The impact of IFRS 16 on lease accounting

The entry into force of IFRS 16 –leases– on January 1st, 2019, changed the accounting standards on operating leases. Aiming for less bias and more uniformity, IFRS 16 stipulates that all lease agreements must be treated the same and accounted for using a traditional capitalisation formula.

Abstract: A new accounting model, IFRS 16, has established new criteria and fixed treatment for all types of leases regardless of whether the risks of ownership of the asset are transferred to the lessee. By standardising the way in which leases are accounted for, IFRS 16 seeks to ensure that reporting entities account for financing from operating leases on their balance sheets and that credit risk analysis is less biased. Some sectors -including airlines, retail and tourism/leisure- will be more affected by the new criteria than others and most market players had already taken steps to address associated challenges. Nonetheless, the broad implications of the new standard are only just beginning to be understood.

Background: A standard with uniformity as its goal

Under the current accounting model (IAS 17 and associated interpretations), reporting entities must distinguish between operating and finance leases. If all risks are transferred from the lessor to the lessee, the arrangement is considered a finance lease and reporting entities must recognise both an asset and a liability. If, on the other hand, the risks are not transferred, the lease qualifies as an operating lease and reporting entities recognise the annual lease expense as an operating expense in their statements of profit and loss.

The new accounting model (IFRS 16) sets a fixed treatment for all leases. Regardless of whether the risks of ownership of the asset are transferred to the lessee, the latter must account for the lease using a traditional capitalisation formula.

The overriding objective is to have reporting entities reflect the financing represented by operating leases on their balance sheets. Given that leases are currently treated differently depending on the contract, the credit risk analysis conducted by financial institutions and the universe of market agents may be biased.

Under the current accounting framework, leases are recognised differently in reporting entities’ financial statements. However, an analysis of the virtues of IFRS 16 and its implications raises three important issues:

- The use of operating leases is not a decision taken exclusively to enhance leverage ratios, but rather reflects the choice of a more flexible mechanism over traditional asset financing methods (Europe Economics, 2017).

- The use of operating leases is, to a significant degree, more of a sector trend than a decision taken at the individual company level.

- We do not observe asymmetries in any given sector (discussed later) — the new accounting framework will certainly modify financial statements, but the impact will be similar for all reporting entities (Europe Economics, 2017; IASB, 2016).

- Credit rating agencies, and by extension market analysts, have already taken stock of the need to adjust the financial statements of companies that have tended to rely on operating leases, to ensure that their ratings properly reflect the risk incurred by financiers seeking to fund these types of firms.

As a result, despite the change in the accounting information that will be disclosed by these reporting entities, the agents using that information were already aware of the discrepancies, so the conclusions of their risk assessments should not change substantially.

For the time being, the new standard only affects reporting entities applying the International Financial Reporting Standards (IFRS), as it has not yet been fully incorporated into the Spanish General Accounting Plan.

Lessees: The most impacted by IFRS 16

Accounting implications

What are the main accounting implications of IFRS 16 for lessees? (Lessor accounting is not set to change.)

First, the changes in how operating leases are accounted for will affect lessees’ balance sheets as well as their statements of profit and loss. In cash flow statements, the only impact will be the reclassification of the various items (as cash flows under the leases will not be altered).

- On the asset side of the balance sheet:

- Lessee reporting entities will see their assets increase by the amount of operating leases they are party to (recognised as leased or rights-of-use assets).

- This balance will be recognised at the present value of the lease payments to be made over the term of the agreement.

- Leases with a term of less than 12 months and leases of low-value assets (phones, computers, tablets, etc.) will continue to be recognised as operating expenses.

- On the liability side of the balance sheet:

- Liabilities will similarly increase by the amount of their binding obligations under their lease agreements (as if they were a financial liability).

- This change may impact associated leverage ratios (e.g., the ratio of debt/EBITDA).

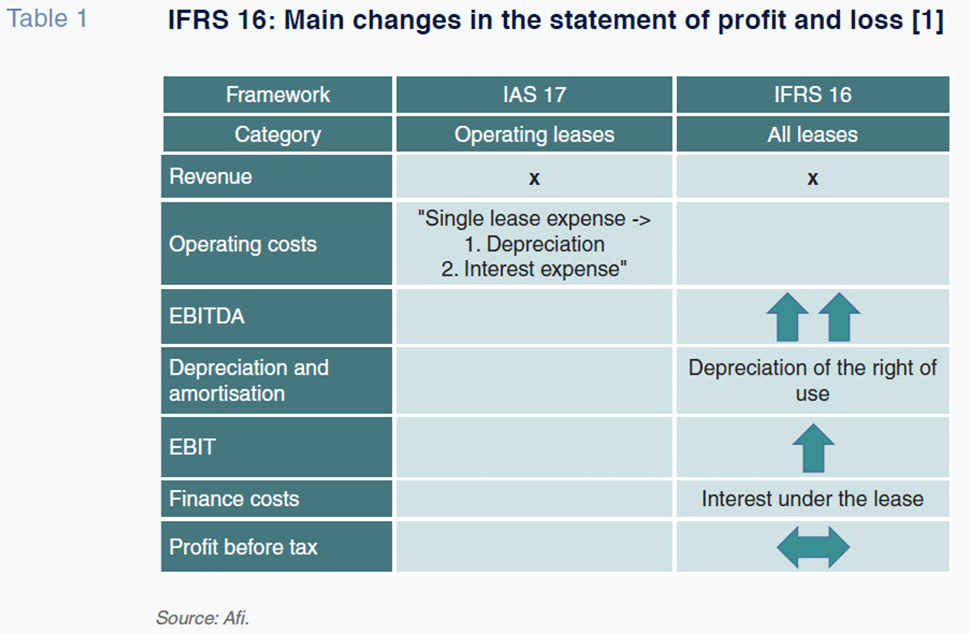

- In profit and loss (see Table 1):

- The former operating expense in respect of leases (recognised above EBITDA) will be replaced by two line items:

- Depreciation of the right to use the asset (presented below EBITDA); and,

- Lease interest expense, which, given that it is a finance expense, will be recognised below operating profit (EBIT).

- As a result, IFRS 16 will imply an increase in reported operating profit (EBITDA and EBIT), as the lease charges (representing the financing component of the agreement) will be moved below these line items.

Measurement of lease agreements: Key issues to keep in mind

The key variables determining the amount at which operating leases are recognised for accounting purposes are:

- The lease term;

- The rate of interest to be used for discounting/measurement purposes; and,

- Any options in the agreement.

Term

The lease term is defined as the non-cancellable period of a lease, together with the periods covered by an option to extend or terminate the lease, depending on the probability of exercising those options.

The term is not, therefore, an objective variable. Based on this definition, a lessor’s past practice regarding the period over which it has typically used particular types of assets (whether leased or owned), and its economic reasons for doing so, may provide information that is helpful in assessing the lease term.

It is important to stress that although the standard stipulates that leases with a term of under 12 months continue to be treated as operating expenses, there are two exceptions:

- The shorter the non-cancellable period of a lease, the higher the probability of renewing due to the costs of finding a replacement asset; and,

- A related factor is the importance of the underlying asset to the lessee’s operations: the unique or strategic nature of these assets would make it very difficult to justify the use of very short lease terms.

Interest rate used for measurement purposes

Reporting entities can use one of two interest rates for lease recognition purposes:

- The interest rate implicit in the lease: the rate of interest that causes the present value of the lease payments and the unguaranteed residual value to equal the sum of the fair value of the underlying asset and any initial direct costs of the lessor.

- The lessee’s incremental borrowing rate (mandatory for existing leases on the date of first-time application of IFRS 16): the rate of interest that a lessee would have to pay to borrow over a similar term, and with similar security, the funds necessary to obtain an asset of similar value in a similar economic environment.

In practice, the implicit rate tends not to be observable, so it is likely that reporting entities will resort to using their incremental borrowing costs to discount their leases to present value.

The interest rate is a more objective variable than the lease term, but as the former is conditioned by the latter, the failure to model realistic terms could lead to measurement bias.

Lease term options

In determining the lease term and assessing the length of the non-cancellable period of a lease, an entity shall apply the definition of a contract and determine the period for which the contract is enforceable.

A lease is no longer enforceable when the lessee and the lessor each has the right to terminate the lease without permission from the other party with no more than an insignificant penalty.

Lease termination options come in several forms:

- Only the lessor has the option to terminate the lease: the lease term will include the non-cancellable period and the period covered by the option.

- Only the lessee has the option to terminate the lease: the lease term will be shortened by the option period depending on the probability that the option will be exercised.

- Both the lessor and the lessee have the option to terminate the lease: in this event, it will be assumed there is no obligation to extend the lease agreement, and therefore the lease term coincides with the non-cancellable period.

Implications for risk and valuation metrics

In terms of analysing the creditworthiness of a company, the most significant changes anticipated are:

- Less financial autonomy for reporting entities, as the percentage of third-party borrowings over total assets will increase;

- Changes in the amounts of EBITDA and EBIT reported; (IASB, 2016); and,

- Changes in leverage ratios (net debt/EBITDA), the direction of which will depend on borrowing changes associated with the leases recognised and the proportionate reduction in operating expenses in the statement of profit and loss. Because this ratio tends to be part of the standard covenants included in borrowing agreements, it will be important to ensure there are no covenant breaches as a result of these changes.

There may also be changes in the valuation metrics commonly used in the markets, such as company valuations that rely on earnings performance. In share purchase agreements, in which a valuation multiple benchmarked to EBITDA was negotiated before IFRS 16 came into effect, the changes implied by the new standard effectively imply an increase in business valuations. It is important to factor these considerations into ongoing M and A negotiations to minimise the risk of prices being paid down the line that do not reflect the current business reality.

Sectors most affected and implications for risk analysis

Sectors most affected

Three sectors will be more exposed to the new accounting criteria: airlines, retail and tourism/leisure. Each of these sectors have traditionally used operating leases as a key tool for configuring operating assets, and the new rules will lead to the recognition of new borrowings and assets on their balance sheets.

Based on global estimates by the IASB, the weight of operating leases as a percentage of total assets stands at over 20 percent in these three sectors. Other sectors, such as telecommunications, energy and media, are exposed to operating leases to a lesser degree (about five percent of total assets) (see Exhibit 1).

It is likely that the biggest changes to classic credit risk assessment ratios will be concentrated in these three sectors, although companies in other sectors will logically also be affected by IFRS 16.

Implications for risk assessment

Rating agencies, and the credit analyst community in general, had already formulated procedures over the years for adjusting the information provided in companies’ financial statements to properly reflect the risk posed by trading their securities or funding them. Those methodologies are not exactly the same as those proposed in IFRS 16.

The approach taken by the rating agencies has consisted of one of two options:

- Determining the present value of the company’s leases using the minimum lease instalments payable, subject to a cap (set as a multiple of lease payments); or,

- Applying a sector-appropriate multiple to the lease payments made by the company.

These adjustments, which are analytical (the agencies do not question the veracity of the financial disclosures), have been made across the board regardless of the specific accounting standards applied (US GAAP or IFRS). The multiples and assumptions used to measure leases have been fine-tuned over time to factor in changes in the economic environment, as well as the risks to which various sectors are exposed.

Beyond the realm of the rating agencies, several surveys of financial sector professionals have found that it is common to make adjustments when companies use operating leases without distinguishing between company size or sector (Europe Economics, 2017).

For all these reasons, the introduction of IFRS 16 should not impact the credit ratings of affected companies nor the conclusions drawn about the company’s credit risk, as all operating leases have been treated as incremental borrowings, altering the snapshot directly observable from the financial statements.

However, the subjective nature of the new accounting standard’s definition of the lease term (and, by definition, the discount rate applicable) could trigger discrepancies in the analytical adjustments currently performed, prompting asymmetries in the conclusions drawn from a company’s financial disclosures.

Assessment of the new standard

The need for IFRS 16

Companies use operating leases not only for reasons related to their leverage ratios, but because they are flexible. If the use of operating leases can be considered a sector-specific practice, did the criteria really need to change when all market players were already aware of the need to adjust companies’ financial disclosures to properly reflect credit risk (regardless of the formula used to finance their assets)?

Greater subjectivity in formulating financial statements

The measurement of leases for accounting purposes —contracts that are not traded on an organised market— involves a significant amount of subjectivity. The level of discretion allowed in determining the lease term, and the knock-on effect on the discount rate, could mean that financial statements will actually fail to provide reliable information.

It is vital that reporting entities select measurement assumptions aligned with their business realities and not criteria designed to minimise the impact on the financial statement. The probability that reporting entities will provide biased information (possibly inconsistent with the risk metrics used in the financial industry to value lease agreements) cannot be dismissed, possibly impeding the interpretation of the information companies publish.

Valuation guidelines

In practice, an asset is not financed completely by borrowings. Therefore, the financing cost or incremental borrowing cost to be applied must, to a degree, factor in the contribution of a company’s own funds that any financier would insist on. As a result, the cost of debt or incremental borrowing cost should end up at an intermediate point between the company’s cost of senior debt and its cost of equity or subordinated debt.

However, IFRS 16 does not consider the use of capital structure-weighted costs. This is a deviation from the risk assessment exercises that any financier would perform, and casts a significant shadow over whether the new accounting standard can create more standardised financial disclosures.

Notes

The arrows denote changes in the corresponding heading with respect to the accounting treatment under IAS 17.

References

EUROPE ECONOMICS (2017), “Ex ante Impact Assessment of IFRS 16,” February.

IASB (2016), “Effects Analysis. International Financial Reporting Standard: IFRS 16. Leases,” January.

Pablo Guijarro and Alexandra Cortés. A.F.I. – Analistas Financieros Internacionales, S.A.