Challenges for Spain’s auto industry: Mobility model uncertainty and collapse in exports

Although home to Europe’s second largest automobile industry, the value of Spanish automotive exports has fallen in recent years due to stagnation in European export markets as well as the prevailing product mix that favours alternative fuel models over diesel vehicles. For this reason, the Spanish and European authorities should design transitional measures that support the production of less environmentally harmful diesel vehicles.

Abstract: The Spanish automotive sector is a key part of the country’s industrial sector, accounting for 9% of GDP and nearly 8% of employment. Notably, export growth between 2013 to 2019 was equivalent to a constant annual rate of 2.6%, just shy of growth in Germany (2.9%) but ahead of Italy (2.4%) and France, where annual average growth in exports has been just 0.5%. However, export growth has been slowing, a concern given that historically eight out of every ten vehicles produced in Spain are exported. This slowdown in exports has also occurred in countries, such as Germany, Italy and France, leading to a deterioration of trade balances in the automotive sector. Unfortunately, the arrival of COVID-19 interrupted a recovery in car exports, leading to an annual export contraction of 87.9% in April. That said, there are longer-term challenges other than COVID-19 that threaten the future growth of the industry, including significant competition from abroad, slower growth in new car registrations in Europe, and uncertainty regarding the cleanest alternative technology for cars. The latter is of particular importance and will call for the design of transitional measures that address the reorganisation of the production of diesel cars, which, in any case, are less environmentally harmful than previous diesel models.

Introduction

Spain produced 2,822,360 vehicles (passenger cars: 2,209,497) in 2019, which makes it the number-two producer of automobiles in Europe after Germany. However, the automotive sector is much more than just the manufacturing of vehicles. It encompasses the manufacturing of parts for those vehicles as well as the sales and after-sales segments.

[1] In all, the automotive sector is responsible for 9% of GDP and nearly 8% of employment.

[2] The production of vehicles is in the hands of multinational car manufacturers which between them have 17 factories in the country.

[3] They are supported by a highly dynamic and innovative parts sector whose footprint is nationwide. As such, it plays a core role in the distribution across Spain of wealth generated in the automotive sector.

Spanish vehicle exports in the international context

The automotive sector is a global industry made up of mature markets (North America, Europe and Japan) and fast-growing developing markets (China, India and Latam). Car manufacturers have maintained local footprints in these so-called major regional markets in order to attract demand. As a result, even though transport and logistics costs have fallen and could justify mass re-location to low-cost producer nations, many automobile manufacturers have made the strategic decision to maintain a presence across several countries within a given region (Sturgeon and Van Biesebroeck, 2010). For example, in Europe there are parent companies (Volkswagen, PSA and Renault) headquartered in mature markets (Germany, France and Italy) that have expanded their manufacturing footprint across other countries. They initially spread to the southern periphery (Spain and Portugal). During the second wave of expansion, new factory locations were concentrated in those countries that joined the European Union in 2004 (Czech Republic, Slovakia, Slovenia and Poland) and in 2007 (Romania and Hungary). More recently, they have set up bases in Turkey and Morocco. This factory location process has been accompanied by a production specialisation phenomenon which explains the intense flows of trade that characterise the automotive sector in Europe.

Spain is one of the biggest exporters of automobiles in Europe. Eight out of every ten vehicles made in Spain are exported. Although the propensity to export is a little lower in the parts sector (58% of output was exported in 2019), the parts makers have accompanied the automakers in their international expansion, locating themselves in proximity to their factories. Analysis of export flows reveals the strengths of a sector that has retained its leadership in Europe but also points to the weaknesses already in existence before the pandemic triggered the current collapse. The new international context requires addressing those challenges if the automotive industry is to overcome the prevailing difficulties unleashed by COVID-19 and survive in an uncertain future.

An analysis of Spanish exports first requires a comparison with exports from the main producers in the European Union (Germany, France and Italy). The flows of exports of motor vehicles and motor vehicle parts and accessories from these countries is illustrated by Eurostat’s annual international trade data. The manufacturing of motor vehicles and parts and accessories for the motor vehicles sector is comprised by the export of motor cars (781); motor vehicles for the transport of 10 people or more (783); motor vehicles for the transport of goods (782); motors for road vehicles (713.23); and parts and accessories for road vehicles (784).

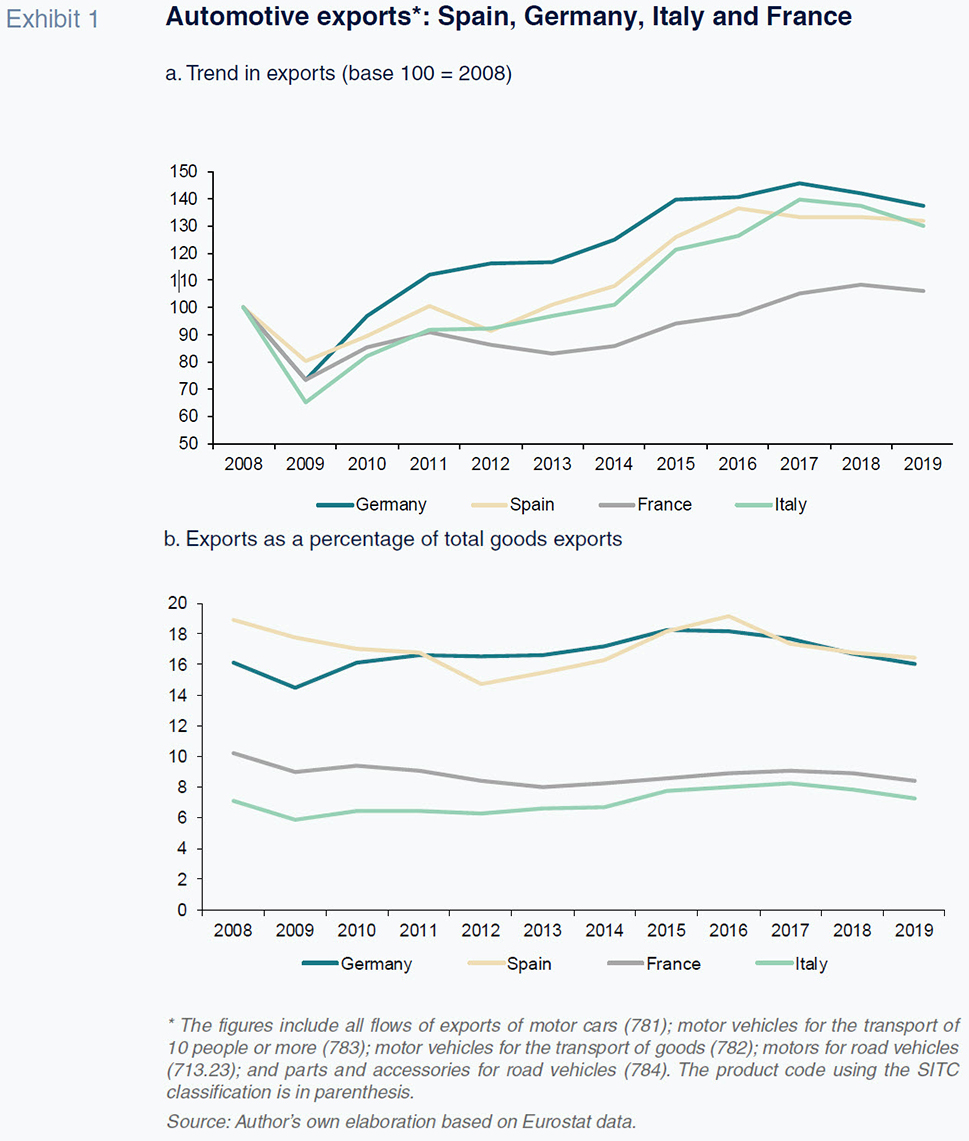

[4] For a broad perspective, we looked at a complete economic cycle, namely from 2008 until 2019. Exhibit 1.a shows the growth in the value of exports on an indexed basis (to facilitate a comparison of the trends in numbers of very differing magnitudes), revealing an overall positive performance by the Spanish industry this last decade. By 2013, Spain had regained the export receipts recorded prior to the recession and in 2019 it exported 32% more than in 2008. In sum, the Spanish automotive sector has registered export growth equivalent to a constant annual rate of 2.6%, just shy of growth in Germany (2.9%) but ahead of Italy (2.4%) and France, where annual average growth in exports has been just 0.5%.

Spain’s strong performance observed during the last decade was driven by particularly dynamic exports between 2012 and 2016, when annual growth averaged 10.6%. As a result, the sector’s exports rose up to 19% of all Spanish goods exported. Since 2016, however, Spanish exports of vehicles and parts have lost momentum, accounting for 16.4% of total goods exports in 2019 (Exhibit 1.b).

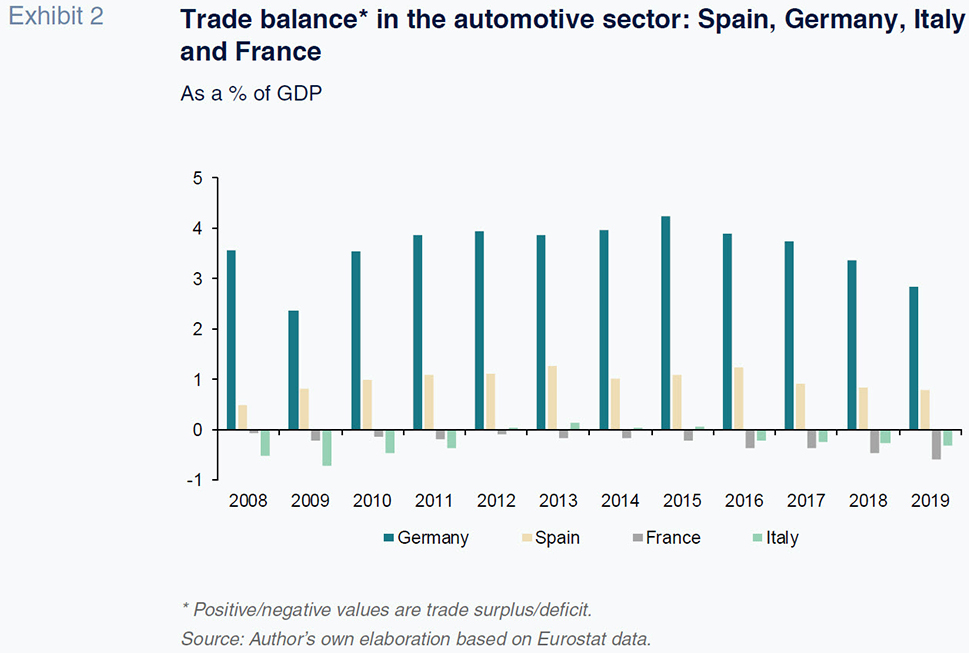

The stagnation and drop in exports are a pattern also observed in the other countries analysed (in Germany in 2015 and a little later in Italy and France). As a result, the trade balances in the automotive sector have deteriorated. As shown in Exhibit 2, the trade deficits in France and Italy have widened and the trade surpluses in Spain and Germany have narrowed. This indicates that automotive exports were in trouble before the onset of the pandemic. It is crucial to analyse which risk factors were driving the sector’s downward trend that not only compromised firms’ profitability but also the economies’ trade accounts. In Spain, where very few manufacturing sectors present trade surpluses, the sector’s exports account for 4% of GDP.

Pandemic-induced collapse of already weakening exports

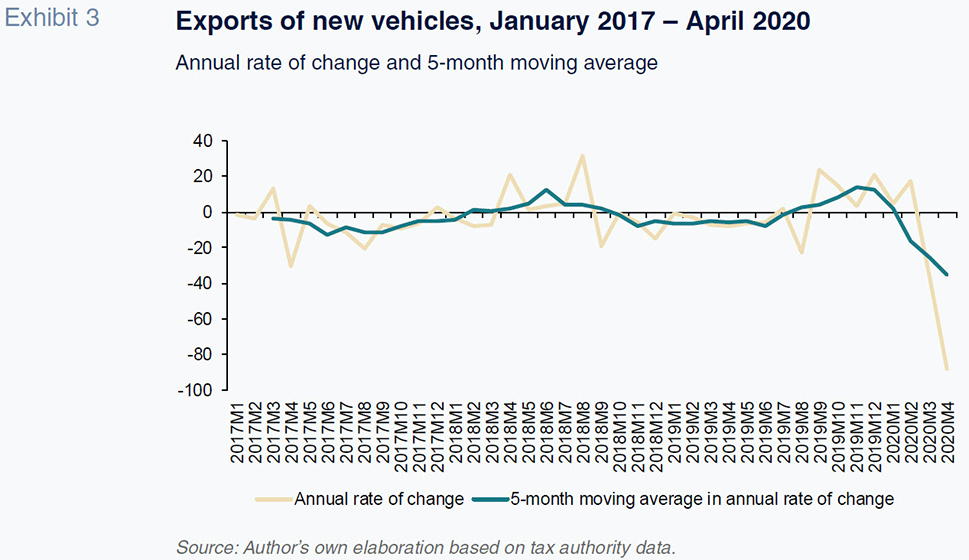

To calibrate the collapse in exports precipitated by the COVID-19 pandemic, we look solely at passenger and off-road vehicles, as they account for the bulk of the vehicles exported by Spain. We also distinguish between sales of new and second-hand vehicles, selecting only exports of new vehicles, which represent 95% of receipts.

Exhibit 3 provides the annual rate of growth in exports of passenger and off-road vehicles declared to the Spanish tax authorities between January 2017 and April 2020. These figures confirm the above-mentioned adverse trend as most months the numbers are negative. Car exports had been recovering since the third quarter of 2019, only to be stopped short by the production shutdown triggered by COVID-19 (Moral, 2020). Specifically, in March, due to the two-week lockdown period, exports contracted by 36.2%. This contraction widened in April to 87.9% year-on-year when the economy was totally shut down for the first half and in ordinary lockdown the rest of the month.

[5]

Given the scale of the contraction, public intervention will be needed to facilitate a return to pre-pandemic levels.

[6] In the next section, however, we focus on establishing the causes of the adverse trend in exports most months in recent years in order to identify all the challenges that need to be tackled.

Automotive exports: Risk factors

There are three key factors that have adversely affected Spanish exports: i) a significant increase in competition from abroad; ii) slower growth in new car registrations in the main European markets to which the majority of Spanish exports go; and, iii) uncertainty regarding the cleanest alternative technology which is resulting in counter-productive demonisation of diesel cars that form an important component of the European automobile manufactures’ product mix, to the advantage of Asian automobile manufacturers. On top of these factors, the US has been threatening to impose tariffs on European cars. That said, this threat would mainly affect Germany, which has the highest exposure to the US market. Spain is less exposed to this risk factor as the US accounted for just 2.2% of the value of automotive exports from Spain in the first few months of 2020.

To combat the first risk factor, the sector needs to further boost productivity levels and win business for car models with promising sales forecasts. Spain has done a good job on this front, managing to attract exclusive production (in Europe and sometimes worldwide) for a number of models even though the Multinational Enterprises (MNEs)’ decision centres are not in Spain. It is important to continue to pursue this line of initiative.

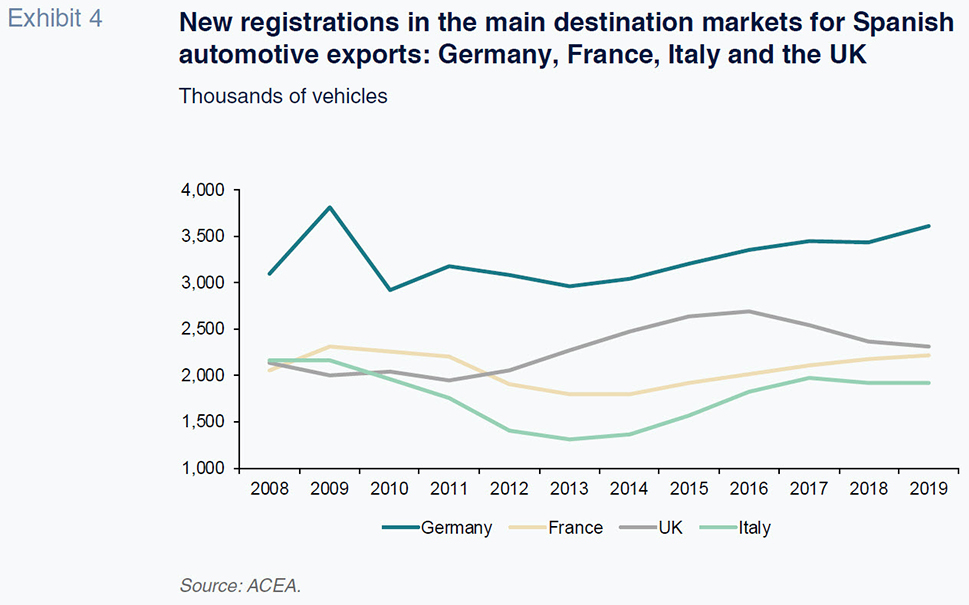

The cause of the second risk factor lies in the fact that Spanish exports are very concentrated in Europe. Sales to Germany, France, Italy and the UK accounted for 65% of all exports in 2019. In theory, that is only a weakness when those markets register slower than expected growth or are affected by unforeseen developments, such as Brexit. In those four markets, new registrations began to stagnate in 2016 with a considerable decline observed in the UK (Exhibit 4), placing considerable pressure on Spanish exports. To mitigate this situation, firms looked for new markets. Within the European Union, they increased their exports to Poland, while outside the EU they increased exports to Morocco, Turkey, Egypt and Israel, among others. However, the strategy of diversifying outside of the European Union did not yield the desired results and was abandoned. More recently, companies have re-focused on intra-EU exports.

The biggest threat facing the Spanish automotive industry resides with the mix of vehicles it produces. The industry is more intensive in diesel vehicles than other countries it competes with, which embarked on the transition to hybrid and electric models sooner than in Spain. This vulnerability pre-dates the pandemic and is of increasing importance in light of developing mobility models. However, addressing this challenge will be very slow process and require decisions by parent companies located in other countries. In parallel, there is scope for toning down the ‘demonisation’ of diesel engines as the newer vehicles are more environmentally friendly than previous diesel models.

[7] In fact, the growth in sales of petrol and hybrid petrol vehicles (which at high speeds perform like petrol engines) is driving an increase in total CO

2 emissions as their emissions are, on average, 15% higher than diesel cars. As a result, Spain’s 2040 emission reduction target, which requires the elimination of diesel cars, should be accompanied by a clear transition period for all technologies. While many have assumed that diesel engines will be a thing of the past, the degree of uncertainty surrounding this process is very high. Meanwhile, Spanish car manufacturers have begun to modify their product mixes. The new European Emissions Performance Standards Directive (Regulation EU 2019/631 of April 17

th, 2019), under which every automobile manufacturer must guarantee that their new vehicles emit fewer than 95 grams of CO

2/km, took effect on January 1

st, 2020. Although there is a three-year transition period, breach of the new requirements will entail hefty fines.

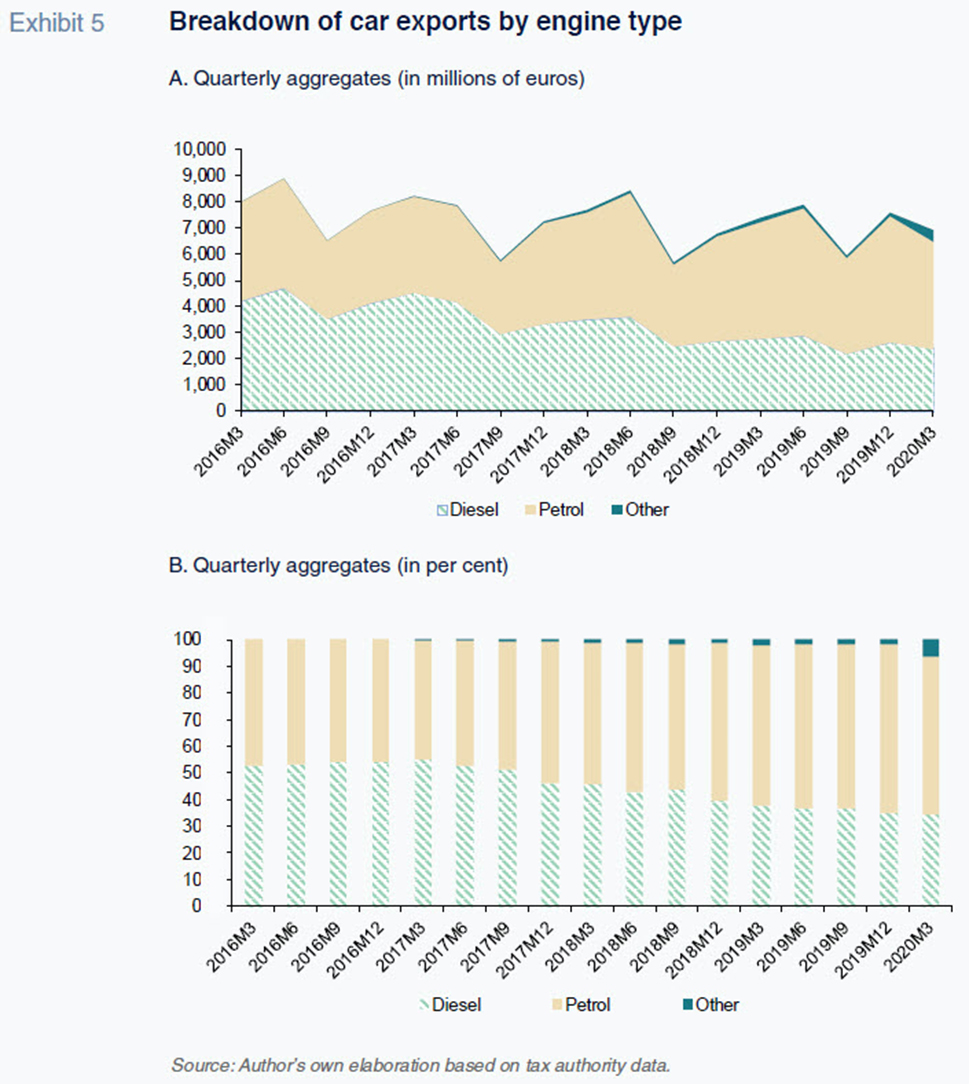

Building from the Spanish tax authority’s trade data, Exhibit 5 provides the breakdown of new car exports by engine type (petrol, diesel and other)

[8] in absolute and relative terms. Until the third quarter of 2017, receipts from the sale of diesel cars overseas accounted for over half of total revenue from new vehicle exports. In September 2017 the new World Harmonized Light Duty Vehicle Test Procedure (WLTP) took effect, resulting in a shortfall of qualifying engines, leading to a shift in the sales trend. Since then, the weight of diesel vehicles in total exports has been falling. However, the growth in petrol vehicles has not been sufficient to maintain export volumes, which, as we have seen, have fallen. Moreover, the prevalence of vehicles fuelled by other engines (hybrid and electric) is residual, accounting for just 6.5% of all passenger vehicle exports in the first few months of 2020 when the new emission performance standards were already in effect.

In sum, the Spanish automotive sector is at a clear disadvantage when it comes to hybrid and electric vehicle exports. In addition, the replacement of diesel by petrol cars has had the effect of leaving the average price per new car exported stagnant at around 13,358 euros in the last three years.

Conclusions

The motor vehicle and parts manufacturing industry is strongly entrenched in the Spanish industrial landscape. Its contribution to wealth creation, employment and the trade surplus is key. This paper takes a look at the recent trend in automotive exports in comparison with Germany, Italy and France, showing that Spain’s performance has trended in line with that of the European sector champion, Germany.

Automotive exports (by value) have been trending slightly lower in Spain since 2016, primarily due to the substitution of diesel cars, compounded by a slower transition to more environmentally friendly cars that fetch similar or higher prices. Alternative-fuel vehicles are marginal within Spain’s production mix and that weakness is weighing on exports. Meanwhile, sales of petrol-run cars (which are cheaper on average) have not fully offset the downward trend in diesel car sales. The market has also been affected by a drop in new registrations in the UK and stagnation in Germany, France and Italy, the main buyers of the cars made in Spain.

It was against that weak backdrop that exports collapsed in March and April as a result of the economic standstill due to the COVID-19 pandemic. As a result, the sector is facing a challenging environment. However, the current situation also represents an opportunity for the Spanish automotive industry to react and, with the help of the public sector, regain its predominant role in the Spanish economy.

Spanish manufacturers need to shift their production towards cleaner car models in order to capture more consumers. However, the Spanish and European institutions should also roll out measures designed to reduce uncertainty regarding the new mobility models, emissions regime and energy savings requirements. The authorities should design transitional measures for diesel cars manufactured today, which are more fuel efficient than older diesel models. The production of these models cannot be eliminated in the short term without a significant impact on jobs and Spanish industry. The risk is that measures aimed at stimulating demand could largely translate into growth in imports from China –the leader in electric vehicle sales– which, while entirely legitimate, would not resolve the problems facing a manufacturing sector of such strategic importance to Spanish and European industry.

Notes

Laborda and Moral (2017) analyse the post-sales sector (repair shops, dealers, spare parts, rental, consultants and insurance brokers) in Spain.

According to Spain’s national car and truck manufacturing trade association, ANFAC, the vehicle and parts industry accounted for 566,400 direct jobs (2.9% of the working population) in 2019.

In May, Nissan announced plans to close its factory in Barcelona in December 2020.

The lockdown began on March 14th; however, on March 29th, the Spanish government decreed a compulsory paid leave for employees who did not provide essential services (Royal Decree-Laws 10/2020 and 11/2020) to further reduce mobility and curb COVID-19 more effectively.

Royal Decree 569/2020 (June 16th, 2020) regulates the efficient and sustainable mobility incentive plan (known as MOVES II) which regulates the provision of subsidies for the purchase of alternative-fuel vehicles, among other lines of initiative.

A passenger vehicle registered in 2000 emitted 230g of CO2/km. In January 2020, the emissions legislation requires registered vehicles to emit less than 95g/km on average.

Broken down to the eighth digit in the product classification. “Other” includes hybrid diesel and petrol engines and electric cars.

References

LABORDA, J. and MORAL, M. J. (2017).

Libro Blanco de la Posventa del Automóvil en España [White Book on After-Sales in the Automotive Industry in Spain]. Published by After Market Club. ISBN: 978-84-9701-330-7.

MORAL, M. J. (2020).

El freno industrial durante marzo es intenso pero menor al observado en Europa. [The industrial slump in March was intense but less than that observed in Europe]. Retrievable from the Funcas blog at

www.funcas.esSTURGEON, T. and VAN BIESEBROECK, J. (2010). Effects of the 2008-9 Crisis on the Automotive Industry in Developing Countries: A Global Value Chain Perspective. In O. CATTANEO, G. GEREFFI and C. STARITZ.

Global Value Chains in a Postcrisis World: A Development Perspective.

María José Moral. UNED and Funcas