Housing markets ahead of the threat of recession

Despite the drop in household income as a result of inflation, the housing market has remained dynamic due to its safe-haven appeal, pent-up savings and abundant financing. This atypical trend may, however, be reaching an inflection point in the face of changing monetary conditions; nonetheless, we are not looking at a market standstill or a major increase in non-performing loans but rather a sharp slowdown of the current expansionary cycle, with the main risk to this baseline scenario stemming from the macroeconomic effects of the energy crisis and a worsening geopolitical context.

Abstract:

Despite the drop in household income as a result of prevailing inflation, the housing market has remained dynamic: transaction volumes are up 20% so far this year and prices are tracking 8% higher. This atypical trend is attributable to the safe-haven appeal of housing at a time of rampant inflation, in addition to the savings accumulated during the pandemic and access to abundant financing. The current bull market may be reaching an inflection point, however, in light of the tighter monetary policy stance. Though we still expect prices to increase by around 6% on average this year, in line with our earlier estimate, a marked slowdown is predicted for next year. The market will not collapse, however, in light of the strong underlying demand and relatively healthy financial position of households. The main risk to that baseline scenario is not the formation of a bubble (as is the case in other countries), but rather the macroeconomic fallout from the energy crisis and general climate of uncertainty.

Introduction

In recent months, particularly since the invasion of Ukraine, the economic outlook has deteriorated sharply. The intensification of the energy crisis, coupled with the effects of the war and its broader geopolitical tensions, have heightened the risk of recession, especially in Europe (ECB, 2022). That turbulence is also continuing to fuel inflationary pressures, forcing the main central banks, including (after much hesitation) the ECB, to change monetary tack.

In an increasingly uncertain environment, one of the main unknowns relates to the housing market. Its predicament is an important question from the social point of view as well as in terms of financial stability. The property market has been surprisingly dynamic throughout the pandemic, fanned by the prospects of recovery and ongoing low interest rates. Now that the risk of recession looms, the sustainability of that dynamism is in question.

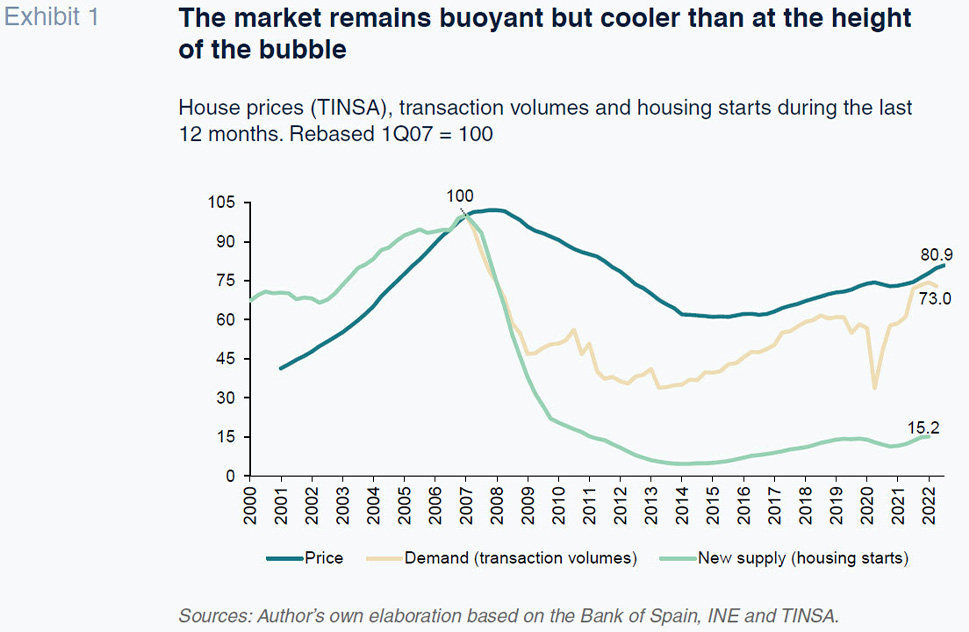

The housing market has continued to grow despite the economic slowdown

For now, the downturn in economic prospects has hardly affected the housing market, at least in Spain. Transaction volumes continue to rise at an annual rate of over 20%, according to the second-quarter figures, albeit slowing slightly compared to the start of the year (Exhibit 1). Prices have also been heading north since the dip taken during the pandemic. The average appraisal value has been increasing at an annual rate of close to 8% up until the summer. In August, a traditionally slow month, the price index fell back slightly (-0.8% compared to July, which is similar to the contraction observed in August 2021).

There are no major differences among the various regions, although the trend is less even than in recent years. Prices continue to rise in places like Madrid, the Balearics and, to a lesser extent, the Canaries. However, prices are stagnating in regions with less dynamic demographics, such as Castile La Mancha, Castile & Leon and Extremadura, and they are stagnating at relatively low levels, moreover.

Nor are we seeing a change of trend in the mortgage market, where transactions are registering year-on-year growth of close to 1% so far this year, compared to 0.7% in 2021. That performance contrasts with the contraction observed prior to the pandemic when loan repayments were outpacing the arrangement of new loans.

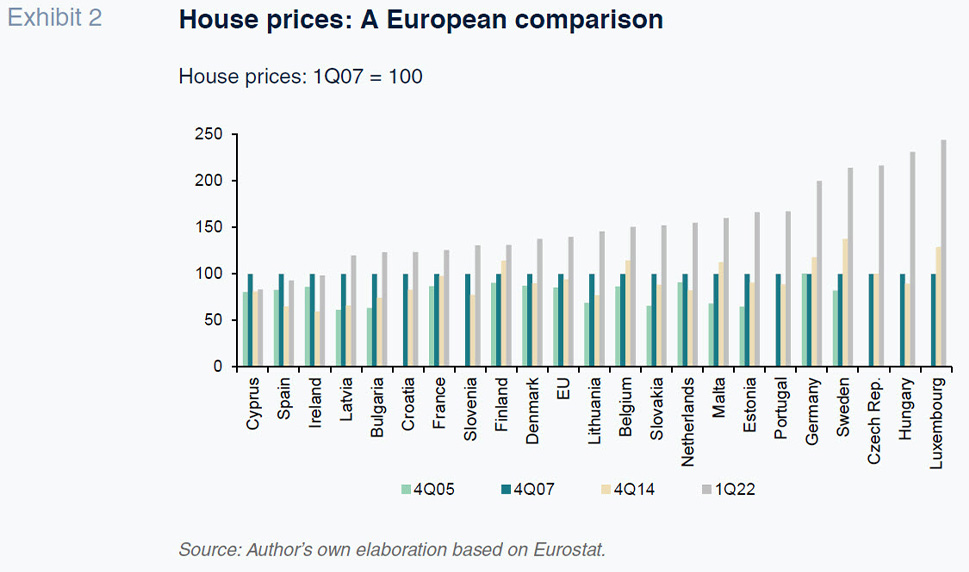

In short, despite the economic slump, the market continues to grow, although the pace of that growth may well be easing. We are therefore talking about dynamics that contrast starkly with those observed when the real estate bubble burst, evidencing the fact that this time the market is not starting from a position of widespread overvaluation. A comparison with other European countries leads to a similar conclusion (Exhibit 2). According to the European statistics office, Eurostat, the Spanish market remains below the valuation levels observed at the height of the bubble 15 years ago, while the EU market as a whole has revalued almost 40% and the German market has doubled in price. The analysis performed by the Bank for International Settlements, an organism watched closely by the market, coincides with these findings (BIS, 2022).

Housing growth has been nurtured by surplus savings and demand for safe assets in a context of inflation

The main market support factor is buyers’ perceptions that housing is a safe investment in the current context of uncertainty and inflation. Housing is a wealth-preserving investment for now, unlike liquid deposits which tend to depreciate with CPI, or financial products, such as bonds and shares, which have proven highly volatile so far this year.

The return on property investments, in addition to being relatively stable, stands at 3.7% (without factoring in valuation upside). That yield is very attractive relative to other alternatives for financial savings (take a look at the housing market indicators updated periodically on the Bank of Spain’s statistics portal). For now, that return is also higher than the related borrowing cost, thanks to favourable mortgage terms and conditions, despite monetary policy tightening. The expectation that rates will rise may even have triggered a temporary spike in purchase intent.

Elsewhere, the savings set aside during the pandemic are also driving demand for housing, offsetting the loss of purchasing power induced by current inflation. Spanish households increased their savings by €75 billion between 2020 and 2021, in clear contrast to the excessive leverage observed during the previous real estate bubble. Those surplus savings are fuelling demand for housing while helping finance investments in refurbishment which had stagnated during the lockdown. Although the savings rate fell back during the first half of this year, it remains slightly above the long-run average, evidencing households’ cautious attitude in the current climate of uncertainty.

Another plus is the fact that the job market has performed relatively well. Social Security contributors numbers have continued to increase, albeit seemingly starting to lose momentum, as the economy looks increasingly likely to slump. The jobs being created are, moreover, more stable than before the labour market reform, which may be giving buyers a sense of security.

Lastly, the supply side is reacting slowly to the growth in demand due to the paralysis of the construction sector during the lockdown and, afterwards, the onset of bottlenecks in the supply chain. According to Spain’s official statistics office, investment in housing remained 8.5% below pre-crisis levels as of the fourth quarter of 2021. The run-up in production costs in the construction sector has also eroded supply-side responsiveness to vibrant demand. Average construction material prices are 19% higher than before the pandemic (using INE data as of November, by comparison with November 2019 figures).

The shift in monetary policy: Prelude to a significant deceleration but not a market collapse

In the very near-term, we are likely to see additional increases in prices as a result of lingering underlying support factors on both the demand and supply sides.

However, the market is expected to slow as financing terms and conditions tighten, as is to be expected in light of rising interest rates. EURIBOR, the main benchmark index for the mortgage market, which was still in negative territory at the start of the year (at around -0,5%, which is close to the ECB’s deposit facility rate for the first part of the year), is currently trading at over 2%. The Funcas consensus estimate suggests that EURIBOR will rise a further half a point over the coming year (Funcas, 2022).

It is estimated that each additional point in mortgage rates increases the ratio of borrowing costs to disposable income by four percentage points – the housing affordability index. Note, however, that effect takes place gradually, as the stock of mortgages gets turned over. That estimate is based on the following equation:

A=I*(D/GDI)+(R/GDI),

where A is the Affordability index; I is the Interest rate; D is the Debt taken on to purchase a home; R is the annual loan Repayment amount and GDI is the household’s Gross Disposable Income.

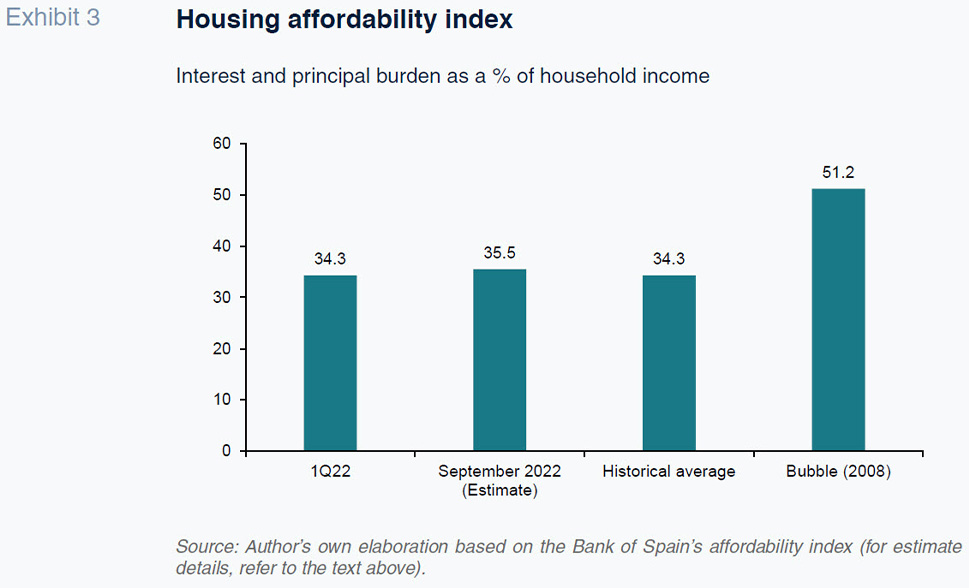

The values observed in the market today yield an estimated affordability index of 35.5%. In other words, the households that borrow money to buy their homes have to earmark over one-third of their income to the payment of interest and repayment of principal. That estimate is in turn underpinned by the following assumptions:

- The average house purchase price is equivalent to 8.5 times’ gross disposable income and the mortgage taken on by home-buyers represents 65% of the value of the property purchased. Those assumptions yield a borrowing ratio (D/GDI) of 5.5x.

- We assume the mortgage has an average life of 25 years, which, coupled with the previous estimates, leads to a ratio of R/GDI of 22.1%.

- The effective interest rate (EURIBOR plus the fees borne by the borrower), I, is 2.4%.

An increase in the interest rate of one percentage point, to 3.4%, would increase the affordability index to nearly 39.4%. That is the threshold beyond which households will begin to taper their demand for square metres or forgo mortgages either because they cannot afford to borrow or because the banks decide, under prevailing prudential regulations, not to extend them (this estimate already factors in a slight drop in demand).

The affordability index is already slightly above the long-run average (Exhibit 3), such that demand will inevitably slow as the financial burden of purchasing a home increases.

Elsewhere, the volume of bank deposits is not necessarily a good predictor of demand for housing. To sustain new home purchases, the savings accumulated in bank accounts would have to continue to increase, which is unlikely in the context of declining purchasing power.

These mitigating factors will become more tangible from 2023, when mortgage rates will fully reflect the unfolding shift in monetary policy and the supply side will have surmounted the current procurement issues (a prediction in line with others, like Montgoriol, 2022). As a result, in 2022, the current situation of surplus demand should prevail, driving faster growth in average annual prices than in household disposable income, of around 6% (by outpacing the estimated growth in households’ gross disposable income, the affordability index is already worse than before the pandemic, as we have seen).

The tightening of borrowing terms and conditions will become more tangible in 2023, weighing on demand. That, coupled with growth in supply, is likely to trigger a slowdown, with prices potentially trending in line with household disposable income. That situation would still be compatible with the banks’ prudential ratios in terms of financial burden in relation to income at the aggregate level. As a result, we do not expect non-performance to rise considerably, unless the job market takes a turn for the worse: indebted households that have borrowed at floating rates will be able to afford the higher cost of their mortgages so long as they hold on to their jobs, an eventuality that could be more likely than in the past, thanks to the Spanish economy’s overall competitive positioning, the absence of bubbles and the recent labour market reform.

In short, the housing market looks set to weaken as financing conditions tighten. However, we are not looking at a market standstill or a major increase in non-performing loans but rather a sharp slowdown of the current expansionary cycle. The main risk to this baseline scenario stems from the macroeconomic effects of the energy crisis and a worsening geopolitical context.

References

Raymond Torres. Economic Perspectives and International Economy Division, Funcas.