; and (c) differences in business model, asset composition and density of risk-weighted assets (RWA), implying that a given CET1 ratio is not comparable in terms of prudential buffer.

The results obtained, a negative correlation of -58% and R2 of 34%, suggest that the market, on average, associates a higher CET1 ratio with lower multiples. They also make it clear that the CET1 ratio on its own is an imperfect measure for explaining valuation as it does not distinguish between minimum required capital and excess capital.

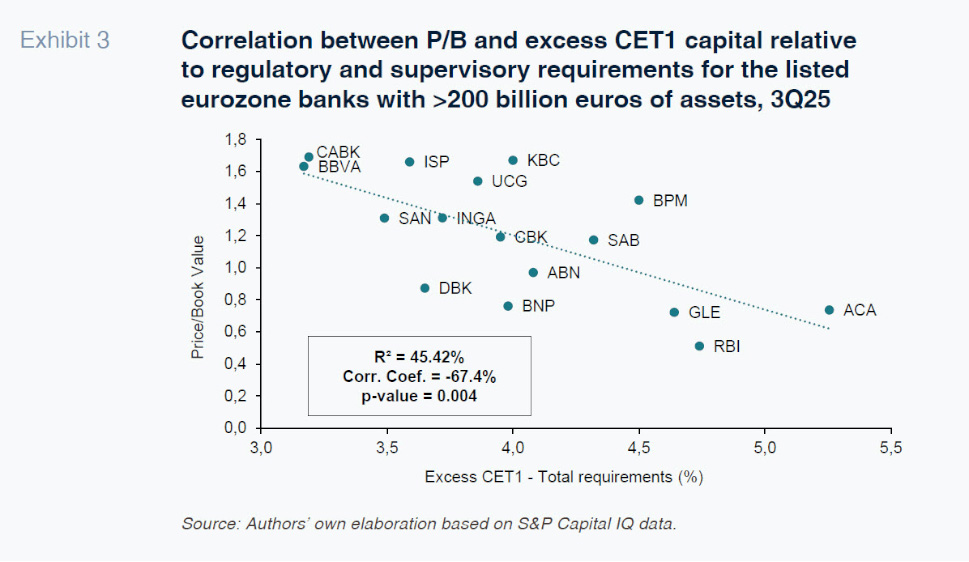

To do that, we look at an alternative correlation (Exhibit 3), relating the P/B multiple with surplus capital, measured as the difference between observed CET1 and the stack of minimum capital requirements, including the regulatory buffers (capital conservation, countercyclical, systemic risk), requirements for systemic importance (O-SII/G-SII), P2R and an estimation of P2G based on the results of the EBA’s stress tests

[1].

This time the correlation is much clearer: a negative correlation coefficient (-67%), an R2 of 45.4% and a p-value for the explanatory variable (excess capital) of 0.004; in statistics, the exogenous variable is considered to have explanatory power when its p-value is under 0.05. The model suggests that the market penalises excess capital more decisively than absolute capital levels. In other words, the signal that appears to matter more in bank valuations is not “how much CET1 you have”, but rather “how much CET1 are you holding in excess, after your SREP and different buffer requirements, than is reasonably prudential”.

This reading is consistent with the underlying rationale: if the supervisory threshold already incorporates a forward-looking assessment of risks (adverse scenarios, loss-absorbing capacity, idiosyncratic vulnerabilities), any additional capital may be interpreted by the market as redundant, unless it provides clear benefits in the form of a lower COE or more profitable growth. In the absence of that mitigation, the excess will tend to act as a “drag” on the return on equity and, by extension, on P/B.

Note, lastly, that the Spanish banks rank in the upper left-hand section of the exhibit, indicating a smaller capital excess, which is rewarded by the market. This outcome offers an alternative argument to the common interpretation that the Spanish banks are the least capitalised in Europe, a reading which should be made analysing excess capital relative to requirements rather than in terms of total capital. At the end of the day, assuming, after more than a decade in place, that the European supervisor has gained credibility with its forward-looking approach, it would not appear to make sense to hold substantially more capital than required by the supervisor, especially considering that the market does not reward that stance, indeed, it appears to penalise it.

Conclusions

The evidence obtained indicates that the more excess capital held relative to the effective prudential threshold, the greater the likelihood that we are talking about capital with an opportunity cost and, by extension, associated with lower valuation multiples. This finding is consistent with the theoretical framework outlined in this article: the market does not reward capital for mere accumulation but rather its ability to translate into sustainable profitability above the cost required by shareholders.

The most illustrative part of this exercise is not the sign of the correlation but rather how its explanatory power changes as the capital variable approaches the magnitude of real importance to investors: the amount of capital that exceeds (or otherwise) the relevant prudential threshold. This suggests that the market distinguishes between the capital needed to meet prudential requirements already configured through a forward-looking prism and additional capital that needs to be justified in terms of lower risk or higher future profitability.

This matter is particularly relevant because supervisors and investors do not analyse capital through the same lens. The former set their requirements based on forward-looking metrics that attempt to anticipate the ability to absorb losses throughout the economic cycle. The latter, on the other hand, assess additional capital in terms of its impact on value creation: whether or not it helps deliver a sustainable improvement in risk-adjusted profitability or reduce the cost of equity.

Ultimately, for the shareholder, a euro retained at a bank in the form of voluntary reserves only makes economic sense if it generates a higher return than it could earn by investing that euro in other assets with a comparable risk profile. If that additional capital does not improve the estimated ROE or considerably reduce the COE, financial logic dictates that it should be redistributed, in the form of dividends or repurchases, rather than remaining as idle capital on the balance sheet.

Moreover, this conclusion is particularly relevant against the backdrop of the current debate around regulatory simplification: if the aim is to make the capital stack more transparent and predictable, the notion of excess capital should be made more observable, leading to greater market discipline for banks and investors alike.

Notes

To estimate the P2G element, we followed the approach taken by the ECB, which classifies the banks into four capital guidance buckets depending on the level of capital depletion observed in the last round of bi-annual stress tests coordinated by the EBA.

Given that the supervisor does not publish the exact level of P2G capital assigned to each entity but does publish the level of capital depletion emanating from the stress tests, we used the mid-point of the P2G interval associated with each capital depletion category as our reference.

Ángel Berges, Jesús Morales and Ricardo Goizueta. Afi