Fiscal progress despite budget stalemate: Spain’s deficit contracts amid political gridlock

Despite operating without a new budget for two consecutive years, Spain has made notable progress in fiscal consolidation. Strong tax revenue growth and a buoyant labour market have offset the political impasse, allowing the deficit and debt ratios to continue falling.

Abstract: Spain’s central government remains mired in budgetary paralysis, with the 2023 General State Budget still in force and no new draft budget likely to pass given the current political fragmentation. Nevertheless, fiscal performance in 2025 has been encouraging: as of August, the deficit fell by half a percentage point of GDP, driven by a 10% increase in tax revenue, outpacing nominal GDP growth. The improvement stems largely from favourable cyclical conditions, including strong job creation and the expiration of temporary tax relief. Looking ahead, AIReF and the Bank of Spain expect further fiscal consolidation in 2026, projecting deficits of 2.0%–2.3% and a debt ratio near 100% of GDP. However, underlying structural imbalances remain, and most of the deficit reduction has been cyclical rather than permanent. From 2027 onwards, Spain will likely face pressure to curb expenditure growth and introduce structural reforms to comply with new EU fiscal rules. Sustaining fiscal discipline amid political uncertainty will require difficult choices, particularly in defence, housing, and public investment.

Budgetary paralysis and economic dynamism

For the second year in a row, the central government is operating outside of the ordinary budget cycle. The public accounts continue to be guided, in essence, by the General State Budget (GSB) for 2023, which was approved by the Congress of Deputies on 24 November 2022. After two years of carryover and with no new draft on the table, the outlook for the 2026-GSB is not looking good. Although the ministerial order for kick-starting its preparation was published in September, [1] the process is very behind schedule. There are still no budget or debt stability targets or any reference rate for the spending rule for 2026-2028. And for the second year running, the required budgetary plan has yet to be presented.

It looks increasingly inevitable that 2026 will once again start with a new extension of the 2023-GSB. Moreover, the announcement by Junts per Catalunya at the end of October that it was withdrawing its support in Congress for the central government has made it even less likely that any draft budget for 2026 would ever get passed.

Extreme fragmentation in the Congress of Deputies is the main reason for the current stalemate, which is without precedent in the last 50 years. However, indeed, Spain is not the United States, and the absence of a budget does not bring the government to a standstill or impede all growth in spending, thanks to automatic updates and executive orders, among other mechanisms (Lago-Peñas, 2025). In the midst of all of this, thanks to a very favourable economic backdrop, the extraordinary growth in tax revenue has helped to bring about a significant reduction in the public deficit.

The rest of this paper is structured into three sections. The first examines the budget outturn so far in 2025 and the outlook for the rest of the year. It goes on to analyse the projections for 2026, with the final section taking a look at the medium-term budget framework.

Budget outturn in 2025

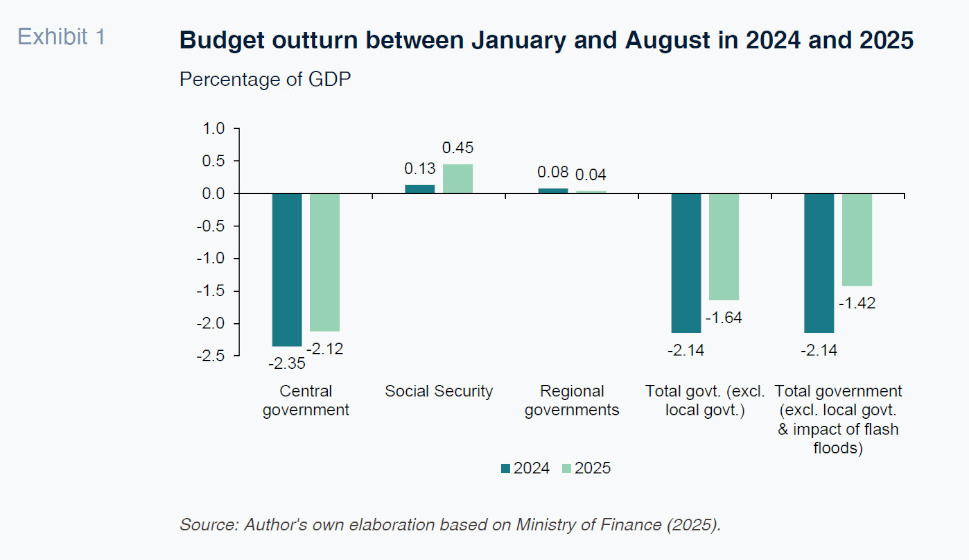

As of 31 August, the public deficit, at all levels of Spanish government except for the local governments, had decreased considerably year-on-year. In terms of gross domestic product (GDP), it had improved by half a percentage point. The advancement has been concentrated at the central government level, with the subcentral governments’ accounts deteriorating slightly: the surplus posted by the regional governments in the same period of last year has diminished by 0.04 points. The local governments, meanwhile, are expected (AIReF, 2025) to report a 0.1 point reduction in their surplus, from 0.4 to 0.3 points of GDP.

Tax revenue is the main factor driving this improvement, thanks to the strength of the labour market and economic momentum in general, as well as the full withdrawal of the energy and food tax relief introduced in 2021 and 2022 in response to the inflation shock (García Arenas, 2025). In the first nine months of the year, tax revenue in Spain increased by 10% year-on-year, which is significantly above the growth in the consumer price index (3%) and nominal GDP (5.7%). The growth has been particularly strong in personal income tax receipts, at 17.6%, and in tax on non-resident income, at 31.4%. VAT receipts are tracking 9.1% higher year-on-year, while revenue from corporate income tax is up 6.3%. Lastly, Social Security contributions are growing by 6.4% year-to-date.

In parallel, non-financial jobs increased by a substantial 5.3% year-on-year to August. In 2025, Spain will increase spending by more than the reference rate (+3.7%) for the trajectory in growth in net primary expenditure set down in its Medium-Term Fiscal-Structural Plan (MTFSP) for 2025-2028. However, that growth should be less than the increase in total non-financial revenue (+7.4%). In other words, although the budget carryover has not done much to slow growth in expenditure, tax revenue dynamics are unlocking fiscal consolidation anyway.

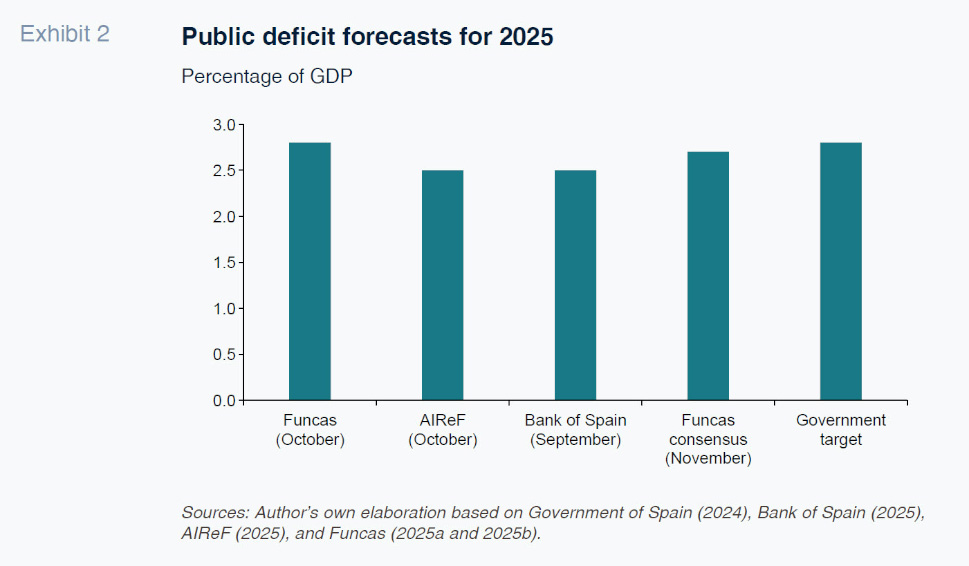

The outlook for the whole year is summarised in Exhibit 2. The Funcas consensus forecast of 2.7% and Funcas’ own estimates of 2.8% suggest the government will come in slightly below or at its target: 2.8%, or 2.5% excluding the impact on spending of the October 2024 flash flooding in Spain. AIReF and the Bank of Spain are expecting an even stronger performance: they are forecasting an overall deficit of 2.5%. Recall that in 2024, the deficit came in at 3.15%, or 2.8% adjusting for the impact of the floods. Lastly, the public debt ratio is expected to decrease by more than one percentage point according to the Bank of Spain and AIReF, to 100.7% according to the former and 100.3% according to the latter.

The snapshot is less encouraging if we focus on the structural component of Spain’s public deficit. According to the government calculations included in the 2025 Progress Report on the MTFSP 2025-2028, published in April (Government of Spain, 2025), the structural deficit estimated for 2025 is the same as the forecast observed deficit (2.8%), which would mark a year-on-year drop of just 0.1 point. In other words, while the total observed deficit is expected to decrease by between 0.4 and 0.7 percentage points year-on-year in 2025, at least three quarters of the improvement will be attributable to a very favourable economic backdrop, which is very unlikely to continue to help in this manner out to 2029.

Budget outlook for 2026

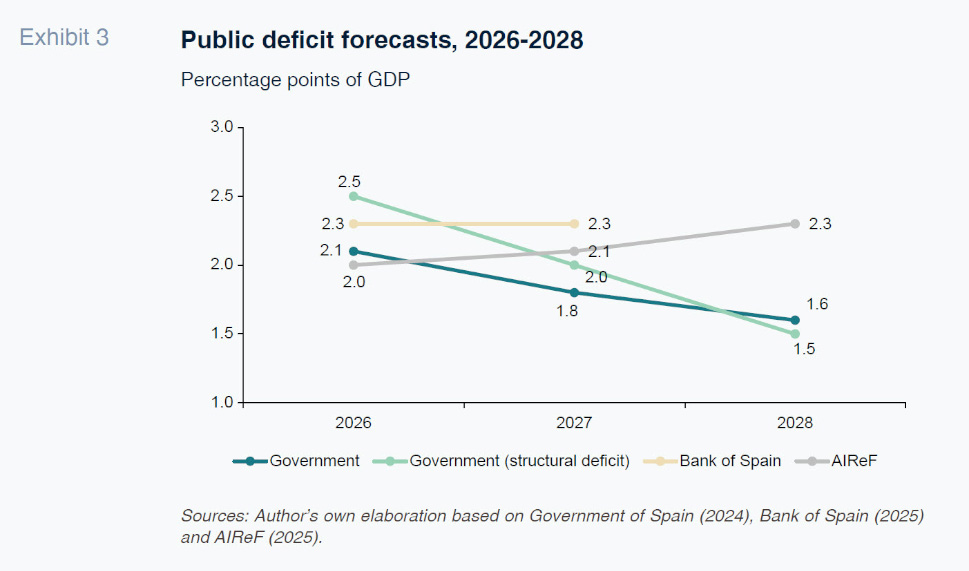

Despite the uncertainty around the fate of the 2026-GSB and the scarcity of official budget strategy documents in 2025, both AIReF (2025) and the Bank of Spain (2025) agree that the public deficit will come down further as a percentage of GDP in 2026 (Exhibit 3). The former is forecasting a reduction in the total deficit to 2% of GDP, while the central bank is estimating a deficit of 2.3%. The government’s target as per the MTFSP 2025-2028 falls in the middle (2.1%). [2]

Once again, public revenue dynamics will be the main factor behind the fresh improvement in the deficit, underpinned by a healthy job market and growth in household and corporate income, albeit slowing from 2025: the Bank of Spain is forecasting real GDP growth of 1.8%, AIReF is estimating 2.1%, the same figure as the latest Funcas consensus.

Public expenditure will come under pressure from the need to honour national defence commitments, a higher average cost of debt and population ageing. Assuming no policy changes and no official budget in 2026, the Bank of Spain estimates that net expenditure, calculated in accordance with the new fiscal rules, will increase by around 4% in 2026, while AIReF puts that figure at 4.6%. Both forecasts exceed the 3.5% benchmark included in the MTFSP 2025-2028 for 2026. However, the surplus that materialised in 2024 will allow Spain to continue to remain within the space provided by the cumulative control account introduced in conjunction with the European fiscal rule reforms. [3]

Lastly, AIReF is estimating a ratio of public debt to GDP of 99.1% in 2026, down from 100.3% in 2025, thanks to the growth in nominal GDP and forecast for a small primary surplus. In contrast, the Bank of Spain does not expect this ratio to drop below the 100% mark in 2026 (it is forecasting 100.4%).

Looking further ahead: Outlook for 2027 and 2028

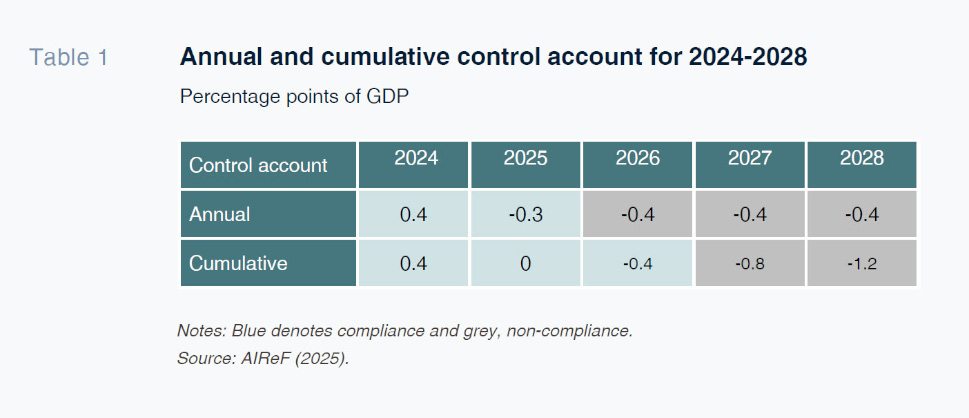

Looking to 2027 and beyond, AIReF believes that Spain will continue to breach the annual and cumulative spending growth limits, forcing it to make additional cuts in order to stay on the trajectory agreed with the European Union (Table 1). Specifically, it would have to make additional adjustments equivalent to at least 0.4 points of GDP between 2026 and 2028. Moreover, it is essential that national regulations be adapted for the new European rules in order to avoid inconsistencies. [4]

Without additional cuts, government debt will continue to come down in 2027 and 2028 but at a very slow pace. AIReF is forecasting a debt ratio of 97.8% in 2027 and 96.8% in 2028, while the Bank of Spain’s most recent projections put the ratio at 100% in 2027.

Beyond strict compliance with the fiscal rules, it is important to underline the additional benefits of keeping balanced and solid public accounts, which on their own warrant greater ambition when it comes to setting the national targets. For example, if the goal is to bring the structural and observed deficits below 1.5% of GDP within three years, Spain would require annual adjustments of close to 0.5 points between 2026 and 2028, which is equivalent to around 8 billion euros.

Proactive management of the fiscal consolidation process presents considerable economic policy challenges, exacerbated by the requirement to keep up a sustained effort over time and the emergence of new demands in the areas of national defence and housing, the need to finance investments in the energy transition and digitalisation, which from 2027 can no longer be funded via the Next Generation EU funds, and the growing burden of preparing for and responding to extreme events.

The selection of specific measures for adjusting and fine-tuning spending and revenue needs to be articulated around three essential pillars. Firstly, a full embrace of a culture of rigorous assessment of public expenditure so as to focus decision-making on the areas where savings are easier to achieve and less costly in social terms. The second pillar consists of tackling far-reaching reform of the Spanish tax system so as to bring about more efficient and equitable tax collection irrespective of the level of fiscal burden chosen by the government in power. The third is an educational mission: fostering an understanding of why healthy and balanced public finances are essential to preserve fiscal space in times of need, reduce the debt burden, and strengthen the country’s resilience in the face of any future sovereign debt crisis.

Notes

Ministerial Order HAC/974/2025, of 1 September 2025, issuing the rules for formulating the General State Budget for 2026.

Although the government’s projections were drawn up before the flash flooding of October 2024, the impact on spending will be marginal by 2026. Overall, the impact between 2024 and 2026 is estimated at 0.6 points of GDP, a little over 0.3 points in 2024, 0.2 points in 2025 and nearly 0.1 point next year.

The new expenditure rule requires that the growth in primary expenditure, net of discretionary revenue measures, must be aligned with the commitments assumed in the MTFSP, excluding certain expenditures such as interest payments and cyclical unemployment benefits. The growth is subject to specific limits: namely, the annual control account, which establishes a maximum permitted deviation with respect to the target agreed for each year of 0.3% of GDP; and the cumulative control account, which increases that room for manoeuvre to 0.6% of GDP over the overall adjustment timeframe. In practice, annual eligible expenditure is compared against the target, allowing for some flexibility in the event of unexpected shocks, while the cumulative control prevents countries from running up persistent deviations over several years. If, in a given year, a country exceeds the annual limit, the cumulative balance can be used to offset the annual deviation to the extent that limit is not exceeded as a result.

For example, the national rule is applied individually at each level of government (except for the Social Security), using difference reference rates and methodologies than the European equivalents, which sum up to the commitment assumed by the various levels of government as a whole and factor in non-recurring items and temporary revenue measures. This mismatch means that even if in some years, like 2025, compliance with the national rule guarantees compliance at the European level, from 2026 and particularly in 2027, the adjustment needed to comply with Spain’s European commitments would be higher than that required under national legislation.

References

AIREF. (2025).

Report on the projects and fundamental lines of the budgets of public administrations for 2026. 29 October 2025.

www.airef.esBANK OF SPAIN. (2025).

Macroeconomic projections and quarterly report on the Spanish economy. September 2025. 16 September 2025.

www.bde.esFUNCAS. (2025a).

Spanish economic forecasts for 2025-2027. 22 October 2025.

www.funcas.esFUNCAS. (2025b).

Spanish Economic Forecasts Panel. November 2025.

www.funcas.esGARCÍA-ARENAS, J. (2025).

Nota breve. Ejecución presupuestaria [Brief note. Budget outturn]. 15 September 2025.

www.caixabankresearch.comGOVERNMENT OF SPAIN. (2024).

Medium-Term Fiscal-Structural Plan (MTFSP) 2025-2028. Kingdom of Spain. 15 October 2024.

www.hacienda.gob.esGOVERNMENT OF SPAIN. (2025).

Annual progress report. 2025. Kingdom of Spain. 30 July 2025.

www.hacienda.gob.esLAGO PEÑAS, S. (2025).

Una prórroga que se dilata: sobre los efectos económicos de la inercia presupuestaria [Budget extension, again: The economic ramifications of budget rollover]. Instituto de Estudios Económicos.

https://www.ieemadrid.esMINISTRY OF FINANCE. (2025).

Ejecución presupuestaria de las Administraciones Públicas [Budget outturn figures] September. 31 October 2025.

www.hacienda.gob.es

Santiago Lago-Peñas. Professor of Applied Economics at Santiago de Compostela University and Senior Researcher at Funcas