The Spanish economy: Signs of recovery in the midst of high uncertainty

COVID-19 has led to an abrupt decline in output in key sectors, which form the backbone of the Spanish economy, and the projected recovery in the second part of 2020 will only make up for part of the ground already lost. While growth should rebound more strongly in 2021, there are significant downside risks related to new outbreaks, rising unemployment and subdued demand reflecting a rise in precautionary savings.

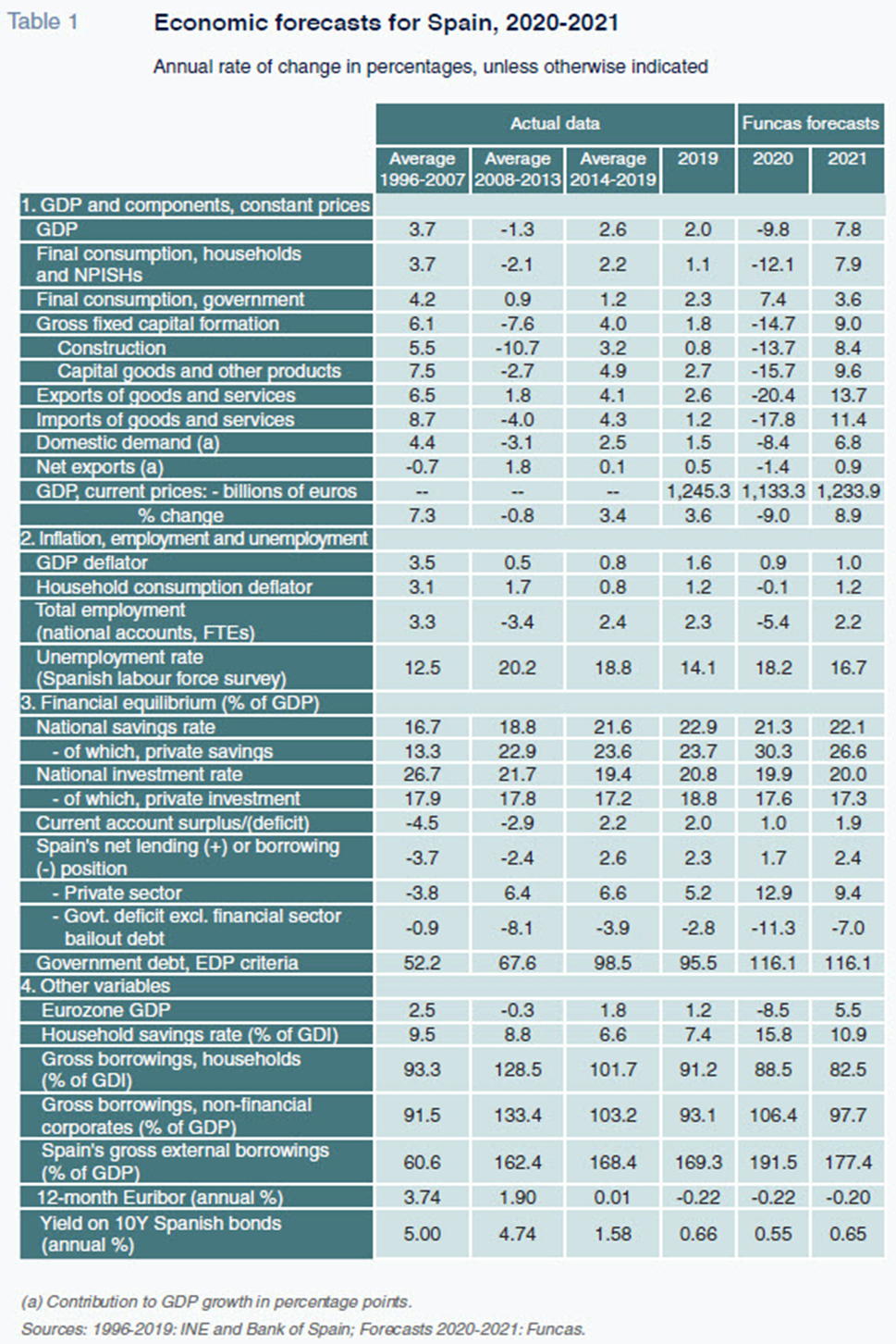

Abstract: COVID-19 is forecast to have contributed to an 18% quarter-on-quarter decline in GDP in 2Q2020. While lockdown measures have eased, the economy is not expected to reach pre-pandemic levels until 2023, at best. From a sectoral perspective, the automotive industry was particularly hard hit, with a contraction of nearly 90% in April and May. Likewise, the services sector’s turnover index in April declined by 42%. However, job losses in the construction sector exceeded those of the services industry. International trade has been strongly affected, too. April figures show exports declined by 32% in real terms compared with February, and imports dropped by 29%. COVID-19 also contributed to a significant expansion of government debt by more than 24 billion euros in 1Q2020. While the Spanish economy should experience a rebound in 3Q2020, it will not make up for the ground lost during the state of emergency. In general, projections are subject to significant uncertainty due to potential new outbreaks, the increase in savings rates, and the fate of furloughed workers once the employment support scheme expires.

First green shoots

Having contracted by 5.2% in the first quarter of the year as a result of the collapse in activity during the second half of March, the situation in Spain will deteriorate further in the second quarter, when GDP is expected to decrease by 18% quarter-on-quarter. Activity levels hit bottom in April and began to recover in May, a process which gathered pace in June, as the ‘easing’ measures accelerated, albeit without reaching pre-pandemic levels.

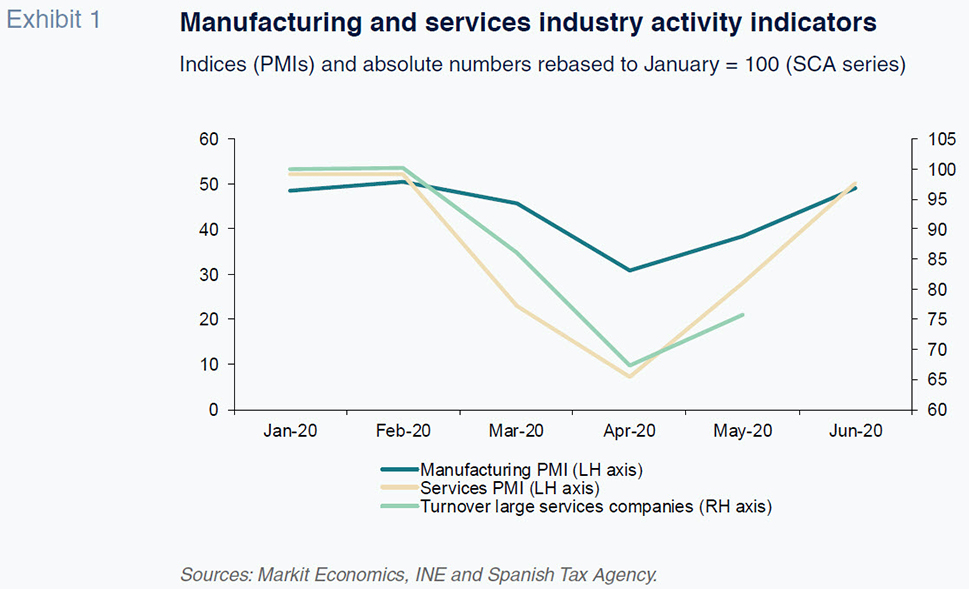

For example, Spain’s industrial production index (IPI) contracted by 33% in April with respect to February, recovering a scant third of that decline in May. However, according to the manufacturing PMI and industrial confidence index, the recovery gained traction in June (Exhibit 1). An analysis of the trend in the various manufacturing segments reveals that the automotive sector was the hardest hit in March and April, registering a contraction of close to 90%. That collapse undermined the momentum underway since the middle of last year as the sector began to recover from the slump that emerged in September 2018. The next hardest-hit sectors were the textile, garment, leather and footwear, and furniture segments, which sustained smaller but still sizeable declines. The segments affected the least were the food and pharmaceutical industries. The rest –capital and semi-manufactured goods– fell somewhere in the middle. The May figures suggest that the sectors most impacted by the crisis were, with the exception of the garment sector, also the sectors to post the strongest incipient recoveries. Nevertheless, production volumes were still well below crisis levels in May.

In the services sector, the contraction was initially harsher than in the manufacturing sector. There was a 42% decline in the services sector’s turnover index in April along with the collapse in the number of overnight stays and tourist arrivals. The services segments most affected were eateries, hospitality establishments, and the retail sector. In other areas, such as professional and telecommunications services, the impact was smaller. However, the services PMI readings suggest that following a modest recovery in May, activity picked up sharply in June (Exhibit 1).

The construction sector was more heavily affected at the start of the crisis than expected, with job losses in March and April exceeding the services sector and a drop in cement consumption of over 50%. However, it is also the sector to have rebounded most sharply. In May alone, cement consumption regained 72% of the above loss and between May and June around 60% of the jobs destroyed in March and April were created, a much stronger recovery than observed in either the services or manufacturing industries.

Turning to international trade, the most recent figures date to April and show exports declined by 32% in real terms compared with February, as well as a drop in imports of 29%. These figures suggest a sharper impact than observed in overall international trade. Specifically, global trade declined by 16% and exports from developed economies were 25% lower in April.

[1] Drilling down by segment reveals exactly the same pattern as the IPI readings. The products registering the sharpest decline in exports were automotive products, followed by textiles, garments, leather goods, and footwear. In contrast, exports of food products actually increased.

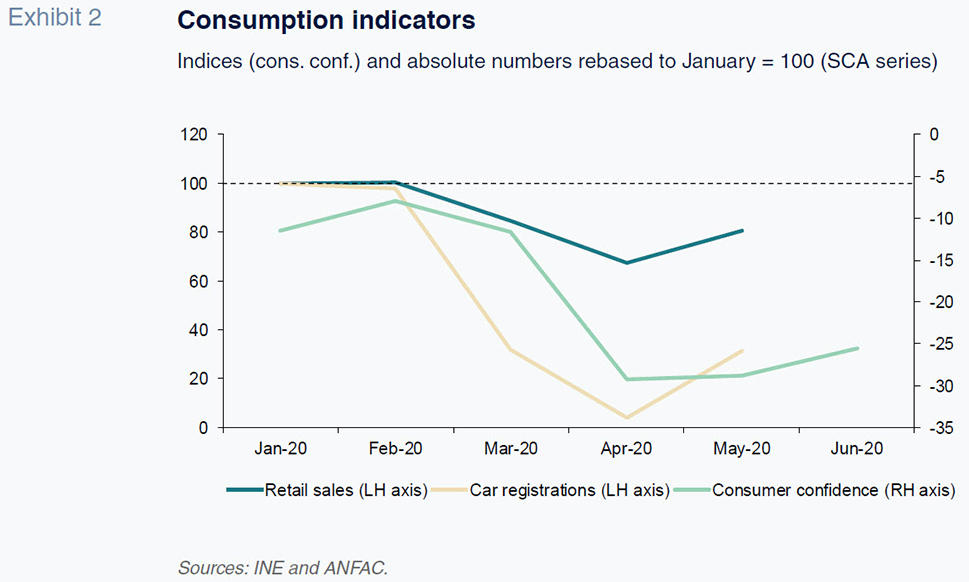

The consumer confidence indicators are also showing some encouraging signs. Having fallen sharply in March and April, retail sales rebounded in May, as did car registrations and the consumer confidence index in June, albeit still far from pre-crisis levels (Exhibit 2). Other high-frequency indicators, such as POS card payments, also point to a sustained recovery, with volumes closing in on pre-crisis levels by the end of June.

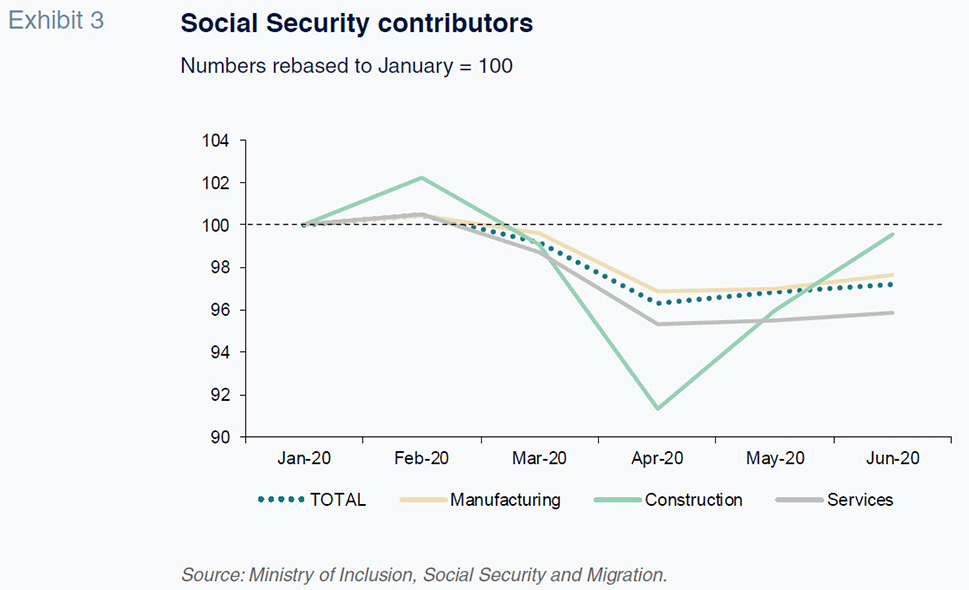

The job market is also showing signs of a recovery. Around 170,000 of the nearly 800,000 contributors who lost their jobs between March and April found work in June (Exhibit 3). Additionally, roughly 1.5 million employees out of a total 3.3 million affected as of the end of April exited furlough.

The balance of payments has deteriorated in the wake of the crisis. The drop in expenditure on imports, accentuated by the oil price correction, was not enough to make up for the collapse in tourism receipts. Consequently, the current account showed a 2.5 billion euro deficit for the first four months of the year, compared to a modest surplus during the same period in 2019.

Lastly, public finances are beginning to show the impact of the crisis. In the first four months of the year, the deficit at all levels of government except for the local corporations stood at 24.04 billion euros, compared to 6.74 billion euros in the first quarter of 2019. The expenditure related with COVID-19 amounted to nearly 8.9 billion euros, while public revenue fell by 3 billion euros.

Forecasts for 2020-2021

The forecasts assume a virus scenario of controlled outbreaks that do not necessitate the reintroduction of lockdown measures. They also factor in the economic policy measures already announced (state-sponsored loans for troubled businesses, extension of the furlough scheme, select support for demand and sector-specific plans). They do not incorporate either a European Recovery Plan or a State Budget for 2021 (at preliminary stages).

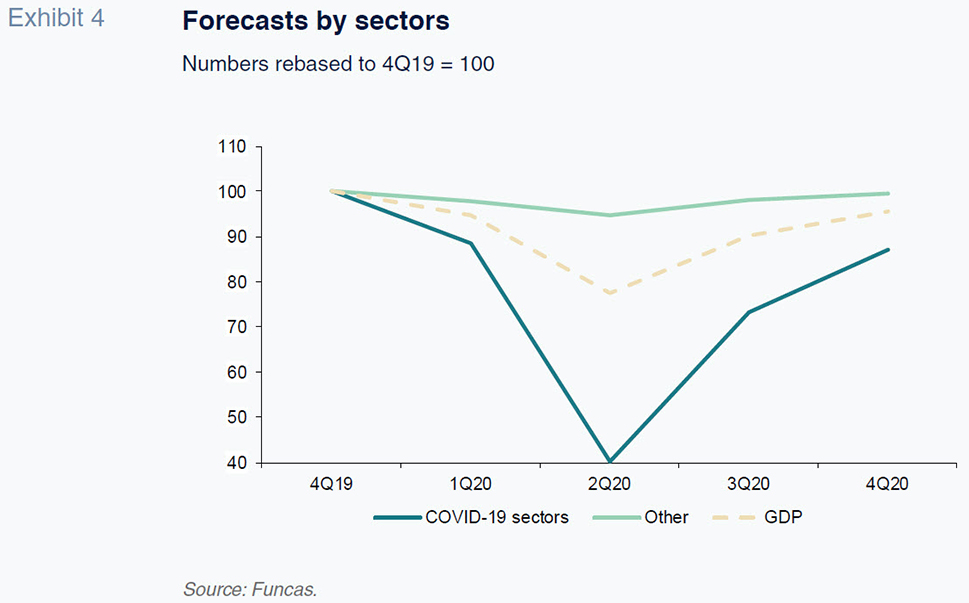

In light of the above assumptions, it is expected that the rebound initiated in the wake of the lockdown will continue during the months ahead, as more and more businesses come back to life and supply chains are reconfigured. We also expect to see new signs of recovery on the demand side. Households may decide to increase purchases of durable goods, having postponed decisions during the lockdown. Tourism is expected to stage a slight recovery and exports should restart, particularly among European countries. As a result of the above (and the increase in activity underway since early May which will automatically have a knock-on effect in the months to come), GDP is expected to rebound by 16.3% in the third quarter (Table 1). However, the recovery is set to be uneven (Exhibit 4). Certain sectors, such as the food, chemicals and pharmaceutical industries, as well as the health services and others that function well under remote working conditions, are likely to spearhead the recovery. At the other end of the spectrum, the hospitality and catering, transport, culture, leisure and performance and automotive industries are expected to experience a prolonged recession. The other manufacturing and the construction sectors will fall somewhere in the middle.

In addition, the recovery expected in the second half of the year will fail to make up for the ground lost during the state of emergency. Once pent-up demand has been released, private spending is likely to suffer from a spike in precautionary savings shaped by households’ fear of losing work or a significant proportion of their income. The household savings rate is expected to near 16% in 2020, an all-time high, while private consumption is expected to collapse by 12%. Investment is likely to experience an even greater blow, due to the extraordinary uncertainty surrounding the duration of the pandemic and its global impact, thereby affecting business expectations. The decline in investment is estimated at 15%, which would put the corporate sector’s capital expenditure efforts back at 2015 levels. Foreign trade will detract from growth due to the disarray in global trade, coupled with the crises affecting the tourism and automotive sectors which, between them, account for over 25% of export receipts in Spain. Public sector demand, shaped by the growth in health spending and investment, is likely to prove the only bright spot.

For 2020 as a whole, the forecasts point to an unparalleled contraction in GDP of 9.8%, due to a collapse in both domestic and foreign demand. The impact on the job market should be smaller than in the last crisis, thanks to the furlough schemes rolled out to enable businesses facing liquidity problems to contractually retain their employees. Fewer jobs will be lost than might be expected on account of the scale of the GDP contraction. This, coupled with the decline in the labour participation rate, should cushion the impact of the crisis on unemployment. Despite that, the average unemployment rate is estimated at 18.2% in 2020.

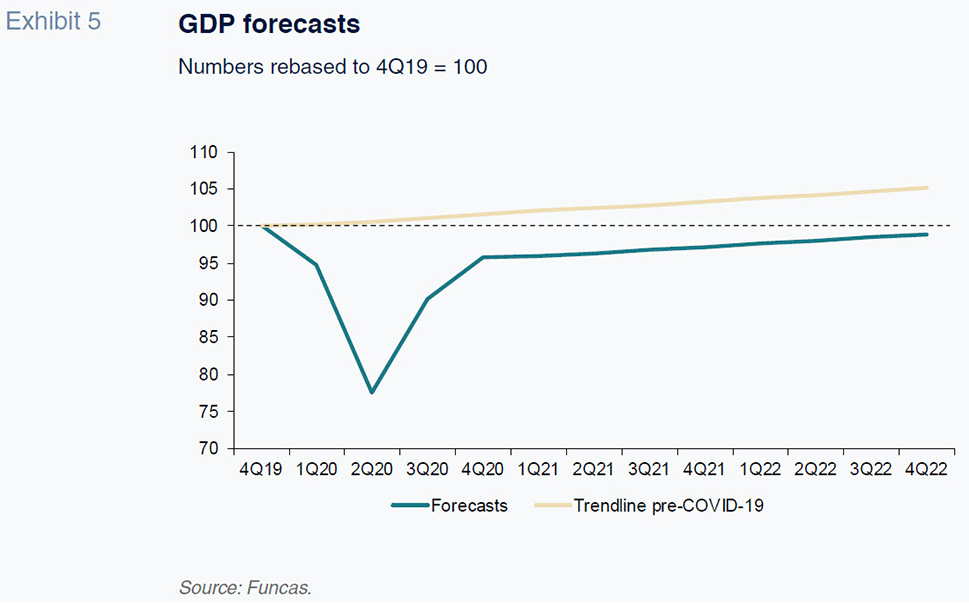

The recovery should gather pace in 2021. Growth that year is forecast at 7.8%, in part thanks to carry over effects and in part thanks to stronger contributions from private demand and tourism. As the level of uncertainty surrounding the health crisis diminishes (due to the availability of either an effective therapy or, in the best of cases, a vaccine), households might become more inclined to spend rather than save, and businesses to invest. Foreign trade should also make a positive contribution to growth in 2021 due to the gradual normalisation of international travel and tourism. Nevertheless, the numbers suggest that GDP will not revisit pre-crisis levels until 2023, or even later, considering the economic trajectory before the onset of the pandemic (Exhibit 5).

The recovery will benefit the job market but the impact will be subdued by fact that the end of the furlough scheme (the full return to work of people currently under the scheme or on short-time arrangements) will dampen companies’ hiring needs. In addition, the entry into the workforce of youths who had prolonged their studies will drive the participation rate higher. As a result, the unemployment rate is expected to come down slowly and remain above pre-crisis levels at the end of the projection horizon.

In the absence of information about the direction of fiscal policy, the public deficit would diminish due to the interplay of automatic stabilisers. All that improvement will achieve, however, is to stabilise government borrowings at high levels of around 116% of GDP.

Risks and opportunities

The forecasts remain subject to an unusually high degree of uncertainty and, by extension, a much higher than usual margin of error. This is not only because of the possibility of a second wave that would require new confinement measures or restrictions on certain economic activities, but also the significant uncertainty regarding the trend in certain macroeconomic variables. By way of example, it is only possible to make a reasonably informed guess about how high precautionary savings will rise, a factor set to prove an important determinant of the scale of the recovery in consumption. Another source of uncertainty –a very significant one in the case of the Spanish economy– relates to the trend in international tourism in the short- and medium- term, which is very hard to quantify and requires reliance on estimates. A final aspect that is particularly hard to forecast is what will happen to employment when the furlough scheme ends. It is possible that many companies, observing a permanent loss of business, will ultimately have to let some of their employees go, potentially triggering a second round of layoffs at the end of this year or the early part of next year.

Lastly, on the positive side, it is not inconceivable that a recovery plan at the European level, coupled with a reform programme, could stimulate corporate investment, helping to underpin the recovery from 2021 onwards.

Notes

Raymond Torres and María Jesús Fernández. Economic Perspectives and International Economy Division, Funcas