Banks’ market value in times of COVID-19

Although COVID-19 hit banks’ share prices hard across the globe, the effect was particularly acute in Europe. However, analysis shows that those banks that have recognised the highest provisions have outperformed during the recovery period since the market fell to its lowest point in March.

Abstract: COVID-19 issued a substantial blow to banks’ share prices across the globe but especially in Europe. Notably, this occurred in the context of a three-year-long sector valuation slump despite an improvement in banks’ capital and liquidity levels. Analysis of banks’ equity prices and COVID-19 incidents shows the intensity of the equity market contractions sustained by the national banking systems is somewhat correlated with the incidence of the pandemic. Looking more deeply at the impact, data show these market corrections have sharply eroded banks’ price-to-book ratios. However, the industry has broadly seen a recovery since the lows of March, due to fiscal and monetary stimulus, the possibility of a vaccine, and effectiveness of lockdown measurements. Interestingly, those banks that have made the greatest loss provisions have also been the institutions to perform most strongly during the recovery.

Background

The lockdown introduced to curb the COVID-19 pandemic contributed to sharp declines in banks’ share prices during the initial weeks of crisis. While the effect was global, it was particularly acute among European banks. This occurred in the context of a three-year-long sector valuation slump, shaped by extremely low business growth and ultra-low and even negative rates, which combined have compressed banks’ return on equity (ROE). (Berges, Pelayo and Rojas, 2018).

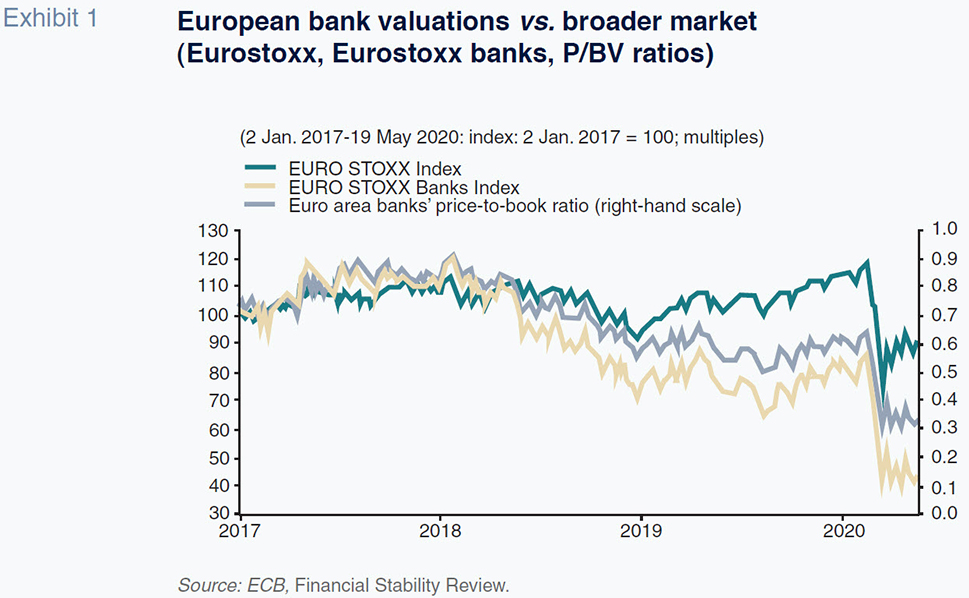

Exhibit 1 highlights the underperformance of the Eurostoxx Banks Index compared to the broader Eurostoxx over the last three years. From the start of 2017, the general index gained 20% while the banks index fell by the same amount over the three-year period. Notably, this decline excludes the adverse impact of COVID-19, which accentuated the downward trend.

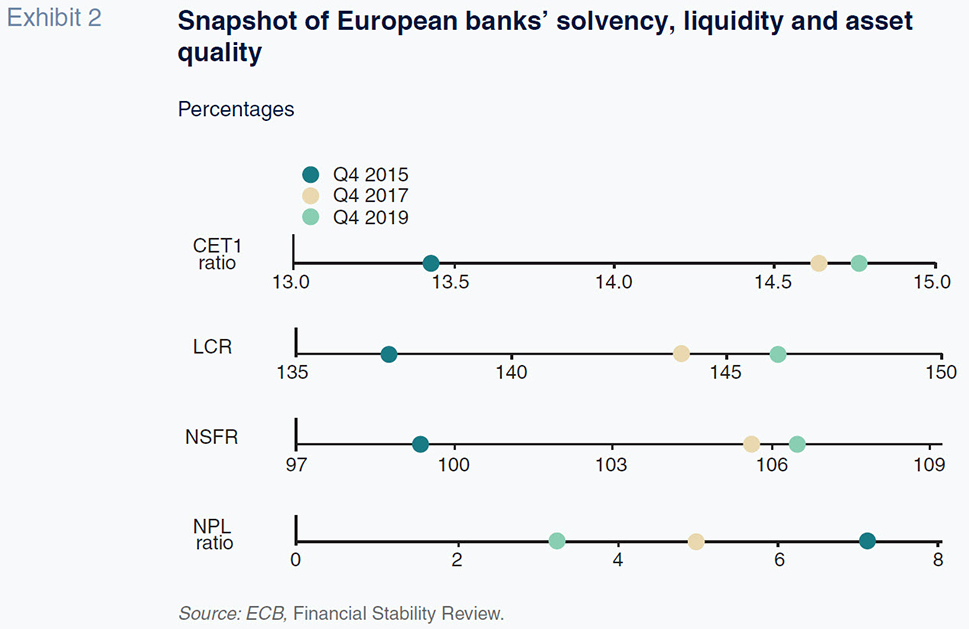

The sector’s negative stock market performance contrasts sharply with the improvement observed in its key metrics, as noted by the ECB in its recent

Financial Stability Review. From 2017 to 2020, the eurozone’s banks have exhibited a clear improvement in their capital and liquidity levels as well as the quality of their assets. This has provided the sector with a significant buffer for tackling the inevitable slump in economic activity due to COVID-19.

Pandemic response measures sent the markets into free-fall

It was against this backdrop of sector devaluation and the banks’ reinforcement of their capital and liquidity buffers that the COVID-19 crisis emerged. The health crisis was unprecedented and marked by significant uncertainty as to its intensity and duration. This, coupled with the pro-cyclical nature of the banking business, has left banks particularly vulnerable to the adverse economic ramifications of COVID-19, notwithstanding the buffers built up in recent years.

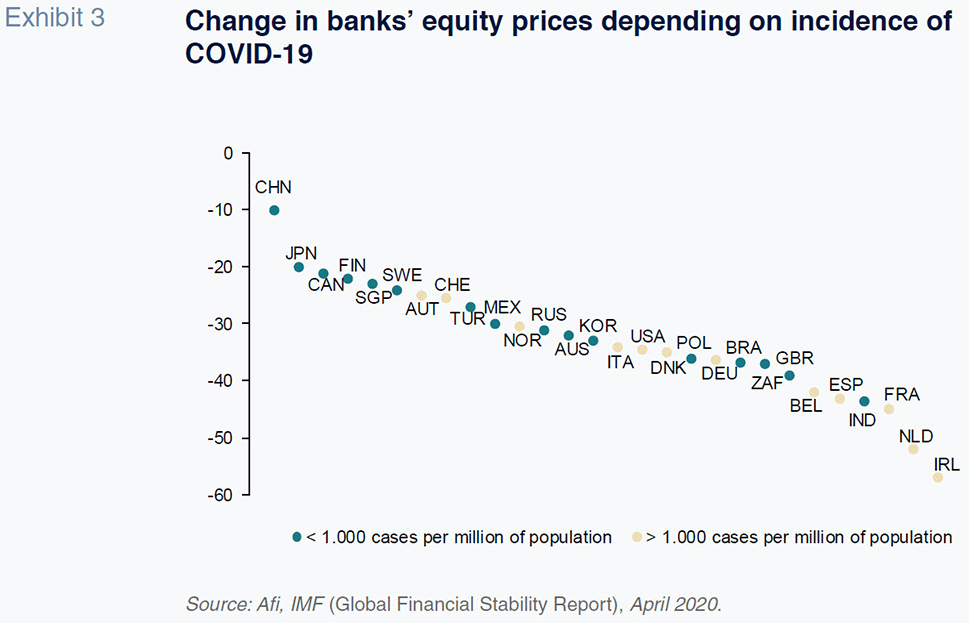

That vulnerability is already evident in equity price data highlighted in Exhibit 3. It shows how the intensity of the equity market contractions sustained by the national banking systems is somewhat correlated with the incidence of the pandemic. While differences in infection rates and investor behaviour suggest these data should be analysed with caution, the data do indicate a global contraction in banks’ share prices occurred in response to COVID-19 and the lockdown measures adopted to combat it.

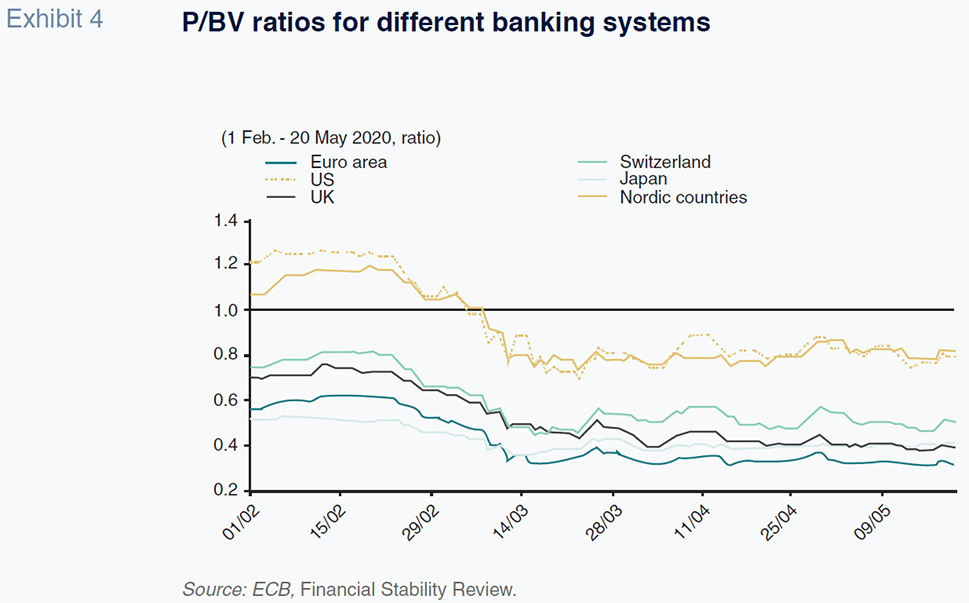

The market correction has sharply eroded the banks’ valuation measurements, specifically their price-to-book (P/BV) ratios. As shown in Exhibit 4, the crisis triggered by the pandemic has taken an even greater toll on the European banks, whose valuations were already depressed, with their stocks trading at less than book value across the board. However, the exhibit allows us to make an additional observation. Since the middle of March, which is when the coronavirus was declared a global pandemic, the US and Scandinavian (Denmark, Norway and Sweden) banking systems, the only ones that had been trading at a P/BV ratio of more than one, have seen their valuations dip below that threshold. Consequently, at present, all the world’s banking systems are trading below book value.

Banking sector staging a more pronounced recovery than other sectors

The last three months have been marked by several changes in equity investor sentiment (the so-called risk-on and risk-off phases). This has clear-cut implications for the banks’ share prices, which are always more volatile than the market as a whole (the banks’ betas range between 1.4 and 1.6). The sharp corrections sustained in March gave way to a strong recovery in April, only to be followed by a fresh rout during the first half of May. Since then, banks’ share prices have been recovering healthily.

The strong rebound observed between March and the start of June can be attributed primarily to three factors:

- The first is the arsenal of economic policies rolled out to combat the adverse macroeconomic shock caused by the pandemic. In terms of monetary policy, the main central banks around the world have acted swiftly (unlike in previous crises), deploying expansionary monetary policies including conventional (rate cuts in the US and Europe) and unconventional measures, thus preventing the onset of a liquidity crisis that could hurt the flow of credit to the real economy. In terms of fiscal policy, the vast majority of governments have passed fiscal stimulus measures (of varying nature and intensity) with the aim of mitigating the adverse consequences of the crisis. In Europe, there has been decisive progress on shaping a pan-European recovery plan which, for the first time, contemplates grants and not just loans.

- The second factor relates to the progress made on a vaccine for the virus, decreasing the probability priced in by the market that new outbreaks will shut the economy down again.

- The third factor is the proven positive impact of the lockdown measures in controlling the pandemic in much of the world. That success is paving the way for an accelerated transition towards a ‘new normalcy’ in the main economies. While this is good news for the stock markets, the risk of fresh outbreaks lingers.

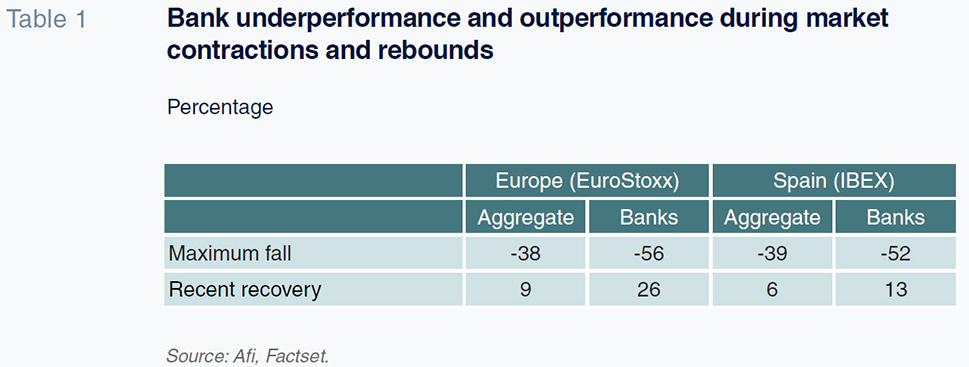

Regardless of the relative importance of each of the three factors, what is clear is that during the general stock market recovery that occurred to June, the banks outperformed the broader stock market in Spain and across Europe by about as much as they underperformed during their period of contraction.

The same holds if we break that analysis down for a sample of European banks (including Spanish banks) with the rebounds broadly as strong as the original contractions.

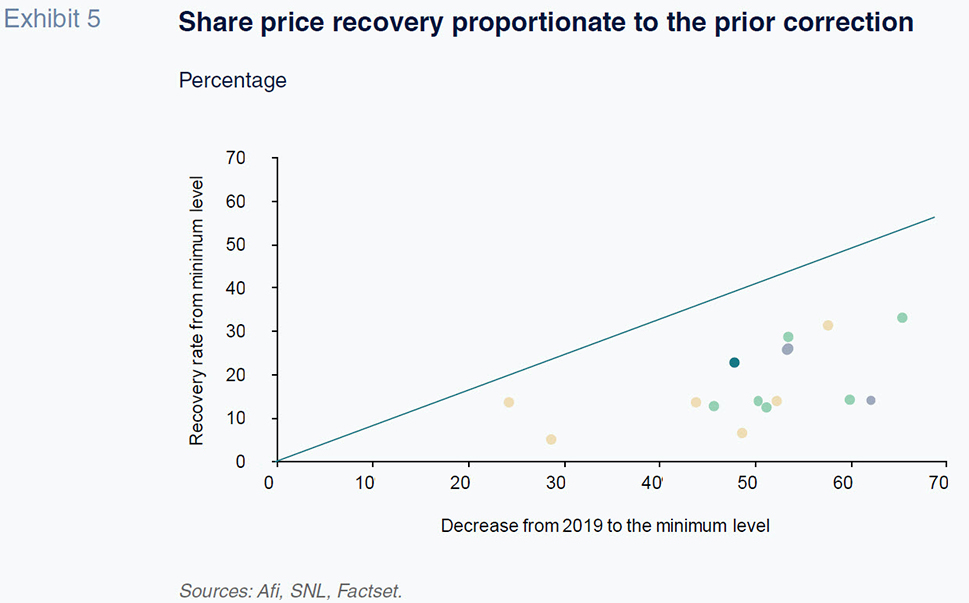

Exhibit 5 compares the maximum contractions registered in 2020 (between year-end 2019 and the height of the pandemic crisis), which range between 30% and 70% (horizontal axis), with the recovery, measured as the percentage recovery left to reach pre-crisis highs (vertical axis).

The exhibit shows how the banks that suffered the harshest share price corrections have gone on to sustain the strongest recoveries. In other words, the percentage rebound is somewhat correlated to the prior contraction, a sort of correction mechanism. However, the exhibit reveals an observation with all the dots on the scatter plot below the diagonal line. This indicates that each of the entities analysed have yet to fully recover from the share price rout caused by the pandemic.

Share price recovery and first-quarter provisioning effort

We next look at the relationship between the rates of recovery and the level of prudence exhibited by the various banks in response to the COVID-19 outbreak, with a specific focus on provisions recognised in their first-quarter 2020 financial statements.

Analysis of the banks’ first-quarter earnings presentations shows that the entities (including Spanish banks) have taken a decidedly prudent approach. Spanish banks have recognised sizeable volumes of impairment losses against their first-quarter 2020 profits. In the case of Spain, the impairment losses recognised in the first quarter of 2020 were roughly double the average recorded in the four quarters of 2019, acknowledgement that in the current context of heightened uncertainty, the traditional credit risk assessment models could fall short.

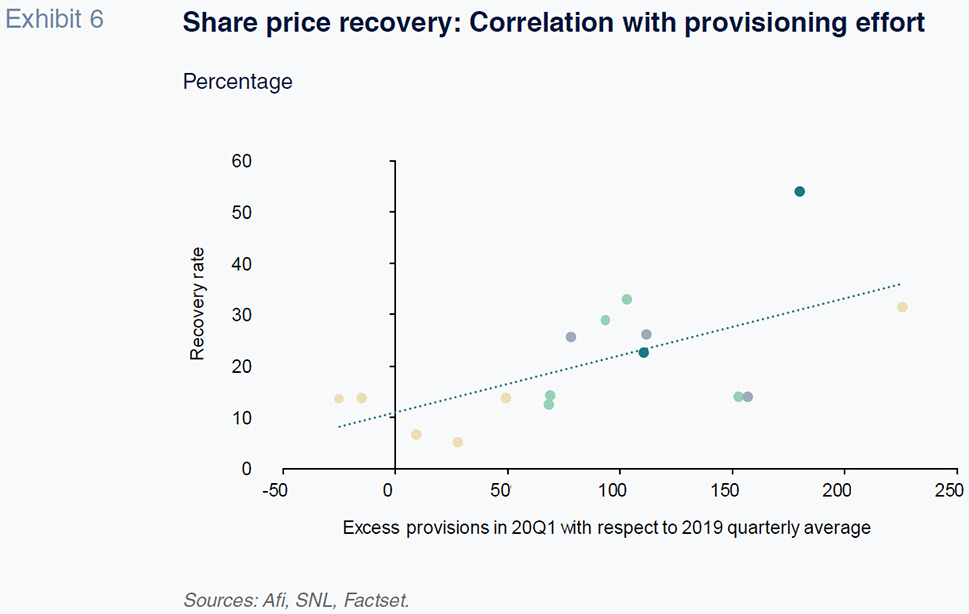

Against that backdrop, Exhibit 6 shows how the equity market has rewarded those banks that have made greater provisioning efforts. For a wide sample of European and Spanish banks, the exhibit presents: a) their percentage recovery from lows on the vertical axis; and, b) the excess, in percentage terms, of the provisions recognised in the first quarter of 2020 compared to the 2019 quarterly average on the horizontal axis.

Exhibit 6 shows there is a clear positive correlation between the volume of credit loss provisions recognised by the banks and the recovery in their share prices. The market has rewarded prudence as the banks that have recorded higher allowances have outperformed their peers.

Should this correlation continue to hold during the coming (quarterly) reporting seasons, we would see the opposite of what we witnessed during the financial crisis of 2008-2012, when the general perception was that the banks were much slower in writing their assets down for impairment than other sectors.

Conclusion

As we have shown in this paper, the equity market correction triggered by the COVID-19 crisis has hit the banking sector particularly hard. So much so that no banking system anywhere in the world is currently trading at above book value. The European banks’ extremely depressed valuation measurements have forced the supervisory authorities to ban the payment of dividends to facilitate the replenishment of capital in case they are unable to tap the equity markets.

However, expansionary monetary and fiscal policies, coupled with expectations regarding the development of a vaccine and the end of lockdown, have paved the way for the recovery since financial markets fell to their lowest point in March. The banks have outperformed the broader market during the recovery, as expected given the cyclical nature of the industry. Additionally, the recovery has been stronger among those banks whose share prices had been hit hardest by the onset of the health crisis and those institutions that recognised higher volumes of provisions against their first-quarter 2020 earnings.

References

BERGES, A., PELAYO, A. and ROJAS, F. (2018). Spanish, Eurozone and US banks: The link between market valuations and profitability.

Spanish and International Economic & Financial Outlook, Vol. 7(3), May.

ECB. (2020).

Financial Stability Review, May.

IMF. (2020).

Global Financial Stability Report, April.

Ángel Berges, Marta Alberni and Diego Aires. A.F.I. - Analistas Financieros Internacionales, S.A.