Changes in financing trends and payments preferences under COVID-19

COVID-19 has increased the volume of business loans and disrupted traditional preferences for cash transactions in Spain. While the demand for credit may persist depending on the duration of the crisis, the uptick in card payments should not be interpreted as a definitive movement away from the use of cash.

Abstract: The COVID-19 pandemic has disrupted Spain’s credit markets and payments methods. In regard to the former, it has triggered the need for financial aid programmes, including state guarantees of business loans. Notably, the volume of outstanding business loans in Spain, which had registered year-on-year growth of 1% in January and 0.4% in February, accelerated to 1.1% in March and to 3.1% in April. As for origination, while new loans amounted to 55.12 billion euros in January and February, the aggregate amount for March and April rose to 89.91 billion euros, providing a glimpse of the extra effort made by Spain’s banks to extend financing during the pandemic. Turning to payments, ATM cash withdrawals contracted by 9.3% year-on-year in April, having registered growth of 0.3% in 2019. Meanwhile, point-of-sale card payments, which had sustained growth of 9.4% in 2019, increased by a much lower 2.3% in the first quarter of 2020. That said, this does not foretell the death of cash, with certain segments of the Spanish economy still displaying strong preferences for this form of payment.

Introduction: Financial context and regulatory responses

The financial context as Spain exits the most restrictive aspects of its pandemic response could be described as one of cautious optimism. If new lockdowns are not required, the economic recovery may begin to gather pace. The financial sector is emerging as a key driver not only of the economic recovery but in the effort to mitigate the most immediate effects of COVID-19 on economic activity.

The underlying risks, exacerbated by the growth in public and private debt in recent years, have been contained by (even more) expansionary monetary intervention. On June 4th, the European Central Bank said it was expanding its Pandemic Emergency Purchase Programme (PEPP) by 600 billion euros and extending its duration until at least June 2021. It also signalled it would reinvest maturing principal payments from securities purchased under the PEPP until at least the end of 2022. These announcements were well received by the equity markets, which were beginning to view Europe as increasingly ready to reopen for business. However, in recent weeks, the good news has been mingled with fears of fresh outbreaks and the difficulties in permitting mobility between the EU member states and third countries in the current epidemiological context. Either way, the monetary accommodation has meant that the Eurosystem’s liquidity flows have remained immune from the effects of COVID-19. Indeed, the financing received by the banks from the ECB, which had increased by around 1% monthly between January and March, jumped by 4.3% in April and 5.1% in May.

The various EU members states have gone to noteworthy lengths to mitigate the effects of COVID-19 with financing programmes and solvency support. That said, some initiatives have been more or less generous and included different mixes of liquidity versus capital reinforcement programmes. In Spain, the largest programme has been the state-backed guarantee scheme. The fifth and last tranche of this scheme was activated on June 16th. It consists of 15.5 billion euros of loan guarantees with priority access for the self-employed, SMEs and firms from the tourism and automotive sectors.

Based on data as of June 1st, Spanish banks had extended 35.28 billion euros of financing to SMEs and self-employed professionals and an additional 12.97 billion euros to other enterprises. In total, they had provided 63.144 billion euros of financing. By comparison, in April and May of 2019, they granted 57.18 billion euros of loans, suggesting that they are lending more in 2020 than they would have in the absence of the coronavirus-induced uncertainty.

It is hard to imagine the economic effects of COVID-19 proving so limited in impact or duration that further extraordinary financing will not be needed in the coming months. Against that backdrop, this article attempts to estimate how much credit will be needed to alleviate the impact of the coronavirus and stimulate economic recovery. It also addresses matters of a more microeconomic nature related with citizens’ financial behaviour during the pandemic. Specifically, we look at how COVID-19 may have affected the manner in which Spaniards pay for things and the controversy arising around the advisability of using electronic payment methods at the expense of cash.

How much credit is enough?

Answering this question is constrained by limitations, mainly of an interpretative nature. Firstly, the financing extended can serve as a ‘bridge’ for covering business outlays during the period of idleness but cannot resolve some of the other existing issues. By this we mean that new financing will not solve the problems of a significant number of companies that were already facing viability issues. Unfortunately, these companies will not be able to survive the ramifications of the lockdown measures. For similar reasons, the relative ‘success’ of the loans extended to businesses will also depend on the non-occurrence of fresh outbreaks requiring new partial or total shutdowns, as many companies’ solvency would be compromised by additional leverage. On the other hand, it is hard to establish the reference parameters for determining how much credit is necessary to cover businesses’ liquidity needs. If the financing attributable to the extraordinary measures rolled out to mitigate the effects of COVID-19 reaches the targeted 100 billion euros (the estimated total size of the state guarantee scheme), we would be talking about an amount equivalent to around 30% of the new loans needed by Spanish companies in 2019. However, it is very likely that the vast majority of the COVID-19 funds will be used to cover income losses and urgent outlays rather than being earmarked for investment. One approach is to look at the relationship between credit demand during the period affected by the pandemic and subsequent months. Although there are no official statistics, there is anecdotal evidence from a number of Spanish banks to suggest that the demand for financing (the state guarantee scheme and other standard loans) has significantly outstripped supply. However, the demand for credit has been largely met through the guarantee and similar schemes so that in the event that new tranches were to materialise, it would be possible to identify the amount of residual demand for credit.

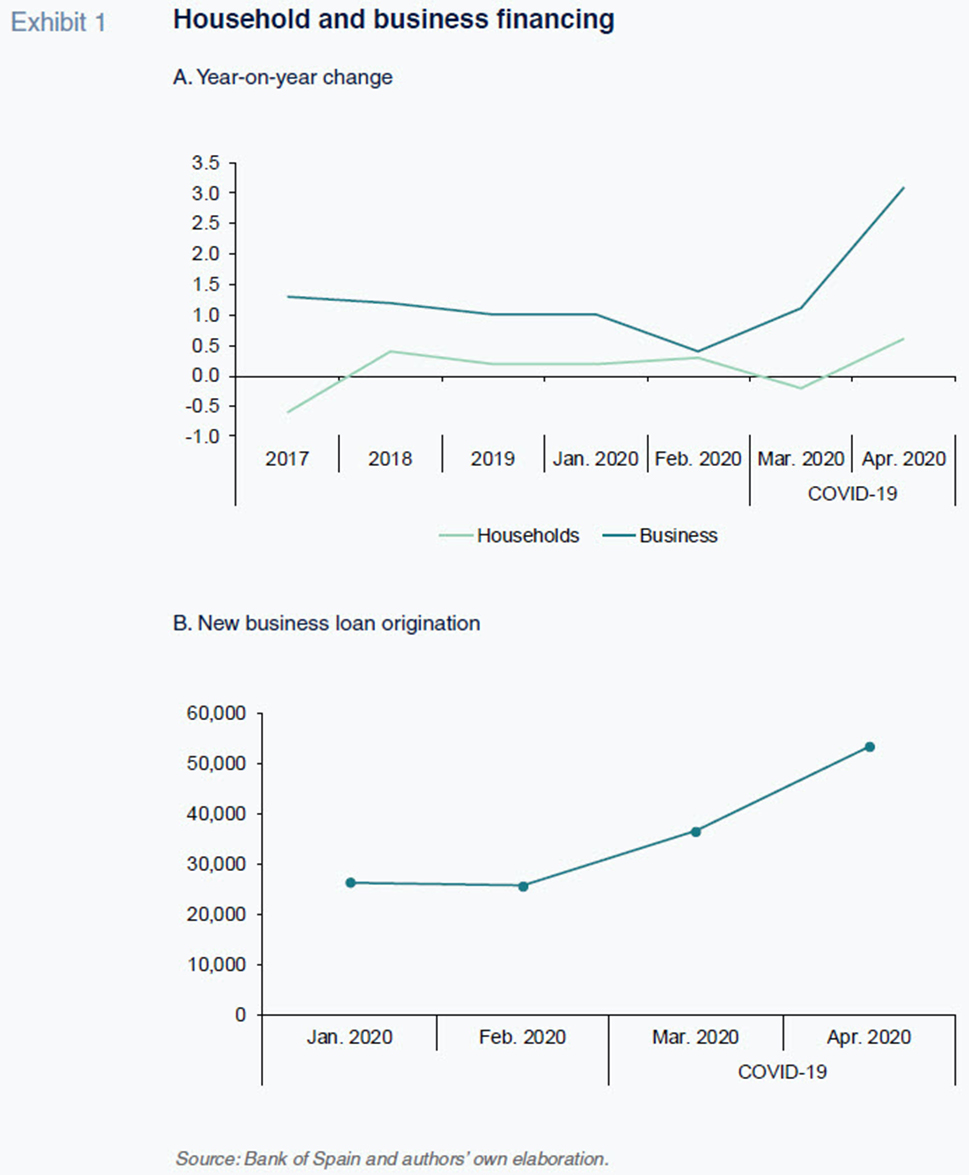

Some recent figures point to a significant increase in company lending in March and April (the only months impacted by COVID-19, in part or in full, for which numbers are available). The first panel of Exhibit 1 shows the year-on-year rate of change in the outstanding volume of financing for Spanish households and businesses. In the household lending segment, the total loan book decreased slightly in March (by 0.2% year-on-year) compared to prior months but went on to recover in April (+0.6%). In the corporate lending segment, which is where the bulk of the public-private schemes are targeted, the volume of credit outstanding increased by 1% in January and 0.4% in February. This trend continued during lockdown, with the volume of outstanding credit rising by 1.1% in March and 3.1% in April. The second panel depicts the volume of new business loan origination. Having amounted to a combined 55.12 billion euros in January and February, the aggregate for March and April increased considerably, to 89.91 billion euros.

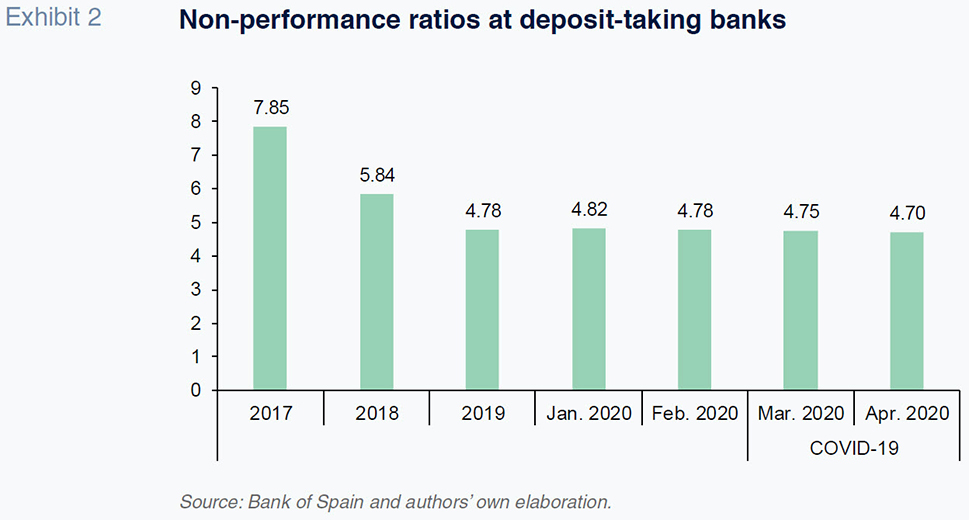

Although a significant proportion of the financing extended enjoys state-backed guarantees, a limit on new loans is an appropriate risk control measure. Loan non-performance is likely to increase in the coming months in tandem with some of its key drivers, such as the unemployment rate. Based on the most recent data available, the non-performance ratio (Exhibit 2) remained at 4.70% in April, below the readings for March (4.75%) and February (4.78%).

The biggest increases in non-performance will most likely come after the summer. The public guarantees for those non-performing loans will also have adverse effects on Spain’s public finances. Importantly, the extent of the rise in non-performance and the ability to bring it quickly under control will depend largely on the occurrence of new outbreaks and their impact on the economy.

Payments in times of lockdown... and beyond

As outlined above, the primary concerns during the pandemic centre on business financing and viability. In this matter, public policies and private strategies constitute a significant social experiment – the impact of which remains unknown. For households, however, one of the biggest financial experiments in the wake of COVID-19 has affected something as basic and all-important as how to pay for things. Among the rumours and misinformation prompted by the irruption of the pandemic, one of the earliest to emerge is related to the importance of using electronic methods rather than cash for hygiene purposes. However, many monetary authorities (the ECB and the Bank of Spain included) have since said there is no foundation for such claims. Also, the Bank for International Settlements (BIS) said in its April bulletin (No. 3: “COVID-19, cash, and the future of payments”) that the scientific evidence suggests that the probability of transmission of the virus via banknotes is very low when compared with other frequently-touched objects, such as credit card terminals or PIN pads. In fact, the coronavirus can survive on a stainless-steel surface between 10 and 100 times longer than on our cotton-fibre banknotes.

The BIS also said that even though we are advancing towards greater use of digital payments, many consumers need to use cash and should be permitted to do so without constraints. That is perhaps the most important observation in terms of gauging the trend in retail payments post COVID-19. Generational change and technological momentum point to growing use of electronic payment instruments in the long-term. However, all payment instruments have their own advantages and disadvantages. Many citizens continue to prefer to pay in cash and, in light of recent efforts in some European countries to impose limits on its use, the ECB has come to their rescue stating that money is legal tender and cannot be forbidden, particularly considering how dependent a significant percentage of the population is on it for their payments. The Bank of Spain published its latest survey on payment preferences in 2018 in which it found that 53% of Spanish citizens say cash is their most commonly used method of payment (57% in small towns), while 43% expressed a preference for debit cards.

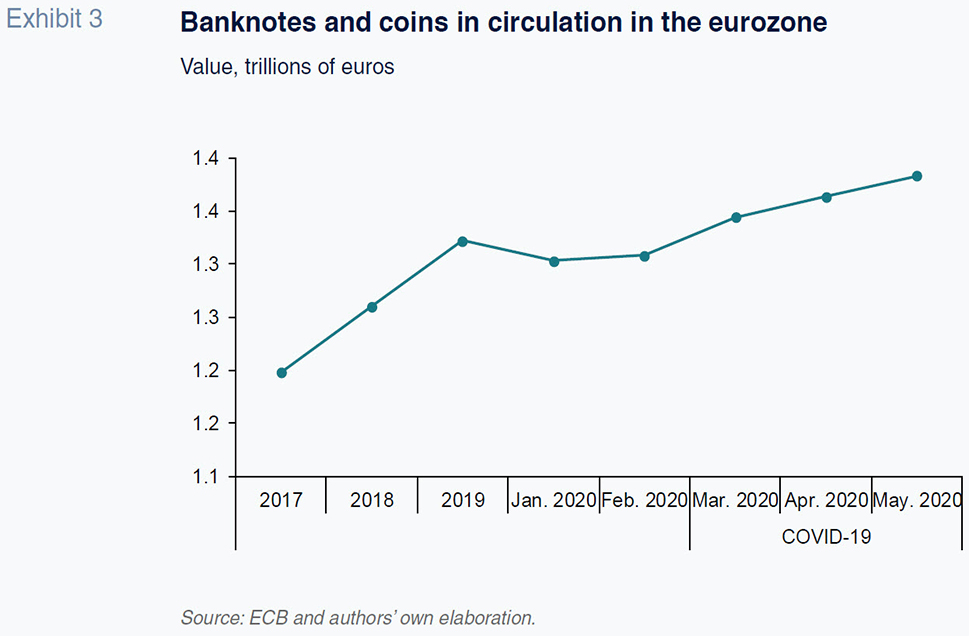

It remains to be seen whether COVID-19 will drive a significant and permanent change in payment preferences. In the meantime, the evidence does not point conclusively in that direction. In the eurozone, the value of banknotes and coins in circulation (Exhibit 3) has increased in recent months, particularly during the COVID-19 crisis period (between March and May). Specifically, notes and coins in circulation increased from 1.3 trillion euros in January to 1.38 trillion in May.

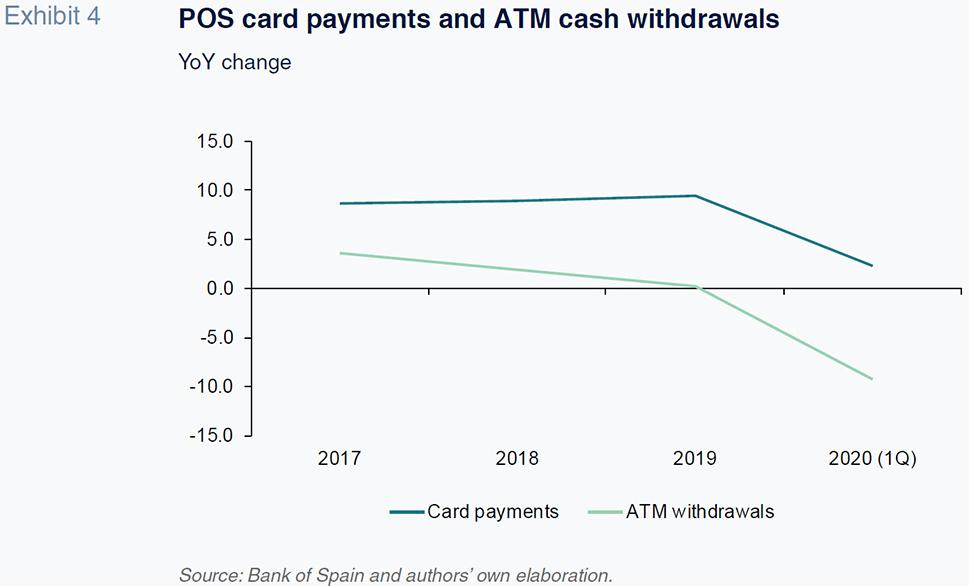

However, it is also important to the methods used to settle transactions. The most recent data in Spain suggests that the lockdown triggered a significant decline in the use of payment instruments in general. As shown in Exhibit 4, according to Bank of Spain data, ATM cash withdrawals contracted by 9.3% year-on-year in 1Q2020, having registered growth of 0.3% in 2019. Meanwhile, point-of-sale card payments, which had sustained growth of 9.4% in 2019, increased by a much lower 2.3% in the first quarter of 2020. We will have to wait until economic and social activity normalises to assess whether the payment trends observed prior to the pandemic have shifted meaningfully.

Conclusions

COVID-19 is causing one of the biggest social and economic disruptions of recent decades. For households and businesses, how to get financing and how to make payments have become key concerns.

In the credit arena, the articulation of public-private financing schemes has enabled the provision of liquidity vital to keeping many businesses afloat. However, it is hard to determine if they will prove sufficient in the medium-term. All signs suggest that further intervention will be required and that the current programmes will have to be extended, including the state-backed guarantee scheme.

As for payments, the coronavirus and the resulting need for social distancing are conducive to the use of contactless payments. However, it has also evidenced the fact that much of society needs or still prefers to pay with cash so that the imposition of restrictions on its use could lead to financial exclusion and issues for basic household activities.

Beyond question, however, is the fact that COVID-19 represents an exogenous factor from which economic studies stand a lot to learn. Future studies will examine not only which public policies or bank strategies are best in the credit and retail payments fields, but also whether this pathogen has by itself triggered structural changes in basic financial activities.

Santiago Carbó Valverde. CUNEF, Bangor University and Funcas

Francisco Rodríguez Fernández. University of Granada and Funcas