What it would take to reverse Europe’s global decline

Europe’s lacklustre economic growth reflects deep-seated structural weaknesses, from fragmented financial markets to chronic underinvestment and low productivity. Without further fiscal and capital markets integration, the bloc remains exposed to external shocks and the risk of a managed decline.

Abstract [1]: Europe’s economic malaise is driven by structural weaknesses rather than short-term shocks. Germany’s reliance on traditional industries and Spain’s reliance on immigration-fuelled growth, albeit providing temporary relief, both highlight the EU’s failure to generate productivity. Overregulation, fragmented finance, and chronic underinvestment have left Europe lagging behind in high-tech sectors, while persistent trade surpluses have exposed the bloc to external shocks from Russia, China, and U.S. tariffs. Germany represents 24.5% of EU GDP, but its core industries are stagnating. Europe’s tech deficit is stark: of the 50 largest global firms, only four are European. Trade dependency is 22.4% of EU GDP, nearly double the U.S. share of 12.7%, leaving the bloc highly vulnerable to Trump’s tariffs—15% across EU exports, 50% on steel and aluminium—which triggered EU commitments of €600 bn in U.S. investment (2025–2028), $750 bn in energy imports, and $40 bn for AI chips. At the same time, Chinese exports to the EU rose 8.3% year-on-year in April 2025, while European firms struggle to sell to China. Without reform, fiscal and monetary tools alone cannot compensate. Only a fiscal and capital markets union can provide the scale of investment needed. Otherwise, Europe– including Spain – risks sliding into managed decline.

Introduction

There is an old joke about Boris Yeltsin that applies to the economic situation in Europe, and in Spain specifically. When asked by a reporter to summarise the situation of the Russian economy in one word, he said: “Good”. Clearly not expecting Yeltsin to comply with the one-word constraint, the reporter came back and said: “Ok, two words.” To which Yeltsin replied: “Not good”.

As absurd as this example sounds, it does apply to European countries. Germany is rich, but has low GDP growth. In Spain, there is a dichotomy between high GDP growth, but low productivity growth. If you looked at only one macroeconomic time series, chances are that you are missing the bigger picture. And if you only look at data, chances are that you have no explanation of why the economic situation has become so much worse everywhere in Europe. Most likely you would invoke the lame excuse of a string of bad luck events: the pandemic, Vladimir Putin’s war, and now Donald Trump’s tariffs. But the bad-luck story is becoming increasingly implausible. Wars and pandemics are dreadful, but there is no reason to think that they should have a persistently negative effect on your economic growth. Germany’s own economic miracle happened after the second world war. Our story is more complicated.

Germany is the canary in the coalmine. What happened there, will happen elsewhere in Europe with a delay. Germany’s decline is a result of several determining factors: a dependency on too few industries for economic growth (cars, mechanical engineering, and chemicals); a banking system geared towards supporting those industries, but not towards funding new companies and industries; a lack of investment in high tech industries specifically and a lack of financial and physical infrastructure that would encourage such investments. Germany was instrumental to get the EU to pass data protection legislation – the general directive of data protection and regulation on artificial intelligence – measures that effectively frustrate all data-based businesses. With GDPR, the EU gave itself the world’s most restrictive legislation on data protection. It passed its AI regulation before it had AI. The same occurred for crypto-currencies. As a result of excess regulation, an inflexible banking system, and the resulting under-investment the EU is not a primary participant in these industries. Of the fifty largest tech companies, only four are European. Except for Sweden’s Spotify, none of them have been founded from scratch this century.

Structural weaknesses and external shocks

The Germans may be extreme in their anti-tech crusade and their Luddite disposition. They still have fax machines in the public sector and in doctors’ offices. But this is a wider European problem. As Mario Draghi reminded us in his report on Europe’s competitiveness, virtually all of the productivity gap between the U.S. and the EU is accounted for by high-tech industries. In a speech in August 2025, he compared the small-scale high-tech investment in Europe, fragmented across member states, with investments in the U.S. and China that are more than ten times the scale. Europe lacks the infrastructure for this type of investment because of how we run our economy. If our existing companies do not produce economic growth, no one will. We do not have the financial and regulatory infrastructure for 21st century entrepreneurship.

To exclude high-tech from the productivity comparisons and to pretend that everything is fine would be dangerously complacent. It is true that the Americans are not more productive in the same industries in which they compete with the Europeans. The U.S. is rarely in the top group of global competitiveness rankings. But competitiveness is the wrong metric. And the rankings leave us Europeans with a false sense of achievement. Far more important are productivity and innovation – where we are lagging.

Europe’s weakness in tech is probably the biggest overt structural problem that holds us back, but behind this lies a whole number of structural policies that have caused and contributed to it. It goes to the heart of how we think about Europe, about our European socio-economic model, and our own distinct version of capitalism, sometimes also described as Rhenish capitalism.

The world around us has changed. China transformed from a consumer of European exports to an aggressive competitor in key technologies like electric batteries and cars, AI, and solar panels. This is quite possibly the most important of all the changes in our external environment. Donald Trump’s tariffs are another one. We cannot dismiss external shocks if they become permanent. Russia’s war in Ukraine necessitates higher defence spending in countries that are geographically close to Russia. I have sympathies for Spain’s critical view about Nato 5% defence spending target. It makes more sense for Poland and for Germany than for Spain and Italy, countries which should focus on economic reform at this point.

I think Trump’s tariffs will be permanent. Legal challenges might dent some of them, but the fact is that tariff revenues are becoming a critical part of U.S. fiscal policy going forward, even beyond the Trump presidency.

A decade ago, an article on the European economy would have focused on monetary and fiscal policy and on financial stability. They still play an important role in our story, but not the semi-exclusive role they once had. Fiscal and monetary policy are not in a position to offset these shocks. The fiscal expansion during the pandemic, helped by the suspension of the stability pact, managed to offset the direct shock. But the euro area did not revert to its previous growth path. Important as they are, fiscal and monetary policies cannot reverse a structural slump.

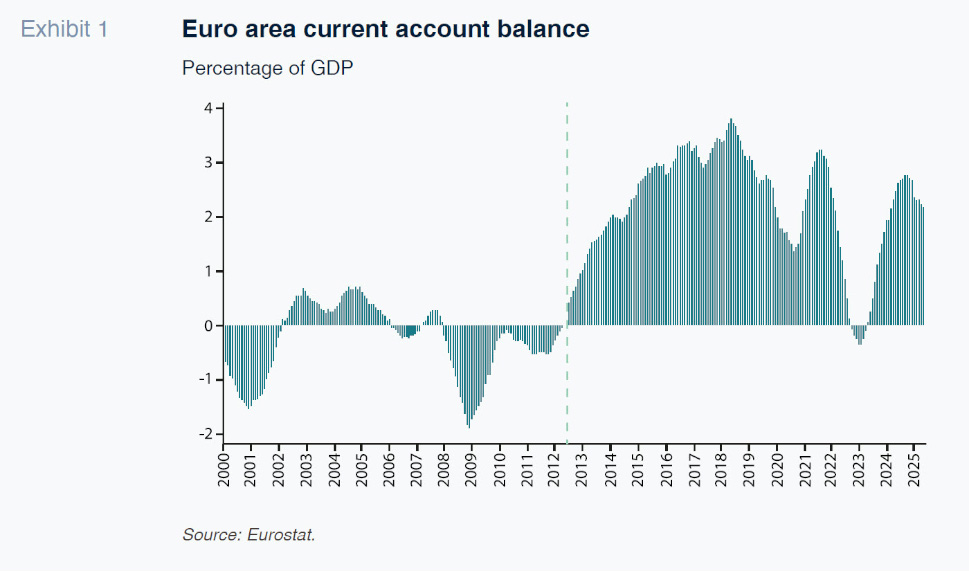

What macroeconomists should have foreseen, but did not, were the dire consequences of the euro area’s structural current account surpluses. Ever since the eurozone crisis, the euro area has been recording large and persistent surpluses against the rest of the world, as Exhibit 1 impressively demonstrates.

The break occurred in 2012 at the height of the eurozone’s sovereign debt crisis. Until then, the eurozone’s current account position was healthy. It fluctuated between small deficits and surpluses. But more important than their relative size was the lack of persistence. They went down and up and down again. This is how it should be. After 2012, the eurozone adopted synchronised austerity as a quid-pro-quo for Mario Draghi’s backstop, which from 2015 turned into asset purchases that were only stopped in 2023. The current account surpluses briefly fell during the pandemic as European companies struggled to export. But they came back soon afterwards.

In the last decade, it was customary for the German media to celebrate the large export surpluses. This was essentially a celebration of an imbalance. The problem with this imbalance is that it made Europe even more dependent on others – and that dependency has become the most important driver of Europe’s structural economic decline. The first shock was the Brexit referendum in the UK. The pandemic exposed supply chain vulnerabilities. Russia’s invasion of Ukraine exposed Europe’s dependency on Russian gas. The sanction policies against Russia ended up hurting a vulnerable Europe more than a nimble Russia. Within a year, Vladimir Putin transformed Russia into a war economy, and struck strategic deals with China, North Korea, India and Iran. What was left for Europe was our dependency on the United States, but with Donald Trump’s second term, that relationship too is now looking increasingly fragile. Trump has shifted the position of the U.S. in the Ukraine from that of Ukraine’s largest financial supporter to that of a neutral referee. Trump has imposed a 15% generalised tariff on all European exports, and 50% on steel and aluminium, and pro-rated on goods that contain those metals. The EU is committed to reducing its tariffs on U.S. products. I am hearing suggestions that the EU informally agreed not to apply its digital markets act against U.S. tech companies. The EU also agreed to step up their investments in the U.S. to €600bn until 2028. That translates to $170bn per year, on top of the $100bn EU companies are already investing each year. This is a huge increase, especially considering that Europe’s export surplus is likely to fall as a result of the tariffs. The U.S. trade deficit with the EU was $235.9 billion in 2024. The rationale behind these investments is to neutralise the surplus.

The EU also committed to purchasing of $750bn for liquid natural gas and nuclear energy products until 2028, roughly $200bn per year. This number compares to annual U.S. energy exports into the EU in the order of $80bn. The EU is also committed to investments of $40bn in AI chips from the U.S. for its data centres. There is no way the EU can fulfil all of these promises. It remains to be seen what Donald Trump will do once it becomes clear that the EU is not fulfilling its side of this Faustian bargain. But one way or the other, we can safely conclude that the era of Europe’s trade surpluses against the U.S. is well and truly over. Of the countries that absorbed Europe’s trade surpluses in the past, India is now the last one standing. But this is also not much of a consolation.

The UK maintained its deficit with the EU since Brexit, but it is no longer as closely integrated into industrial supply chains. Given the persistent weakness of the UK economy, it may not be in a position to uphold its moderately large trade external deficit of 2.6% of GDP in 2024. And in the long run, it would be reasonable to expect the UK to diversity its trade away from the EU. For example, by relaxing its tariffs and import restrictions for U.S. agricultural products, we should expect to see rising imports from the U.S. into the UK, to the detriment of European competitors.

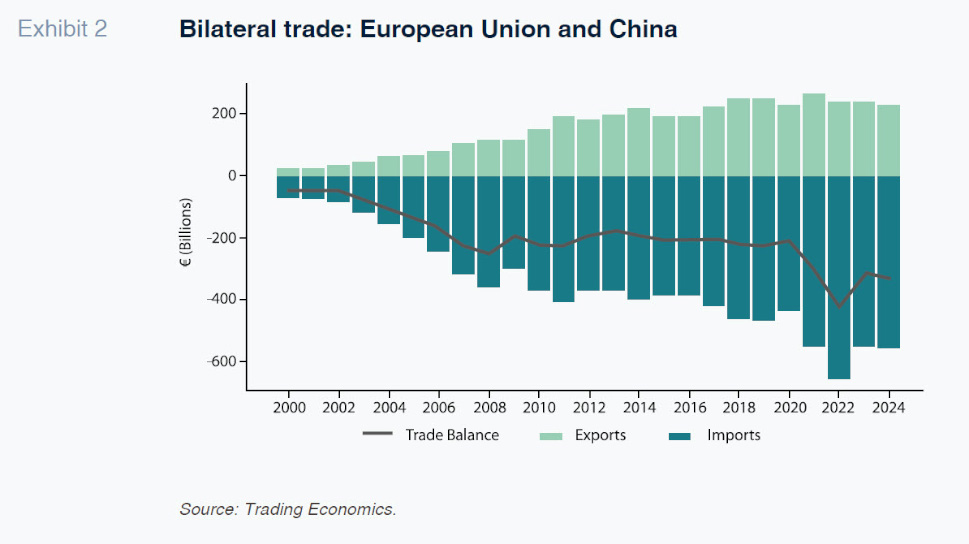

China has been running bilateral trade surplus against the EU throughout this century. But it was only since 2007/2008 that that these surpluses have became very large.

There are indications of a second China shock underway that is not yet reflected in the above exhibit. After Donald Trump announced his “Liberation Day” tariffs on April 2, China diverted trade into the EU. According to Chinese customs data, China registered an 8.3% increase in export growth to the EU, year-on-year, in April, with figures of 4.8%, 5.8% and 7.2% for the subsequent months. Chinese imports from the EU were down by 5.6% in January/February 2025 compared with the year earlier. Anecdotal evidence suggests that European companies, especially car companies, are struggling to sell to China.

I am devoting so much time to the external side because it is the change of external environment that drives our economic performance. Europe is far more dependent on the rest of the world by comparison to the US. Measured against GDP, total trade only accounts for 12.7% in the US, but 22.4% in the EU. These numbers exclude intra-EU trade.

[2]

Apart from our external dependencies, which are expressed in those data above, the EU has also some internal dependencies that we need to take account of. Poland and other Central and Eastern European countries are heavily dependent on Germany industry, as supply chain providers. Spain’s SEAT is part of the Volkswagen group as is Skoda of the Czech Republic. Germany’s role as the EU’s industrial hub makes the rest of Europe more dependent on the German economy than what would be warranted given Germany’s relative size in the EU’s GDP of about 24.5%.

This dual dependency, EU on Germany, and Germany on the U.S. and China, has the potential to produce a domino effect against which economic activity and economic policy takes place.

As a policy consequence, the EU should reduce one-sided economic dependencies on the rest of the world. These shifts would require more than just simple tweaks to existing policies, but a reboot of how the EU works, and how economic policy making works. The investments needed both in the private and the public sector exceed what the public sector and the financial sector can stem. Don’t blame the banks. It is not their job to fund risky private ventures. The European Commission does not have the budget for multi-billion investment projects. Just look at the recovery fund. Praised by many as Europe’s Hamiltonian moment, it was another too-little-too-late type investment projects. As the EU debt is funded by future membership contributions, it constitutes an intra-governmental transfer, which limits its political appeal amongst net contributors to the EU budget. It is unsurprising that northern European resist it.

The case for deeper integration

I have concluded a while ago that Europe’s economic problems are insolvable without the creation of a fully-fledged fiscal union, one that operates independently of the member states. It is the combination of fiscal union, combined with limited tax raising powers, and a proper capital markets union that can leverage the investments that are needed. Both are also required for the euro to be able to challenge the dollar. Economists wasted far too much time drawing up clever plans for hybrid eurobonds.

Investors can tell the difference between sovereign debt and exceedingly complex financial structures, where nobody knows who owes what to whom. If the goal is to catch up with the U.S. and China in 21st century technology and to assert Europe’s economic power globally, the creation of a fiscal union is without alternative.

While everybody, without exception, would benefit from such a construction in the long-run, perceptions might vary about the short-term. The Germans would naturally fear that the EU would raise too much debt. Spain might delude itself into thinking that its currently strong economic performance would continue forever, and that changes to the EU’s way of working are not needed. Italy and Germany would not want to agree to a capital markets union as part of which they would lose control over their banking system. Who else, but the Italian banks, would want to hold Italian sovereign debt at current unattractive rates? If the euro crisis were to come, there would be no national banks left to act as a shock absorber for governments. I see this as a feature of a European fiscal union, not a bug.

I am not denying that there would be lots of losers. The road towards new investments, and towards resilience goes through Schumpeterian creative destruction. In this new world, underperforming companies will go out of business – even if it is the car industry. That is not the case today.

I have been participating in “What Europe Must Do” type debates for several decades. With the introduction of the euro, the EU reduced its ambitions for political union. Without it, I don’t think there is a solution that could get the job done. Investment plans are not about newspaper headlines. The EU is very good at generating positive headlines, but all its investment initiatives have ultimately failed. The €300bn Juncker investment fund was a smoke-and-mirror magic trick when it was launched in 2014. It did not raise any new investments. The €300 billion grants from the recovery fund at least were real money. But it took five years for EU countries to spend only half of it. There are also no demonstrable signs that it raised productivity growth. Instead, the EU ended up harming the economy by passing restrictive regulations through its bureaucratic Green Deal, and its anti-tech crusade. If there is no willingness to move towards a fiscal and capital markets union, one that does not try to out-regulate the rest of the world, there is not much we can do except manage our decline.

For now, Spain is fortune in that it can generate GDP growth, but this is due mainly through immigration. Spain is lucky in that many immigrants speak Spanish. The Germans and the Dutch do not enjoy that privilege. I am all in favour of high-skilled immigration, but economies cannot grow sustainably based on immigration alone. We know that politics intrudes. Productivity growth is a critical metric for the underlying dynamics, and on this metric Spain is no better than the rest.

This is why we are having a collective action problem. I have been advocating for European political and fiscal union throughout my journalistic career, which began in the mid-1980s. I fear that this is a battle my co-conspirators and I are losing.

Notes

Most recently, Münchau authored Kaput: The Decline of the German Economy, published

by Swift Press in 2024. For the Spanish version of the article, please see Kaput, El Fin Del Milagro Alemán, Plataforma Editorial, 2025.

Wolfgang Münchau. Director of Eurointelligence Ltd.