Spain’s budget: Challenges for 2024

While at first glance Spain’s 2023 fiscal performance appears favorable, lack of adjustment on the structural deficit paints a less optimistic picture going forward. Continued structural fiscal adjustment will be needed to improve the probability of compliance with the new EU fiscal deficit targets.

Abstract: Delivery of the targeted deficit below 4% for 2023 is plausible, thanks to the healthy momentum in tax collection boosted by higher than expected growth in gross domestic product (GDP). At first glance, the anticipated outcome for 2023 appears favourable and in line with expectations, with last year’s deficit around 1% of GDP lower than that of 2022. However, the result is less favourable if we take into consideration the scant adjustment in the structural deficit, which in 2023 will exceed headline deficit figures. Domestic political tensions first delayed the 2024 budget process and ultimately resulted in the draft budget being pulled in order to begin preparing the 2025 budget. Despite a likely increase in tax revenues as a result of the upside in GDP growth once again, there is no guarantee that Spain will escape the EU’s Excessive Deficit Procedure in 2024, which, under the new rules, will continue to be activated in the event of a deficit over 3% of GDP. For this reason, fiscal decisions altering the 2023 extended budget in the next months should be compatible with a significant reduction of the structural deficit to advance toward compliance with the EU’s deficit and debt targets.

Forecasts for 2023 [1]

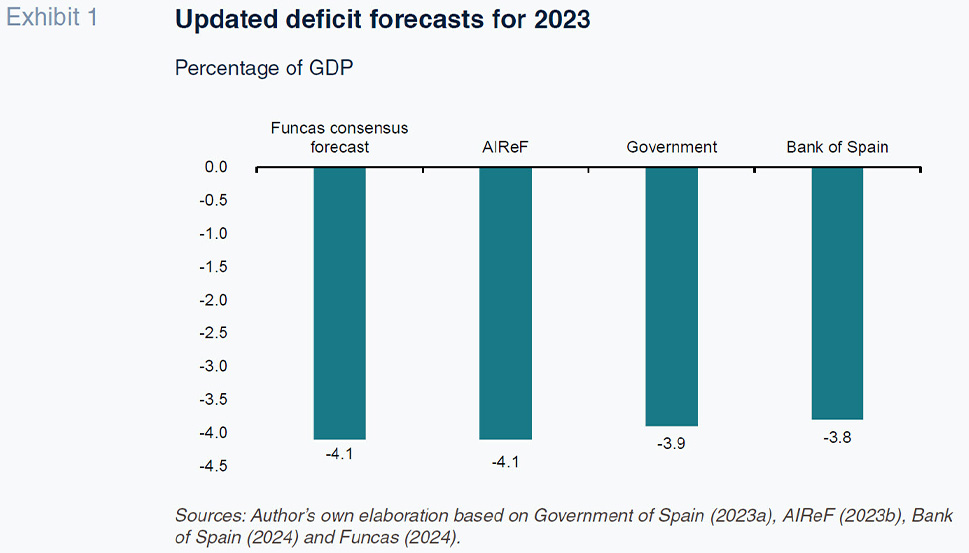

At the time of writing, the definitive figures for 2023 were not yet available. Exhibit 1 provides the deficit forecasts of the Spanish government, which have not changed during the past year, the Bank of Spain, AIReF and Funcas (consensus). They all fall within a range of 3.8% to 4.1%. Therefore, delivery of the targeted deficit of 3.9% is plausible, thanks to healthy momentum in revenue, in turn facilitated by growth in gross domestic product (GDP) that exceeded all expectations. The growth in tax receipts reflected the impact of the response to the inflation crisis which began during the last quarter of 2021. The deficit will be around one percentage point of GDP lower this year than in 2022 (4.8%). On paper, that looks like a good result and in line with expectations (Lago-Peñas, 2022).

The assessment is less encouraging if we look at the structural component of the observed deficit. According to the calculations included by the Spanish government in the budgetary plan sent to the European Commission in October of last year (Government of Spain, 2023b), that deficit component will fall by just 0.3pp, from 4.5% to 4.2%. Therefore, two thirds of the improvement will be attributable to the business cycle. In 2023, the structural deficit will exceed the headline deficit.

2025 budget pending

The snap election in July 2023 and the protracted investiture process delayed the process of preparing the general state budget for 2024 (2024 GSB), so this year began with the rollover of the 2023 GSB and a Draft Budgetary Plan for 2024 (Government of Spain, 2023b). The latter document assumed no change in current policies and no extension of the anti-inflation policies in place in 2023. It did, however, factor in the increase in pension expenditure and the increase in the remuneration of public employees. Given that the accumulated cost of those anti-inflation compensation measures was equivalent to close to 1% of GDP in 2023, their elimination was expected to deliver a substantial decrease in the structural deficit, from 4.2% to 3.4%. In parallel, the improvement in the cyclical component was expected to bring the overall deficit down towards 3%. That is of particular importance in light of the reinstatement of the fiscal rules, a matter discussed in detail at the end of this paper.

However, in January 2024, the Congress of Deputies decreed the partial maintenance of this package of anti-crisis measures, so modifying these calculations. According to estimates by García-Arenas (2024), the temporary extension of the VAT and excise duty cuts, the transport assistance and the financing for household natural gas discounts will be equivalent to approximately 0.3pp of GDP. Although it is probable that tax revenue will increase as a result of upside in GDP growth, the fact of not having a new budget for 2024 means that there are no new discretional measures to guarantee that Spain will be saved from the Excessive Deficit Procedure which, under the new rules, will continue to be activated in the event of deficits in excess of 3%.

For the reasons given above, coupled with the limits implied by the lack of a budget tailored for the commitments and objectives of the government at the start of the legislature, approval of the 2024 GSB was considered a priority.

The events of February made it clear that it will be hard to get backing for budget stability targets in a Senate in which the majority is in the hands of the main opposition party (Partido Popular). The government refused to accept the demands made by Partido Popular: deflation of personal income tax, reduced VAT on electricity, gas, meat, fish and canned foods, elimination of the tax on electricity generation and creation of a fund to finance regional spending on health, education, and social policies. As a result, the stability targets were voted down twice, for the second time on 6 March, leading to an unprecedented situation for which prevailing legislation has no clear solution. Under the scope of a report issued by the state’s legal counsel, the government opted to sidestep the double veto in the upper house by returning to the targets established in the Stability Programme Update sent to Brussels in March 2023. [2]

That strategy was abruptly interrupted on 13 March when the regional government of Catalonia called a snap election, to which the central government immediately responded that it would no longer seek to approve a budget for 2024. Instead, the Ministry plans to start to work on the 2025 GSB soon. That decision has three key consequences: it makes it harder to implement the coalition agreement reached between PSOE and Sumar; it complicates the materialisation of the investiture agreements that require budget funding; and it further entrenches fiscal policy inertia in Spain.

The government finds itself faced with a complex sudoku which will require a lot of skill to solve. To ensure its stability and the support of its allies in Congress, the government will be forced to resort to decrees to cover increases in public spending. Increase that will come on top of the cost of partially extending the above-mentioned package of anti-crisis measures and other initiatives not contemplated in the Draft Budgetary Plan, specifically including the reimbursement of corporate income tax (as a result of the Constitutional Court ruling STC 11/2024 of 18 January) [3] and the personal income tax adjustment passed by the Cabinet on 6 February 2024 so that the lowest income brackets do not become taxable in the wake of the increase in the minimum wage, which, according to the Ministry of Finance, could cost nearly 0.1pp of GDP (1.39 billion euros). Lastly, the extension in time of the temporary windfall taxes on energy companies, banks and financial institutions and the so-called solidarity tax on large fortunes via Royal Decree-Law 8/2023 of 27 December 2023 does not affect the revenue currently forecast for 2024 in the Budgetary Plan but rather that of 2025. [4]

The new fiscal rules and upcoming tightening

Spain’s budget predicament for the rest of the decade is challenging. Not only to comply with the European fiscal governance framework, but also to keep the debt service burden under control so as to have a financial buffer in the event of future shocks and preserve a credit reputation to shield it from financial storms affecting sovereign debt.

The new fiscal rules agreed at the Ecofin Council summit on 20 December 2023 and endorsed in February by the European Parliament, Commission and Council following small modifications, provide more flexibility than the previous rules. However, Spain’s current fiscal metrics leave it at a distance from complying with the quantitative targets for its public deficit and debt as a percentage of GDP. Reducing the structural budget deficit is therefore imperative. Specifically, Spain needs to reduce its structural deficit by half a percentage point per annum until the headline deficit falls below 3% of GDP and by 0.4 percentage points from when it crosses that threshold until it reaches 1.5%. It would take a fiscal consolidation plan that looks seven years ahead to enable a meaningful reduction in the pace of correction, approximately 0.25 percentage points per annum.

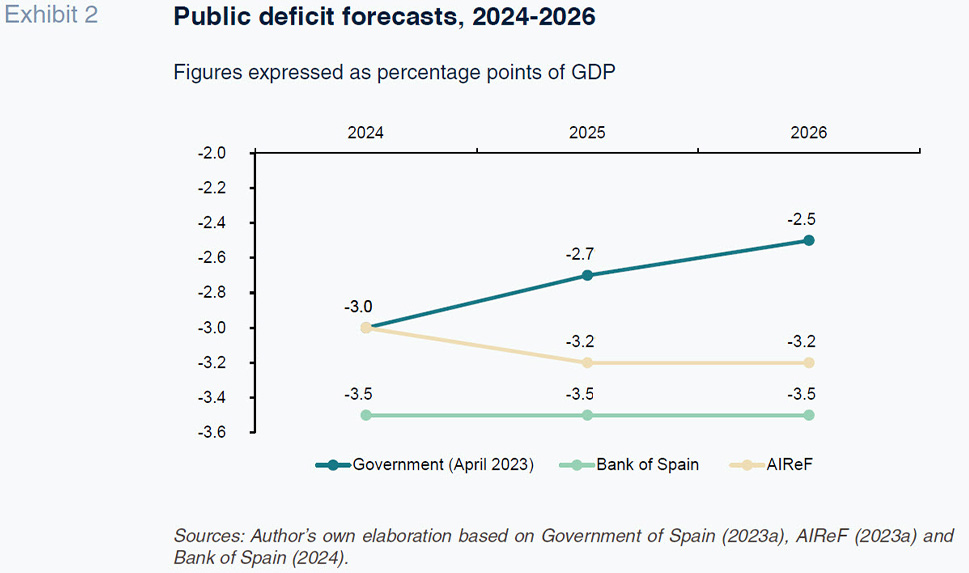

Exhibit 2 depicts the fiscal consolidation pathways estimated for 2024-2026 by the government, Bank of Spain and AIReF. Even assuming that Spain can reduce its deficit to under 3% in 2024, the reductions forecast for 2025 and 2026 may prove insufficient. First of all, because AIReF and the Bank of Spain believe that the deficit could rise back above the 3% mark. Secondly, because the government itself is only forecasting a reduction of 0.3 and 0.2 percentage points in the headline deficit in 2025 and 2026, respectively, and of just 0.2 percentage points in the structural deficit (Government of Spain, 2023a). Therefore, even if Spain manages to negotiate a seven-year plan, the reduction in the structural deficit would fall somewhat short of what will be demanded. Thirdly, because the new rules are more stringent around the public debt dimension. AIReF’s calculations (2024) use the European Commission’s prevailing methodology to monitor the sustainability of Spain’s public debt and its requirements under the incoming rules. The combination of deterministic and stochastic projections indicates the need to reduce public debt by 0.64 points of GDP per annum between 2025-2028, for a cumulative reduction of 2.56 points, to meet several requirements under the new framework. That figure could be reduced to 0.36pp if the government tries to take advantage of the possibility of extending the adjustment period beyond seven years (2025-2031).

The simulations performed by Lorenzo, Martínez and Pérez (2023) provide fresh insight into the issue. They estimate the structural public deficit reduction needed for Spain to be able to reduce its public debt-to-GDP ratio by 20 percentage points over a decade. That would put Spain’s public debt below 90%, a figure with new-found significance in the new European fiscal governance framework by way of interim target on the path towards the 60% threshold. In their baseline scenario, in which the fiscal multiplier stays within the median range estimated in economic literature, Spain would need to go from its current structural deficit of around 4% to very close to zero in structural terms. Once again, that would require annual fiscal consolidation of 0.4 percentage points.

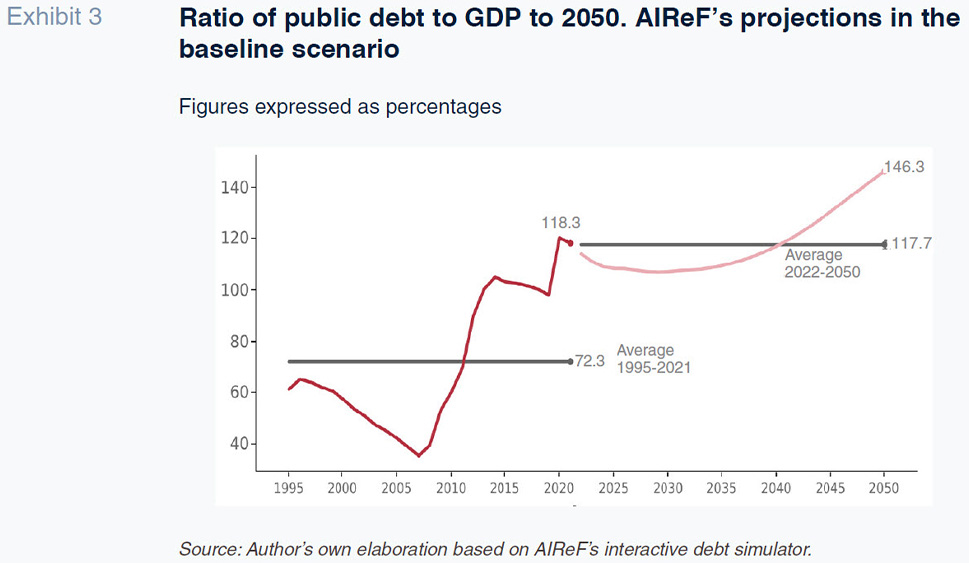

Exhibit 3 illustrates the potential consequence of not tackling fiscal consolidation. With no change in policy, the debt to GDP ratio would become entrenched at over 100%, increasing sharply in the 2040s, which is when Spain’s baby boomers are set to retire. Moreover, these simulations do not model the potential impact on Spain’s public finances of factors such as climate change and the energy transition. The impact of extreme weather events such as droughts, coastal flooding, river bank flooding and wind storms is expected to be particularly intense in Spain by comparison with the EU-27 average. Some of the projections published by the European Commission and IMF show that by 2032, the cumulative impact of climate change and energy transition on Spain’s public debt ratio could imply an increase in the country’s public debt of over five points of GDP (Lago Peñas, 2024).

Without question, management of the fiscal consolidation challenge in a proactive and sustainable manner will come up against economic policy issues, aggravated by the fatigue that could come from having to keep the effort up over time. The combination of spending and revenue measures is a crucial policy decision which should be articulated around three fundamental axes of change. The first is to fully embrace a culture of public spending assessment and consequential decision-making. The second is to comprehensively reform the Spanish taxation system to deliver more efficient and just collection irrespective of the targeted ratio of revenue to GDP. The third is to embark on an educational drive to convince Spanish citizens of the importance of solid public finances.

With respect to this third line of initiative, the work done by Lago-Peñas (2022) shows that the citizens that acknowledge greatest interest in economic affairs are more aware of the public deficit issue in Spain and the need to address it, reinforcing the idea that outreach and engagement on this topic is worthwhile. Elsewhere, citizens’ political ideology colours their preferences about the composition of the fiscal adjustments required: those that lean more to the left are more inclined to increase taxes than cut spending than those that lean more to the right. Econometric estimates show that left-wing party voters tend to perceive the public deficit as a less serious issue. That suggests it might be worth insisting on the message that healthy public finances are essential so that the public sector can intervene actively in the event of an unexpected shock and so that an excessive debt service burden does not absorb funds that could otherwise be used to improve public services.

Notes

The author would like to thank Diego Martínez López for his feedback on an earlier version of this paper.

Literally, the report concludes that: “due to the lack of approval, in accordance with internal legislation, of a convergence path towards budget equilibrium, the contents of the Stability Programme will be applicable, provided that it has been favorably evaluated by the Council [of the EU]”; something the latter did in the recommendations it issued in the wake of its assessment of the Stability Programme of the Kingdom of Spain last July.

Although the impact of this ruling is unclear, some provisional estimates point to a range of between 4 and 7 billion euros (El País, 12-2-2024, p. 25), some of which could materialise subsequent to 2024.

Those taxes were initially to be applied to earnings for 2022 and 2023 but effectively paid in 2023 and 2024, respectively.

References

AIREF. (2023a).

Report on the main budgetary lines of the public administrations for 2024. 26 October 2023.

www.airef.esAIREF. (2023b).

Monthly stability target monitoring. December 2023. www.airef.esAIREF. (2024).

Debt Observatory. February 2024. February 2023. www.airef.esBANK OF SPAIN. (2024).

Macroeconomic projections for the Spanish economy (2024-2026). 12 March 2024.

www.bde.esFUNCAS. (2024).

Spanish Economic Forecasts Panel. January 2024.

www.funcas.esGARCÍA-ARENAS, J. (2024). Impact on the national accounts of the partial extension of anti-inflation measures in 2024. 8 February 2024.

www.caixabankresearch.comGOVERMENT OF SPAIN. (2023a).

Stability Programme Update, 2023 – 2026. Kingdom of Spain. 28 April 2023.

www.hacienda.gob.esGOVERMENT OF SPAIN. (2023b).

Draft Budgetary Plan for 2024. Kingdom of Spain. 15 October 2023.

www.hacienda.gob.esLAGO PEÑAS, S. (2022).

Déficit y consolidación fiscal en España: ¿Qué opinan los ciudadanos? [Deficit and fiscal consolidation in Spain: What do citizens think?]. Funcas Technical Note.

www.funcas.esLAGO PEÑAS, S. (2024).

La dinámica de la deuda pública en España: Pasado, presente y futuro [Public debt dynamics in Spain: Past, present and future]. Funcas Technical Note.

www.funcas.esLORENZO, R., MARTÍNEZ, D. and PÉREZ, J. (2023). La deuda pública en España: escenarios de evolución y condicionantes [Public debt in Spain: Scenarios and limiting factors].

Papeles de Economía Española, 175.

Santiago Lago Peñas. Professor of Applied Economics at Vigo University and Senior Researcher at Funcas