The blow to tourism and the recovery of the Spanish economy

With the tourism sector having accounted for 12.3% of GDP and 12.7% of employment in 2018, the paralysis of international travel has dealt a hard blow to the Spanish economy. Although both state and EU-level support have been mitigating factors, it is unlikely that the tourism sector will rebound quickly, with adverse consequences for Spanish GDP growth and the current account balance.

Abstract: COVID-19 resulted in a sudden interruption in global tourism after years of sustained growth. In Spain, the tourism sector accounted for 12.3% of GDP and 12.7% of employment in 2018. Both the European Commission and Spanish government have unveiled plans to support the tourism sector. Taking into account the furlough scheme and business stoppage benefits, the state guarantee lines, and the deferral of taxes, the government estimates it has earmarked 19.54 billion euros to the tourism sector. Nevertheless, some sector representatives have argued that these funds are moderate in size compared with the losses the sector faces in 2020. Specifically, tourism export receipts could fall to around 33.6 billion euros, representing more than a 50% decline from 2019. While a diversion of residents’ expenditure abroad could cushion the pandemic’s impact on the tourism sector’s GDP and on the balance of payments in 2020, the forecast for 2021 is less optimistic. As oil prices rebound and a rise in internal demand leads to an increase in imports, the strong current account dynamics observed since 2013 may weaken.

Introduction

The COVID-19 pandemic is an unprecedented shock that morphed into an economic crisis. While a recovery will eventually follow, it is difficult to forecast and bound to be uneven across various sectors and countries. Both the scale of the initial loss of activity and the ongoing disruption in supply and demand depend on the risk of contagion. Of all sectors, tourism has taken one of the hardest hits due to its dependence on air travel, activities that involve contact with large groups (restaurants, museums, bars, clubs, beaches), and the risk that tourists could be left stranded and therefore dependent on a foreign healthcare system.

As of May 7th, the World Tourism Organisation calculated that international tourist arrivals could fall by between 60% and 80% worldwide in 2020 compared to 2019, implying a loss of export receipts equivalent to between 910 billion and 1.2 trillion euros. In Spain, the tourism sector accounted for 12.3% of GDP and 12.7% of employment in 2018, according to the National Statistics Office’s satellite accounts; 54% is foreign tourism. The share of GDP includes the direct effect (6.4% in 2017) and the indirect effects on other sectors. In 2019, the trade surplus in tourism amounted to 46 billion euros, making it a core component of the current account surplus the Spanish economy has reported since the last crisis.

The second quarter of 2020 will be marked by a virtual standstill in foreign tourist arrivals, as foreshadowed in the visitor and expenditure figures for April. The first tourists began to return on June 21st and although bookings indicate signs of an uptick in interest from several of Spain’s core markets, business volumes are set to be far from normal all summer long. To alleviate the economic and social costs of this situation, the sectors and authorities have been taking action on several fronts. In May, the European Commission unveiled a package of guidelines for the coordinated reopening of its borders (albeit a competency delegated to member states) and the resumption of tourism within the European Union. The Spanish government has presented a plan for supporting the sector and the regional and local governments are working to facilitate the return of foreign tourists. While less sector-specific in scope, the Recovery Plan presented by the European Commission on May 27th includes the tourism sector as one of the recipients of the funds.

An unprecedented blow after an extraordinary cycle

The sudden interruption in global tourism comes after years of sustained growth. International mobility had reached historical levels before the pandemic. Recent estimates (Recchi, Deutschemann and Vespe, 2019) point to nearly 3 billion cross-border movements in 2016. Tourism represents an overwhelmingly high percentage of these movements.

Spain has managed to retain its status as one of the most popular tourist destinations in the world, thereby benefitting from this growth cycle. In 2019, Spain welcomed 83.7 million tourists (78.1% of whom were European) who spent 91.33 billion euros. As shown in Exhibit 1, despite the slowdown observed in 2017, both tourist arrivals and export receipts were extremely strong in the run-up to the pandemic.

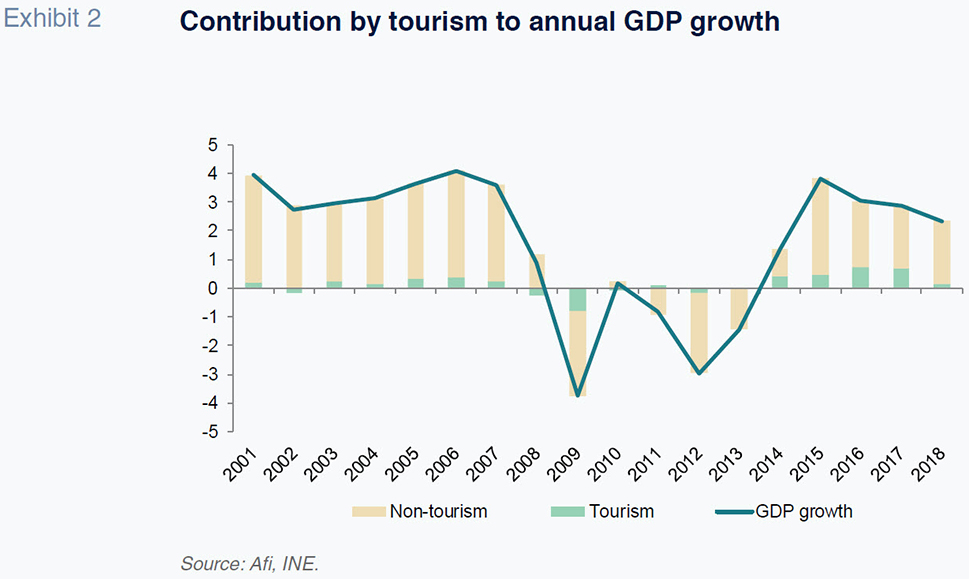

The strength of the tourism cycle is also evident in its contribution to growth in GDP (Exhibit 2), averaging 0.5 percentage points between 2014 and 2019. Indeed, tourism GDP increased from 118.12 billion euros in current 2015 prices to 147.95 billion euros in 2018. In constant terms, it registered growth of 18% in just three years, lifting its weight in GDP by 1.3 percentage points. An analysis of average GDP growth in Spain by region reveals that the regions with the strongest growth (the strongest being the Balearic Islands with average real growth of 3.2%) are those with the highest incidences of tourism.

Although the nature of the pandemic means that it should prove a temporary negative shock, this is unlikely to be the case for the tourism sector. Not only is the sector expected to take longer to recover to 2019 levels, the crisis is also likely to drive structural changes in demand for tourism services. The perceived risk of transmission could deter foreign tourists, stimulate tourism nearer to home and drive travellers away from more crowded environments. Although recovery came relatively swiftly after crises of confidence in the past (such as the 9/11 attacks), on this occasion it is highly likely that it will take longer for tourist mobility to reach pre-pandemic levels.

The cost in terms of jobs will unquestionably be considerable and will force relocation to other activities (construction, national tourism, logistics service and last-mile delivery). The sector’s gross operating surplus (including gross mixed income) is also set to contract sharply in 2020; nevertheless, the drop in the return on capital will come after years of strong growth, so that the companies that remain viable should be able to withstand the blow.

In sum, the challenge facing the sector is to withstand the shock, find a path towards sustained gradual recovery, preserve Spain’s competitive position relative to other destinations and make an effort to adapt, renew and boost the quality of what Spanish tourism has to offer.

Public measures designed to facilitate the transition

The tourism sector has been one of the most active sectors in tapping the furlough and state-backed loan guarantee schemes rolled out by European governments to mitigate the impact of the pandemic. According to the data presented by the Spanish government, the state guarantee scheme has supported the provision of over 10.5 billion euros of financing to nearly 83,000 companies from the tourism, leisure and culture sector, in addition to the 400 million euro Thomas Cook line (which was reallocated to mitigate the consequences of the pandemic). In parallel, 147,000 sector companies have used the furlough scheme for 948,000 employees, while the scheme providing compensation for the temporary closure of activities has benefitted 260,000 self-employed professionals.

On May 13th, the European Commission unveiled a support package for the tourism and transport sector articulated around the following key initiatives:

- A coordinated approach for lifting the restrictions on free movement within the EU.

- A coordinated approach in support of the gradual and safe renewal of transport for passengers and workers.

- A recommendation on vouchers as an attractive alternative to reimbursement for flight cancellations. Customers must expressly accept a voucher instead of reimbursement; vouchers should be protected against carrier insolvency; and vouchers should be refundable if not redeemed within one year of issuance.

- Common criteria and principles for the safe and progressive resumption of tourism services, including specific safety protocols for hospitality establishments.

In the Recovery Plan presented on May 27th, the European Commission estimated losses for the sector of between 171 and 285 billion euros, equivalent to 26.4% of total estimated losses attributable to the pandemic. The Commission estimates that the tourism sector requires investment of 161 billion euros. The European Recovery Plan, a coordinated investment plan to be financed through the issuance of joint debt, will focus on the digitalisation and sustainability of the tourism sector. However, the sector can also benefit from several of the tools contemplated prior to the Recovery Plan which will be earmarked to the regions and sectors hit hardest by the pandemic. Both the increased use of digital technology and progress on the sustainability front represent drivers for enhancing the quality of tourism services.

On June 18th, the Spanish government presented its programme, dubbed Plan for Boosting the Tourism Sector: Towards a Safe and Sustainable Sector, which comprises 28 measures endowed with 4.26 billion euros of funding articulated around five initiatives:

- Restoring confidence in Spain as a destination: Embracing health safety as the priority, the plan formulates 21 specific recommendations for the prevention of transmission, which will be formalised as UNE and ISO specifications and standards. Compliance with the standards will be distinguished with a safe tourism seal.

- Measures for reactivating the sector: On the job front, the most important measure relates to the Terms for the force majeure extension of the furlough scheme from June 30th, which will facilitate a gradual return to work at tourist service providers. The plan also contemplates measures for facilitating training and the acquisition of new skills to prepare employees to provide more specific services. To maintain the flow of financial support, a preferential sub-tranche of 2.5 billion euros has been set aside within the state guarantee scheme for tourism businesses. Lastly, the government will launch a mechanism that enables self-employed professionals and businesses with mortgages secured by assets used in tourism activities to obtain a moratorium on principal repayments for up to 12 months.

- Improving Spain’s competitiveness as a tourist destination: This section includes a raft of measures, mostly in the form of loans on advantageous terms, for financing investments in sustainability and digitalisation, including investments aimed at advancing towards smart tourism destinations.

- Boosting tourism sector knowledge and intelligence: The goal here is to improve the quantity and quality of data tracking trends in sector demand, with an emphasis on key issuer markets and domestic tourism.

- Marketing and publicity.

Taking into account the furlough scheme and business stoppage benefits, the state guarantee lines, and the deferral of taxes, the government estimates it has earmarked 19.54 billion euros to the tourism sector. Nevertheless, some sector representatives have argued that these funds are moderate in size compared with the losses the sector faces in 2020. However, it is important to highlight that the goal of public intervention is not to compensate for or reduce losses but rather to mitigate to the extent possible the impact on jobs; create the health, safety and logistical conditions needed to restore foreign tourists’ confidence in Spain; and, facilitate adaptation to an environment set to remain challenging for many months to come. Beyond these short-term objectives, the sector support policies need to be framed by a vision for boosting and transforming the quality of the services offered in Spain. The plan unveiled by the government should constitute a first step in articulating a national strategy that relies on public-private sector coordination and supports invesments in high qualiy tourst services that are safe, sustainable, and technologically advanced.

Sector prospects

The outlook for the rest of 2020 and 2021 remains shrouded by uncertainty. Any significant setback in combatting COVID-19 would further erode confidence and thus prove very costly. If setbacks are avoided, the sector will begin to recover. However, it will take time to return to pre-crisis levels. The following estimates, built from foreign tourist arrival estimates in order to arrive at estimates for revenue and tourism GDP, depict a baseline scenario with a lower than normal probability of materialisation.

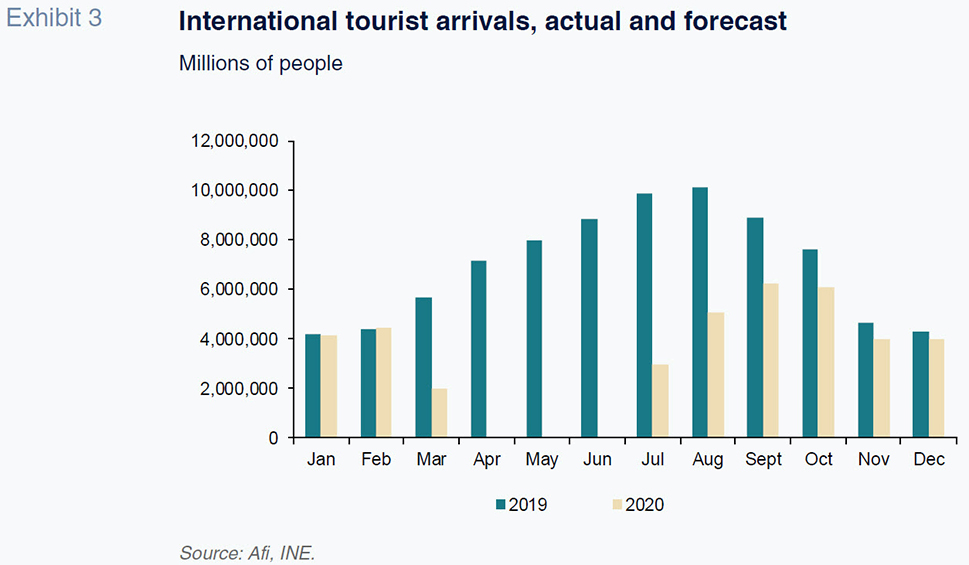

The 64% drop in foreign visitors in March was followed by zero arrivals in April, activity levels that will likely be seen in May and June data (despite partial reopening towards the end of the month) as well. Compared to 2019, this washout quarter implies a loss of income (in balance of payment terms) of 22 billion euros. In the third quarter, we assume international visitor arrivals could reach 50% of 2019 levels, with incremental increases expected based on current bookings. For the fourth quarter, we assume that international arrivals will return to 80% of last year’s numbers.

There is a direct correlation between tourism receipts and the international visitor arrivals and in turn between tourism receipts in real terms (deflated) and tourism GDP, so that we can get a clear idea of the damage this pandemic will leave in its trail.

Historically, the relationship between growth in tourism revenue and tourist arrivals has not been one to one. That is because of the various factors that affect tourist expenditure: average stays, average daily spending and tourists’ geographic distribution. As a result, an increase of 2% in visitors implies a smaller percentage increase in revenue. However, that correlation is likely to be affected by the current situation. We expect the relationship to be close to one to one in the wake of the drastic collapse in business volumes. This is borne out if we look at the international arrival figures for the first quarter of the year. In March visitors fell by 25% (three-month average), with revenue dropping in tandem (-23%).

The loss of visitors will therefore trigger a drastic reduction in tourism export receipts, which could fall to less than half of the 71.24 billion euros of revenue reported from tourism in the balance of payments accounts in 2019. In 2020, we estimate receipts of around 33.6 billion euros. The impact on the balance of payments will therefore be of an unparalleled magnitude and will hit tourism GDP heavily.

Some of the foreign visitors lost could be offset by domestic tourism. Faced with the new restrictiosn, lower incomes, and health concerns, families may decide to switch destination and stay in Spain, particularly for most of the high season. Domestic tourism in Spain, according to the Resident Tourism Survey, accounted for over 48 billion euros of expenditure in 2019, the third quarter being the most important, representing 40% of annual expenditure. In contrast, Spaniards spent 16 billion euros abroad. However there are a number of issues that may limit the extent to which domestic tourism offsets the drop in foreign visitors:

- The magnitude of the figures involved (14.2 million domestic tourists forecast between July and September versus 28.9 million in 2019),

- Most of the travel undertaken by Spanish residents between July and September is already domestic tourism (> 85%), such that the scope for the diversion of tourists is limited; and,

- Average daily expenditure by domestic tourists is 70% below that of foreign visitors (ETR and Egatur).

As a result, it is hard to imagine domestic tourism making up for the loss of foreign visitors. However, diversion of resident expenditure abroad (in 3Q2020) could cushion the pandemic’s impact on the tourism sector’s GDP and on the balance of payments (expenditure by Spanish tourists abroad is accounted for within foreign payments).

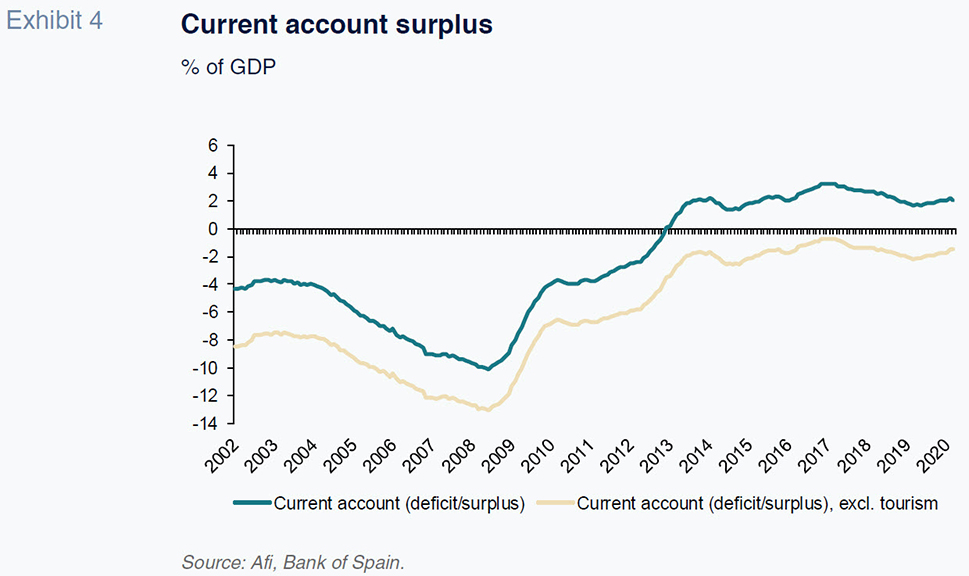

Looking only at factors related with the tourism sector, the effect on the current account will be negative. Specifically, the loss is estimated at around 25 billion euros,

[1] which would leave the surplus at around 21 billion euros, compared to 46 billion euros in 2019. This represents a reduction of just under two percentage points of GDP.

However, the impact will be partially offset by the reduction in oil consumption. We estimate savings of 10 billion euros in 2020 thanks to the correction in oil prices alone. That figure is set to be higher as a result of the sharp drop in intermediate and end demand. As a result, it is conceivable that the current account surplus will not be eroded this year on account of various offsetting forces.

In contrast, 2021 looks less promising in terms of the current account as the recovery in internal demand is likely to fuel imports and, if expectations for a global rebound materialise, oil prices may rise, too. Additionally, any structural damage due to the pandemic will likely affect social dynamics the hardest and, by extension, sectors such as hospitality and eateries. Under these circumstances, the tourism sector is unlikely to fully recover (meaning a return to 2019 business volumes) while the shadow of a new outbreak lingers. As a result, the new current account dynamics observed since 2013, marked by strong surpluses that can almost be described as structural, could disappear.

The effect on tourism GDP will be severe. Given that foreign tourism accounts for half of the sector’s activity, using income indicators as our benchmark, the net loss would be equivalent to the estimated decline in the tourism current account surplus (25 billion euros), which is just short of 20% of tourism GDP. This approach assumes that the portion of Spanish residents that cease to import tourist services will switch to the home market. However, we believe this is an overly optimistic hypothesis as some of that income will be channelled into savings. As a result, it is likely that the effects of the shock on tourism GDP will be higher, possibly close to 25%.

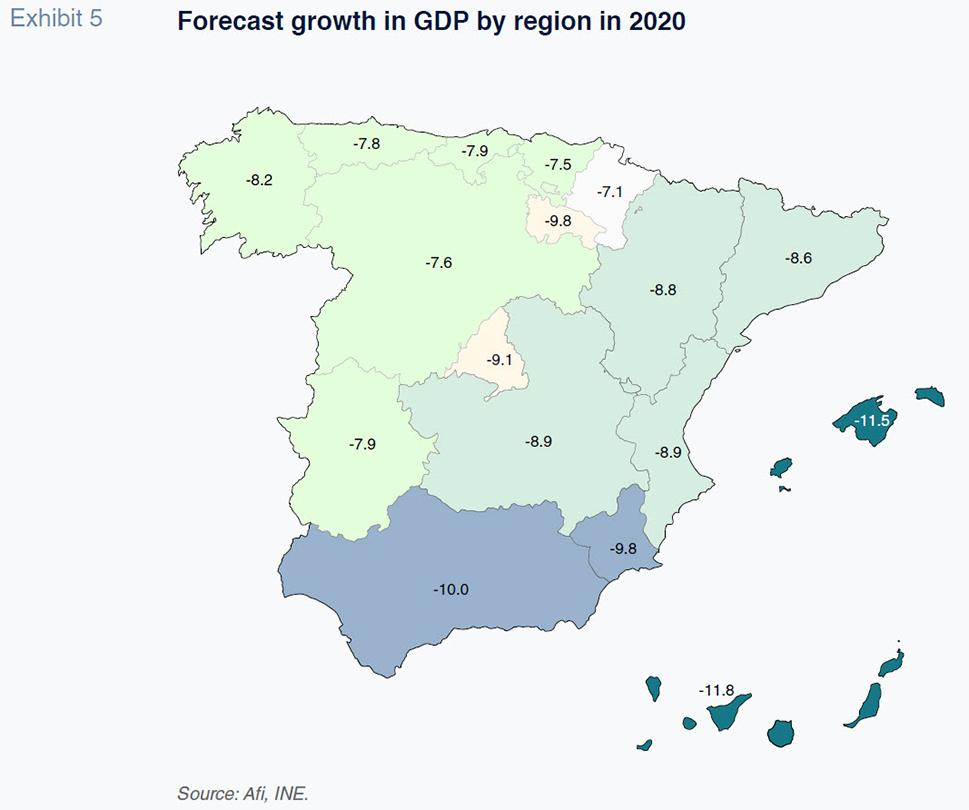

That prospect has a direct impact on the forecasts for regional growth in Spain in 2020. The regions most exposed to tourism, namely the Balearic and Canary Islands, in which tourism GDP and employment account for over 30% of the totals, stand to see their growth contract by as much as four percentage points more than the least exposed regions. The differences in economic structure will therefore determine the intensity of the GDP contraction.

Conclusion

Of the unprecedented contraction forecast for Spanish GDP in 2020, between 2 and 2.5 percentage points may be due to a decline in tourism. Over the short-term, the key concern should be to stem the loss of jobs by facilitating the gradual rehiring of employees under the furlough scheme and the sector and geographical mobility of those who do lose their jobs. Taking a longer-term perspective –acknowledging that it is impossible to tell how the pandemic will affect trends in international mobility– it is important to take advantage of the slump in demand to invest with the aim of pushing Spain out along the digitalisation and sustainability curves to put it in a better position to offer higher quality and value-added services at a lower environmental cost.

Notes

If we assume that Spanish overseas tourism will trend in line with overseas arrivals, tourism payments abroad would decline by an estimated 11 billion euros, which is roughly one-third of revenue.

References

EUROPEAN COMMISSION. (2020). Proposal for a regulation of the European Parliament and the Council establishing a Recovery and Resilience Facility. COM (2020) 408 final.

— (2020). Commission Staff Working Document identifying Europe’s recovery needs. SWD (2020) 98 final.

EUROPEAN COMMISSION JOINT RESEARCH CENTER. (2020). Estimating and Projecting Air Passenger Traffic during the COVID-19 Coronavirus Outbreak and its Socio-Economic Impact. April 24th.

EXCELTUR. (2020). Medidas aplicadas por los distintos países en apoyo de las empresas turísticas, [Measures applied by a selection of countries to support their tourism business].

GOVERNMENT OF SPAIN. (2020). Plan de impulso para el sector turístico: hacia un turismo seguro y sostenible, [Plan for boosting the tourism sector: towards a safe and sustainable sector]. June.

RECCHI, E., DEUTSCHEMANN, E. and VESPE, M. (2019). Estimating transnational human mobility on a global scale. RSCAS 2019/30 Robert Schuman Centre for Advanced Studies Migration Policy Centre. European University Institute.

Gonzalo García Andrés and Andreu García Baquero. A.F.I. - Analistas Financieros Internacionales, S.A.