Spain’s insurance sector: Underpinning market confidence in the broader financial system

The Spanish insurance industry continues to demonstrate financial strength, solvency, and stable profitability, acting as a buffer for the broader financial system. A conservative investment profile and steady income growth highlight the sector’s resilience even amid market volatility.

Abstract: Spain’s insurance sector remains one of the most robust segments of the financial system, combining sustained profitability with exceptionally strong solvency positions. Capital ratios comfortably exceed European averages, supported by prudent asset allocation and limited exposure to market risk. Premium growth continues across both life and non-life segments, with the latter showing particular dynamism driven by auto and health lines. While the low-interest rate legacy still constrains returns on older portfolios, higher yields are gradually improving investment income and supporting new product growth. The sector’s cautious risk management and focus on long-term stability have made it a key stabilizing force within Spain’s financial landscape, underpinning confidence among policyholders, regulators, and investors alike.

Introduction

The Spanish economy continued to perform well throughout the first half of 2025. Inflation has eased significantly, and interest rates have continued to decline, favouring consumption and investment and making the Spanish economy one of the most dynamic of the developed world. GDP growth remains at close to 3.0% with employment and domestic demand performing well in the context of a solid external surplus, shrinking public deficit and ongoing private sector deleveraging.

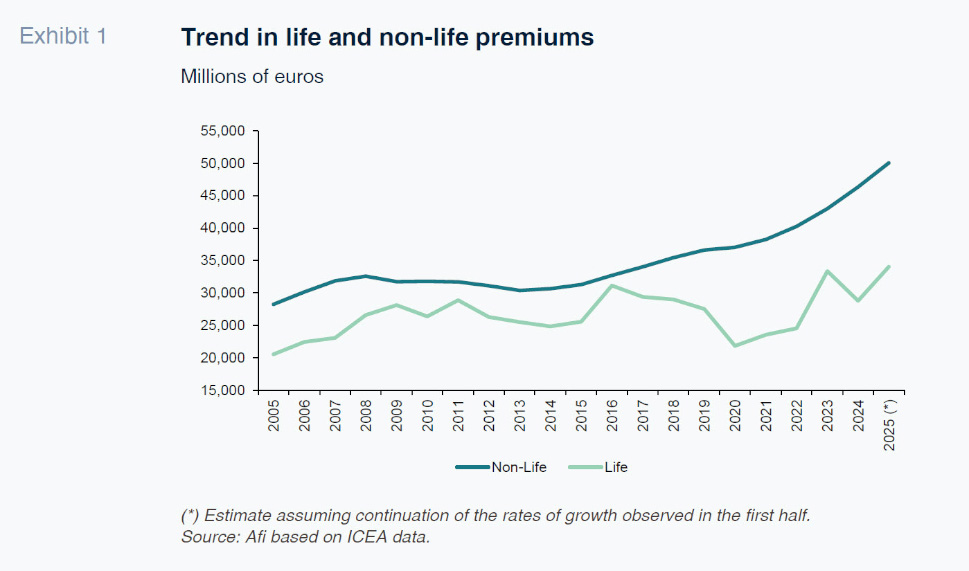

This environment has helped shore up household and business confidence, which has translated into stronger flows into insurance products, with growth still robust in the non-life business, particularly health and motor insurance. In parallel, the life insurance business has rebounded after premium revenues stabilised in 2024 in the wake of explosive growth in 2023 on the back of interest rates, which reached their highest levels in a long time that year. Although interest rates have stabilised at significantly lower levels so far in 2025, the success in curbing inflation and “normalising” the rate curve has been good for the long-term savings in which the insurance business specialises. In addition, despite geopolitical uncertainty, the debt and equity markets have also helped consolidate and expand the savings-life insurance business, as well as making a positive contribution to the insurance companies’ finance income. As a result, within Europe, Spain is currently one of the most dynamic insurance markets.

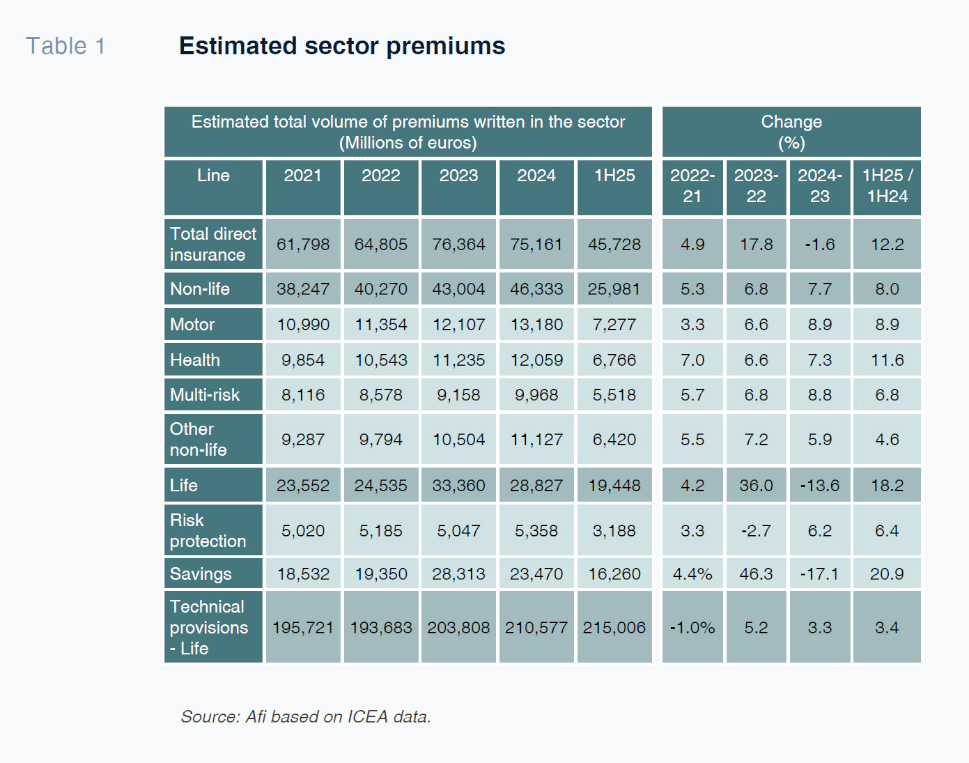

Total revenue from premiums amounted to 45.73 billion euros in the first half of 2025, marking double-digit year-on-year growth (+12.2%), which, if sustained, as is fairly likely, would put full-year premiums in Spain well above the 80-billion-euro-mark for the first time.

Rebound and transformation in the life insurance business

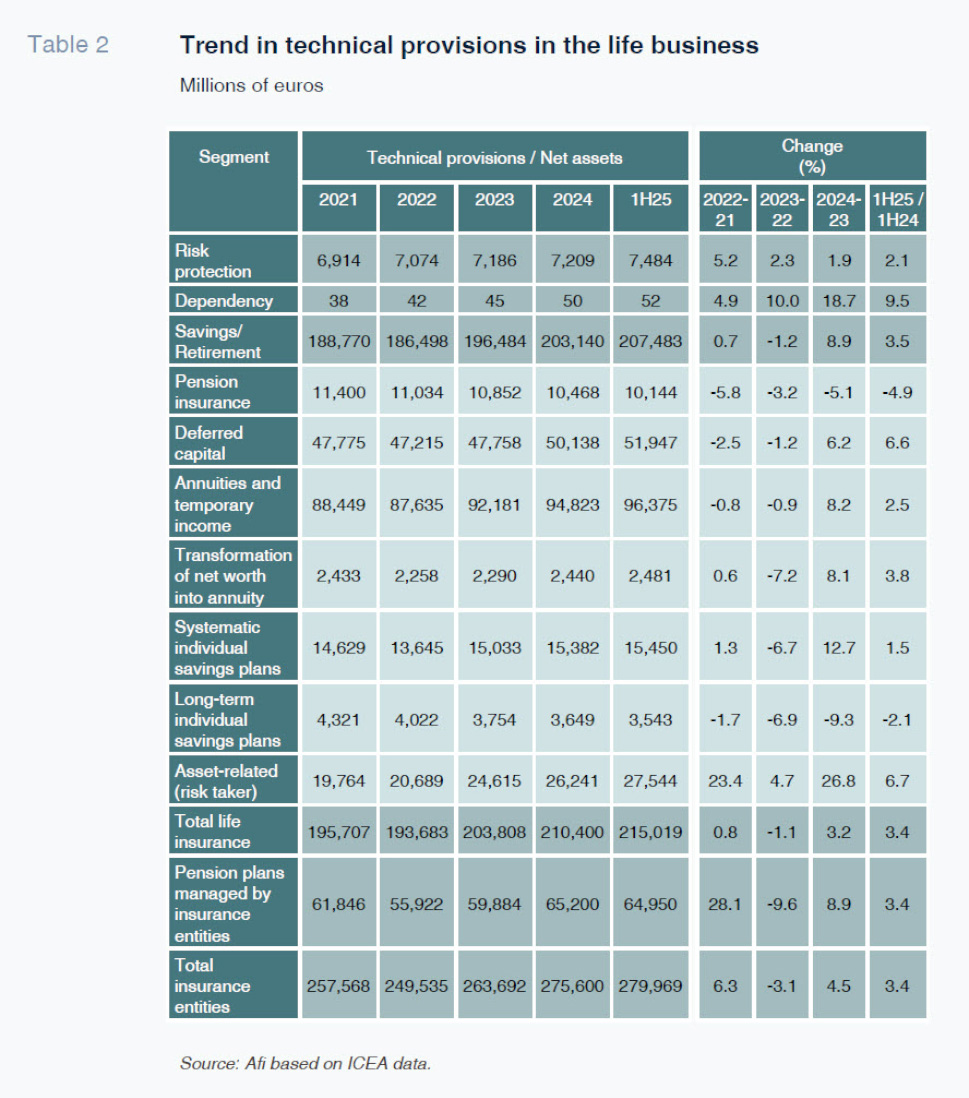

As was the case two years ago, when high interest rates fuelled the life business, this segment is again spearheading the growth in sector revenue (premiums), although in a different context, as already noted. Lower interest rates (albeit reasonable given the current context of low and controlled inflation) and a positive slope conducive for medium- and long-term savings, coupled with debt and equity markets, which, volatility notwithstanding, have trended higher and proven resilient, have made it easier for the insurance companies to once again attract household savings flows. That is certainly the case in savings-life insurance products, where the growth of 20.9% derives from a favourable environment for medium- and long-term investing given the current rate curve and reduced competition via bank deposits considering surplus bank liquidity. Moreover, unit-linked savings products, for which penetration is much lower in Spain than other parts of Europe, have extended the momentum of recent years so far in 2025. Life-risk insurance, meanwhile, also recorded growth of 6.4% in the first half. As a result, the life insurance business as a whole registered year-on-year growth in premiums of a remarkable 18.2% in the first six months of this year. That growth is materialising naturally in the technical provisions in the life segment, which are already above 215 billion euros, implying year-on-year growth of 3.4% and evidencing the stability and solidity of the business.

Continued strength in the non-life segment

As already noted, the life insurance revival is currently being accompanied by considerable growth in the non-life business. Its growth of 8%, which is even better than that recorded in 2024 despite the slowdown in inflation, is being underpinned by two factors. Firstly, economic momentum in Spain, as already referred to. Secondly, the repricing of premiums: in the current environment, the insurance companies have been able to pass price increases through to policyholders, particularly in the areas in which claims levels had eroded margins of late, specifically motor insurance. Higher premiums and growth in vehicle sales drove growth in revenue in that line of nearly 9% year-on-year in the first six months of 2025 (same rate as in 2024). Health insurance, meanwhile, is growing even faster, at 11.6%, proving that the extraordinary demand for this form of insurance remains intact. Its buoyancy, independent of the economic cycle, means that sooner or later this will become the most important area of the non-life insurance business, displacing motor insurance. The other two segments, multi-risk and other non-life, are growing at lower rates but are nevertheless outpacing nominal GDP growth.

Strong profitability supported by improved claims ratios

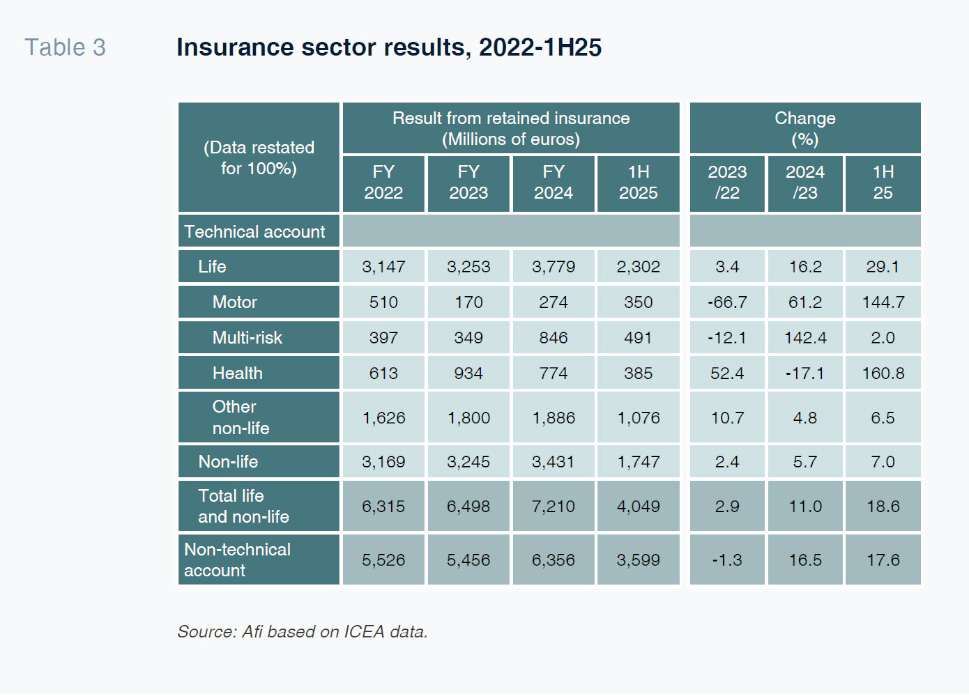

Thanks to the improvement in claims rates, which had eroded margins in some non-life segments, the widespread healthy performance in revenue from premiums in all lines in the first half translated into substantial earnings growth. Specifically, the insurance sector’s technical account amounted to 4.05 billion euros, growth of 18.6% from the first half of 2024. This performance was driven primarily by the improvement in profits in the non-life business (+29.1%) as a result, mainly, of earnings spillover from the motor insurance business. In the first half of 2025, profits in this line were already ahead of the figure for all of 2024 and double that of 2023. In the life insurance business, meanwhile, the technical account improved by 7%.

The combined performance of the life and non-life businesses translated into extraordinary profit levels in the first half of the year, with the technical account topping 4 billion euros and the non-technical account reaching 3.6 billion euros, foreshadowing a year of record earnings and higher profitability than in previous years, combined with solid and stable solvency across the sector as a whole.

Bancassurance as a cornerstone of the Spanish market

Another derivative of the insurance sector’s healthy performance is its positive impact on the banks’ financial statements. Recall that of the 172 insurance and reinsurance companies operating in Spain at the end of 2024, 29 of them (unchanged from the year before) were related to bank groups or entities. Of the 29, 15 operate in the life insurance business, making the banks the main channel for the distribution of life insurance in Spain (both savings and risk-life insurance). The remaining 14 operate in the non-life segment, in which, despite a minority presence, the banks have been showing growing interest in recent years. More significant than the number of banks comprising this bancassurance universe, however, is their share of the overall insurance business. Indeed, these 29 insurers with bank ties continue to account for around 50% of that business measured in terms of assets, technical provisions managed or earnings. The banks’ substantial role in the “control of the insurance business” in Spain is clearly concentrated in the life business, which is logical considering its significant financial component. In the life insurance segment, the banks’ insurance providers account for a little over 70% of total earnings. In the non-life segment, the insurers related to banking groups garner just over 25%.

Given the relevance of bancassurance, the healthy momentum in the broader insurance business will obviously translate into a bigger contribution to bank profitability this year. Definitely in absolute terms, but also maybe in relative terms this year. This would contrast with the last few years when the insurance business’s recurring contribution had been somewhat watered down by the extraordinary growth in banking business margins. Relative stabilisation in net interest margins this year, coupled with a fresh leap in earnings in the insurance business, will once again highlight the importance of the contribution by the latter.

Daniel Manzano. Partner at Afi